Since 2021, tokens on the DEX track have risen sharply. For example, UNI and SUSHI have increased by more than 4 times, but there are still investors who say that the value of UniSwap and SushiSwap has been underestimated.If we understand from the product, this is true.The exchange is the core product of the cryptocurrency industry, and it is also one of the products with the most mature profit model and development model. This conclusion has been proved by the development of CEX for several years. From CEX to DEX, the development experience of the trading market can make DEX products rise rapidly.

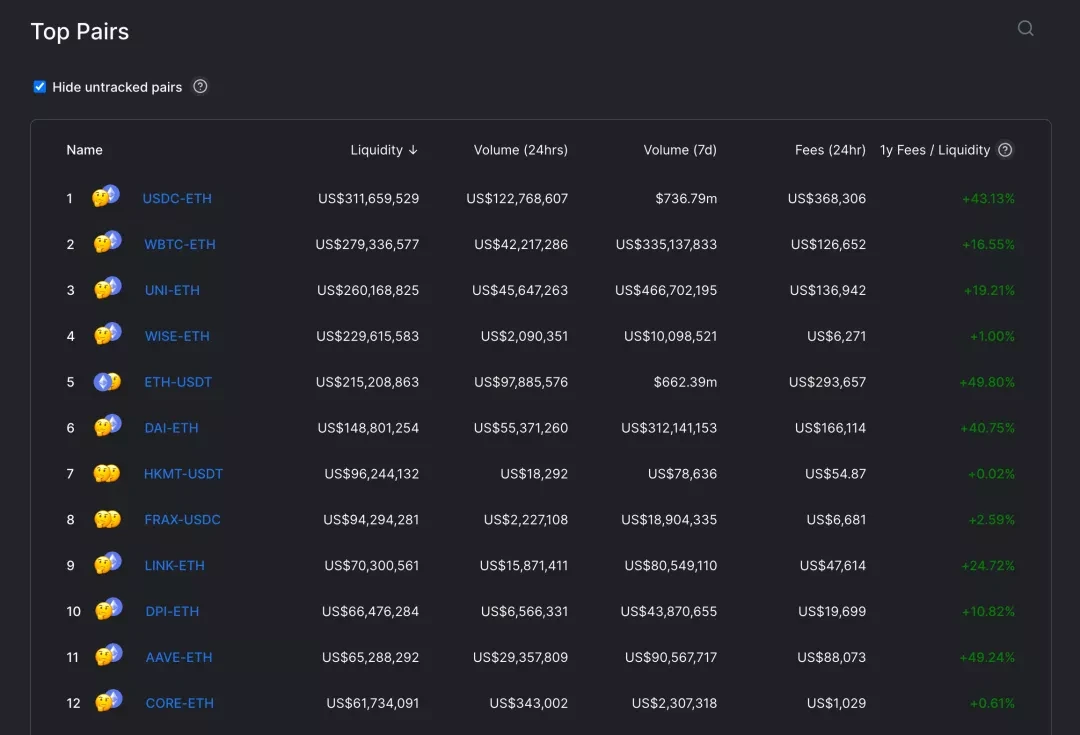

The figure above shows the top trading pairs and trading volume of UniSwapToday, we will analyze the trading market from the perspective of products and users. The goal of this article is to see where are the trading market opportunities other than UniSwap and SushiSwap?Find the long tail market first?The long tail keyword originated from search engines, because search engines can only search for a single keyword at first, and with the improvement of search technology, search engines began to have the ability to search for complex words. This complex vocabulary is called long-tail keywords. It refers to adding progressive or descriptive words before and after a single keyword to form long-tail keywords. Long-tail keywords represent the progression of user search needs.

