Original author:@Yuki,PSE Trading Analyst

Since Ethereum switched to PoS, LSDFi came into being and became a new and eye-catching track. The reason why LSDFi has become the focus of the market is that it has re-innovated based on the Yield Bearing attribute of liquid pledge tokens. However, as the ETH pledge rate continues to increase and the pledge yield continues to decrease, the market space is continuously squeezed, and the development of LSDFi has come to a standstill.

Looking back, we have gone through three stages of development of the LSDFi track. From the competition of liquidity staking protocols, to LST becoming a new consensus circulating asset in DeFi, to the diversified and large-scale application of LST. Now, we are in a period of obvious development difficulties. This article attempts to clarify the current situation of the LSDFi track based on data, and explore where LSDFi will go in the future through the analysis of specific projects.

1. Looking at the current status of LSDFi track from data

1.1 The growth bonus period has expired, the development of the track has stagnated, and the decline in yields has led to the flight of funds from the track

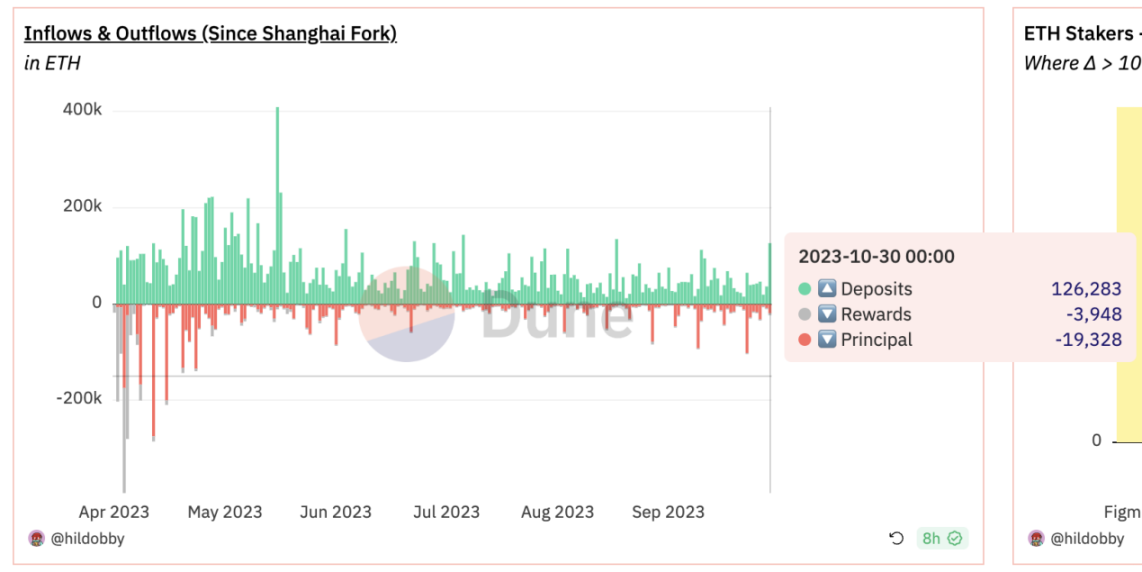

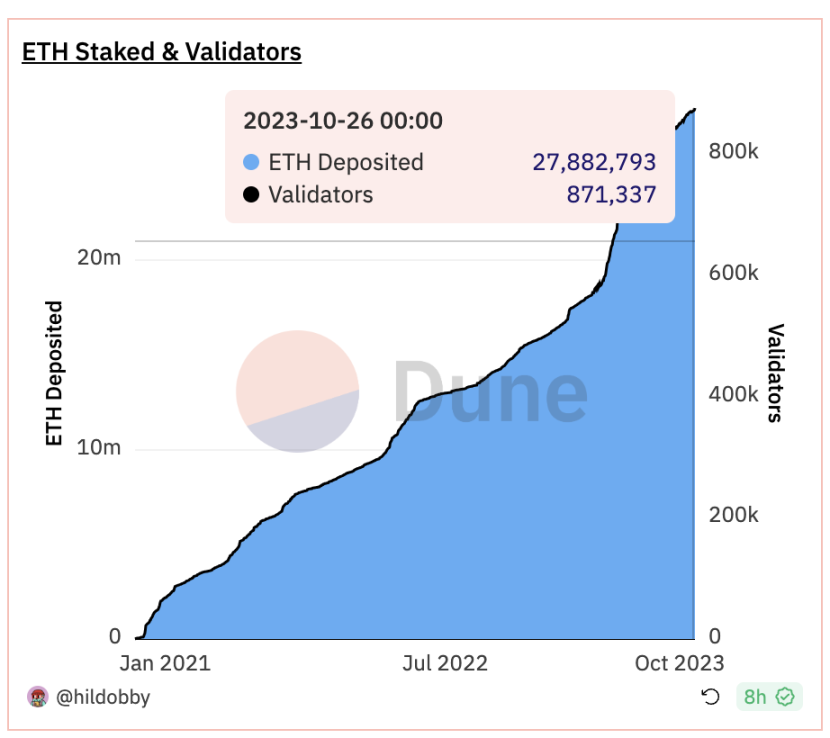

According to Dunesdata, judging from the number of net pledged ETH, the overall amount is flattening, and the number of Validators waiting in line to enter is also decreasing, and the period of violent pledge growth has passed. Correspondingly, the total TVL of the LSDFi track (the current total TVL is 839 M) has been in a state of significant slowdown in growth since September 26 this year, and has even experienced negative growth. It can be expected that in the absence of paradigm innovation, the LSDFi track as a whole will not experience significant growth in the future.

