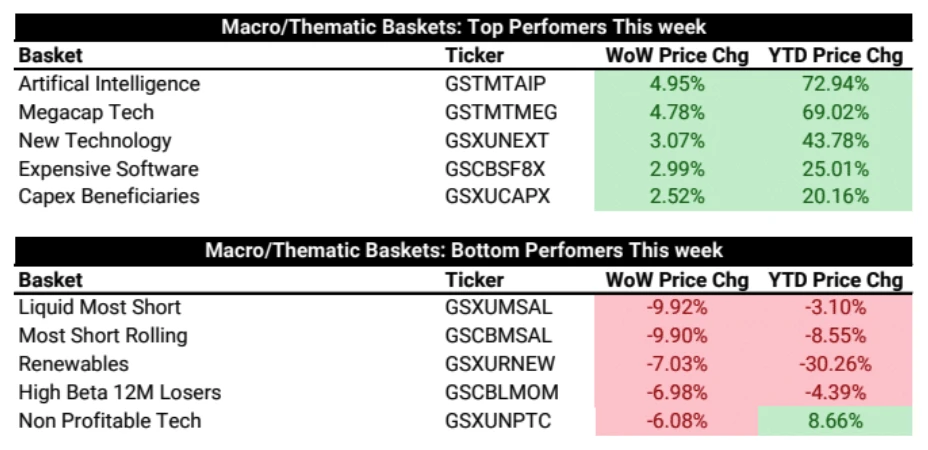

Driven similarly by Wall Street, most stock markets have strengthened, mainly driven by the previous big blue chips, and small-cap stocks/unprofitable stocks have returned to weakness; US stock market sentiment and position data consistently show that they are still in the process of recovery, and there is still room for recovery. . The performance of the Chinese market is relatively weak, and the latest Chinese inflation has returned to deflation. The crypto market continues to surge, led by Ethereum and altcoins, but market breadth is still poor, and ETF hype may gradually lack passion. This week, attention will be paid to the Apec summit. The United States is shutting down while trying to tussle with China. As the CPI data is destined to continue to slow down year-on-year, the markets focus will still be on core inflation. If it continues to hover at a level slightly above 4%, the superposition The slowdown in growth in the fourth quarter may trigger discussions of stagflation.

· Poor 30-year Treasury Auction: Thursdays U.S. 30-year Treasury auction performed poorly, with $24 billion of 30-year bonds attracting below-average demand, with a bid-to-cover ratio of 2.24, below the average of the previous 10 bond auctions. Ratio 2.38. Subsequently, the 10-year Treasury yield surged 11 basis points to 4.64%. The 30-year bond yield surged 15 basis points back to 4.8%, one of the largest one-day gains since June 2022. The 2-year Treasury yield is back above 5%, a fresh November high.

· Earlier Wednesday’s US$40 billion 10-year Treasury bond sales statistics were also mediocre, but considering the increase in auction size, the results were actually not bad, so the 10 yr yields after the auction were slightly lower, while short-term yields rose, The inversion of the curve deepened, indicating that investors were betting that the central banks rate hike cycle was over. But then the 30yr auction led to another jump in long-term yields, mainly showing concerns about long-term economic and fiscal stability. Taken together, this will create a headwind for risk assets.

· Cyber attack: The U.S. branch of the Industrial and Commercial Bank of China suffered a ransomware attack. As an important U.S. bond market participant, transactions conducted through ICBC failed to settle due to the attack. The timing of this cyber attack coincided with the focus of new bond supply, It may have had an impact on the auction results, although the U.S. Treasury Department has not disclosed details.

· Demand and pricing issues: There was mention of a drop in demand for these bonds, with both direct and indirect customer participation at their lowest levels in two years. The auction caused yields to rise, meaning bonds sold at lower prices. The 30-year Treasury yield climbed to 15 basis points.

Powells hawkish comments also pushed yields higher: Powell told a panel that the central bank did not believe it was doing enough to combat high inflation and reminded markets that it would still raise interest rates if necessary.

· Italian bond auction: The poor sentiment at the U.S. Treasury auction also seemed to affect the Italian bond auction. Later, the Italian Treasury sold 1 billion euros of 30-year BTP bonds at a yield of 5.05%, the highest since July 2013. the highest level. This seems to be felt in the global bond market sentiment linkage.

