Original author: CM (X:@cmdefi)

holy grail

Decentralized stablecoins form an impossible triangle problem among capital utilization efficiency, degree of decentralization, and price stability. Constantly finding a balance between these three has become a desirable but elusive goal.

USDT and USDC are particularly outstanding in terms of capital utilization efficiency and price stability. They have also created huge market capitalization and application scenarios with this, but they are very concentrated in terms of decentralization.

As the decentralized stablecoin with the longest history, DAI was very good at decentralization at first. It mainly used ETH as collateral to over-collateralize to mint stablecoins. However, although the ultra-high mortgage rate can stabilize the price, it sacrifices In terms of capital utilization efficiency, it is far inferior to centralized stablecoins in terms of application scenarios and market value. Then DAI gradually accepted centralized assets as collateral, sacrificing decentralization in exchange for a gradually rising market value.

UST is the most controversial decentralized stablecoin. It achieves the ultimate in capital utilization efficiency and also has decentralized characteristics. It once created a market capitalization second only to USDT USDC. However, its radical strategy can lead to extreme situations. This has caused stablecoin prices to enter a death spiral.

Therefore, until today, there has not yet been a perfect decentralized stablecoin. This may be the Holy Grail that builders are chasing after one after another.

Frax Finance is a full-stack protocol with decentralized stablecoins as its core. It started from the initial partially mortgaged algorithm stablecoins and gradually transitioned to full mortgages, while retaining the improvement of fund utilization to the maximum extent, and at the same time expanding horizontally to multiple field, eventually forming a matrix-type full-stack DeFi protocol driven by stablecoins. At the same time, it is also the longest-surviving non-fully collateralized stablecoin.

Its products include:

FRAX stablecoin: decentralized USD stablecoin★

FPI: An inflation-resistant stablecoin tokenizing a basket of goods★

frxETH:LSD ★

Fraxlend: Lending★

Fraxswap: Time-weighted decentralized exchange★

Fraxferry: Cross-chain transfer★

FXS veFXS: Governance Module☆

AMO: Algorithmic Open Market Operation Controller★

Frax Bond - Bond (v3 coming soon) ☆

RWA - Real World Assets (v3 coming soon) ☆

Frax Chain - Layer 2 (not yet online) ☆

Frax has gone through three versions: v1 v2 v3 since its launch. Unlike many protocols on the market, each version of Frax is not only a functional upgrade, but also accompanied by major strategic adjustments. That is to say, if you miss If you read a certain version, your understanding of Frax may be completely different.

Frax v1: It was launched with the goal of becoming an algorithmic stablecoin, using a fractional algorithm to gradually reduce the mortgage rate to maximize the efficiency of fund use.

Frax v2: Strategically abandon the method of gradually reducing the mortgage rate of algorithmic stablecoins, and shift to increasing the mortgage rate to become fully mortgaged. Develop AMO to enter Curve War to compete for on-chain liquidity governance resources, and develop frxETH to enter the Ethereum liquidity staking track LSD.

Frax v3: Introducing real-world asset RWA and continuing to use AMO for on-chain and off-chain liquidity.

This article will start with the latest version v3 of Frax that will be launched soon, analyze and sort out the full stack of Frax products one by one, and take you to uncover the whole picture of Frax Finance.

Frax Finance v3

Frax v3 is an upcoming version. Its core will revolve around RWA, while continuing to utilize the AMO in v2 to gradually make FRAX a fully exogenously collateralized, multi-dimensional decentralized stablecoin that captures on-chain and off-chain assets at the same time. .

completely exogenous collateral

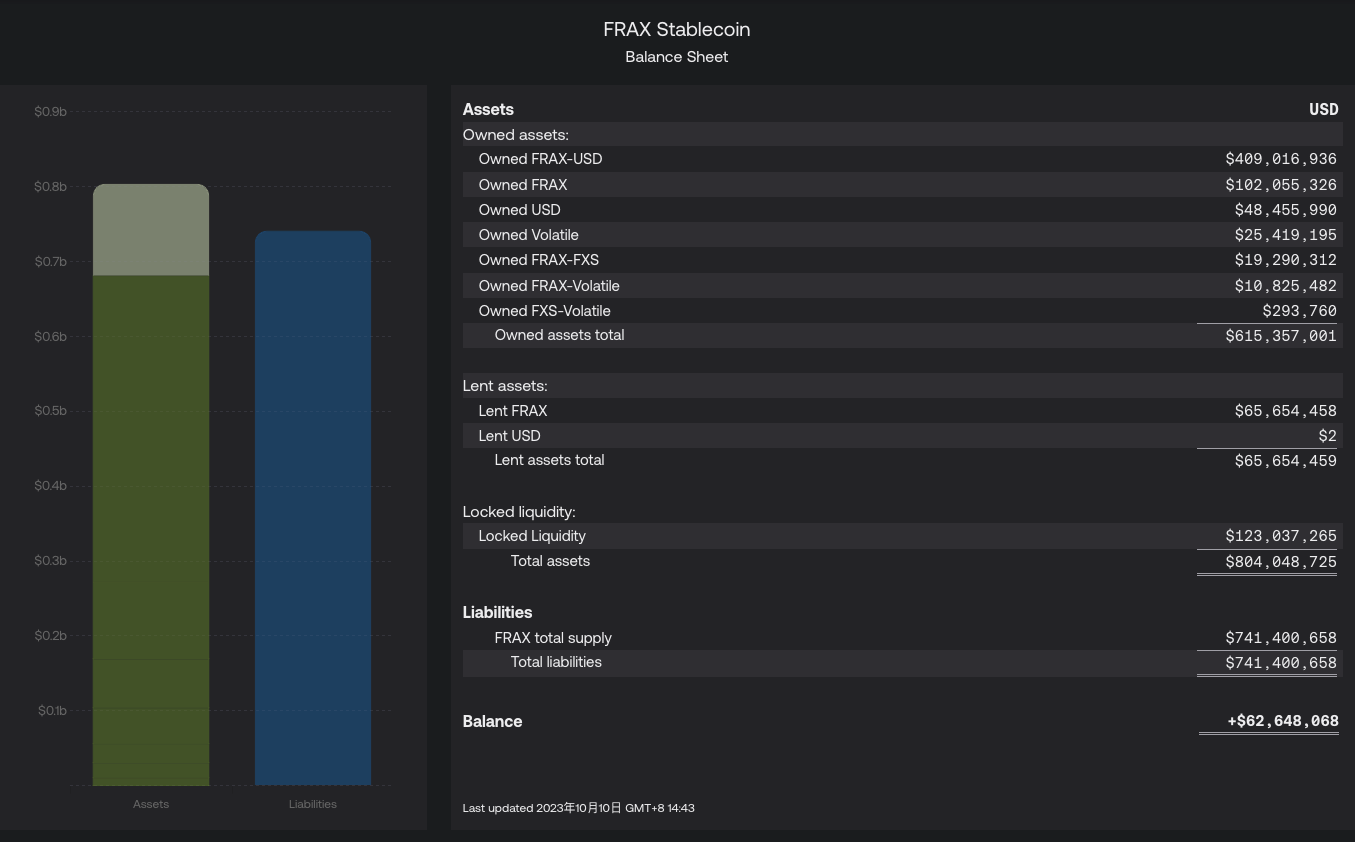

according toFRAX Balance Sheet, the current version of FRAX’s Collateral Ratio CR (Collateral Ratio) is 91.85%.