There may be two reasons for this situation. On the one hand, due to the lack of growth in staking within the Ethereum ecosystem, the increase in Ethereum’s staking rate has led to a decrease in staking yields (as shown in the figure below, the basic yield is only 3% +). The LSDFi protocol has fallen into a yield bottleneck, and the entire track has The attractiveness of funds has declined, resulting in capital outflows; on the other hand, it is due to the impact of the external environment, the most serious of which is the rising yields on U.S. bonds under the high interest rate environment in the United States, which has a siphoning effect on funds in the crypto industry , LSDFi funds fled to U.S. debt and DeFi U.S. debt derivatives with higher basic returns.

Source: https://defillama.com/yields?category=Liquid+Stakingchain=Ethereum

1.2 Project homogeneity is serious, involution but insufficient innovation

Since the development of DeFi, there are two important parts that are still shining as the cornerstones that generally maintain the operation of the entire DeFi system: lending and stablecoins. Among the operating rules of LST, lending and stablecoins are also the most basic and feasible operating methods. Based on the interest-generating attributes of LST, the project directions of the LSDFi track can be roughly divided into the following two categories:

LST serves as collateral for lending protocols or stablecoin protocols (represented by Lybra, Prisma, and Raft);

LST principal and interest separation (represented by Pendle);

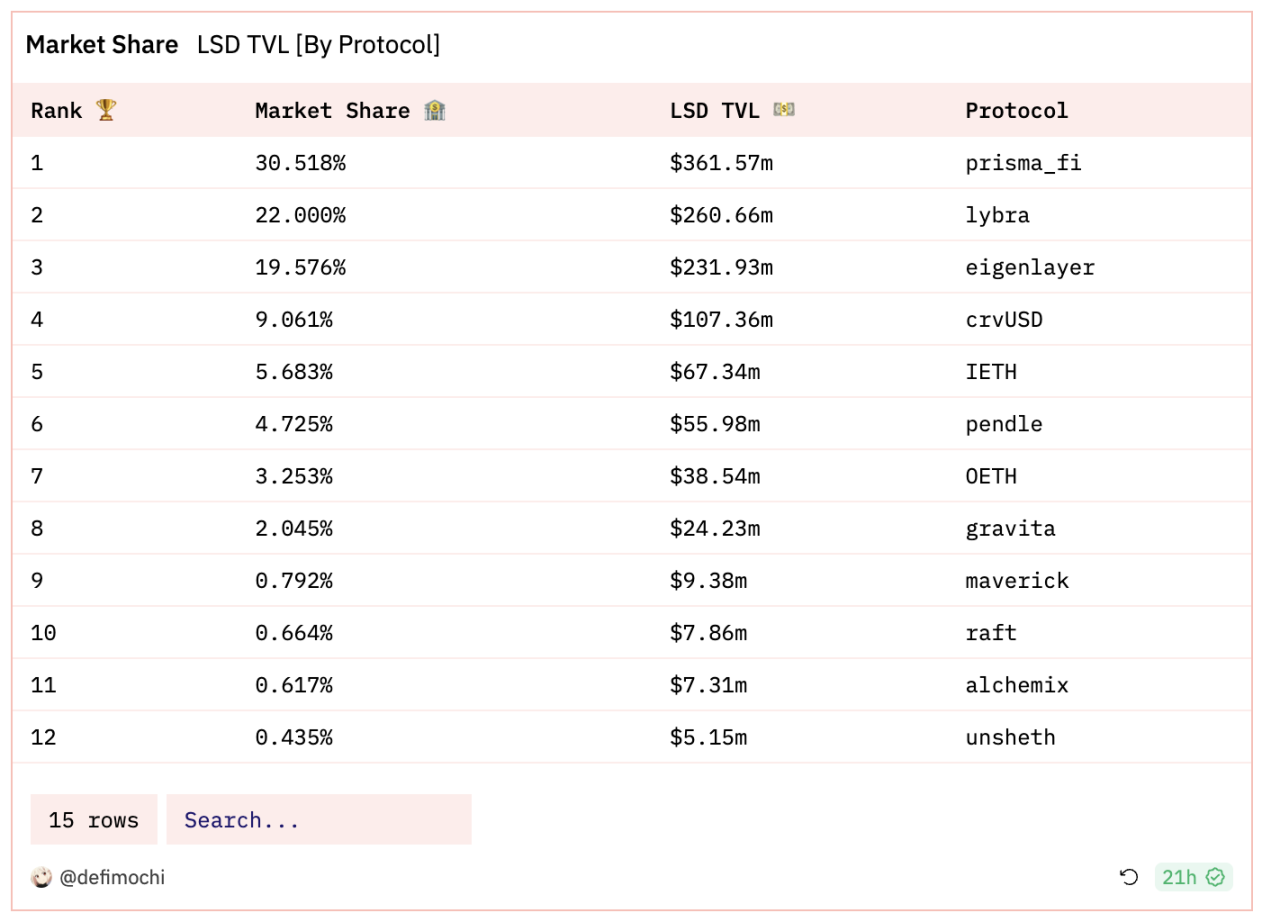

Source: https://dune.com/defimochi/lsdfi-summer

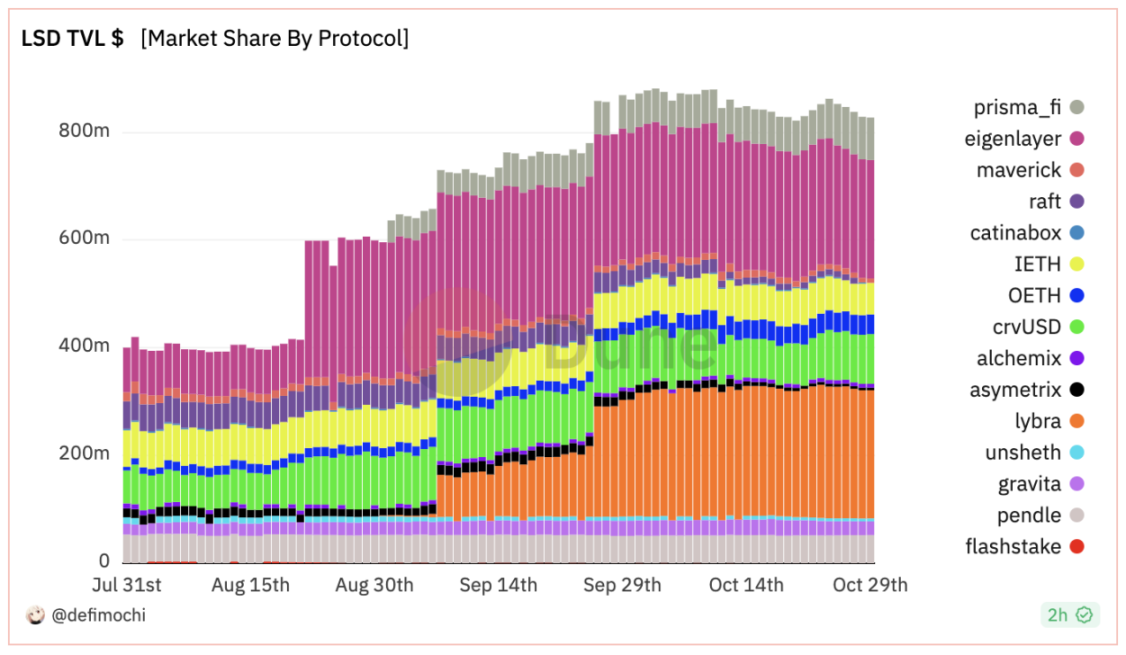

It can be seen from Dunes data that among the current top 12 TVL projects on the LSDFi track, 5 are stable currency protocols based on LST. Their basic mechanisms are almost the same: users use LST as collateral, mint or lend stablecoins, and when the price of the collateral drops, the collateral will be liquidated. The few differences are different stablecoins, different LTV, and different supported collateral.

After Terra collapsed and BUSD was forced to be delisted due to regulatory risks, there were many gaps in the stablecoin market that needed to be filled. The emergence of LST, which has its own interest-generating properties, can contribute to the stable currency market projects that are more in line with the needs of decentralization. It’s just that after the wave, the overall innovation of the track is weak, and they are just interfering with LTV, collateral types, and stablecoin yields (most of the yields rely on project token subsidies, which are essentially just air). If the late comers do not have the differentiation points to challenge the early comers, going online means the end of the project.