The Long Tail Theory of Internet Search

The demand of cryptocurrency exchanges is trading, but trading represents the form, and the essential goal of users is investment, that is, the core demand is investment.Starting from this demand, investors need to find investment products on the platform, and then buy and sell them. The basic functions of DEX and CEX we have seen are all like this.A more detailed representation can be seen from the design of each trading platform.Looking at CEX from the product model, its goal of satisfying transactions is to earn daily income from handling fees and a single large amount of income such as currency listing fees. Therefore, from discovering user needs to guiding user needs, CEX will select good trading pairs to list on the exchange, subsidize trading, improve trading experience, shape trading depth, etc., all in order to let users enter the exchange and trade here for a long time.DEX is slightly different in terms of product attributes. Many DEXs in the cryptocurrency field exist in the form of open source products, and codes and protocols can be used in other products. From the perspective of product models, DEX will also form a single flow Entrance, the main earning is also the handling fee, but the apportionment of operating costs is the use of token incentives. This means that there is no direct income goal of CEX. For investors, it will be difficult to grasp the trading experience, and their trading experience is far from the standard.

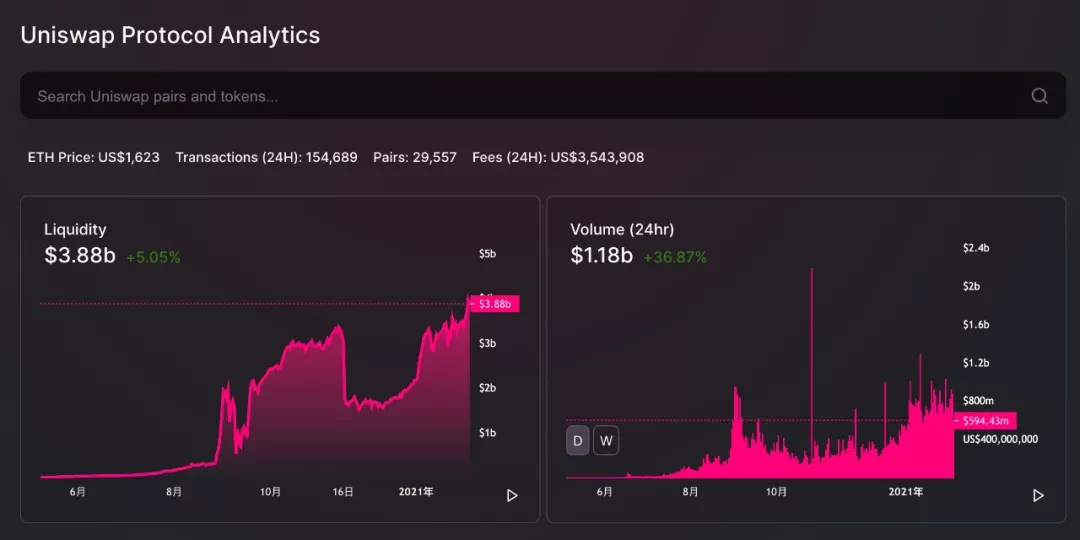

Statistics of UniSwap info

According to UniSwap info statistics, there are currently more than 29,000 UniSwap v2 trading pairs, and according to SushiSwap analysis tool data, there are about 6,600 SushiSwap pairs, which means that UniSwap and SushiSwap have become the first choice for all tokens to be listed on exchanges.The existence of such products is extremely beneficial to the cryptocurrency project side. If the cryptocurrency has a plan to land on the centralized exchange, it can first conduct the initial token sale and market value management through UniSwap.From the above existing experience, we can see two kinds of markets that find progressive demand representatives. One is the long tail market faced by UniSwap and SushiSwap. The long tail here is distinguished by assets, that is, In addition to the mainstream currencies, there are a large number of small currencies that have transaction needs. This is the long tail defined by the cryptocurrency category, and it is a progressive demand.Find the progressive law of demand for DEX

Let’s divide the upgrade path of investors’ demand, and then we can find out the progressive demand of DEX according to the map.Starting from the trading needs of investors, the following rules can be found:1. Basic spot trading (no targeted selection of trading pairs)2. Upgrade spot trading (targeted selection of trading pairs)3. Advanced spot trading (targeted selection of trading pairs, required transaction fees, minimal losses)4. Risky spot trading (targeted selection of trading pairs, increased leverage)5. Ordinary contract transactions (leveraged, long, short, settlement at any time)6. Optimize contract transactions (targeted trading pairs, strategic long and short, and require immediacy)7. Other derivatives transactions (targeted trading pairs)The above classification is considered from the demand side. As the demand increases, more control over the detailed process is required.For example, UniSwap, balancer and other exchanges with basic swap functions, users do not require specific price calculation accuracy for prices, and most retail investors will follow the trading pairs with large gains and good trends to trade.If the demand for basic transactions is upgraded, the requirements for transaction details will be increased, such as requiring low gas fees, better transaction pairs, and strict control over transaction prices. Raising the requirements again, you can also require the use of margins to increase leverage to increase returns.