CR = (Owned assets+Lent assets) / Liabilities

CR = ( 615, 357, 001+ 65, 654, 459) / 741, 400, 658 = 91.85%

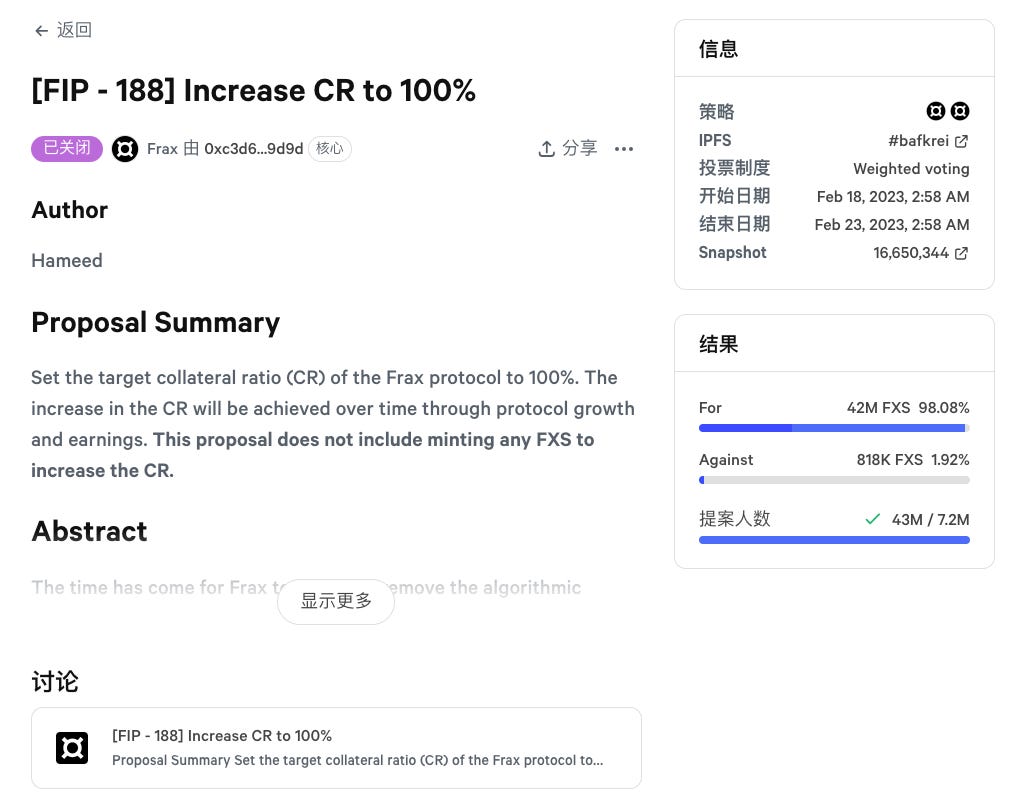

Starting from the Frax v3 version, the protocol will introduce real assets (RWA) to increase CR until CR>= 100%, eventually achieving 100% exogenous collateral for FRAX. In fact, in February 2023, the community proposal FIP 188 stopped the process of the FRAX algorithm stable currency and began to use AMO and protocol income to gradually increase the mortgage rate CR:

FIP 188

This proposal is of landmark significance to Frax. Starting from FIP 188, Frax will completely stop the fractional algorithm and decollateralization functions. Gradually move from partially collateralized algorithmic stablecoins to fully collateralized. Here are some key points of the proposal:

The initial version of Frax included a fractional algorithm, a variable collateral ratio, that adjusted based on market demand for FRAX, effectively letting the market decide how much of the combination of external collateral and FXS was needed to equal $1.00 per FRAX.

The reason for discontinuing the fractional algorithm is that, judging from the market environment, the costs of being slightly undercollateralized far outweigh the benefits it brings. The markets concern about 1% being undercollateralized is far greater than the need for an additional 10% yield.

Over time, growth, asset appreciation, and protocol benefits will increase CR to 100%. To be clear, the proposal does not rely on minting any additional FXS to achieve 100% CR.

Protocol revenue is retained to fund CR improvements and FXS buybacks are suspended.

FRAX Balance Sheet 2023.10.10

FIP 188 proposal passed

RWA

As one of the important means to improve CR>= 100% in Frax v3, Frax’s upcoming frxGov governance module will approve real-world entities to purchase and hold real-world assets controlled by AMO, such as U.S. Treasury bonds.

Users holding FRAX can deposit it into a designated smart contract and obtain sFRAX. This principle is similar to the relationship between DAI and sDAI. Let’s compare the differences between sFRAX and sDAI:

One reason why sDAI can obtain a slightly higher average return on government bonds (currently 5%, with a maximum of 8%) is that not all holders of DAI have deposited DAI into the DSR contract, and Maker’s return on investing in RWA is only It needs to be distributed to those who deposit DAI into DSR to obtain sDAI, so it is equivalent to some people sharing all the RWA income.

sFRAX also meets this condition, but since Frax accumulated a large number of Curve and Convex tokens in the v2 version stage and obtained a large number of vote rights through lock-up, it can control certain CRV and CVX rewards on the chain. This part of the on-chain income will The comprehensive income of sFRAX will be improved. At the same time, when one end of the chain or off-chain has poor returns or the risk becomes high, you can quickly switch to the other end.

IORB Oracle

The FRAX v3 smart contract uses the Federal Reserves Interest Rate on Deposits (IORB) to provide data for certain protocol functions, such as sFRAXs equity returns.

When the IORB interest rate increases, the AMO strategy of the Frax protocol will use treasury bills, reverse repurchase contracts, and U.S. dollars deposited in the Federal Reserve Bank that pays the IORB interest rate to mortgage FRAX in large quantities.

When the IORB rate drops, the AMO strategy will begin to rebalance FRAX staking with on-chain decentralized assets and staking in Fraxlend.

Simply put, FRAX v3 adjusts its investment strategy based on the interest rate on deposits of the Federal Reserve (IORB). When off-chain returns are high, funds are sent to treasury bills, treasury bonds, etc., and when on-chain returns are high, funds are sent to on-chain lending, such as Fraxlend, ensuring maximum returns and stability of stablecoins.

frxGov Governance Module

Frax v3 will remove multi-signature and implement governance entirely through the smart contract frxGov module (veFXS). This is an important step towards decentralized governance for Frax.

FraxBond (FXB) Bond

sFRAX and FXB both bring Treasury yields into Frax, but they differ:

sFRAX is the zero-maturity portion of the yield curve and FXB is the forward portion. The two together form a comprehensive stablecoin yield curve on the chain.

If 50 M FRAX is pledged as sFRAX, then ~50 M USDC (assuming CR= 100%) in the corresponding treasury can be sent off-chain to purchase 50 M worth of short-term government bonds.

If 100 M of 1-year-maturity FXB are sold for 95 M USDC, it means that the off-chain cooperative entity can buy 1-year Treasury bonds with 95 M USD.

In addition, FXB is a transferable ERC-20 token that can build its own liquidity and circulate freely in the secondary market, providing users with stablecoin investment options of different maturities, different rates of return, and different risk levels, and also provides users with stablecoin investment options. New components are provided for building new LEGO sets.

Frax Finance v1

Frax v1 proposes the concept of a fractional algorithmic stablecoin, which simply means that part of its supply is backed by exogenous collateral (USDC) and part is unbacked (algorithmically backed using endogenous collateral FXS).

For example, at a CR of 85%, each redeemed FRAX would provide the user with $0.85 USDC and $0.15 worth of FXS.