Pendle is a relatively unique presence in the entire LSDFi track. Its fixed interest rate products are naturally suitable for LST with interest-bearing attributes (taking stETH as an example, it can be split into ETH and pledge income parts), which is why Pendle has returned to the center of the market after Ethereum switched to PoS. Currently, Pendle is firmly holding on to its market share with product iterations, and there is no strong competitor of the same type on the market.

Pendle’s TVL reached new high on November 1st https://defillama.com/protocol/pendle

1.3 Headline projects currently have no pricing power and long-term growth is not guaranteed.

For DeFi, we can say that Aave is the leader in lending protocols, Curve is the leader in stablecoin DEX, and Lido is the leader in Ethereum liquidity staking service providers. These projects have achieved pricing power in their respective fields. The pricing power I am talking about here refers to the barrier effect formed by monopoly + rigid demand, which creates a certain monopoly effect and brand effect (far leading market share) in the markets rigid demand business.

And what does it mean to have pricing power? I think it means at least two advantages, one is an excellent business model, and the other is guaranteed long-term growth. To sum up simply, barriers with pricing power are the real barriers.

But looking back at the various projects in the LSDFi track, even Lybra Finance, the leading project with the largest market share, has not formed its own pricing power barrier. In the V1 stage, Lybra quickly stood out from the crowd of LSD stablecoin protocols with a rate of return (8% +) that far exceeded the basic return of Ethereum staking, attracting a large amount of TVL. However, the V2 upgrade did not bring effective results to Lybra. Growth, on the contrary, is being squeezed out of market share by Prisma and Eigenlayer, which came online later.

The leading project on the track cannot have its own pricing power. The fundamental reason for this embarrassing situation is: first, as the protocol layer, the technical difficulty of the project itself is not high, not to mention that many LSD stablecoin protocols are directly forked Liquity. Low technical threshold means that competition will definitely be fierce; secondly, the LSDFi project is not the issuer of LST, and essentially relies on the pricing power of ETH (pledge income) to reallocate liquidity; finally, the differences between various projects Very small, the market share is often affected by the protocol rate of return, and the leading project has not formed its own ecology and established absolute pricing power within the ecology.

The lack of pricing power actually means that the current prosperity may be temporary, and no one has found an insurance for long-term growth.

1.4 Token subsidy yield is unsustainable and stablecoin liquidity is sluggish

LSDFi has previously attracted a large number of TVLs in a short period of time with its high yields, but if we dig deeper we will find that these high yields are subsidized by project tokens, and the consequence of this is early overdraft management The value of tokens and high yields are unsustainable.