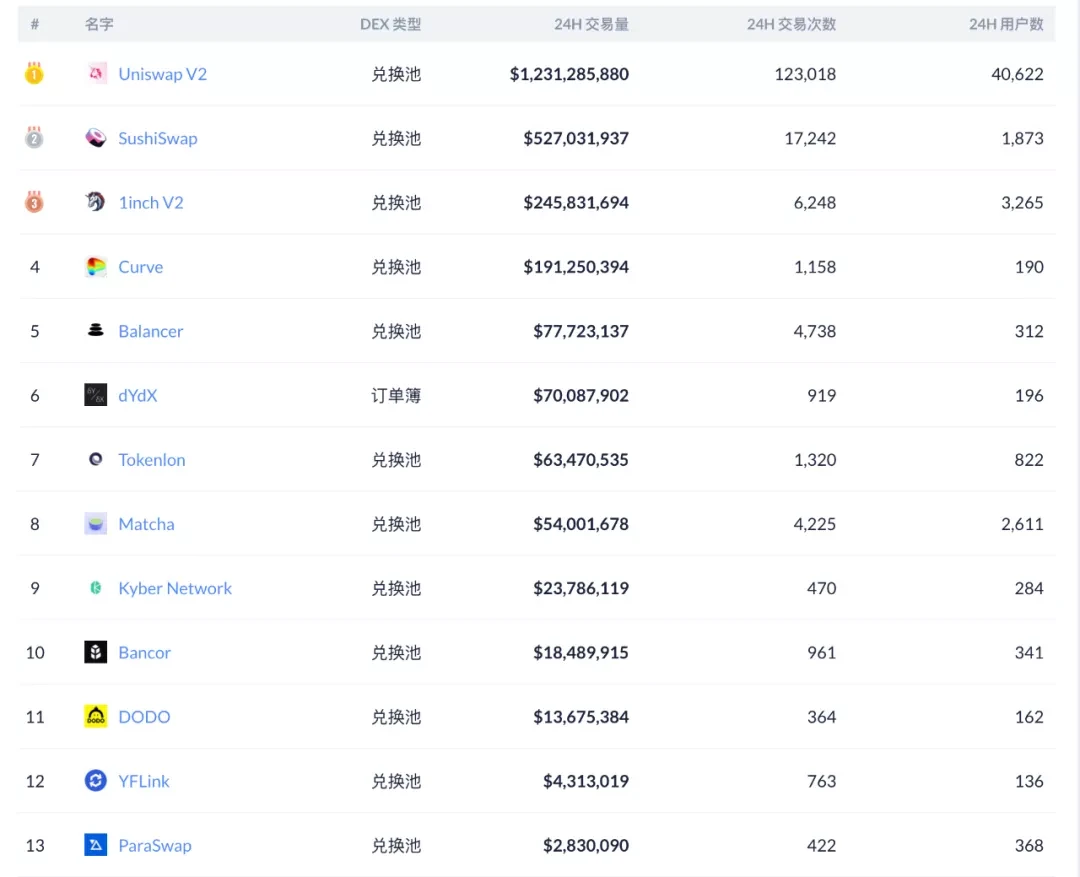

The picture above shows the DEX aggregated by the 1inch platform

When investors are not satisfied with the spot trading form, investors themselves think that they have better control over market changes and pursue higher investment returns. Investors will start to buy derivatives such as perpetual contracts. Such investors are often senior players among trading users. Although the number of users is relatively small compared with the spot market, the average trading volume is large and the market size accounts for a huge proportion.In the demand for contract trading, investors have higher requirements for trading experience and more precise operations. For example, price setting, transaction depth, transaction matching speed and loan demand, etc.Therefore, 1inch, Curve and other aggregated trading platforms have made up for the incremental demand for spot goods. The current trading volume is considerable, and the trading volume of 1inch and Curve has already ranked in the forefront.dYdX with outstanding demand

On January 9, 2021, dYdX tweeted that the transaction volume has exceeded $3 billion since the product was released. As of press time, the trading volume of dYdX has exceeded $3.5 billion, close to $4 billion. These figures prove the necessity of the dYdX business.