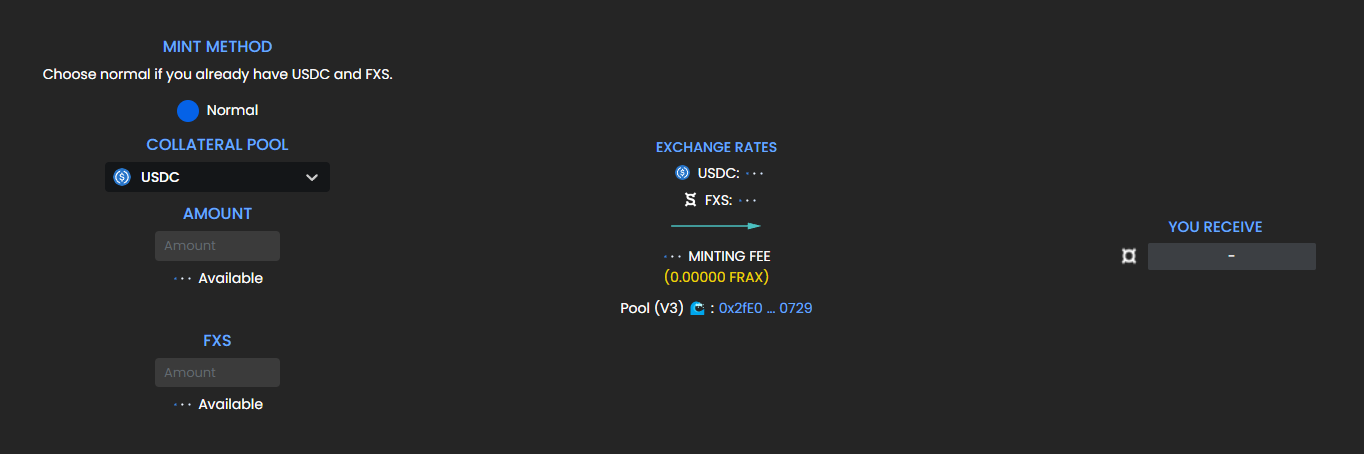

Minting $FRAX using USDC and FXS in Frax v1

AMO exists in its simplest form in v1, in which it is called the fractional algorithm. Its main function is to adjust the CR when casting FRAX according to market conditions. The most original setting is to adjust it at a fixed time (for example, once every 1 hour).

In the first state when Frax v1 was launched, FRAX was minted with CR= 100%, that is, 1 FRAX = 1 USDC. This stage is called the integer stage. After that, at regular intervals, AMO will control the CR to adjust downwards and upwards according to market conditions to enter the fractional stage.

If FRAX >1 is above the peg and needs to be expanded, the CR is lowered, allowing more FRAX to be minted with less collateral.

If FRAX <1 the price falls below the peg, CR increases, thereby increasing the collateral backing each FRAX to restore confidence in the system.

Although the score algorithm can intervene in the CR when newly casting FRAX, this method is relatively slow to affect the CR of the entire system. In addition, two more functions have been added to Frax v1 to promote the dynamic changes of CR to coordinate with the score. The algorithm brings CR to the exact state required by the protocol:

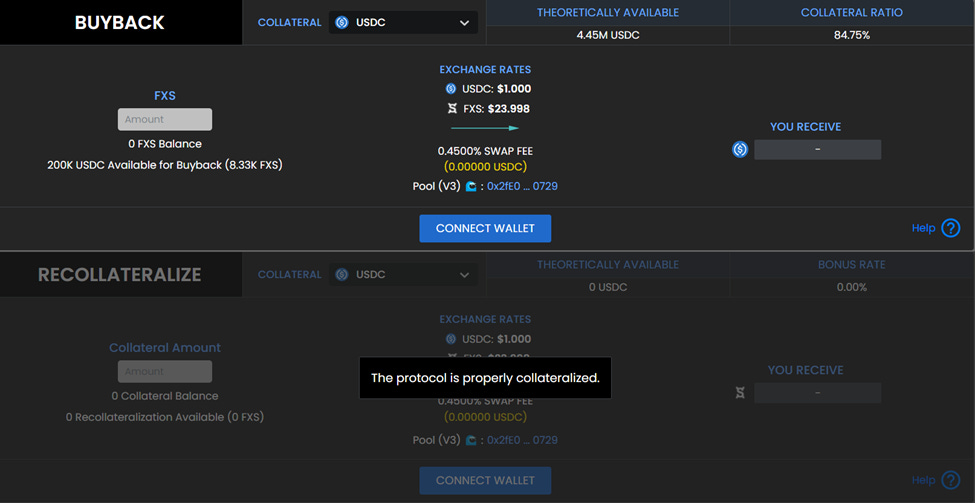

Decollateralization and Recollateralization

Re-mortgage: When the fractional algorithm increases the system mortgage rate, in order to make the actual mortgage rate equal to the system mortgage rate, the amount of USDC in the system must be increased. FRAX sets an incentive: anyone can add USDC to the system and exchange A larger amount of FXS; for example, a user can add $1 worth of USDC to the system in exchange for $1.2 worth of FXS.

De-collateralization (repurchase): When the system mortgage rate is reduced, users can exchange FXS to the system for USDC of the same value at any time, and then FXS will be destroyed. There are no incentives in the buyback mechanism.

De-mortgage (repurchase) and re-mortgage operation page

Frax Finance v2

Frax v2 is the version with the most frequent actions. In this version, the fraction algorithm is stopped, AMO is launched for treasury fund management, and profits are gradually used to fill the mortgage rate CR. At the same time, new businesses such as Fraxlend and frxETH are also launched and participate in Curve Become the winner of on-chain liquidity governance rights in war.

AMO(Algorithmic Market Operations Controller)

AMO is a tool similar to the Federal Reserves tool for implementing monetary policy. Its operating mechanism is that as long as it does not reduce the collateral ratio and change the FRAX price, it can formulate any FRAX monetary policy and print money within the limits of the established strategy algorithm. , destroy and dispatch funds. This means that AMO controllers can perform open market operations algorithmically (hence their name), but they cannot simply mint FRAX out of thin air to break the peg.

Frax currently runs 4 AMOs, of which Curve AMO has the largest amount of funds. With the operation of AMO, the protocol will use idle assets in the treasury (mainly USDC) and a certain amount of money printing (algorithm-controlled FRAX) to be put into other DeFi protocols:

Maximize the use of treasury funds to earn additional income. For example, if the treasury holds 1M USDC, AMO prints 1M FRAX, and forms USDC-FRAX LP for mining, and actually obtains 2M mining income.

Since the ownership of money printed in AMO (algorithm-controlled FRAX) is held by the agreement and can be withdrawn and destroyed in the AMO strategy, it is not circulated to users, so it will not have a major impact on the anchoring of FRAX.

This increases the market capitalization of FRAX without actually adding new collateral.

Take the Curve AMO strategy as an example to interpret:

Decollateralize - Put idle collateral and AMOs newly minted FRAX into the Curve Pool.

Recollateralize - First withdraw FRAX-USDC LP from the pool, destroy excess (once newly minted and controlled by the protocol) FRAX, and return USDC to increase the collateral rate CR.

Protocol Yields - Accumulated transaction fees, CRV rewards, and regular rebalancing of the pool. Deposit LP tokens into platforms such as Yearn, Stake DAO and Convex Finance to earn additional income.

Let’s analyze AMO’s very critical “money printing” ability.

The core of AMO’s “money printing” strategy can be summarized as:

When AMO wants to add treasury funds USDC to the Curve Pool, if a large amount of USDC is added alone, it will affect the proportion of USDC in the pool and thus the price. Therefore, after USDC is matched with the corresponding amount of money printing FRAX to form LP, it will be added to the fund pool with minimal slippage. LP is held and controlled by AMO.

In addition to this, if you want to maximize money printing, there is another scenario:

Assume a pre-money printing supply of FRAX is Y, and the markets tolerance for a decline in FRAX falling below $1 is X%.

If all Y were sold at once into a Curve Pool with Z TVL and A amplification factor, it would have an impact on the price of FRAX of less than X%. This proves that it is acceptable to circulate an additional Y amount of FRAX in the open market.

In other words, since Curve AMO can put FRAX+USDC into LP into its own Curve Pool and control TVL, when FRAX drops by X%, the excess FRAX can be withdrawn and destroyed through the AMO Recollateralize remortgage operation. Boost CR and bring price back to anchor. The more LP an AMO controls, the stronger this ability becomes.

Therefore, before FRAX falls by X%, based on AMOs ability to control LP, it can be calculated that the amount of FRAX is allowed to be sold into the Curve Pool in one go without having a sufficient impact on the price to cause CR to move. This amount is to maximize money printing.