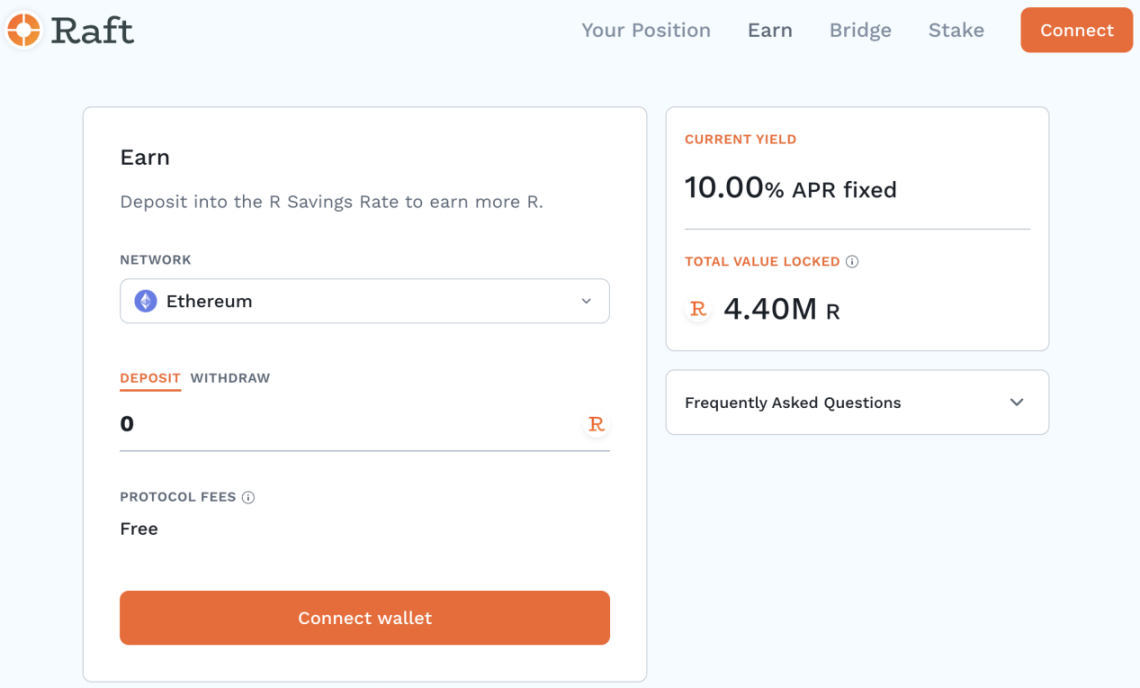

Take Raft as an example. Raft launched the Savings Module in V2, attracting R holders to make deposits with a fixed APR of 10%, but the source of the 10% interest was not disclosed in detail (the official explanation is that it is based on protocol income (subsidy). Looking at the entire DeFi, there are only a handful of projects that can provide a 10% low-risk interest rate, so this makes people wonder whether the project party cast \)R out of thin air to create such a seemingly beautiful APR myth.

It is worth noting that the current mortgage borrowing fee (interest rate) of Raft is 3.5%, which means that users can obtain at least 6.5% arbitrage after minting $R and depositing it in RSM.

