Original author: PSE Trading Trader@Christine

Jerome Powell

Market reaction: Shocked😲😲😲

Last week, after hearing Powells hawkish words, the market felt like it was hit by a heavy hammer, instantly falling 2%. This plot direction was actually expected. Powell took the stage to talk about lower inflation, strong growth and his steadfast commitment to keeping interest rates high to control inflation risks. Of course, in the short term, the line of high interest rates may spook the equities character, but a script tweak in the Summary of Economic Projections (SEP) could give stocks a surprising twist in the medium term. The markets first reaction was like an audiences ovation, with interest rates rising and stocks falling.

Powells view: soft landing should not be used as baseline expectation

SPX: nose dived after FOMC

Powell: Ive always thought a soft landing was a possible outcome...Ultimately, it may be determined by factors outside of our control, but I think its possible.

Dot Plot Trends and Economic Forecasts

The Federal Open Market Committee (FOMC) maintained its 2024 core PCE forecast at 2.6%, revised it to 3.78% in 2023, and raised its real GDP forecast to 1.5% from 1.1%. This combination of soft landings is largely in line with investor expectations and is seen as a medium-term positive for stocks. The FOMC left open the possibility of one rate hike for the remainder of 2023 and raised the midpoint to 5.1% in 2024, while keeping the long-term point at 2.5%. An upward shift in the dot creates a slight counterbalance to positive growth revisions.

Fed’s New Dot Plot

Powells press conference and federal funds

The federal funds rate is rock solid, but bets on a rate hike in November have jumped to 35% from 25% before the meeting. The mood of the market is like a roller coaster, with worries about long-term profit prospects. At the press conference, Chairman Powell seemed to be playing a difficult balancing act. On the one hand, he emphasized the importance of data, but on the other hand, he retained the flexibility of policy choices. This undoubtedly gave the hawkish message to the dot plot. Pour a basin of cold water on it. Despite this, basic expectations remain moderately optimistic, and long-term investments with growth/technology as the top priority remain the markets darlings.

Closed business: The battle between risk and market

If Congress does not cheer up, the U.S. government may encounter a shutdown crisis on September 30. Recent developments, such as the failure of the House of Representatives to vote on the continuing resolution (CR) and the defeat of the motion to advance the defense spending bill, have made the shadow of this crisis thicker. While the short-term risks to the overall economy from a government shutdown are likely to be limited from a macro perspective, stocks that are highly reliant on government spending may feel a chill.

BTC: Bullish despite raging bear market 🚀

Despite all the hawkish messages, I am still bullish on the market. After the market recovers from the shock, investors are sure to bounce back and focus on positive economic data:

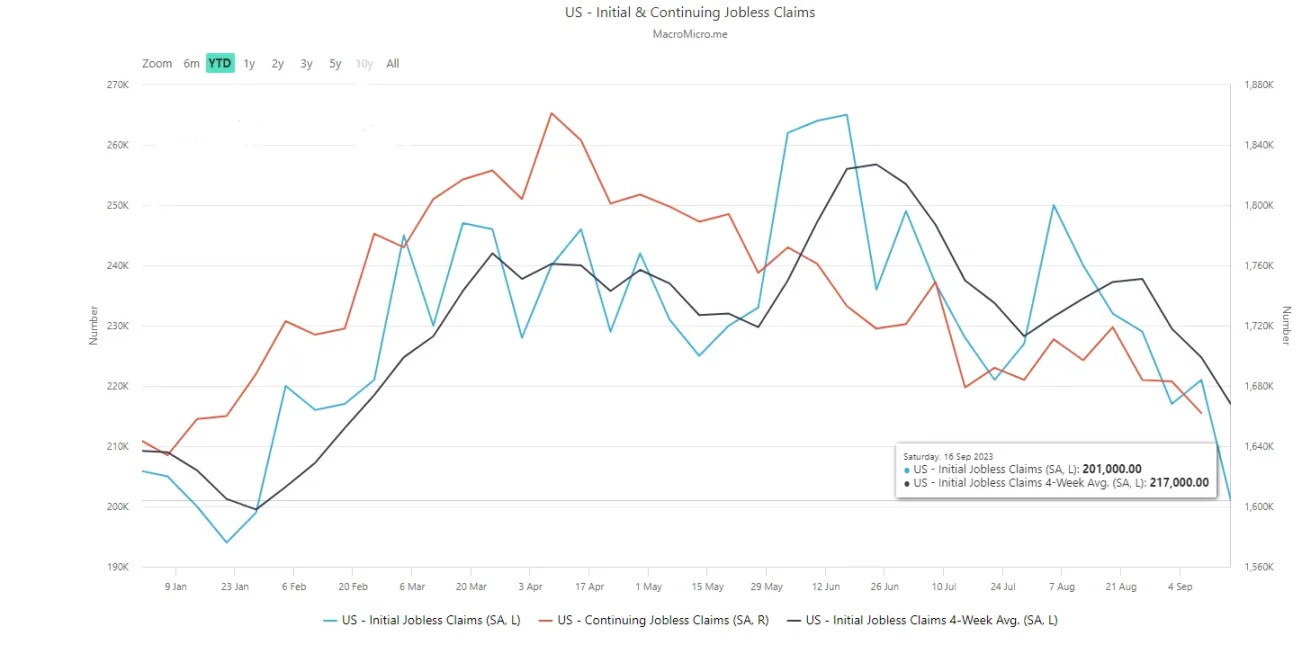

U.S. unemployment claims fall to 201K, lowest level since January

Surprisingly, U.S. unemployment claims actually fell during the week of September 16, rather than the slight increase that everyone expected. They dropped from 221k to 201k. The average over the past four weeks has also declined. Even more encouraging is that the number of people continuing to apply for unemployment benefits dropped from 1683k to 1662k during the week of September 9th. When looking at the data for each state, only 14 states saw an increase in seasonally adjusted initial filings. This decline in initial applications is the lowest we have seen since the beginning of the year and really highlights how strong and tight the current job market is. This suggests we may see solid job growth, which could push the unemployment rate further down.

Jobless Claims Down significantly

Economic activity: remains strong

Last weeks economic data showed that real economic activity remains strong. Retail sales data beat expectations, Purchasing Managers Index (PMI) reports were solid, and weekly jobless claims remained low, pointing to a healthy economy and no layoffs on the rise. On the inflation front, there were no signs of economic weakness, and while inflation was slightly higher than expected, it was not high enough to prompt the Federal Reserve to raise interest rates at the recent Federal Open Market Committee (FOMC) meeting.

US ISM PMI strong

Oil Prices and Inflation: Impact on the Economy

The surge in oil prices is causing gasoline prices to rise, which will undoubtedly hit consumption. But since the United States is now a massive oil producer and largely energy independent, there are winners to balance the losers. Economic bears are watching these price increases and saw higher oil prices pushing headline inflation to +0.6% in August, while core inflation was just +0.2%. Despite concerns about the Fed and inflation, the markets direction and narrative is more focused on the strength of the economy and corporate profits over the next six months.

Brent Crude Oil prices up significantly

Some Risks: Strikes, Lockouts, and Market Volatility

The UAW strike could last longer than expected, while the looming government shutdown in October could deal a modest hit to the economy.

However, the market is ignoring the confusion and political posturing coming from Washington and maintaining its positive momentum, which may tilt it higher towards the end of the year. Tech stocks were still going strong until their earnings disappointed, and Arm Holdings successful initial public offering last week showed a healthy restart in the IPO market and continued demand for risk.