For example, the 330 million TVL FRAX 3 Pool can support FRAX sell orders of at least $39.2 million without the price changing more than 1 cent. If

The above strategy is an extremely powerful market operation that will mathematically create a negotiable algorithmic FRAX floor without any danger of breaking the anchor.

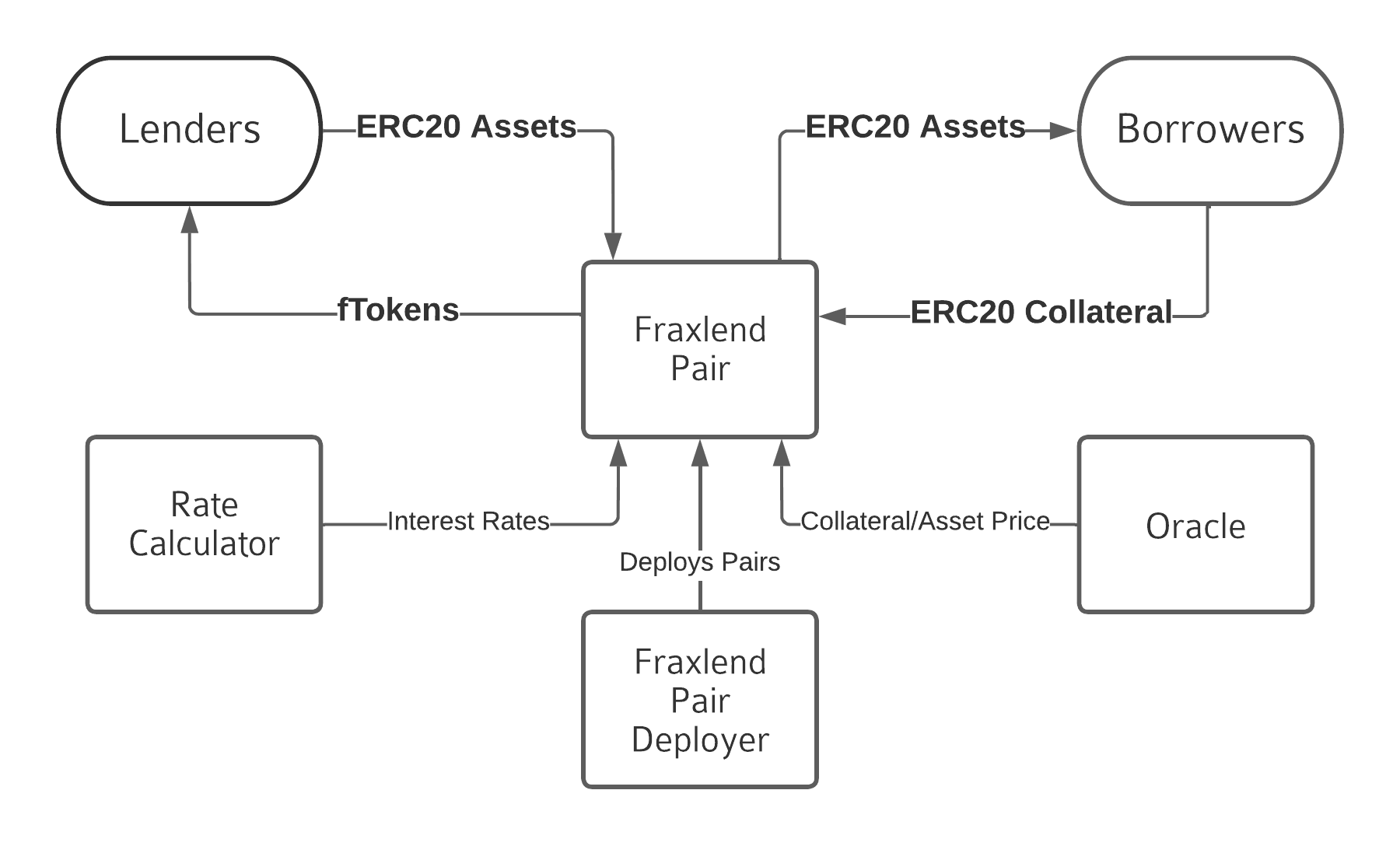

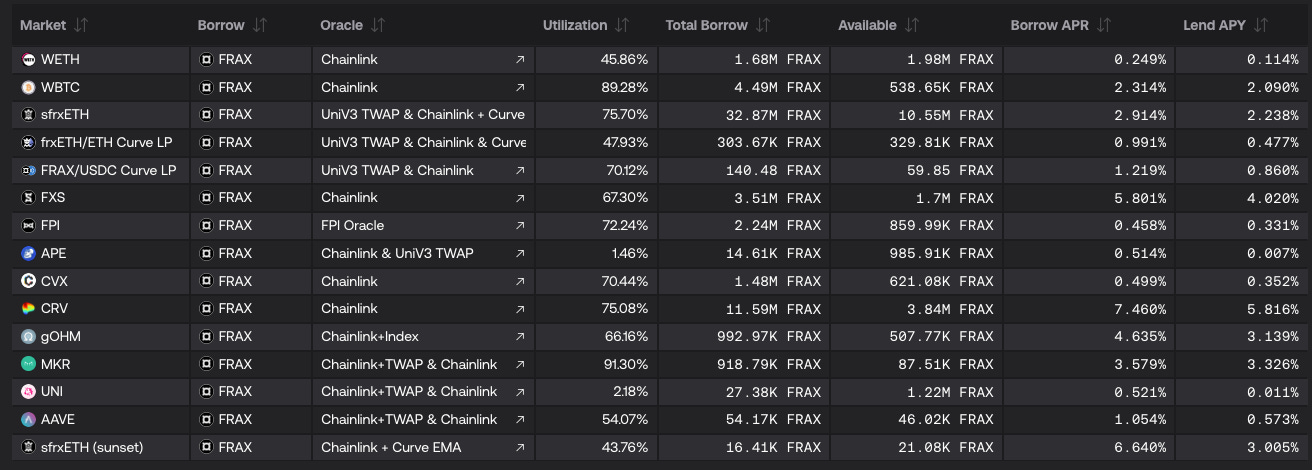

Fraxlend

Fraxlend is a lending platform that provides a lending market between ERC-20 assets. Unlike the mixed lending pool of Aave v2, each lending pair in Fraxlend is an isolated market. When you choose to deposit a certain collateral for borrower borrowing, it proves that you fully recognize and accept the value and risk of this collateral. . At the same time, the design of this isolation pool has two characteristics:

Any issues related to collateral or NPLs are limited to individual pairs and do not affect other lending pools;

Collateral cannot be lent.

Fraxlend mechanism features - interest rate model

Fraxlend offers 3 interest rate models (2 and 3 in practical applications). Unlike most lending protocols, all Fraxlend’s interest rate calculators automatically adjust according to market dynamics without governance intervention. The Frax team believes it is better to let the market determine interest rates rather than having the team come up with governance proposals every time the market moves (as this approach is slower).

