Original author: PSE Trading

As expected, the Federal Reserve has decided to keep its policy rate unchanged at 2 p.m. Wednesday.

The impact on the market is immediate. Stocks and BTC rebounded quickly after Powell spoke - with risk sentiment running high.

FOMC has no decision to raise interest rates, Bitcoin rises

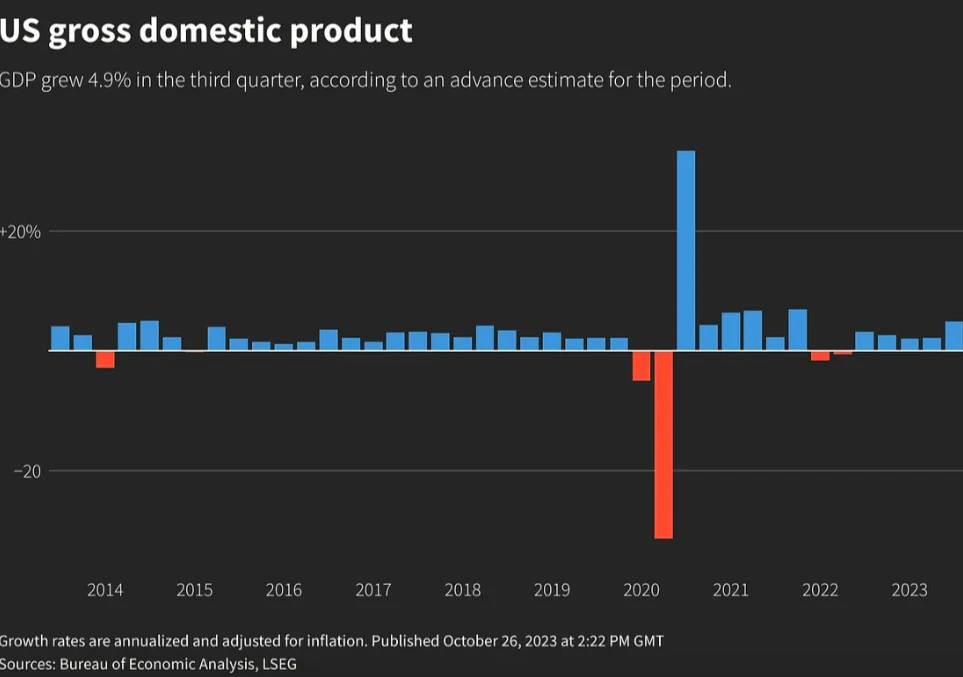

The decision to keep rates on hold came despite strong economic indicators, such as 336,000 jobs added in September, quarterly real GDP growth of 4.9%, and core PCE inflation rising by a third 0.3% month-on-month in September, above target. .

US economy resilient: Real GDP grows 4.9% in Q3

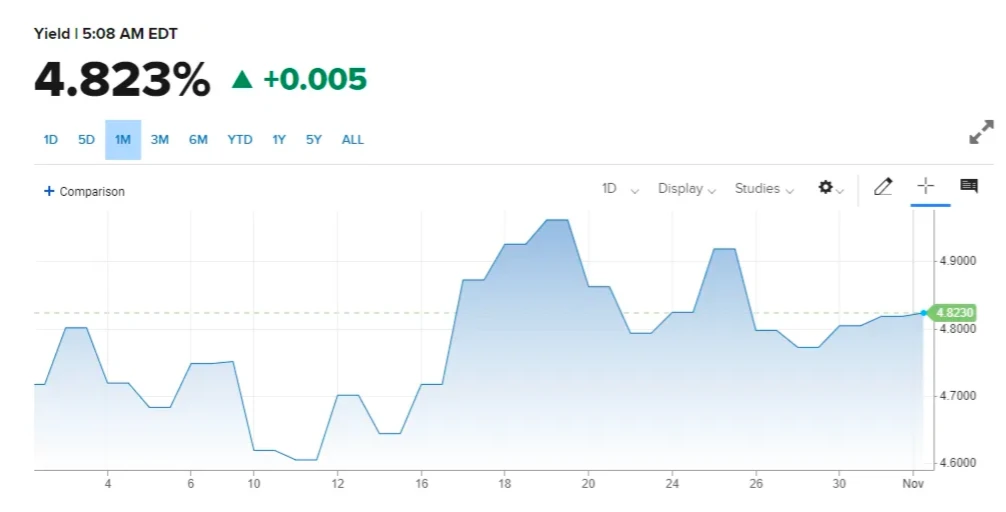

The main factor in this impact was the rapid rise in the ten-year Treasury note, which reached about 5%, which led the Federal Reserve System Treasury Department to pause raising interest rates.

However, President Powells recent remarks reconfirmed that the underlying risks to upward inflation have changed as a result.

The language of the official statement and Powells comments suggest that further rate hikes are still possible.

