TL;DR

1. This report serves as a preliminary analysis of Frax Finance, providing an overview of its current ecosystem, describing its product suite, and exploring its future potential.

2. During the last bull run, $FXS outperformed Bitcoin due to key events such as exchange listings, emissions halvings, and airdrops, although it did not perform as well as the leading liquid staking derivatives due to the late launch of frxETH Coins like $LDO and $RPL reflected price surges. Meanwhile, $FRAX has shown great resilience in the face of market volatility, largely due to its advanced AMO strategy and robust $FXS staking.

3. Frax Finance is launching a series of major upgrades in line with major DeFi trends: FRAX V3 aims to strengthen its stablecoin mechanism and reduce dependence on $USDC; FinresPBC will enter real assets through Fraxbond (FXB); frxETH V2 focuses on decentralization Centralization and revenue optimization; the upcoming EVM-compatible Layer 2 solution FraxChain aims to improve scalability and security, providing a possible boost for the future growth of the protocol and $FXS.

4. Driven by a dedicated team and innovative mechanisms, Frax Finance is developing into a comprehensive DeFi ecosystem with strong synergy, and upcoming developments such as FRAX V3, frxETH V2 and FraxChain are bound to greatly promote It grows and creates value for $FXS token holders.

1. Background

Frax Finance, despite being one of the OG DeFi protocols, has always been a complex protocol for many newbies. Due to its diverse product line and complex mechanisms, it can feel a little intimidating for the first time. However, this is a protocol that everyone should know about as it is one of the most innovative protocols and stands out for its aggressive sector expansion. This report will serve as a beginner’s guide on Frax Finance, reviewing its current status, introducing its products, and examining its potential. As a beginner, not all aspects of the protocol have been covered. The purpose of this report is to help readers quickly gain a basic understanding of the protocol and understand the future development direction of Frax. Readers are encouraged to conduct thorough due diligence to fully understand the Agreement and its associated risks.

2. Introduction

Frax Finance launched in May 2019 as an algorithmically stable protocol and has continued to evolve into the complex DeFi technology stack it is today. Frax Finance now operates multiple business units, including three types of stablecoins, and is supported by three major infrastructures. Frax operates across multiple sectors including stablecoins, DEX, money markets, liquidity staking, and RWA is coming soon. As a result, Frax is one of the most innovative protocols in the DeFi space, but also one of the most complex.

3. Performance Overview

Since $BTC’s performance is often viewed as a beta for the crypto market, comparing coin prices to $BTC can give us a clearer picture of how a coin is performing. Coupled with the increase in key events, this allows us to gauge how the market views an agreement, i.e. if good news fails to trigger any positive price movement, the market may be diverting attention, making it a less attractive investment target.

From the chart, we can see that during the last bull run, $FXS followed the overall market and experienced a pretty decent price increase. Then between December 2021 and March 2022, $FXS outperformed $BTC, experiencing two significant price increases. These increases may be attributed to several positive events during that time, including the Binance listing on 12/10, the $FXS halving launch on 12/20, the $FPI airdrop distribution announcement on 2/19, and the FTX listing on 3/24. Subsequently, $FXS followed the overall market without any significant deviation. Recently, although the Frax team has released news about future plans, $FXS has not been as responsive as before. This may be due to the prevailing bearish sentiment in the market at the moment, and further observation will be needed to see what happens when those catalysts actually arrive.

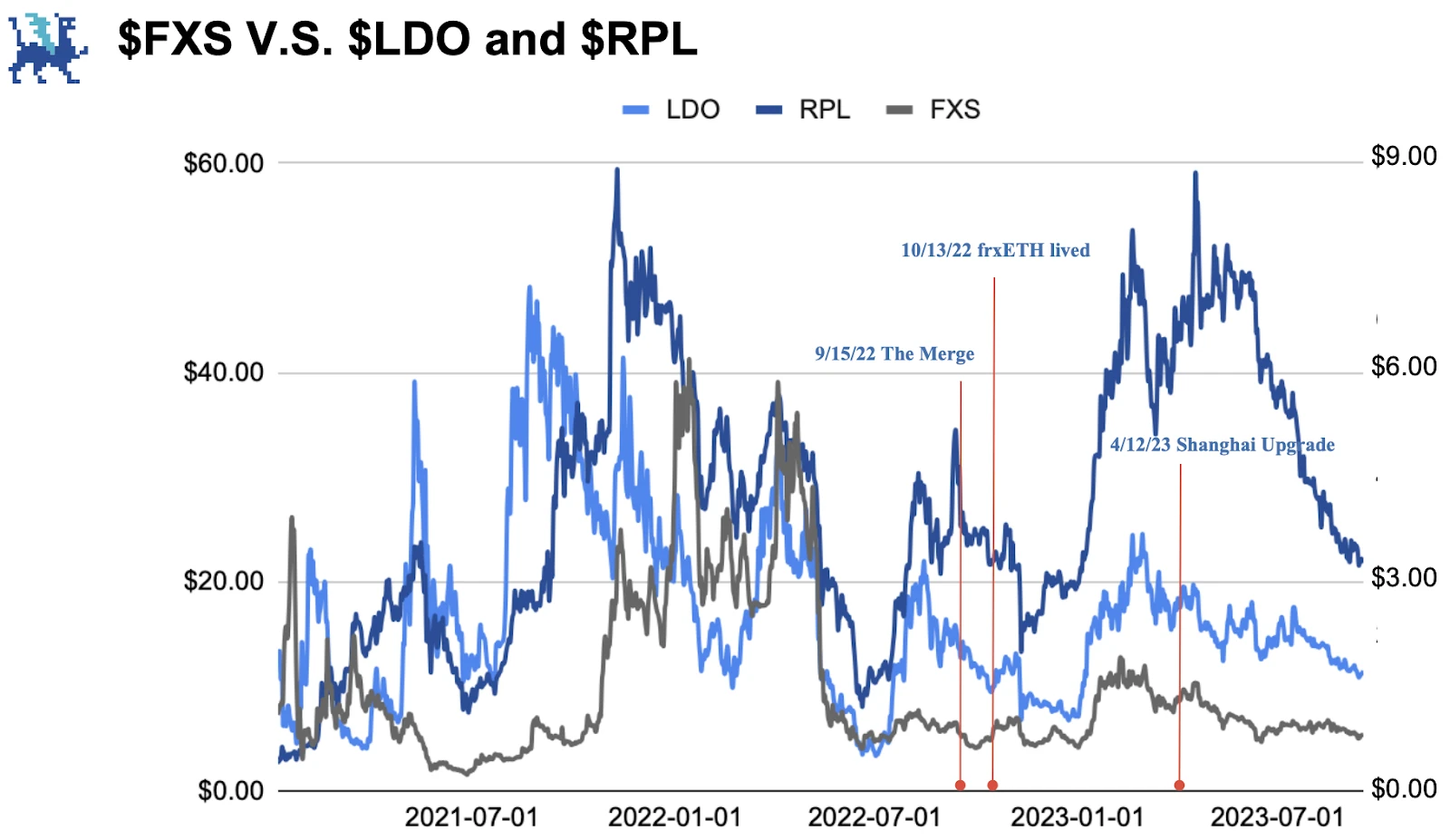

Comparing this to the two leading LSD narrative coins, $LDO and $RPL, we can see that $FXS, due to its late entry into the space, did not experience the same price increase as the other two as the Merge approached, but when the Shanghai Upgrade Experienced pumping water. With frxETH v2 coming online soon, it will be interesting to see how $FXS performs against $LDO and $RPL.

Comparing this to the two leading LSD narrative coins, $LDO and $RPL, we can see that $FXS, due to its late entry into the space, did not experience the same price increase as the other two as the Merge approached, but when the Shanghai Upgrade Experienced pumping water. With frxETH v2 coming online soon, it will be interesting to see how $FXS performs against $LDO and $RPL.