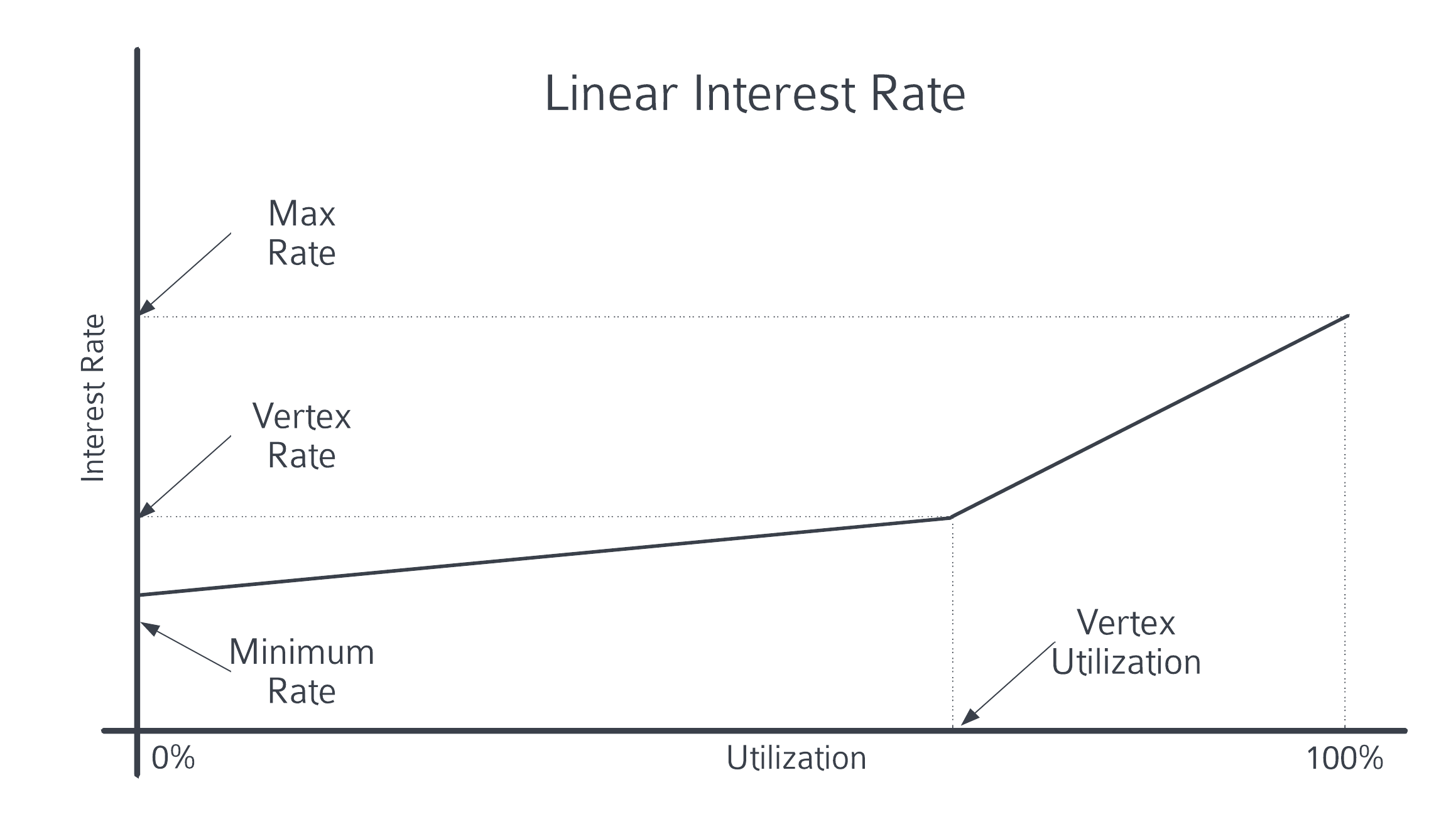

1 linear interest rate

When the capital utilization rate exceeds the critical value of the peak utilization rate, the interest rate rise curve begins to become steeper. Most lending protocols adopt this basic interest rate growth model to ensure that when the funds in the capital pool are borrowed too much, the interest rate is increased to encourage lender deposits. , borrower repayment.

2 Time-weighted floating interest rate

Time-weighted floating rates adjust current interest rates over time. It controls the interest rate through 3 parameters:

Utilization rate: Adjust the interest rate based on the fund utilization rate.

Half-life: This value determines how quickly interest rates adjust. In laymans terms, rates increase using a multiplier when utilization is high and decrease when utilization is low.

Target utilization range: No interest rate adjustments will be made within this range, which is considered to be in line with market expectations.

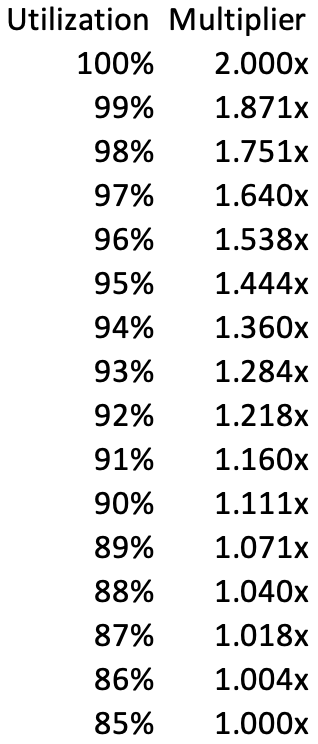

In currently available interest rate calculators, the interest rate half-life is 12 hours. If utilization is 0%, the interest rate halves by 50% each half-life, and if utilization is 100%, the interest rate doubles and increases by 100% each half-life.

This interest rate model played a key role in the CRV liquidation of Curve founder Mich, Curve was affected by the 0-day vulnerability attack on the vyper compiler, resulting in a run on Michs CRV loan position on the chain, a large number of lender withdrawals, and a capital utilization rate soaring close to 80% -100%. The CRV market was adopted in Fraxlend In the time-weighted floating interest rate model, when the fund utilization rate is close to 100%, the half-life is 12 hours, and the interest rate of CRV mortgage borrowing will double every 12 hours. This prompts Mich to first repay the borrowed money in Fraxlend. If it is not returned in time, the doubling rate of the interest rate every 12 hours will be the first to execute Michs liquidation.

Interest rate adjustment multiplier corresponding to 85% -100% utilization rate

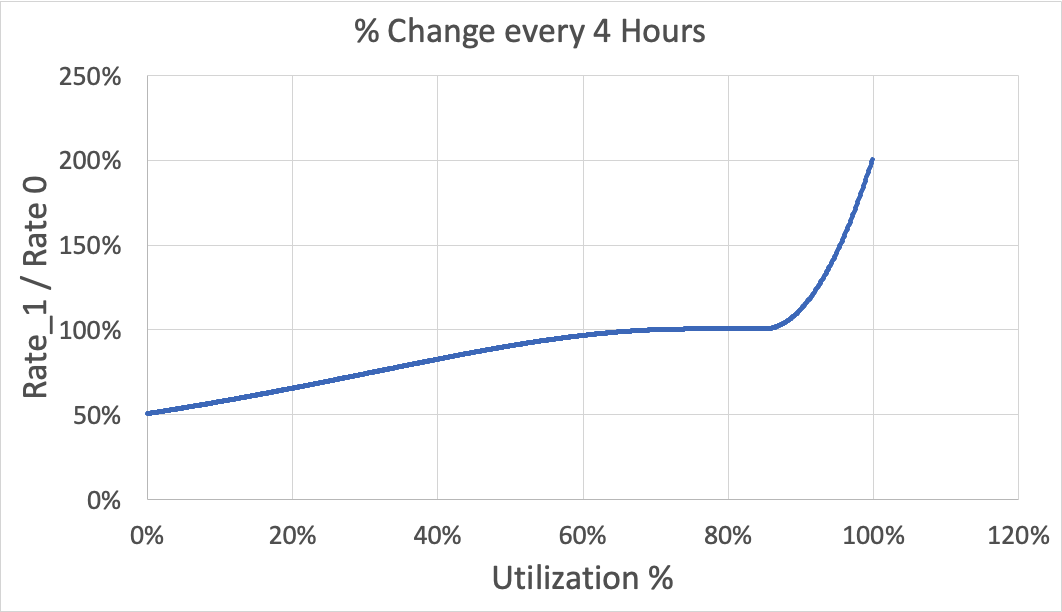

The chart below shows how interest rates change when the interest rate half-life is 4 hours and the target utilization range is 75% - 85%:

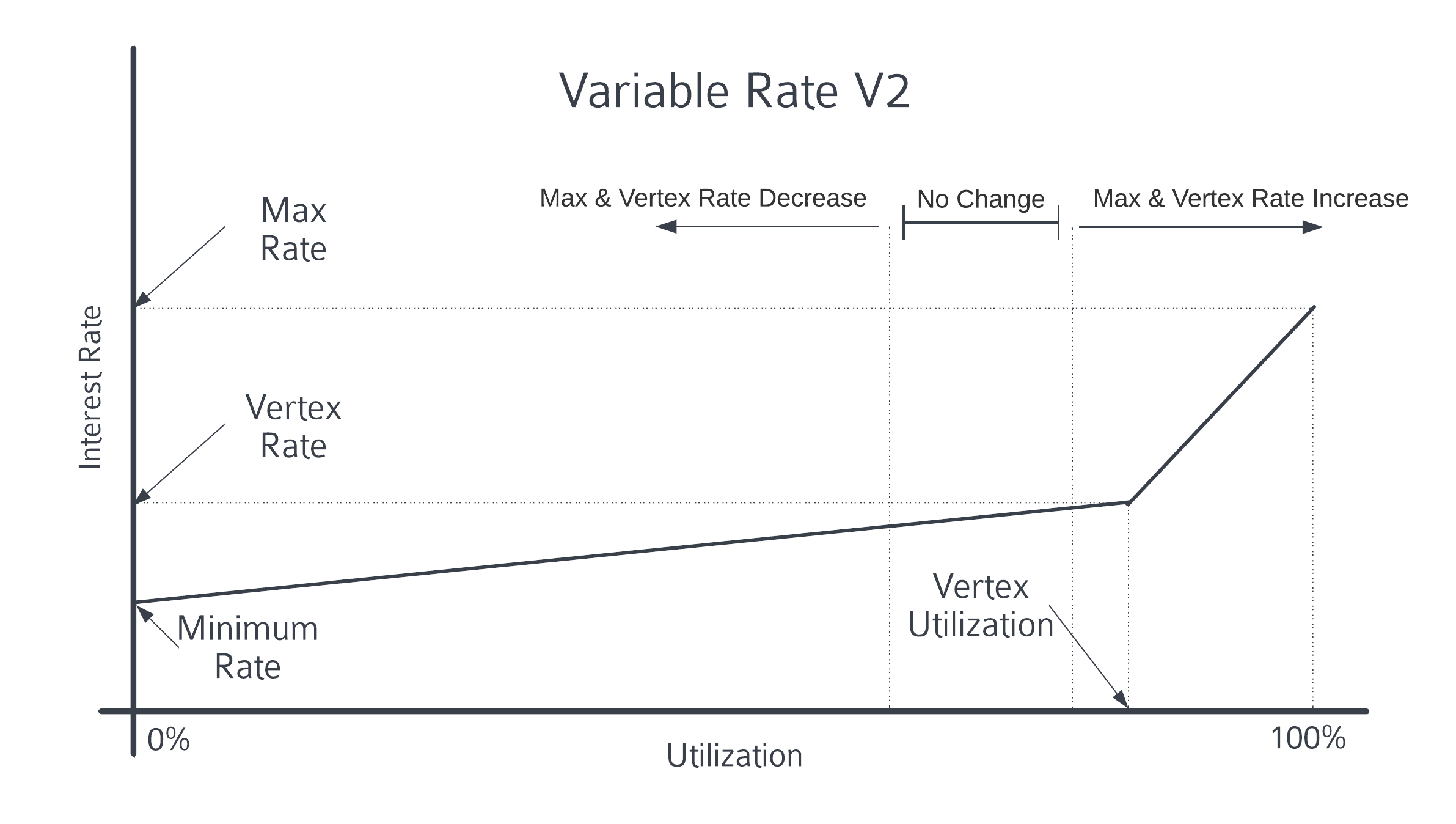

3 Floating interest rate V2

The floating interest rate V2 interest rate combines the concepts of linear interest rate and time-weighted floating interest rate. Specifically, it uses a linear function of the linear interest rate to determine the current interest rate, but uses a formula for a time-weighted floating rate to adjust the peak and maximum rates. It is characterized by the fact that the interest rate will respond immediately to changes in utilization on the linear interest rate curve while adapting to long-term market conditions by adjusting the slope of the linear interest rate curve.

Just like the time-weighted floating rate, floating rate V2 uses half-life and target utilization range parameters. When utilization is low, the top and maximum rates will decrease. If utilization is high, the cap and maximum rates will increase.

Decrease/increase rates are determined by utilization and half-life. If utilization is 0%, the apex rate and maximum rate will be reduced by 50% each half-life. If utilization is 100%, increase by 100% per half-life.

Fraxlend mechanism features - dynamic debt restructuring

In a typical lending market, liquidators can close the borrowers position once the LTV exceeds the maximum LTV (usually 75%). However, in the event of severe volatility, liquidators may not be able to close unhealthy positions before the LTV exceeds 100%. In this case, bad debts will occur, and the person who finally withdraws the funds will suffer the greatest loss, and it will become a run fast game.

In Fraxlend, when a bad debt occurs, the pool will immediately socialize the losses and distribute them to all lenders. This helps keep the market liquid and does not immediately dry up the lending market even after a bad debt occurs.

Fraxlend AMO

The Fraxlend AMO allows FRAX to be minted into the Fraxlend lending market to allow anyone to borrow FRAX by paying interest instead of the underlying minting mechanism.

FRAX minted into the money market will not enter circulation unless the borrower is over-collateralized through the money market, so this AMO will not reduce the direct collateralization ratio (CR). It helps expand the scale of FRAX and creates a new way for FRAX to enter circulation.

Strategy:

Decollateralize - Mint FRAX into the money market. Minted FRAX does not directly lower CR, as all borrowed FRAX is over-collateralized.

Recollateralize - Withdraw minted FRAX from the lending market.

Agreement Yield - Fees incurred by the borrower.

In addition, because Fraxlend AMO has the ability to print money and destroy, it can lower interest rates by minting more FRAX, or destroy FRAX to increase interest rates. This interest rate adjustment ability is a powerful economic lever because it changes The cost to all lenders of borrowing FRAX.

In theory, if Frax is willing and determined, it can mint enough FRAX stablecoins into Fraxlend to attract users to lend FRAX at a lower interest rate than any other stablecoin in the market to expand, which will create the best lending interest rates, and increase interest rates through Fraxlend AMO when needed to respond to the market. It is difficult for stablecoin projects to control their lending rates.

Fraxswap

Fraxswap uses a time-weighted average market maker (TWAMM) for trustlessly conducting large transactions over long periods of time. It is completely permissionless and the core AMM is based on Uniswap V2. TWAMM is discussed in detail in another article:TWAMM time weighted average market maker

FPI (Frax Price Index)

FPI is the first inflation-resistant stablecoin pegged to a real-world basket of consumer goods defined by the U.S. CPI-U average. The FPI stablecoin aims to maintain its purchasing power by keeping its price constant with all items in the CPI basket through an on-chain stabilization mechanism. Like the FRAX stablecoin, all FPI assets and market operations are on-chain and use AMO contracts.

FPI uses the CPI-U unadjusted 12-month inflation rate as reported by the U.S. federal government: a dedicated Chainlink oracle submits this data on-chain immediately after it is publicly released. The inflation rate reported by the oracle is then applied to the redemption exchange price of the FPI stablecoin. This redemption price grows on-chain every second (or falls in the rare case of deflation).

FPIS

FPIS is the governance token of the system and is also entitled to seigniorage from the protocol. Excess proceeds will be distributed directly from the Treasury to FPIS holders, similar to the FXS structure.

When the revenue generated by the FPI is insufficient to sustain the increased support of the FPI due to inflation, new FPIS may be minted and sold to increase the financial support of the FPI.

FPI stabilization mechanism

FPI uses the same type of AMO as the FRAX stablecoin, but its model always maintains a 100% Collateral Rate (CR). This means that in order to keep the collateral ratio at 100%, the protocols balance sheet must grow at least at the rate of CPI inflation. Therefore, AMO strategy contracts must earn returns proportional to CPI, otherwise the CR will drop below 100%. During periods when AMO earnings are below the CPI rate, a TWAMM AMO will sell FPIS tokens in exchange for FRAX stablecoins to ensure that the CR is always 100%. FPIS TWAMM is deleted when CR returns to 100%.

frxETH - Ethereum staking derivatives

Frax ETH currently ranks 4th overall on the LSD track, with TVL $427.64M and a market share of 2.42%. However, in terms of revenue provided, it can reach 3.88% as of press time, ranking 1st. The reason why Frax ETH can provide returns above market levels also comes from its own on-chain liquidity management resources.