Officially displayed R Savings Rate is up to 10%

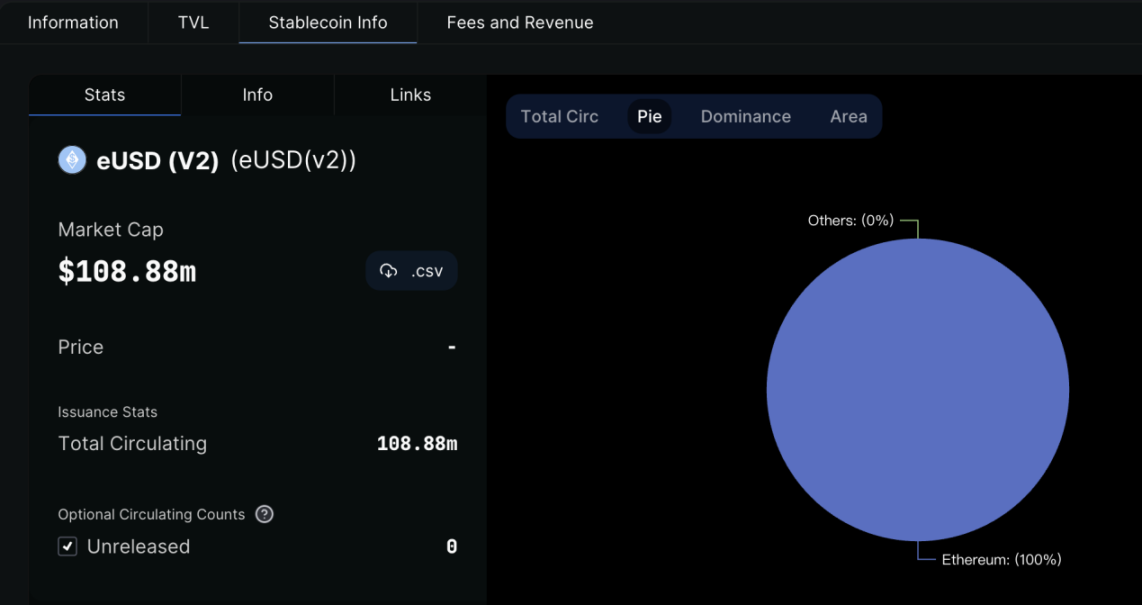

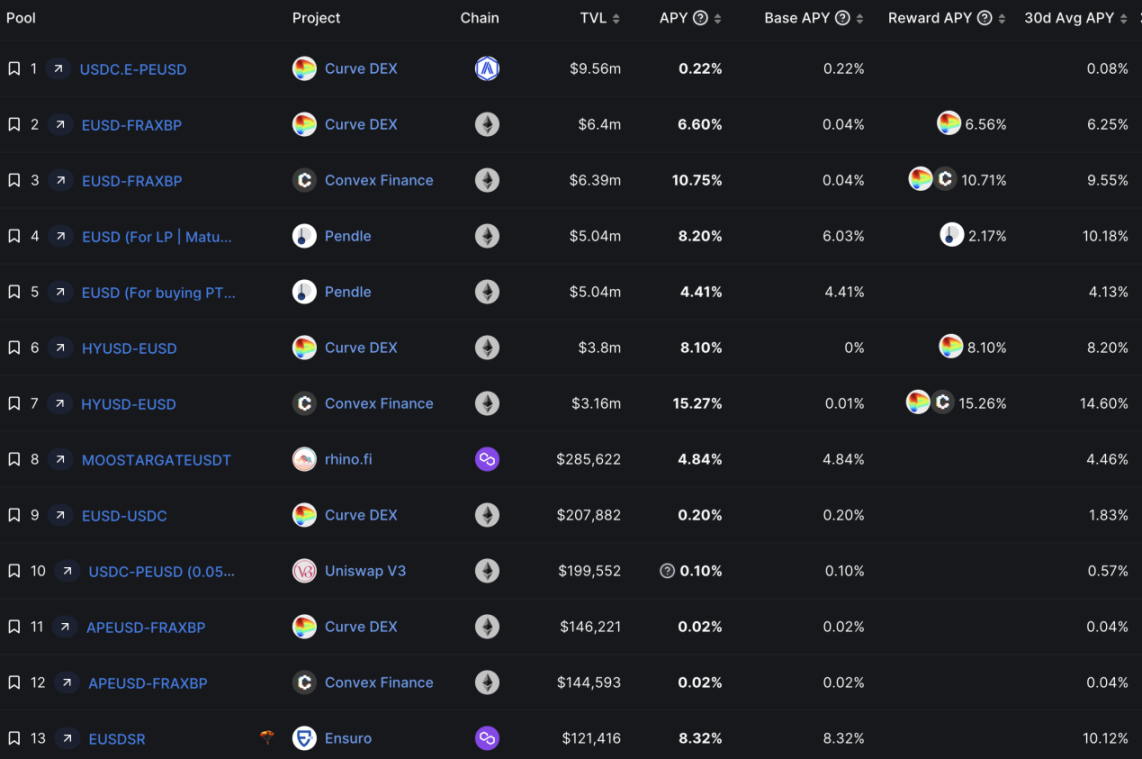

For decentralized stablecoins, liquidity will be the biggest factor affecting their development scale. The reason why Liquity failed to expand in scale and stand out in the last bull market was because its liquidity could not meet user needs. DAI is currently the most liquid decentralized stablecoin. Similarly, most of the current LSD stablecoins also face liquidity problems, that is, the stablecoins they launch are not deep enough, the usage scenarios are not diverse enough, and the real user demand is not enough.

Take eUSD launched by Lybra as an example. The current size of eUSD is 108 M, but its deepest liquidity pool is only the peUSD pool on the Arbitrum chain (peUSD is the full-chain version of eUSD). The depth of the eUSD-USDC pool on Curve is only 207k, which shows that the exchange of eUSD and centralized stablecoins is extremely inconvenient and will affect users use to a certain extent.

Source: https://defillama.com/yields/stablecoins?token=EUSD

2. From the perspective of specific projects, look for breakthroughs in the development difficulties of LSDFi

Although the LSDFi track as a whole has fallen into a bottleneck period of development, there are still some projects that are striving for change. From them, we may be able to get some ideas and inspirations to break through the development difficulties.

2.1 Develop the ecosystem, make up for the shortcomings of the economic model, and establish pricing power: taking Pendle and Lybra V2 as examples

At this stage, LSDFi projects all have a common seemingly unsolvable problem: using governance tokens to subsidize user income, resulting in the value of governance tokens being continuously diluted and eventually becoming worthless mining coins.

A feasible solution with reference significance is to develop its own ecology, use the power of ecological projects to improve the shortcomings of its own economic model, and establish absolute pricing power within the ecology.

2.1.1 Pendle

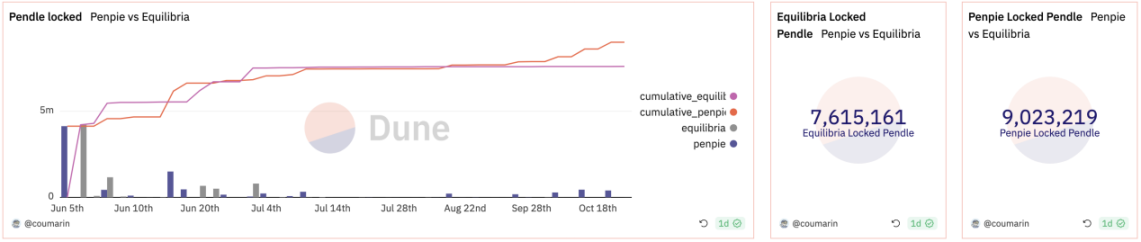

Pendle is currently the most successful representative of this method. Both Penpie and Equilibria are auxiliary protocols that increase the income of PENDLE LP based on the Pendle veToken economic model. LP does not need to pledge Pendle to obtain Pendle mining boost income. There is not much difference between the two business models. The main function is to absorb part of the selling pressure of governance tokens for Pendle, making Pendle itself develop healthier.