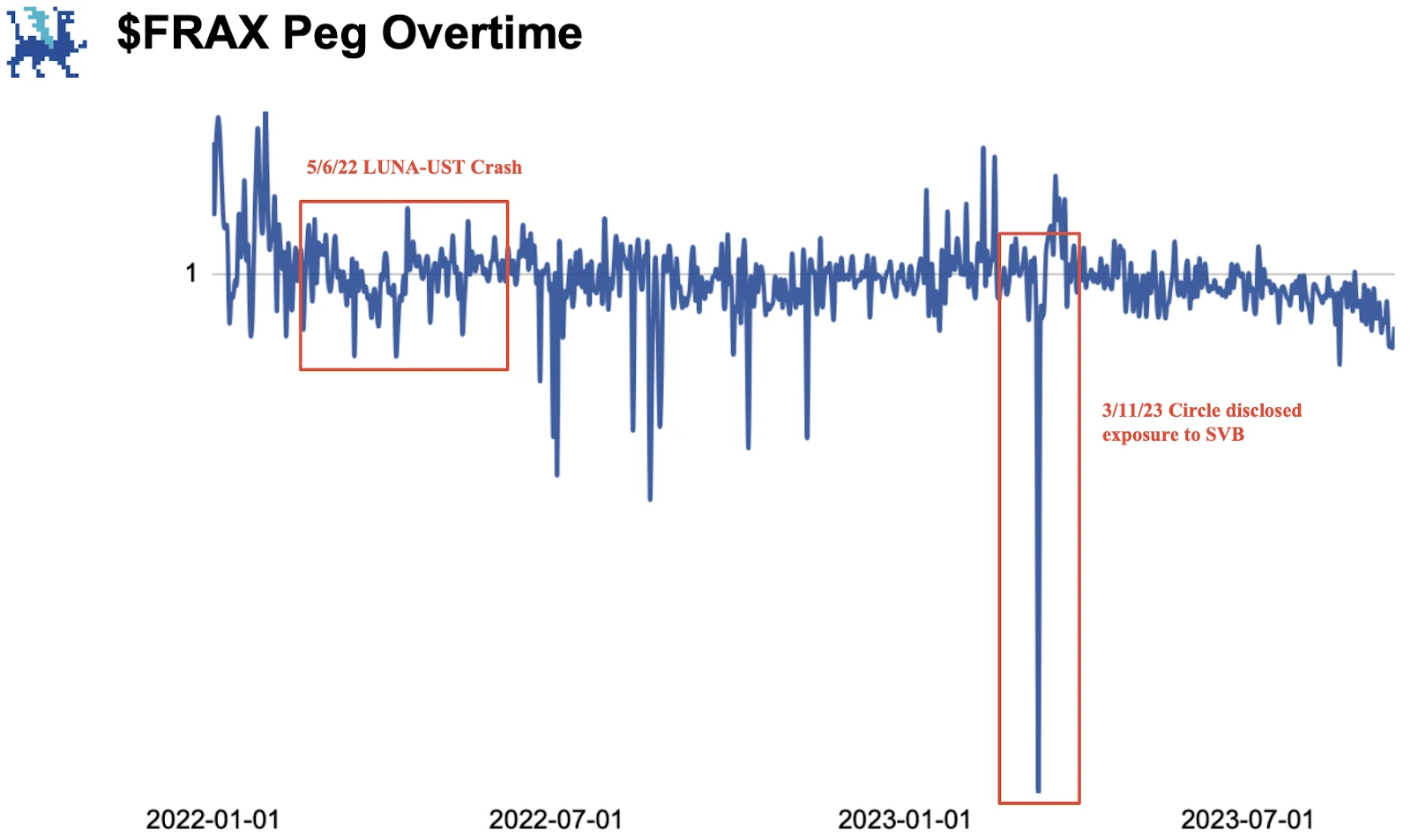

As an algorithmic stablecoin, $FRAX has maintained a fairly good peg over long periods of time. During the LUNA-UST collapse, $FRAX maintained a tight anchor range. While there is sometimes some slight unanchoring, there is always a quick rebound to prevent further rupture. The most significant unanchoring occurred when Circle disclosed its exposure to SVB. Since $FRAX is primarily backed by $USDC, $FRAX is affected. But given that the risk exposure was not large, the anchor returned to normal within a short period of time. Much of $FRAX’s stability can be attributed to the protocol’s complex AMO strategy and $FXS’s high lock-up rate, making Frax immune to the death spiral that other algorithmic stablecoins suffer.

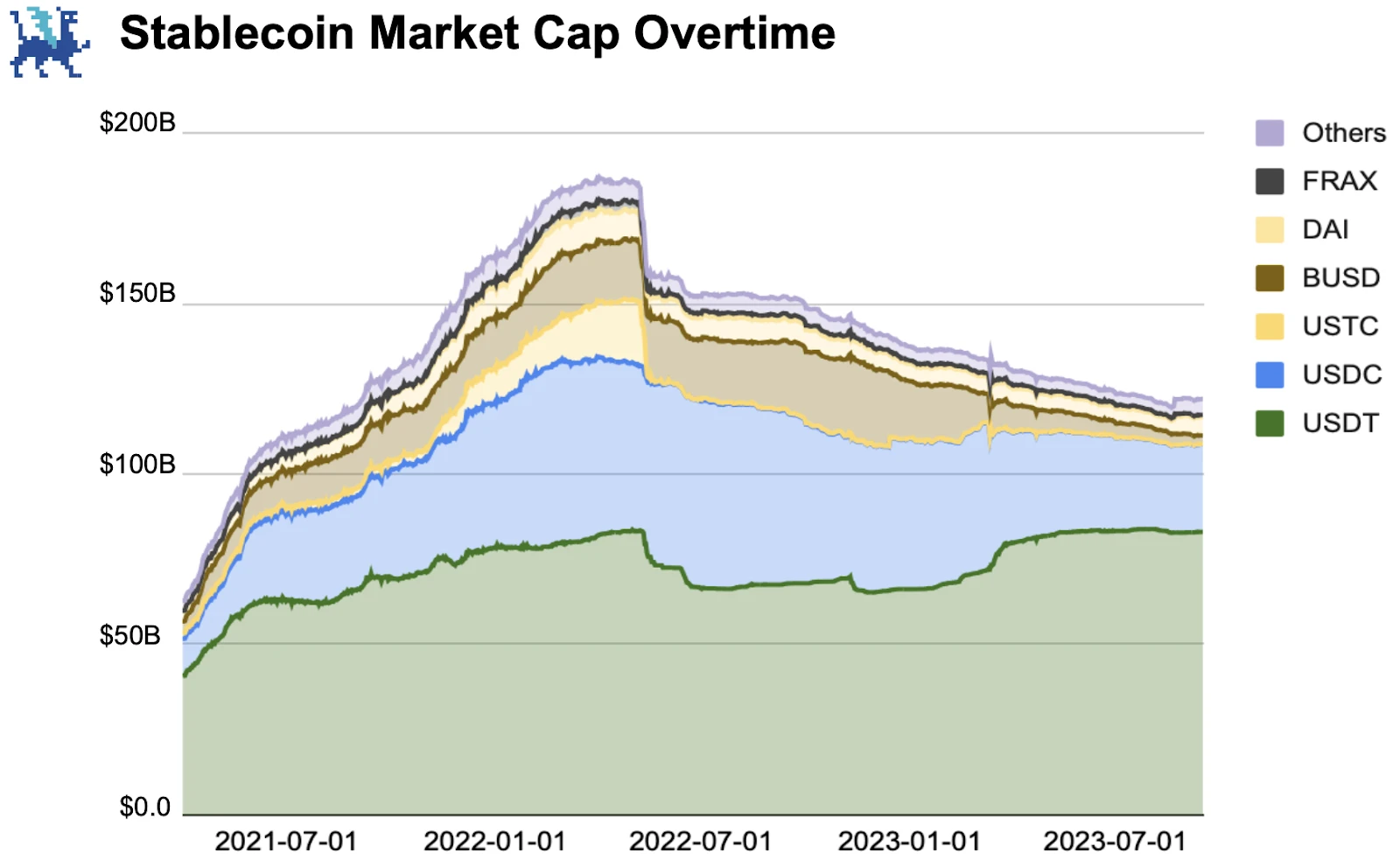

Although the collapse of LUNA-UST did not destroy Fraxs peg, the event still triggered a massive outflow of liquidity, causing the market cap of the stablecoin to drop sharply, especially for decentralized stablecoins like $DAI and $FRAX . The subsequent SVB incident further reduced $USDC’s market share and liquidity shifted towards $USDT, which we have seen as the only stablecoin to see consistent market cap growth since 2023.