In our baseline scenario, core CPI is expected to rise 0.3% month-on-month over the coming October, while the Federal Reserve is not expected to raise interest rates in December. However, if core CPI reaches 0.4% m/m in October, a 25 basis point rate hike in December will become the most likely outcome.

Reason for the pause: Skyrocketing national debt

The rapid rise in the national debt has made Federal Reserve officials more stringent in raising policy rates, increasing the likelihood that the Fed will not raise rates further during the current cycle.

Yields soar: UST hits 5%

However, there are still upside risks to inflation, meaning the committee cannot rule out further rate hikes. At present, the policy interest rate is proposed to be suspended, but it is consistent with the market pricing of higher and longer and favors an interest rate increase rather than an interest rate cut.

At the last Federal Open Market Committee (FOMC) meeting in mid-September, the Summary of Economic Projections (SEP) showed that Federal Reserve officials were increasingly confident that inflation would increase toward target without the economic resources to achieve it. A soft landing for real goals.

This was largely a combination of strong activity and employment growth alongside worrying wage growth and a core soft three months from June to August.

Given that the prospect of suffocating inflation has been overstated many times over the past two years, Chairman Powell and the committee have been very strict in avoiding declaring a victory for inflation or marking the end of interest rate hikes. Instead, twelve of nineteen Federal Reserve officials said another 25 basis points of interest rate increases would be needed this year.

Hawkish Likelihood: The door remains open for more rate hikes

Data released after the September meeting showed that remaining open to further rate hikes appeared to be far-sighted. Rather than ending employment growth, it accelerated to 336k in September. Although readings have been lifted this time by a short-term correction, moving spindles are still above 200,000 a month, well above the roughly 100,000 that would match a natural reversal in labor supply. Activity has also accelerated, with the turnaround in lights coming in at around 2%, compared with a 4.9% turnaround in the third quarter.

For Fed policy, core CPI and PCE inflation accelerated to over 3% annualized in September. This suggests that core inflation, which was close to 2% between June and August, was a temporary soft spot caused by declines in air fares and used car prices and is not here to stay.

PCE inflation accelerated to above 3% annual rate in September

Hulls non-core services swell, also known as supercore, remains sticky, growing faster than pre-pandemic levels, and in the most recent September data, supercore accelerated.

A month ago, we had no idea that this series of data would lead to a 25 basis point rate hike by the Federal Reserve at the November Federal Open Market Committee (FOMC) meeting. That would keep the pace of raising interest rates at each meeting in line with Fed officials emphasizing that the 10-year Treasury note has risen nearly 5%, making Fed officials more determined to raise rates further.

Fed: Cautious and data-dependent

Despite this new firmness, Chairman Powell is expected to reiterate at the press conference that the Fed will remain data-dependent and will respond without skepticism if upside risks to inflation are confirmed. Powell is likely to clarify that the Fed is not trying to target a specific 10-year level but is more concerned with the pace and volatility of sales. This suggests that if stabilization occurs, a rate hike by the Fed will still be possible.

Key words in the statement after the Federal Open Market Committee (FOMC) meeting about raising interest rates:

In determining the degree of additional policy tightening that may be achieved over time to restore 2 percent, the Committee will consider the degree of additional policy tightening of monetary policy, the effects of monetary policy on stagnation in economic activity and inflation, and economic and financial developments.

We expect this attitude to remain unchanged. A dovish surprise might be that if the phrase the degree of additional policy tightening that is likely to be appropriate is changed to the degree of additional policy tightening that is likely to be appropriate, then policymakers may retain the original level of policy tightening. In some languages, ethnic minorities may be excluded within twelve months, thereby increasing the likelihood.

Fed Speech: Volatility in Post-Meeting Statement

Indicators show that inflation in the United States has been increasing and job creation has remained low, although job growth in recent months has been concerning. Inflation levels remain soaring and the Economic Council remains alert to inflation risks. The U.S. banking system is strong and intelligent, but tighter credit conditions for households and businesses could lead to stress on the economy, employment and inflation, although the extent of these effects is not yet clear.

The Committees primary objectives are maximum employment and 2 percent inflation in the long run.

To support these objectives, the Committee has decided to maintain the target range for the federal funds rate at 5 – 1/4 to 5 – 1/2 percent.

federal funds rate

The Federal Funds Rate Committee will continue to evaluate new information and its policy implications for monetary policy. In determining the level of policy reductions required to achieve its 2 percent inflation objective, the Committee considers the cumulative tightening of monetary policy, the time lag in the currencys impact on the economy and inflation, and economic and financial developments. Additionally, the Committee will continue to reduce its holdings of Treasury and agency debt and mortgage-backed securities as previously announced.

The Committee is committed to bringing inflation back to its 2% objective. The Committee will focus entirely on current information about the economic outlook in assessing the appropriate stance of monetary policy.

The Committee remains prepared to adjust monetary policy if risks arise that may prevent the Committee from achieving its objectives. The Committees assessment will consider a variety of factors, including labor market conditions, inflationary pressures and expectations, and domestic and international financial developments.