LSD data from defillama

Frax ETH includes:

frxETH (Frax Ether): An Ethereum stablecoin pegged to ETH. 1 frxETH always represents 1 ETH, similar to Lidos stETH, but holding frxETH alone will not be rebased and will not earn Ethereum staking benefits.

sfrxETH (Staked Frax Ether): sfrxETH is an ERC-4626 vault designed to accumulate staking earnings for Frax ETH validators. At any time, frxETH can be redeemed for sfrxETH by depositing into the sfrxETH vault, allowing users to earn staking benefits on frxETH. Over time, as validators accumulate staking earnings, an equal amount of frxETH is minted and added to the vault, allowing users to exchange their sfrxETH for more frxETH than they deposited. Therefore, in theory, the exchange rate of sfrxETH to frxETH will always increase over time. By holding sfrxETH, users can hold % claims on more and more frxETH in the vault. It works similarly to Aave’s aDAI.

So how did Frax ETH push interest rates above the market average?

Frax has accumulated a large amount of CRV and CVX governance resources in the market through AMO, and built frxETH Pool in Curve and Convex, so that frxETH can obtain incentives in the third-party liquidity market without issuing additional tokens FXS. All staking income of Ethereum will be covered by sfrxETH.

We assume that of the 270,000 ETH pledged in Frax ETH, 100,000 are not pledged to sfrxETH, but form a liquidity pool with other Ethereum assets, such as WETH, stETH, etc. in the liquidity market, and the other 170,000 ETH The stake is sfrxETH. Then the incentives obtained respectively are:

100,000 frxETH in liquidity pools such as Curve and Convex will receive CRV and CVX incentives.

170,000 pieces of frxETH pledged into sfrxETH will receive 270,000 pieces of Ethereum as pledge income.

Therefore, Frax ETH uses the liquidity governance resources on its chain to introduce external incentives to frxETH, improve comprehensive income, and indirectly increase the market interest rate of LSD (sfrxETH).

frxETH Pool comes from Convex

crvUSD already supports sfrxETH as collateral

Frax Shares (FXS)

Financing situation

Frax Finance has conducted two rounds of financing in July and August 2021. The financing tokens accounted for 12% of the total amount, but the financing amount and valuation were not disclosed.

Participating investors in Frax Finance include well-known investment institutions such as Parafi, Dragonfly, Mechanism, and Galaxy digital, as well as well-known project founders in the DeFi field such as Stani kulechov of Aave, Robert Leshner of Compound, Kain Warwick of Synthetix, Eyal Herzog of Bancor, etc. , as well as investments from CEX background, such as Crypto.com and Balaji Srinivasan (former Coinbase CTO and A16Z partner), etc.

Frax Finance Investors

Token distribution

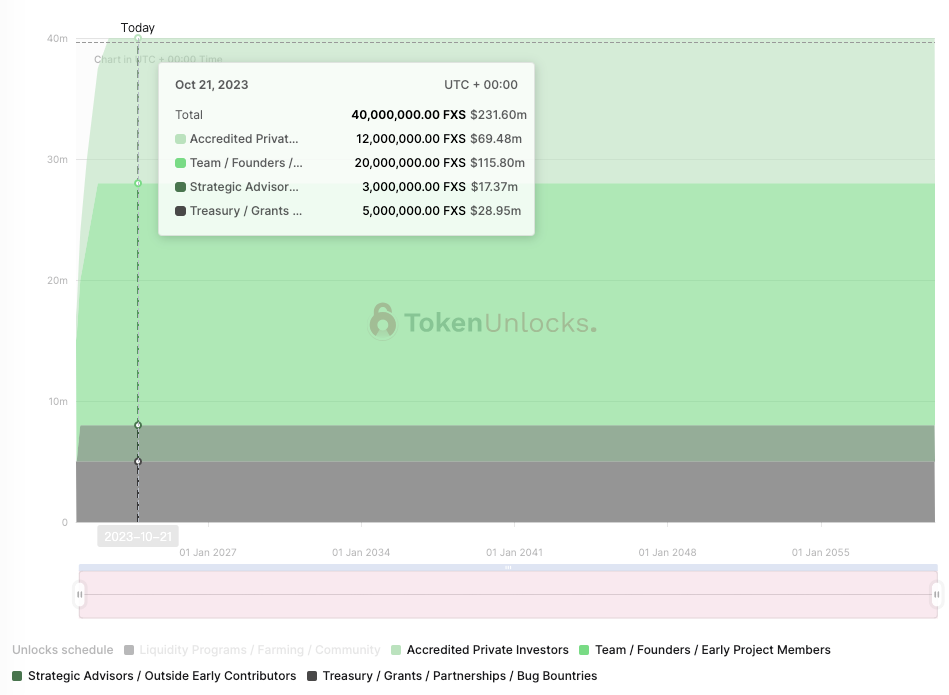

60% – Liquidity Plan/Farming/Community – Naturally halved every 12 months through governance

5% – project treasury/grants/partners/security bug bounties – at the discretion of the team and community

20% – Team/Founders/Early Project Members – 12 months, 6 month cliff

3% – Strategic Advisor/External Early Contributor – 36 months

12% – Accredited Private Investors – 2% unlocks at launch, 5% vests within first 6 months, 5% vests within 1 year, cliff within 6 months.

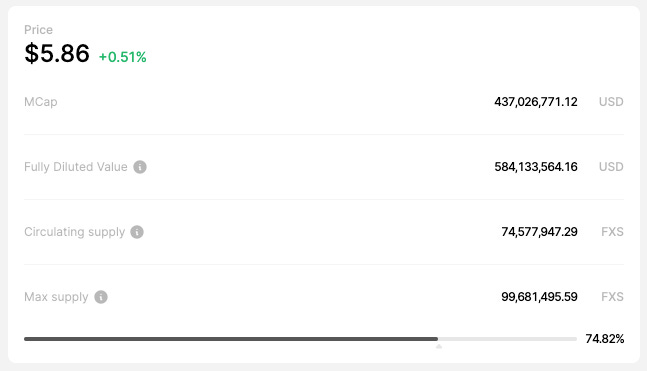

The current total circulation of FXS is 74.57 M, with a total volume of 100 M. The team, advisors, and external investors are all fully unlocked, and all uncirculated parts are community parts (liquidity plan/treasury).

FXS market capitalization and circulation data

veFXS Token Economics

veFXS is a vesting and revenue system based on the Curve veCRV mechanism. Users can lock their FXS for up to 4 years to receive veFXS. veFXS is not a transferable token and is not traded on a liquid market.

Currently, 36.15 M has been locked in veFXS, accounting for 48.48% of the circulating supply.

The veFXS balance decreases linearly as the token approaches lock expiration, approaching 1 veFXS per 1 FXS when the remaining lock time is zero. This encourages long-term staking and an active community.

Each veFXS has 1 vote in governance proposals. Staking 1 FXS for a maximum period of time (4 years) will generate 4 veFXS. This veFXS balance itself will slowly decay to 1 veFXS after 4 years, at which time users can exchange veFXS back to FXS.

Gauge

Similar to veCRV’s power in the Curve system, veFXS can vote to determine the emission of incentives in the liquidity pools supported by Frax.

Gauge

repurchase

The main cash flow distribution mechanism of the Frax protocol is to veFXS holders. Cash flows earned from AMOs, Fraxlend loans, and Fraxswap fees are typically used to buy back FXS from the market and then distributed to veFXS stakers as proceeds.

However, with the strategic adjustments in Frax v2 and v3, the protocol will prioritize increasing CR to 100%, so buybacks may be suspended or restricted. When CR is increased to 100%, veFXS will have the opportunity to capture all of the protocol revenue.