Although the collapse of LUNA-UST did not destroy Fraxs peg, the event still triggered a massive outflow of liquidity, causing the market cap of the stablecoin to drop sharply, especially for decentralized stablecoins like $DAI and $FRAX . The subsequent SVB incident further reduced $USDC’s market share and liquidity shifted towards $USDT, which we have seen as the only stablecoin to see consistent market cap growth since 2023.

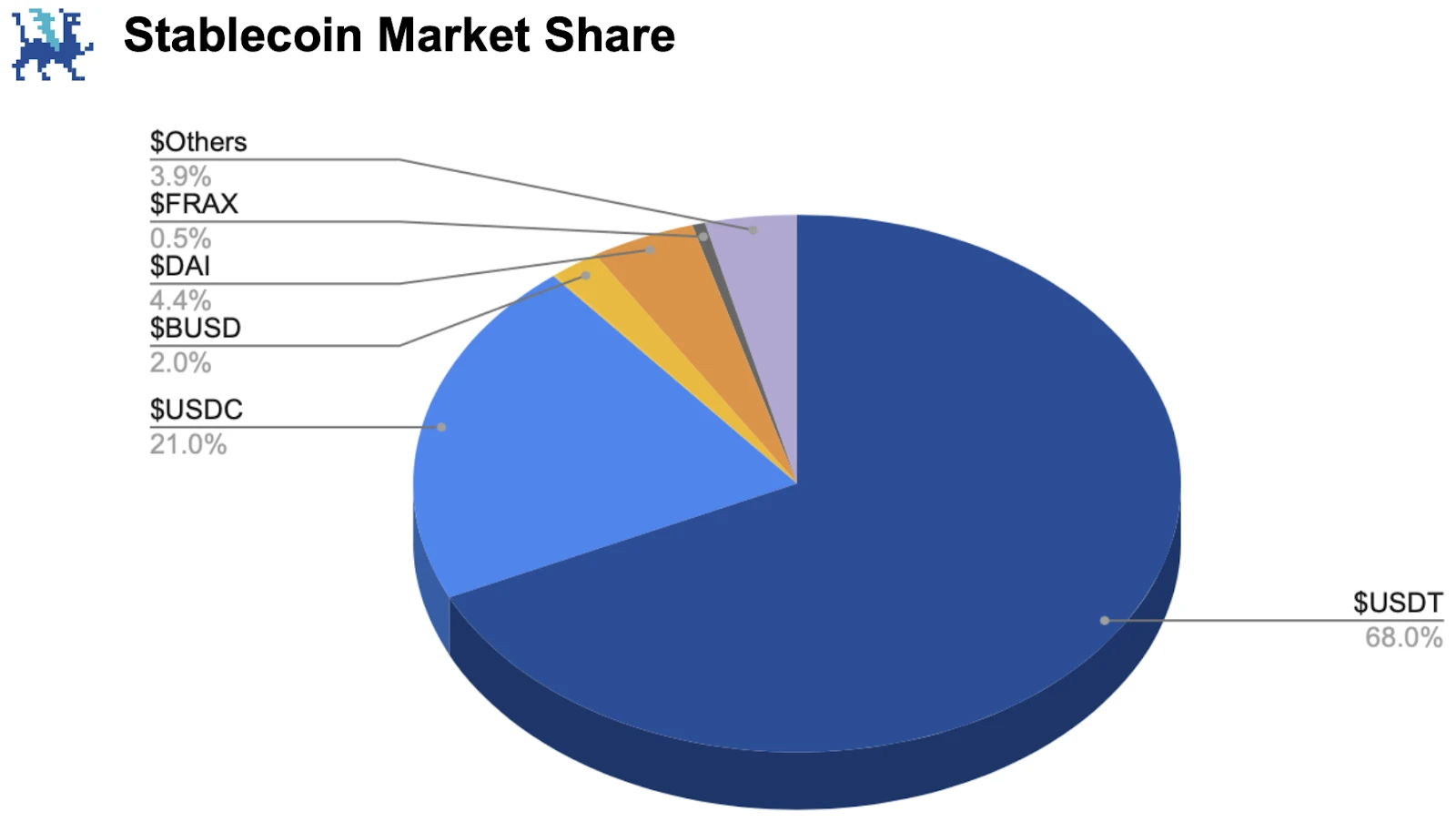

Two other key performance indicators for Frax are stablecoin market share and LSD market share. Although $FRAX is the second largest decentralized stablecoin, its market share is only 0.5%, which is 8.8 times farther away from $DAI and 136 times farther away from $USDT. This gap is caused by a variety of factors. Most importantly, centralized stablecoins serve as a key entry point for new crypto users, as new users primarily use CEX initially. The huge liquidity gap and adoption rate also contribute to this huge gap. As long as there aren’t any major factors driving users away from centralized stablecoins, this gap is likely to persist for quite some time.