Source: https://dune.com/coumarin/pendle-war

2.1.2 Lybra Finance

After Lybra failed to achieve effective growth after the launch of V2, it also began to intentionally build its own ecological project. On October 13, Lybra officially announced the official launch of Lybra War and regarded it as the starting point for the next stage.

Lybra started the Lybra War so openly because it recognized its many problems:

1) High inflation of the governance token LBR caused by maintaining high APR, and V2 mining activities caused excessive short-term selling pressure;

2) Fierce competition in the same track (such as Prisma, Gravita, Raft) has led to sluggish growth, and there are no investors behind Lybra to rely on;

3) The liquidity of eUSD is insufficient, and the promotion and use of peUSD is not as expected;

4) The community consensus was shaken. During the migration process from V1 to V2, the community had questions about the handling of successfully migrated tokens in time (sifu decided the entire voting result with one person).

Source: https://twitter.com/LybraFinance/status/1712505916363592011

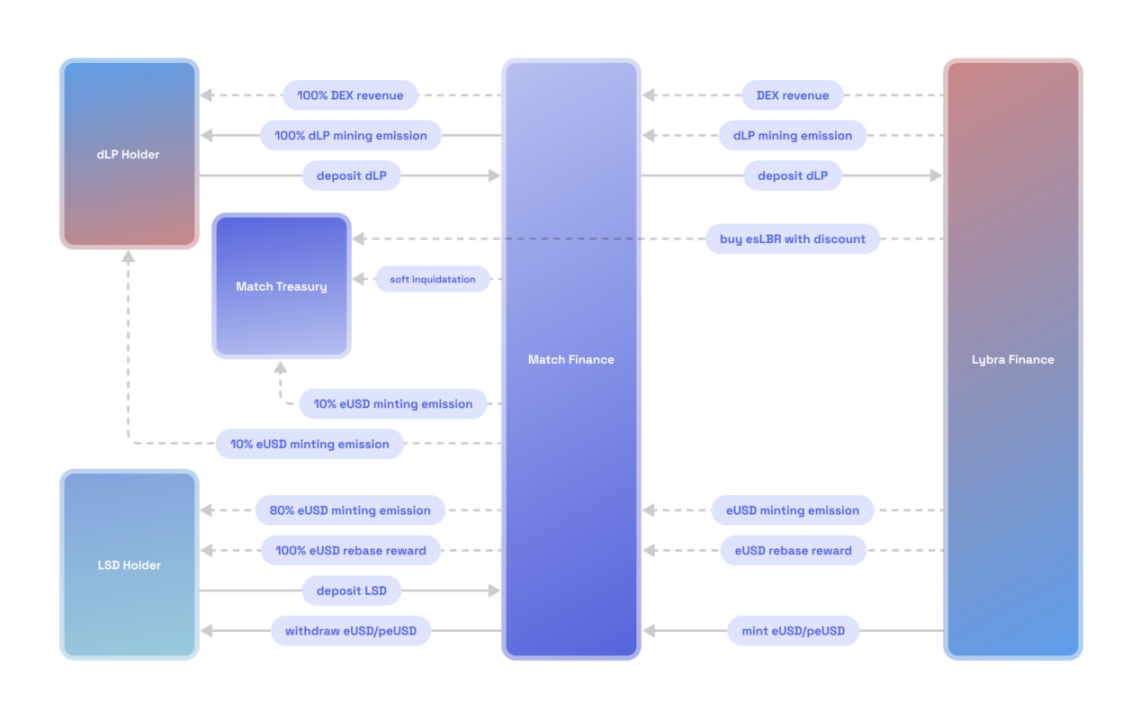

The core of Lybra War lies in the accumulation of dLP and the dynamic matching of dLP and eUSD. Because in Lybra V2, users must pledge at least 2.5% of the LBR/ETH dLP holding eUSD value to obtain the emission of esLBR, so the second-layer protocol of the Lybra ecosystem must obtain more esLBR through yield boosting of esLBR and dLP. . In addition, the distribution right of Lybra War lies in the esLBR emissions between LSD pools. The potential demand parties are mainly LST asset issuers and eUSD minting majors. Lybras LSD pool depth deviation will be more suitable for small LST issuers to accumulate esLBR to increase esLBR voting power.

The only deep players currently participating in Lybra War areMatch Finance, an effective competition pattern has not yet been formed. Match Finance mainly solves two problems (the project mechanism will not be described in detail here):

1) The problem that users cannot obtain esLBR incentives without dLP when minting eUSD;

2) esLBR’s yield boosting and exit liquidity issues.

Match Finance mechanism, source: https://match-finance.gitbook.io/whitepaper/

As the protocol layer of the LSDFi track, neither Lybra nor Pendle are LST issuers. Therefore, while they accumulated a large amount of TVL through high APR in the early days, they also planted a negative seed. In order to achieve healthy development in the future, they choose to develop ecological projects and use ecological projects to continuously provide blood for themselves. Any ambitious LSDFi head project will actually embark on this development path.

2.2 Micro-innovation to improve differentiated user experience

As a non-headline project, how to defend ones one-third-acre field in the fiercely competitive track and find ones own differentiated positioning is the key. Even micro-innovations can reach some vertical users. As long as these users are sticky enough, the project will have the chips to survive.

2.2.1 No liquidation: Take CruiseFi as an example

While most projects are still involved in LTV and collateral categories, some projects have directly launched a no liquidation mechanism to attract traffic.

byCruiseFiFor example, users can mortgage stETH, mint the stablecoin USDx, and then exchange USDx for USDC through the USDC-USDx pool on Curve. The Lender who provides USDC to the Curve stablecoin pool can obtain the interest generated during the stETH mortgage period.