Real mortgage rate analysis

We have reorganized Fraxs balance sheet (2023.10.10), and the protocol holds a total of 616.8 M of assets, including:

The total amount of FRAX held by the protocol is 450.1 M

USD and other assets totaling 166.7 M

In addition, the FRAX lent in Fraxlend is 65.6M (over-collateralized), the issuance size of FRAX (total circulation) is 741.4M, and the mortgage rate is 92.05%.

CR= Asset SUM / total FRAX

If the FRAX held by the protocol is removed from both the asset and liability sides, the mortgage rate value will decrease, but the absolute value of the mortgage rate gap will not change much. This absolute value is currently around 58.97 M.

From here we can see:

Through the AMO strategy, Frax used 166.7 M of underlying assets to leverage several times the size of the stablecoin without breaking the anchor. (If the traditional issuance ratio of 1:1 is followed, the circulation of FRAX is equal to the value of the underlying assets 166.7 M)

To reach CR= 100%, the protocol needs to earn 58.9M into the treasury.

Fraxs profitability level

Currently, most of Frax’s profits come from AMO:

Curve, Convex AMO income 2% -8%

Fraxlend AMO earns 2% -6%

RWA yield 5.5%

sDAI earns 5%

Convex AMO annualized yield

To estimate how long it will take for the protocol to reach CR= 100% from two angles, take the AMO average income level of 5% APY:

If all AMO control assets are maximized

680 M* 5% = 34 MIf most of the AMO money printing funds are recovered (current status)

200 M* 5% = 10 M

In other words, under the current market environment, it will take about 2-6 years to achieve CR= 100% by relying on AMO income. Of course, since most of the income in AMO is CRV and CVX tokens, if the market situation improves, the increase in CRV and CXV tokens will accelerate this process.

1 Evaluate the impact of increases in CRV and CVX on CR

Currently Frax holds 8M CRV (~$3.4M), 3.7M CVX (~$9.8M)

If the price of CRV and CVX rises 4 times compared with the current price, CR can rise directly to nearly 100%

CRV $ 0.44 → $ 1.76

CVX $ 2.68 → $ 10.72

2 Impact of RWA business on CR

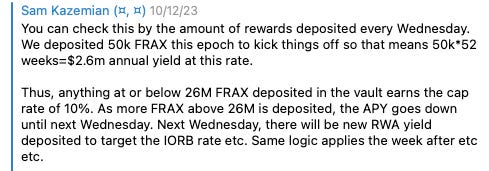

sFRAX was launched in Frax v3 to capture the returns of real-world assets, which is a relatively bright track in the bear market of DeFi. The current return calculation method of sFRAX is to track the IORB interest rate, and 50 K FRAX will be deposited every Wednesday to pay the current The total income of sFRAX in one year is 50 K* 52 = 2.6 M. Calculated based on the actual annualized income of RWA of 5.5%, Frax will deploy at least 2.6 M / 5.5% = 47 M of US dollar assets to RWA. (This data is estimated based on current earnings and may change with IORB fluctuations in the future)

When the deposit in the sFRAX contract is less than 26M, the annualized return of sFRAX will be 10%, which will gradually decrease as more FRAX is deposited.

From Sam, founder of Frax

At present, the potential income of the Frax Finance protocol itself in the RWA business is to deploy AMO funds here to earn income. Another possibility is whether Frax will charge fees or protocol dividends for this part of RWA income in the future. Once the Frax RWA business As the scale grows, and the agreement charges fees or dividends on this part of the profits, this will also greatly accelerate the process of CR = 100%.

3 Impact of Frax ETH business on CR

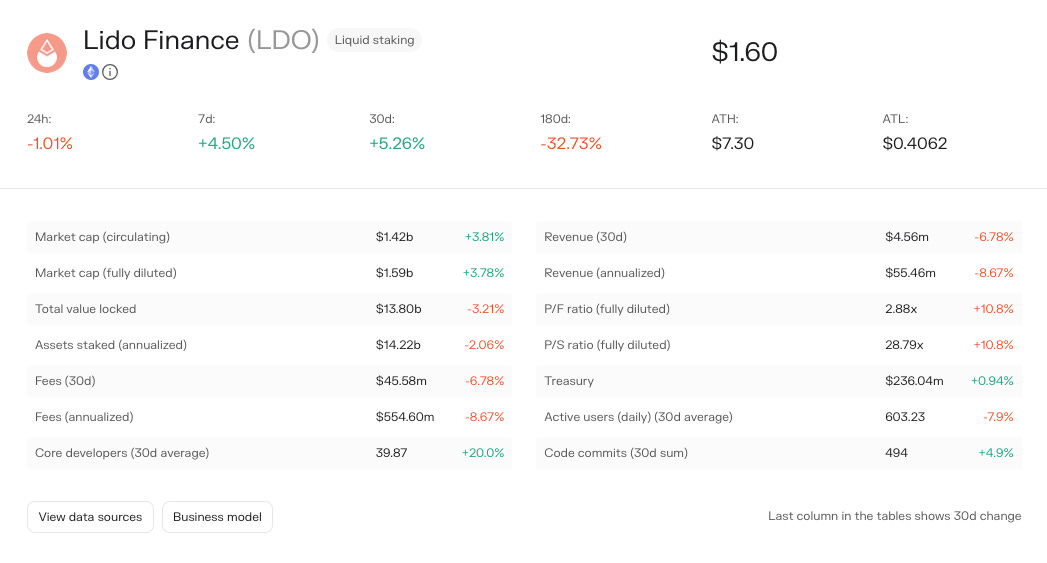

The current income of Frax ETH is $1.31 M per year, compared with Lidos profit level of $55.46 M per year. Judging from the current situation, the income of Frax ETH has a small effect on improving CR. But there’s a lot of room for growth in the LSD circuit, and once Lido’s monopoly is shaken, other protocols will see a big boost.

Frax ETH data from Tokenterminal

Lido data from Tokenterminal

Summarize

Overall, a conservative estimate of the current situation is that it will take 2-6 years to increase CR to 100%. This floating space is large and mainly depends on how Frax uses its own AMO.

If considered relatively optimistically, the rise in CRV and CVX will be of great help to the increase in CR. However, Frax will also face a dilemma at that time. Whether to sell these ticket rights to ensure CR, holding and locking up CRV and CVX will own the chain. If you upload liquidity management resources, you can immediately increase CR by selling them, but you will lose the incentives on the chain.

In terms of business potential, the current growth of RWA business is a key factor in promoting the improvement of CR. MakerDAO has absorbed a large amount of US dollar liquidity through sDAI. If sFRAX gradually gains market recognition, its growth potential will be far greater than other businesses. If Frax then chooses to allocate the RWA proceeds to a portion of the treasury to continue to improve CR, then the process of CR= 100% will be greatly improved.

So from an investment perspective we should pay attention to the following indicators:

Fund utilization and profitability of all AMOs

Price of CRV, CVX tokens

The growth of RWA’s business and whether the agreement’s treasury will receive dividends

Frax has built a large enough full-stack stablecoin system. We can see that both Fraxswap and Fraxlend are serving Frax Finance itself in addition to being launched on the open market. This is similar to the planned subDAO in the MakerDAO endgame:

What they have in common is that both MakerDAO and Frax are planning to expand horizontally around their core (stable currency) and build a full-stack product.

The difference is that MakerDAO decided to subcontract these functions to other subDAOs, while Frax is uniformly governed by frxGov.

The advantage is that Frax has captured almost all the right needs in the DeFi market, has a high ceiling, and is currently forward-looking in terms of mechanism design. But obviously the possible problem is a Frax Chain Layer 2 that covers stablecoins, trading systems, lending systems, cross-chain systems, LSD, and may be launched in the future. Such a huge system requires a very efficient and sound governance module. , at the same time, risk isolation between functions is also particularly important, testing the stability of future protocol functions and on-chain governance.