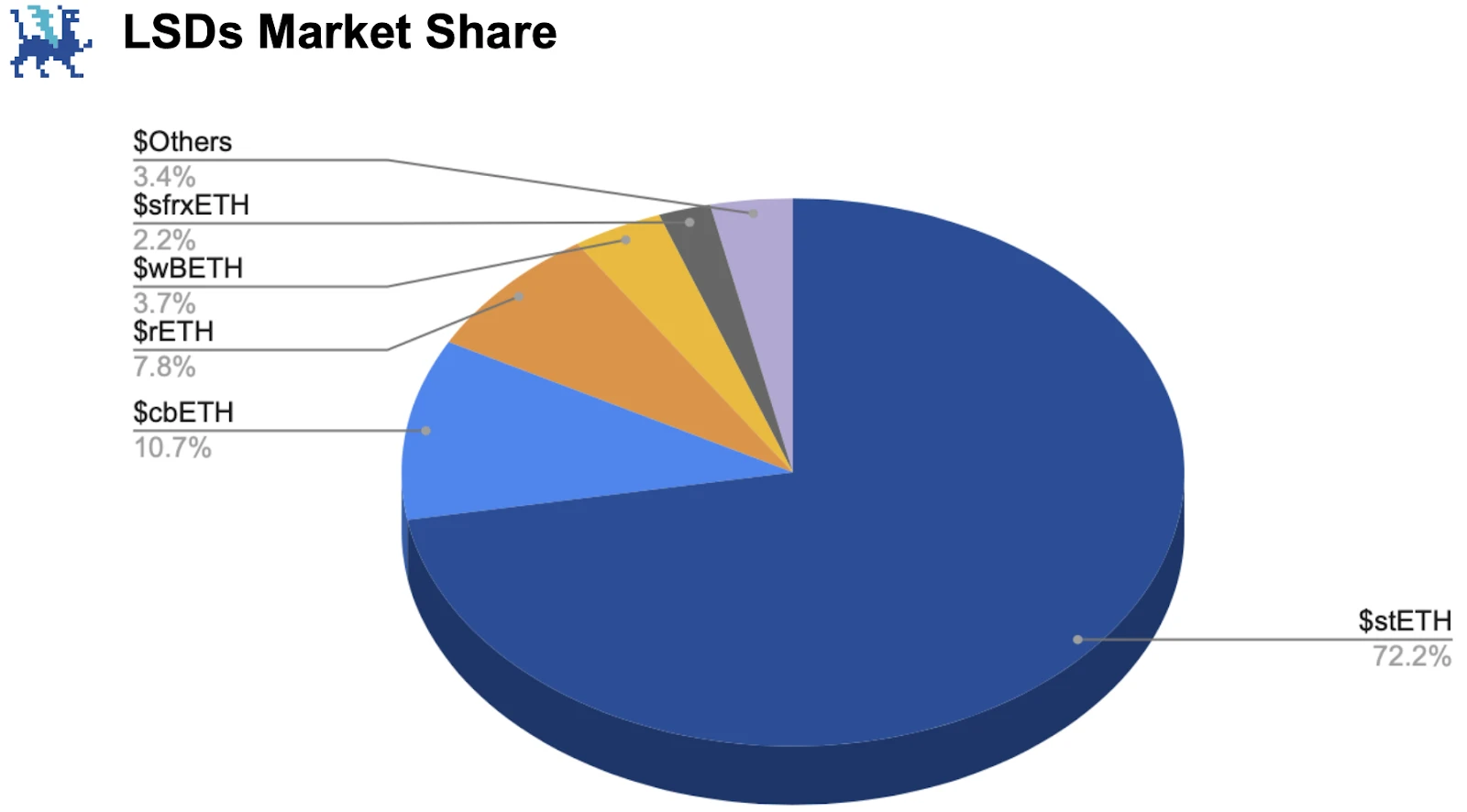

When it comes to LSD market share, Frax is doing better. Apart from Lido, sfrxETH has a very small market share gap with the other three major LSDs. The main reasons are their higher yields and the regulatory pressures CEXs face. With the arrival of frxETH V2, it is expected that Frax’s growth in the LSD space will continue to outpace its growth in the stablecoin space.

When it comes to LSD market share, Frax is doing better. Apart from Lido, sfrxETH has a very small market share gap with the other three major LSDs. The main reasons are their higher yields and the regulatory pressures CEXs face. With the arrival of frxETH V2, it is expected that Frax’s growth in the LSD space will continue to outpace its growth in the stablecoin space.

4. Agreement mechanism

Frax Finance is one of the most mechanically complex protocols in the DeFi space. Its ever-expanding product line and business units allow the protocol to essentially have its own ecosystem of various stablecoins and the DeFi infrastructure that supports stablecoin growth. In this report, we classify the three stablecoins released by Frax as flagship products and consider the supporting mechanisms as core infrastructure. The concept and importance of each stablecoin is presented, as well as how this infrastructure contributes to business operations.

4.1 Flagship product

4.1.1 Frax

FRAX is the first USD-pegged stablecoin issued by Frax. Unlike DAI, the largest decentralized stablecoin by market cap, which is over-collateralized, Frax is an algorithmic stablecoin partially backed by USDC and Frax’s native token, FXS. FRAX is always designed to be equal to 1 USD, and how 1 FRAX is collateralized is determined by market dynamics. Initially, FRAX is 100% collateralized by USDC, and the protocol’s algorithm will gradually reduce the Collateralization Ratio (CR) based on market demand. For example, a CR of 85% means 1 Frax is backed by $0.85 USDC and $0.15 FXS. The higher the demand, the lower the CR and vice versa. Since Frax is always pegged to $1, when the anchor becomes imbalanced, arbitrageurs step in, along with the protocol’s algorithm.

FRAX is currently in its V2 version, which uses multiple automated market operations (AMOs). Essentially, AMOs are smart contracts that perform open market operations (i.e. mint, burn, deploy FRAX) to keep FRAX pegged to $1. In V1, the protocol uses only one AMO, the Core Stability Module, to dynamically adjust CR to maintain the $1 peg. AMOs are one of the core mechanisms leading to Frax’s success. In the next section, the underlying concepts are explained in more depth.

One final note is that in 2023, the DAO has voted to increase CR to 100% as this is the safest way to continue FRAX expansion. Although CR offers greater flexibility and capital efficiency, the DAO has decided that it is no longer needed given Fraxs mature state, and the use of AMOs can still make FRAX highly capital efficient.

4.1.2 FPI

Frax Price Index (FPI) is the second stablecoin released by the protocol. It is designed to maintain purchasing power by being tied to real inflation, as defined by the Consumer Price Index for All U.S. Cities (CPI-U). Frax uses a specialized Chainlink oracle to obtain and report the U.S. federal government’s inflation rate and apply that rate to FPI’s redemption price. Since the anchoring of FPI is closely related to the inflation rate, the redemption price of FPI will rise (or fall) with inflation (or deflation), which means that users who exchange other assets for FPI are predicting that the purchasing power of CPI will Grow faster than the assets being sold.

The motivation behind FPI is to create the first on-chain stablecoin that can be used to represent transactions, value and debt. Using FPI as a baseline measurement can help determine whether the value of treasury or revenue is growing or declining relative to growing inflation, a practice that could be useful for DAO operations or similar activities.