So how to ensure that Borrower will never be liquidated? When liquidation occurs:

1) The project team will lock part of the collateral (stETH), and then give Borrower the pledge income of the locked part of stETH;

2) Positions that exceed the stETH income will be suspended. This ensures that the pledge income will always cover the borrowing interest, which means that Borrower will not be liquidated. However, the disadvantage of this is that the income of stETH will increase with the overall pledge rate of ETH. rise and fall;

3) Regarding the suspended positions, corresponding Price Recovery Tokens will be generated. These PRTs can be exchanged for ETH at a ratio of 1:1 (can only be exchanged when it is greater than the liquidation line). PRTs can be freely traded in the secondary market.

The advantage of this is that Borrower can extend the time for liquidation or avoid liquidation, Lender can obtain ETH pledge income, and PRT holders can obtain ETH future growth income. No liquidation will be very attractive to some users with higher risk appetite in the bull market.

2.2.2 Portfolio rate of return: Taking Origin Ether as an example

In the DeFi world, yield is always the most attractive narrative, and this iron law still applies to LSDFi.

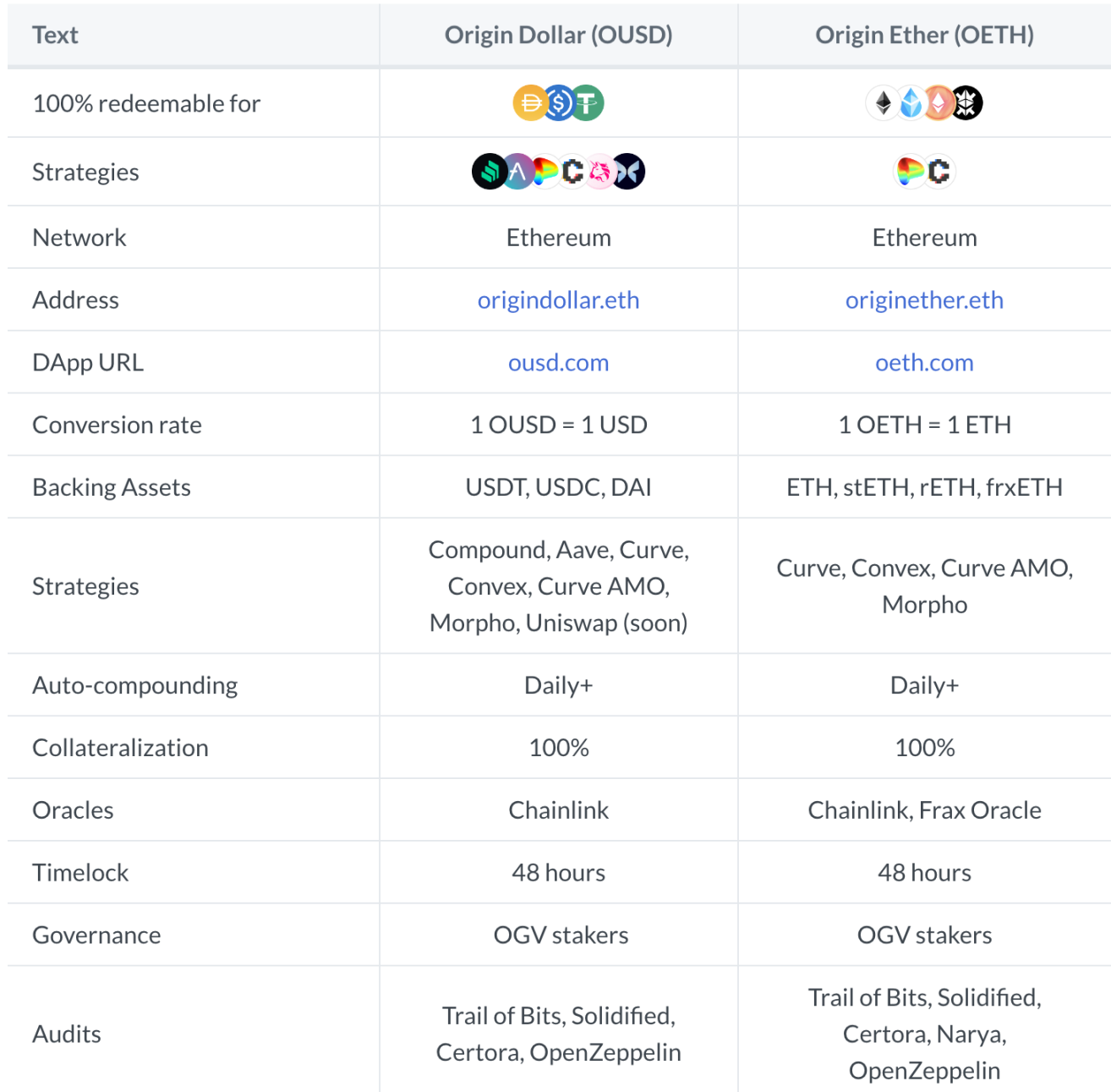

Origin EtherLaunched in May 2023, using ETH and other LST as backing collateral, the value of 1 OETH will always equal 1 ETH.