· Concerns about U.S. government shutdown: If a spending agreement is not reached before November 17, the U.S. government may face a shutdown. U.S. House Speaker Mike Johnson unveiled a Republican stopgap spending measure on Saturday that quickly faced public opposition from some lawmakers on both sides of the aisle.

· The current division within the Republican Party is the biggest problem, with some members calling for a clean temporary spending bill that would last until mid-January without any spending cuts or any conservative policy add-ons. However, hardline conservatives are pressing for a comprehensive strategy that includes spending cuts and strengthening U.S.-Mexico border security, among other policies. Therefore, Johnson’s proposal this time still seems to be unpopular with both sides. Democrats think it is “complex” and some Republicans think it is not “conservative” enough. As the deadline approaches, many voices in the market are doubting new Speaker Mike Johnsons ability to avoid a shutdown.

· Today’s political divisions and ever-expanding debt burden in the United States are a vicious cycle. The more noisy they are, the less helpful they are in solving the deficit problem. In turn, they stimulate market pricing and increase the debt burden.

· Another downgrade: Moodys on Friday changed the outlook for the U.S. governments credit rating to negative, raising the possibility of another downgrade of the U.S. debt rating. The company cited risks to the U.S. fiscal outlook, namely that without effective fiscal policy measures to reduce government spending or increase revenue, interest rates will rise, increasing the risk of higher borrowing costs for the federal government. As the political game will become complicated next year, it may not be until 2025 to see the introduction of major policies to solve the fiscal crisis, so we expect that this will make it difficult for the market to price U.S. bond interest rates significantly higher in the short term, as this news is approaching the close It appears from time to time and is expected to further ferment this week, but the impact should be far less than the market shock after Fitch officially downgraded the U.S. debt rating in August.

· Moodys is the last of the three major rating agencies to maintain its highest rating on the U.S. government. The U.S. Treasury market is considered a safe haven for funds due to its depth and liquidity. Currently, no asset can compete with it, and cryptocurrencies may be a potential competitor.