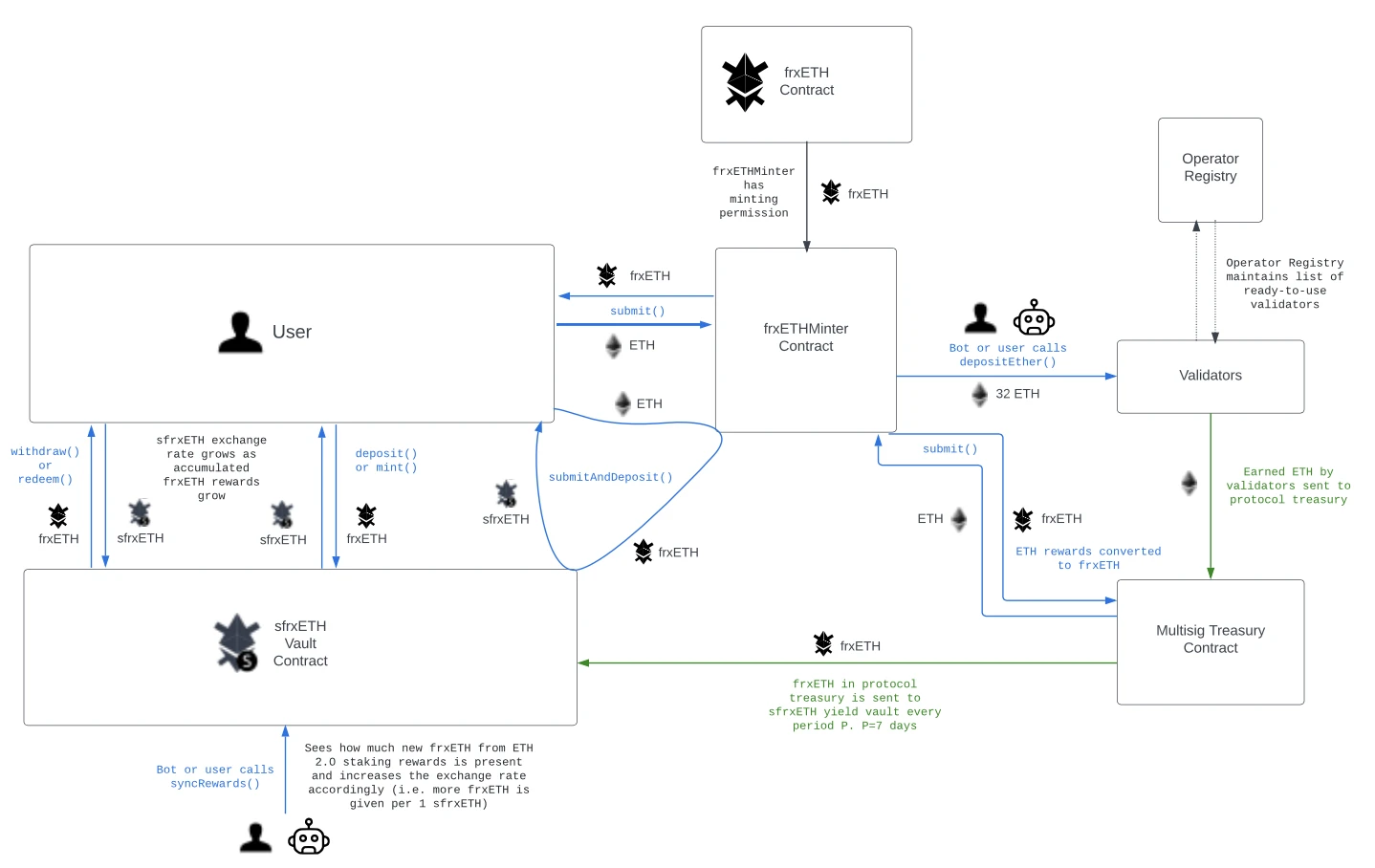

4.1.3 frxETH

Frax Ether (frxETH) is the third stablecoin released by Frax. It is pegged to ETH and has zero collateral rewards. Users can stake frxETH to earn sfrxETH, thereby receiving all staking rewards. Every uncollateralized frxETH contributes to sfrxETH’s earnings. Therefore, each sfrxETH earns a higher staking reward than ETH, which is why the yield on sfrxETH is higher than all other LSDs. Users can provide fexETH-ETH liquidity to the Curve pool and earn trading fees and launch rewards. Because Frax holds a large amount of $CRV and $CVX, it can direct a large amount of rewards to the pool, thus incentivizing liquidity provision.

The launch of frxETH/sfrxETH represents Frax’s strategic expansion into the LSD narrative and deepens its impact in the DeFi ecosystem. Frax cleverly used its prominent position in the Curve War to successfully erode the market share of blue-chip LSDs like stETH and rETH. With Frax about to launch the V2 version of Frax Ether, another wave of adoption growth is expected.

4.2 Core Infrastructure

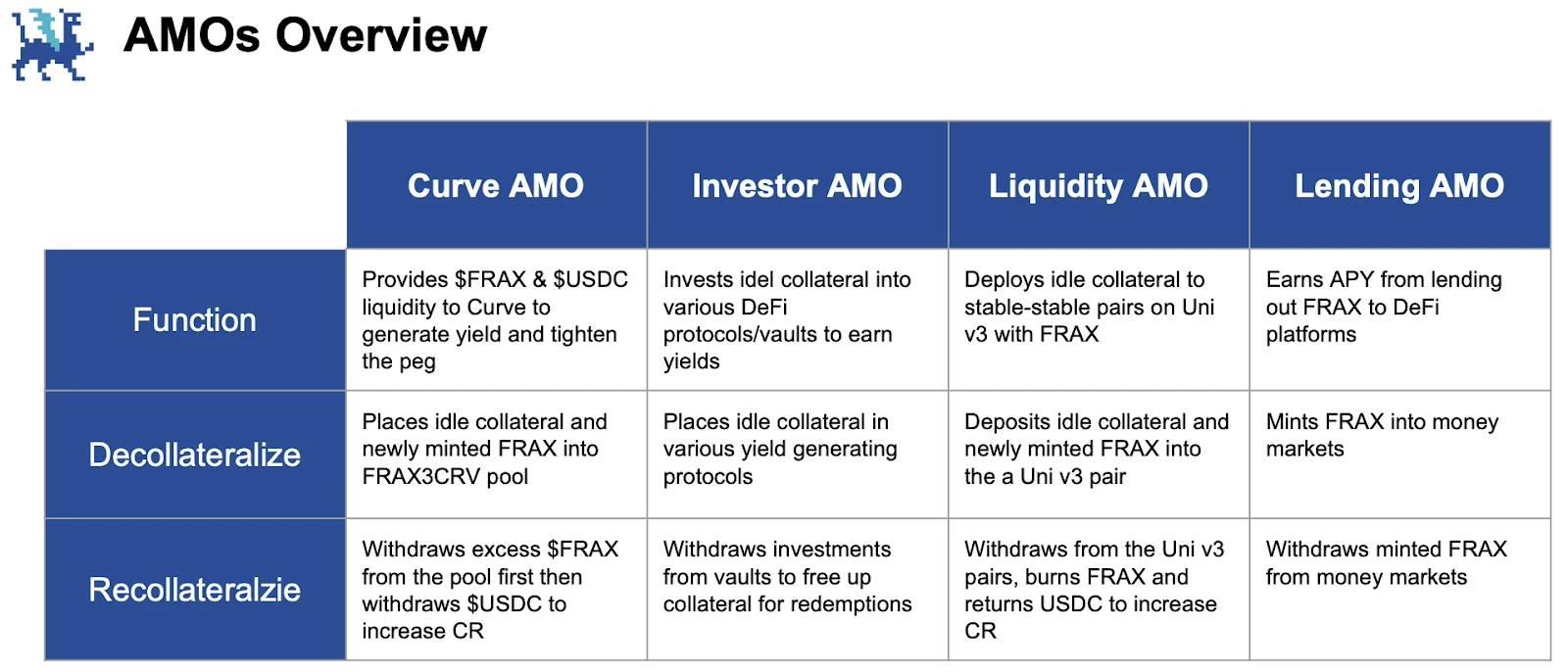

4.2.1 AMOs

For stablecoin protocols like Frax, maintaining stability is crucial. Not only would unlocking erode user confidence, it could also cause a chain reaction that tears the protocol apart. Algorithmic Market Operations (AMOs) are smart contracts that perform different currency operations to maintain the stability of FRAX. Frax Finance has grown from a single AMO in V1 to now four major AMOs in V2. While each has slightly different operations, AMOs all share three attributes: decollateralization - the part of the strategy that reduces CR, market operations - the part of the strategy that operates in equilibrium and does not change CR, and remortgage - which increases CR strategy part.

4.2.2 Fraxswap

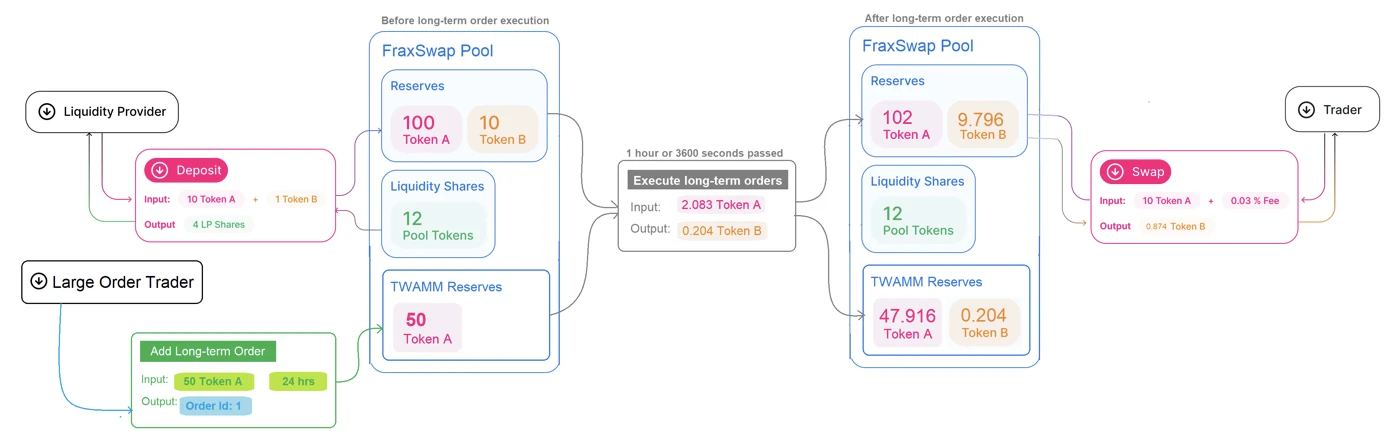

Fraxswap is the first Constant Product Market Maker (CPMM) combined with a Time Weighted Average Market Maker (TWAMM) to optimize the execution of long-term orders, such as order pools and aligned order expirations, and to efficiently handle large Order. The purpose of Fraxswap is to enable protocols to effectively enforce the monetary policy of their stablecoins. More specifically, Frax will use Fraxswap to:

- Use AMO profits to buy back and destroy FXS

- Mint new FXS to buy back and destroy Frax

- Mint Frax to purchase hard assets via seigniorage

Fraxswap is completely permissionless, allowing other protocols and DAOs to leverage it for monetary policy. Fraxswap V2 is also under development and will support centralized liquidity (the current version is based on Uniswap V2) and combine it with related asset liquidity to further expand its functionality.