Source: https://docs.oeth.com/origin-ether-oeth

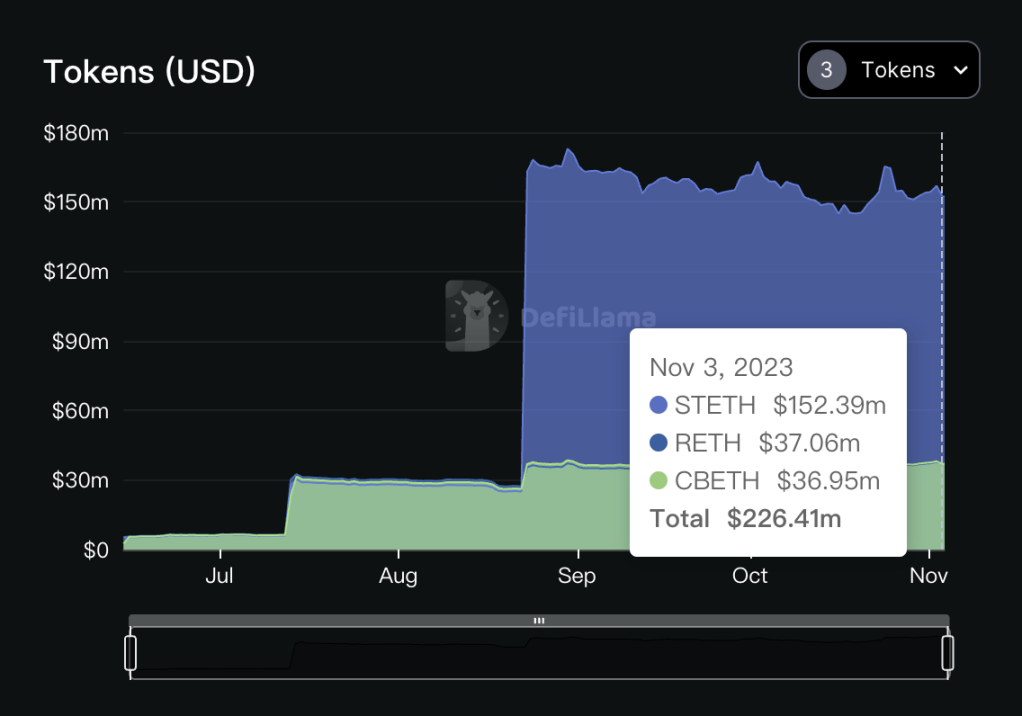

The biggest difference between Origin Ether and other LSDFi is that its source of income is a basket of LST assets such as stETH, rETH, and sfrxETH. In addition, OETH also uses AMO strategies on Curve and Convex through the OETH-ETH liquidity pool, and supports strategies on Balancer, Morpho and other ETH-denominated Curve pools. Through the optimization of a series of liquidity strategies, Origin Ether is able to provide users with APY higher than the market average. This is why Origin Ether has rapidly accumulated a large amount of TVL in recent months (OETH currently ranks seventh in the market share).

Source: https://defillama.com/protocol/origin-ether?medianApy=true

2.2.3 Continue with the matryoshka doll: taking LRTFi based on Eigenlayer as an example

LSDFi, as the matryoshka doll of LSD, has developed to the bottleneck stage, but the emergence of Eigenlayer will lead to a higher level of LRTFi matryoshka doll in the future. This is not only another increase in leverage for the entire LSDFi track, but also a return to Market centers, opportunities for outward expansion.

Although Eigenlayer is still in the closed beta stage and has not yet been opened to all users, judging from the two previous pledges, the market popularity is very high.

Eigenlayer TVL composition, source: https://defillama.com/protocol/eigenlayer

At the same time, many projects based on LRT (Liquid Restaking Token) have emerged, such asAstrid Finance、Inceptionwait. There is no innovation in the core logic of these projects, except that LRT is included in the scope of collateral compared to LSDFis protocol. It is expected that this type of competition will reach a fierce stage after Eigenlayer is officially launched, and it is still in the early stages.

2.3 With the support of capital power, bundle other mature projects and enjoy other ecological dividends: Take Prisma as an example

If a later project wants to catch up with its competitors in a track full of variables, but it cannot achieve paradigm innovation, then finding strong backing and using the dividends from other projects as its own buff will help it stand firm. An effective way to keep your heels on is that we can call this type of behavior taking shortcuts or finding daddy.

Prisma Finance is the most typical success story. Compared with grassroots projects like Lybra Finance (started by the community and without private equity financing), Prisma can be said to be a rich second generation born with a golden spoon. Before any of the project’s products were launched, they had already attracted the market’s attention with a gorgeous public relations release. The most valuable information revealed in the article is not how different its project mechanisms are, but that its investor list includes DeFi OGs like Curve and Convex, as well as large institutions like OKX and The Block.

Then Prismas development path is as advertised, bundling Curve and Convex, obtaining their support, giving additional rewards to the native stablecoin mkUSD (in the form of CRV, CVX), and realizing it through the veToken model (controllable protocol parameters) Flywheel effect.

In the third month after its official launch, Prisma relied on Justin Suns $100 million wstETH support, TVL achieved all-time high, and surpassed Lybra to become the new track leader.

Source: https://defillama.com/protocol/prisma-finance

2.4 Real paradigm innovation

Whether it is an industry or a track, it will always fall into a development bottleneck after experiencing barbaric growth. The fundamental way to solve this kind of dilemma is undoubtedly paradigm innovation. Although there are no game-changing innovations in the development of LSDFi, I firmly believe that as long as the value of Ethereum continues to exist as a strong consensus, there will eventually be game-breaking paradigm innovations that will ignite the raging fire of LSDFi again.

Reference

1.https://foresightnews.pro/article/detail/38534

2.https://foresightnews.pro/article/detail/28437

3.https://www.panewslab.com/zh/articledetails/o0rocg16.html