U.S. stocks in divergence and reversal

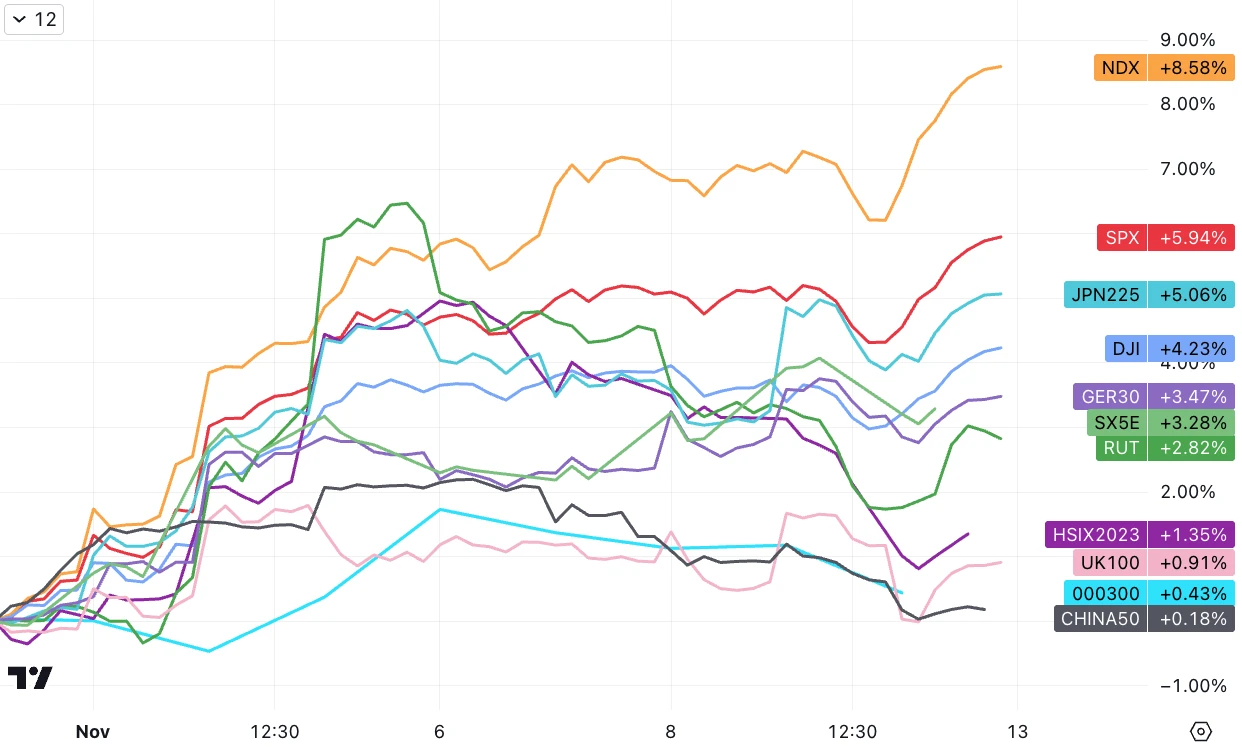

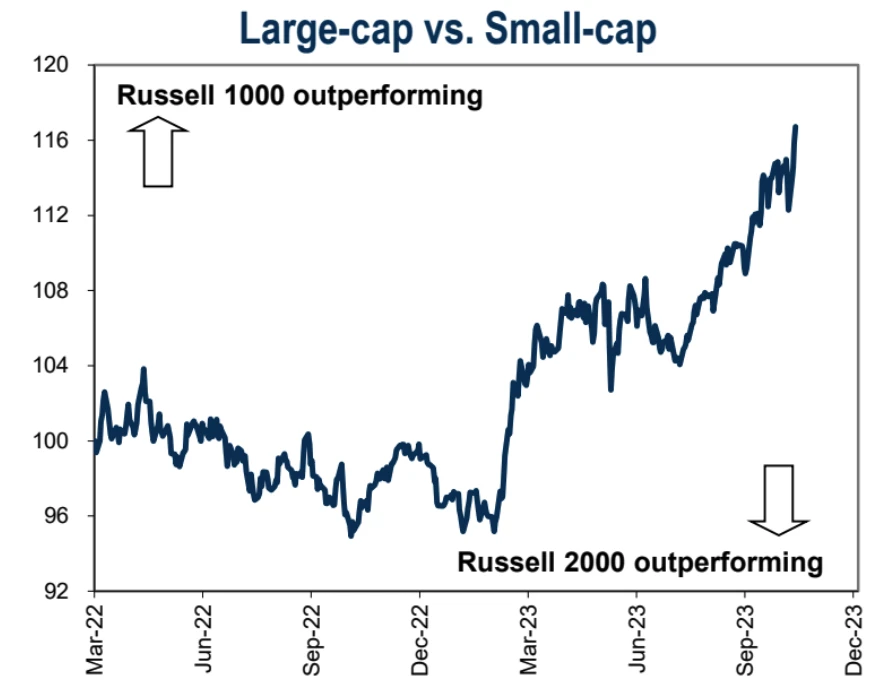

U.S. stocks rose for the second consecutive week, with the SPX closing above 4,400 points for the first time since September 20. Driven by the strength of large-cap technology stocks, NDX outperformed RUT by about 6%, the largest increase in the past eight months. gap.

3Q financial report greatly exceeded expectations

Its been a pretty good week for the Big 7 (minus Tesla)

Large-cap stocks and growth stocks make a big counterattack:

So far, 92% of SP 500 companies have reported actual third-quarter results:

81% of companies reported EPS above expectations, which is above the past 5-year (77%) and 10-year (74%) averages. If the final figure holds at 81%, it will be the highest ratio since the third quarter of 2021 (82%).

Net profit rose 4.1% year over year, ending a losing streak dating back to the third quarter of 2022.

61% of companies reported revenue above expectations, below the past 5-year (68%) and 10-year (64%) averages. If it ultimately holds at 61%, it will be the lowest since the first quarter of 2020 (56%).

Revenue increased 2.3% year over year, marking the 11th consecutive quarter of revenue growth.

The SP 500 PE is 18.0, below the 5-year average (18.7) but above the 10-year average (17.5).

Analysts expect the SP 500 to rise 15.9% over the next 12 months. The energy and consumer discretionary sectors are expected to see the largest gains.