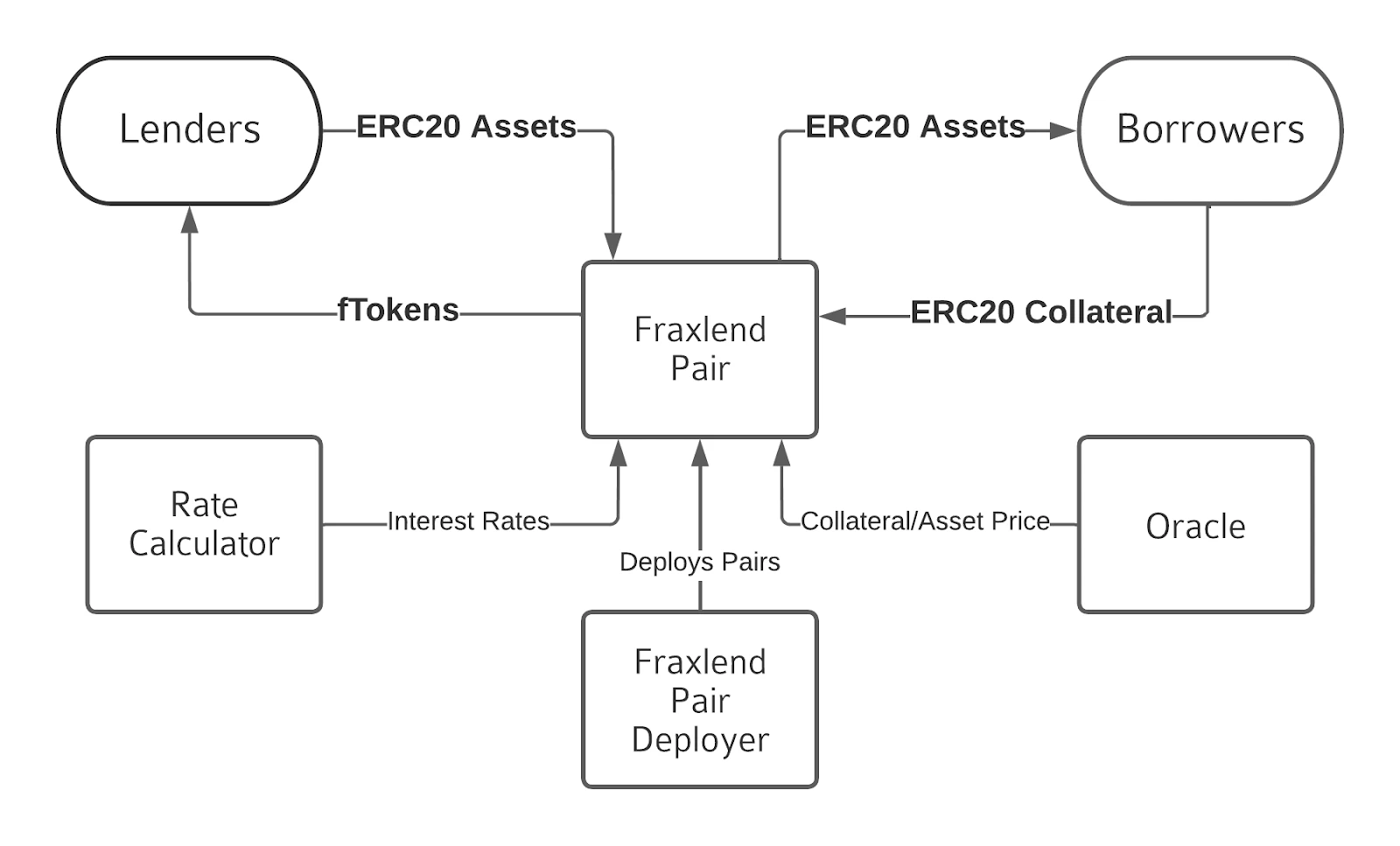

4.2.3 Fraxlend

Fraxlend is Frax Finance’s native currency market that supports lending and borrowing activities using ERC-20 pairs. Each pool is overcollateralized and independent, protecting the protocol from counterparty risk and the threat of bankruptcy. As a stablecoin protocol, Frax’s top priority is to expand usage and adoption of its stablecoins in a natural way, with Fraxlend serving as an important part of achieving this goal. Increases the use of FRAX as a currency in DeFi by allowing users to own CDPs (debt positions) on FRAX. Notably, Fraxlend adopts a no-fee model as an incentive to encourage adoption. Like other infrastructure, Fraxlend also has v2 plans that may introduce low-collateral lending to the platform.

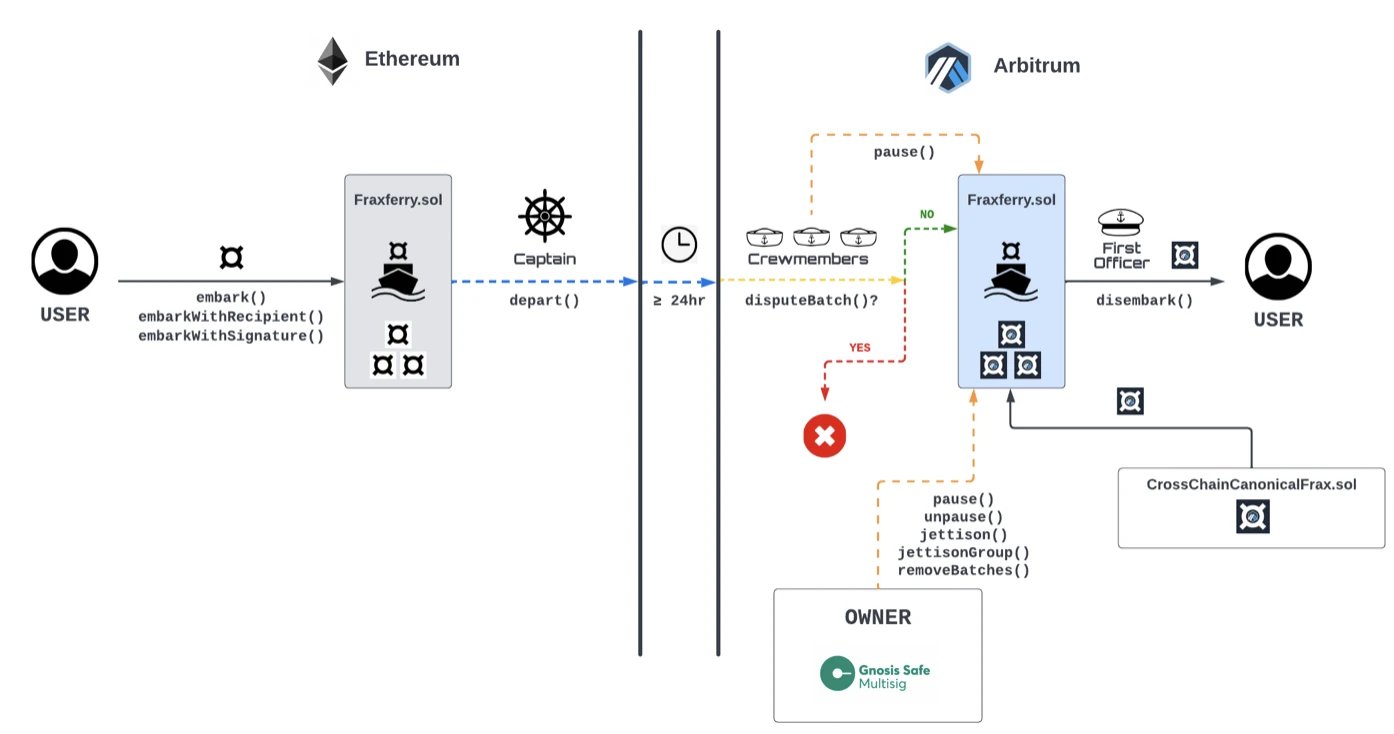

4.2.4 Fraxferry

Frax Finance has launched Fraxferry to enable a seamless bridging mechanism for protocol multi-chain expansion. Fraxferry bridges user assets in a slower but more secure way, designed to maximize security. The v2 version is also about to be launched, which will make the mechanism more decentralized.