Among the top ten DEX trading, dYdX is the only order book exchange

dYdX mainly focuses on the contract trading market, and contract trading is also a natural lending market. So to be precise, dYdX is a decentralized exchange that integrates the cryptocurrency lending market and derivatives contract transactions. It currently includes three businesses: lending, spot trading, and contract trading.As a DEX, the three businesses of the dYdX exchange are designed based on two protocols, the solo protocol and the perpetual protocol. Among them, the solo agreement is used to manage the users basic account and exchange transactions, while the perpetual agreement is used for the execution and liquidation of the users perpetual contract.As we said earlier, in contract trading, investors have more needs, such as price setting, transaction depth, transaction matching speed, and loan demand.dYdX adopts the form of order book transactions, and has a better off-chain solution to solve the problem of transaction matching. The transaction speed directly determines the transaction experience. When a complete layer2 solution is not introduced, dYdX adopts the method of executing transactions on the chain and matching orders off the chain to solve the experience problem. But in this way, the contract matching process still needs to interact with the chain many times, and also requires a slightly higher gas fee.In addition to design principles, dYdX also has requirements on transaction rules, that is, in addition to transaction gas fees and transaction fees, dYdX also has requirements on transaction quotas. For example, the minimum purchase amount required for the BTC perpetual contract is 0.1 BTC, while the minimum purchase amount for the ETH perpetual contract is 200 US dollars.At present, dYdX has very few trading pairs, but with only three trading pairs of BTC, ETH, and LINK, the performance is extremely outstanding.Compared with the current dYdX, the White Project team believes that after dYdX launches Layer 2 solutions in the future, it will usher in a huge increase in transaction scale. The direct reason is that after the launch of layer2, dYdX will be able to support more trading pairs. dYdX founder Antonio said in a recent interview that he will focus on screening new online targets among the leading DeFi tokens with better trading volume in the near future. Moreover, in the upcoming Alpha version, full-position perpetual contract transactions will be realized, and 10 new trading pairs will be launched at the same time. In addition, in the next few years, the goal is to list 30-50 new trading pairs.Margin trading in the exchange track

Through the positioning of the contract market, the future trading volume of dYdX is worth looking forward to.Smart contracts are a very effective way to solve financial credibility and transparency issues. Decentralized perpetual contract products will be a model for the application of smart contract technology. It can also be exaggerated to say that dYdX’s perpetual contract agreement has opened up the current DeFi world Trading possibilities that do not exist.The reason why the transaction volume of the perpetual contract is huge is that as long as the price fluctuates, it will inevitably touch the liquidation of the transaction, which shortens the cycle for a single user to conduct a single transaction, and is a trading product with excellent liquidity. But now in this track, there are not many competitors, and dYdX has a strong first-mover advantage.According to Debank data, the decentralized exchanges that currently rank second and third in trading volume are Curve and SushiSwap (the two alternately). Among the trading volumes of Uniswap, Curve, and SushiSwap, Uniswap and SushiSwap benefit from a large number of transactions Yes, and Curve has benefited from the rise of DeFi mining. However, the trading model of the above three is the AMM liquidity pool. These trading models directly represent that contract transactions cannot be designed. This is where the competitiveness of dYdXs perpetual contract agreement lies.Through the comparison of historical trading volume, it can be found that among the top ten DEXs, there is only one exchange that trades in the order book mode, and that is dYdX. In front of spot trading, contract trading has a clear advantage. Once dYdXs new trading pairs are launched, its trading volume will increase significantly.But at present, what needs to be waited for is the layer2 transaction solution and the launch of Eth2.0. Because this will further reduce dYdX’s trading threshold and stimulate trading demand, and it will also be the only way for dYdX to have a CEX contract trading experience. Once launched, we can expect dYdX to break into the top five DEX trading rankings and stand at the top of the DEX market.