The functionality bridged via Fraxferry is as follows:

1. The user initiates the process by sending tokens to the ferry contract.

2. A designated captain will check and batch the transactions.

3. There is a 24-hour waiting period to allow for further verification before the transfer occurs.

4. Upon execution, the system will ensure the transaction is valid by comparing the hashes.

5. Token Economy

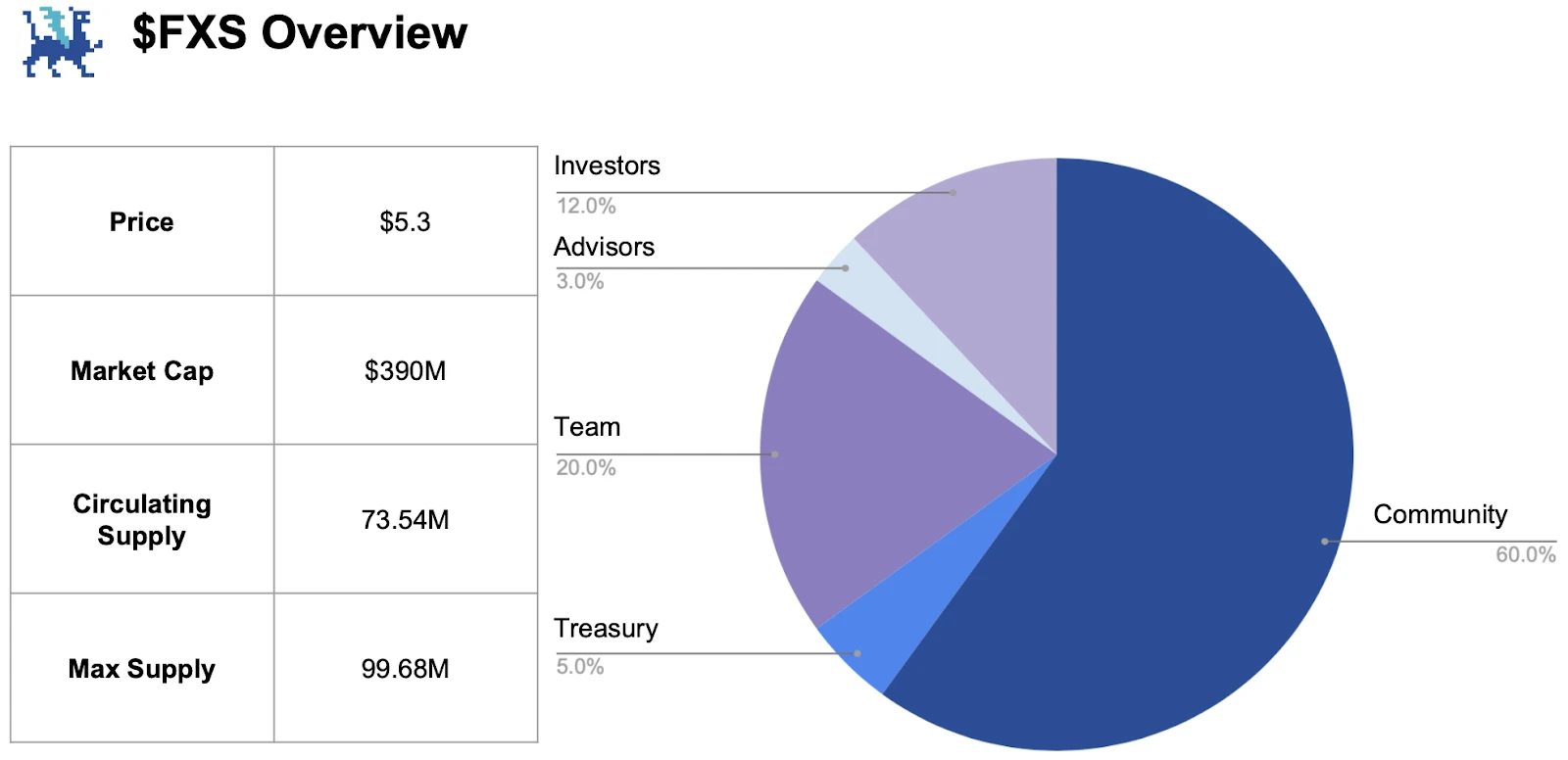

Frax Share ($FXS) is Frax Finance’s staking and governance token, with all earnings and utility focused on $FXS. More specifically, in order to enjoy all the benefits, users are encouraged to lock their $FXS to earn $veFXS, which is the same as Curve’s veToken model. $veFXS holders enjoy voting rights, scale farming boosts, and cash flow from AMOs, Fraxlend loans, and Fraxswap fees. Currently, there are 37.484M $FXS locked, accounting for 50.88% of the circulating supply and 37.6% of the total supply. Notably, post-FIP-256, the protocol will conduct buybacks whenever $FXS falls below $5 and $4, a move that solidifies the token economy by signaling the token’s implied valuation base Study proposal.

6. Growth drivers

Due to its diverse business segments, Frax Finance has multiple upcoming upgrades, which also makes it a good fit for different key narratives that could be a significant tailwind for its future growth. This section reviews them and explores their prospects.

6.1 FRAX V3

Although not many details have been released yet, FRAX V3 aims to eliminate dependence on $USDC and create a new decentralized stablecoin mechanism with the goal of greatly improving the robustness of the protocol. According to Frax co-founder Sam Kazmien, FRAX V3 will abandon the current anchoring mechanism and not rely on legal currency. But more details are yet to be released by the Frax team. Another highlight of v3 is its expansion into the RWA field. A non-profit entity called FinresPBC has been launched to take advantage of attractive U.S. government bond yields. FinresPBC facilitates off-chain trading of U.S. government bonds, and users can participate through Fraxbond (FXB), which can be exchanged for $FXS. RWA is a dominant narrative in the current DeFi market, and this expansion may reflect the success of MakerDAO, whose token price has performed quite well recently due to its RWA operations. This, combined with a more robust stablecoin mechanism, could drive FRAX adoption to new highs.

6.2 frxETH V2

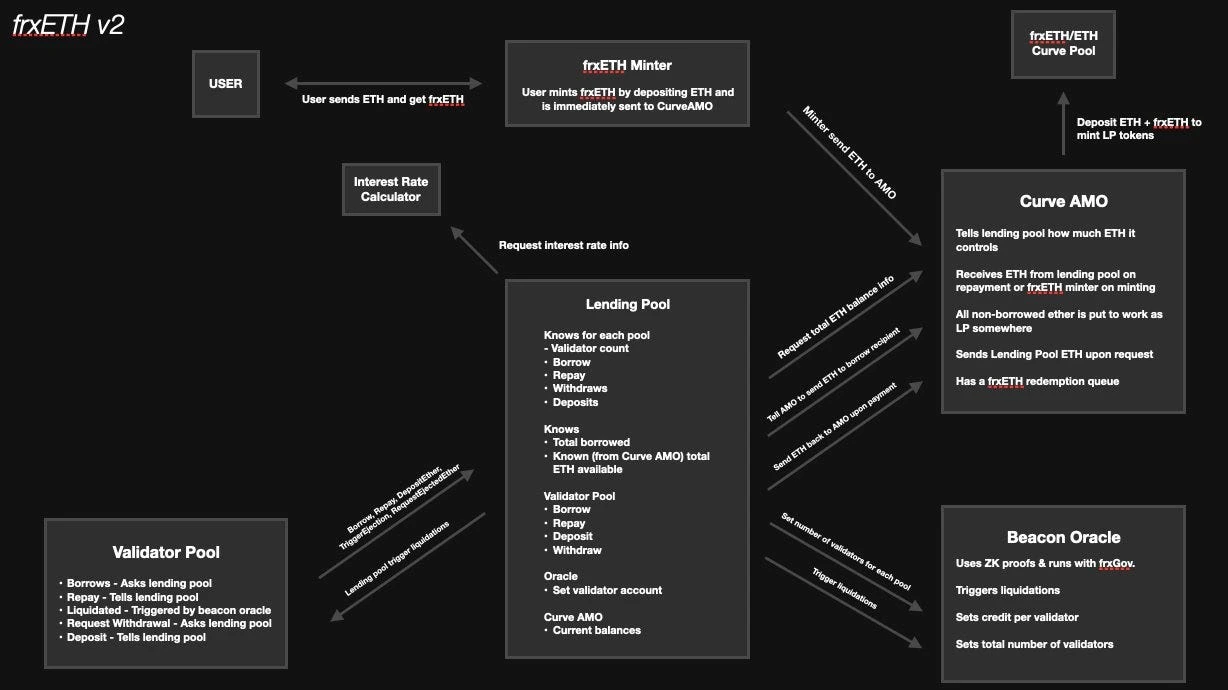

Regarding frxETH, an ongoing complaint from users is the centralization of the mechanism, where the protocol relies on its internal validators. In response, frxETH V2 is about to be launched with the aim of decentralizing the mechanism while providing users with the same or higher yields. At its core, frxETH V2 contains two innovations: usage-based interest rates and a decentralized lending market. Frax facilitates these modifications by treating the LSD market as a lending (stakers) and borrowing (validators) market.

Through the peer-to-pool model, anyone can provide collateral and borrow ETH from stakers to become a validator. Rates are dynamically determined based on utilization. Ultimately, there will be a dynamic market for lenders and borrowers of LSD, facilitating the growth of Frax LSD.

6.3 FraxChain

In a podcast Sam did with FlyWheel DeFi three months ago, he revealed that the protocol would be launching its own EVM-compatible L2 called Fraxchain. Although not many details have been released yet, there are two highlights of this upcoming L2. First, it will be a hybrid rollup, using Optimistic architecture but also integrating ZK technology for enhanced security. Secondly, frxETH will be used as gas fee. The importance of frxETH as a fuel token is that as demand increases, the supply of frxETH will decrease, thereby increasing sfrxETHs earnings and further expanding its LSD market share. Fees will flow to $veFXS holders, and combined with other revenue streams already flowing to $veFXS, the value accumulation of $FXS will be significantly enhanced. The launch of Fraxchain is scheduled for the end of this year, and with the L2 narrative brought about by Cancun Upgrade, market interest is likely to surge.

7. Growth potential

The above-mentioned growth drivers may significantly boost the performance of the corresponding areas. To further demonstrate Fraxs potential, this section will conduct a simple comparative analysis of the LSD market (one of Fraxs main business areas) to provide some insights into the protocols growth prospects.

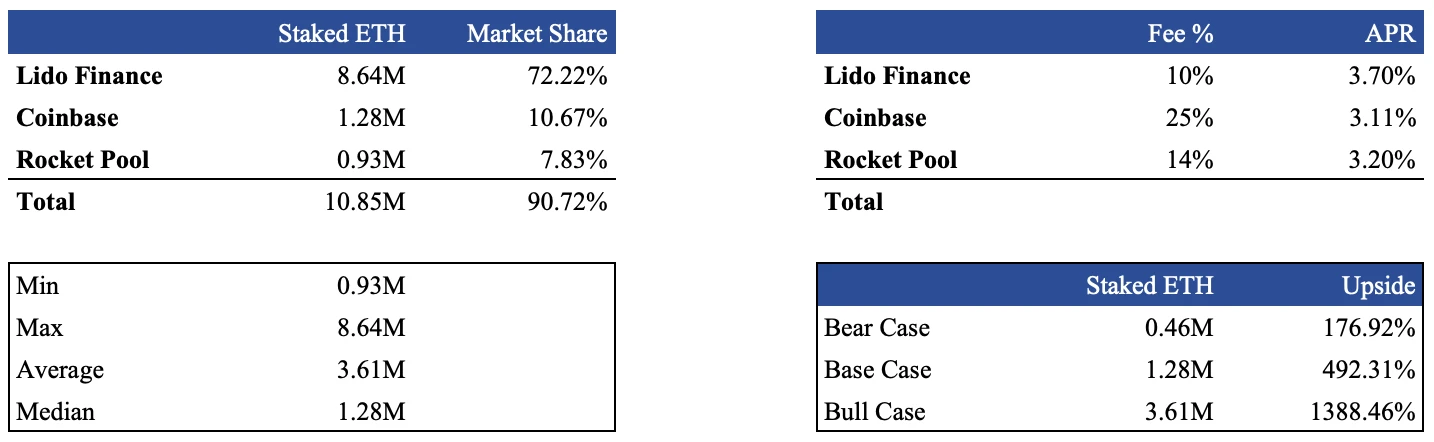

In terms of LSD market share, Lido, Coinbase, and Rocket Pool lead the way. For the purposes of this analysis, we will use the top three LSDs as a representative sample. Currently, the top three LSD protocols have a total of approximately 10.85 M of staked ETH, collectively accounting for 90.72% of the market share. The current amount of staked ETH on Frax is approximately 0.26M. Conservatively assume that the current numbers of the top 3 LSD protocols represent Frax’s targets and set 50% of Rocket’s volume, the median of the top 3 volumes, and the average volume of the top 3 as our bearish, benchmark and a bull market scenario, we can roughly estimate the potential growth upside for Frax LSD.

While this basic comparison highlights the potential of Frax LSD, it is important to realize that reaching the staked volume of the top 3 protocols is not necessarily a simple process, and that the process is affected by a variety of factors. However, this analysis clearly highlights the potential of Frax, and combined with the upcoming V2 update, the future is certainly bright.

(This analysis is a simplified approach to estimating Frax LSD’s potential growth, using the top protocols as a baseline, and their staked ETH amounts as targets. To make a more detailed forecast, there are several additional factors that need to be taken into account, This means that this analysis should only be viewed as a rough measure of Frax ether.)

8. Conclusion

Starting out as an algorithmic stablecoin protocol, Frax Finance has successfully transformed into a robust DeFi stack that encompasses every core area of the ecosystem. The team’s continued efforts are the main reason Frax is what it is today and will underpin its future growth. Its mechanics and products have been cleverly designed to create a powerful synergy that may trigger a positive flywheel effect for the growth of the protocol and the accumulation of value in $FXS. Going forward, it is recommended to pay close attention to FRAX V3, frxETH V2 and Fraxchain, as these will be key developments that will determine the future of Frax.

references

https://docs.frax.finance/?source=post_page-----9c23b056d46c--------------------------------

Disclaimer: This report is by @GryphsisAcademy contributor@BC 082559 Completed original work. The authors are solely responsible for all content, which does not necessarily reflect the views of Gryphsis Academy, nor the views of the organization that commissioned the report. Editorial content and decisions are not influenced by readers. Please be aware that the author may own the cryptocurrencies mentioned in this report. This document is for informational purposes only and should not be relied upon for investment decisions. It is strongly recommended that you conduct your own research and consult with an unbiased financial, tax or legal advisor before making any investment decisions. Remember, the past performance of any asset does not guarantee future returns.