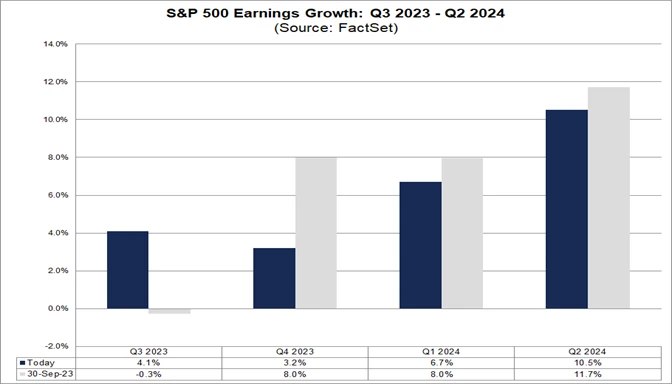

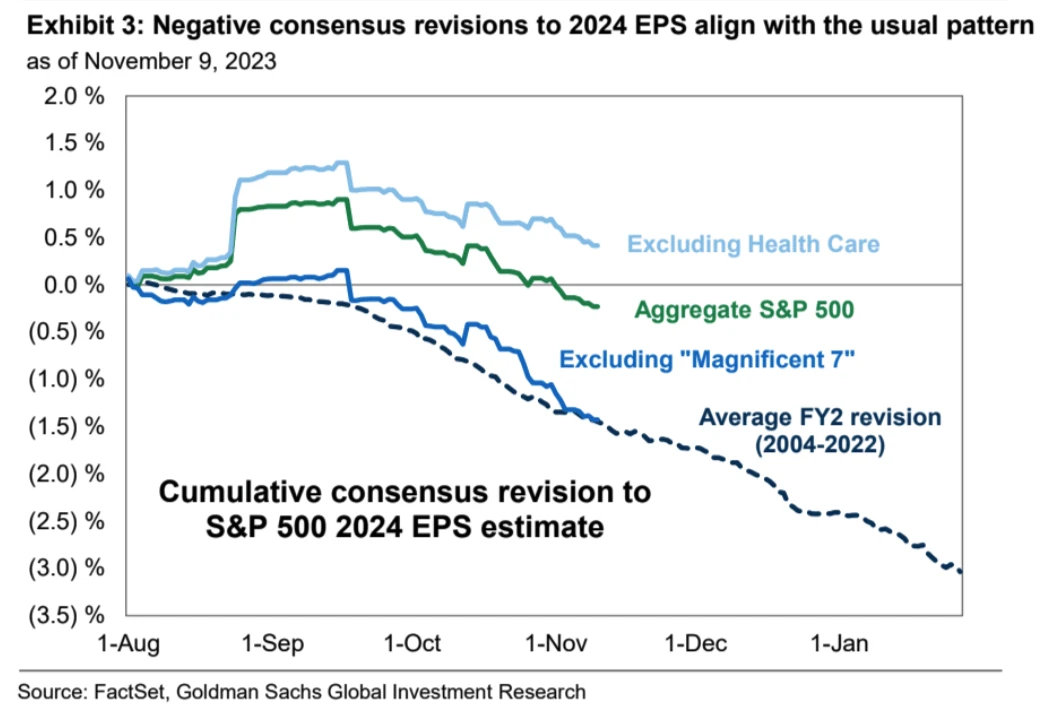

You know, before the start of the financial reporting season, the market expected earnings growth to be close to 0%, but the market has lowered the future earnings growth rate, especially the fourth quarter growth rate of 8% -3.2%:

The health care sector dragged down a sharp decline in SP 500 earnings estimates. Excluding the sector, 2024 EPS estimates are down just 0.4%. From the perspective of individual stocks, the profit expectations of big technology companies remain stable, supporting the 2024 profit expectations. After excluding Mag 7, the 2024 expectation of SP 493 is -1.4%

Additionally, third-quarter company reports also reflected a broad slowdown in cash spending:

Capital expenditures and RD spending increased 5% year-on-year, significantly slower than the 14% year-on-year growth rate in the first half. Several tech giants are driving this slowdown. Apple, Amazon and Meta cut total capital expenditures and RD spending by 6%, 6% and 15% respectively in the third quarter.

Companies continue to reduce repurchase spending (down 9% year-on-year), but at a slower pace than in the first half of 2023 (down 22% year-on-year).

Other markets:

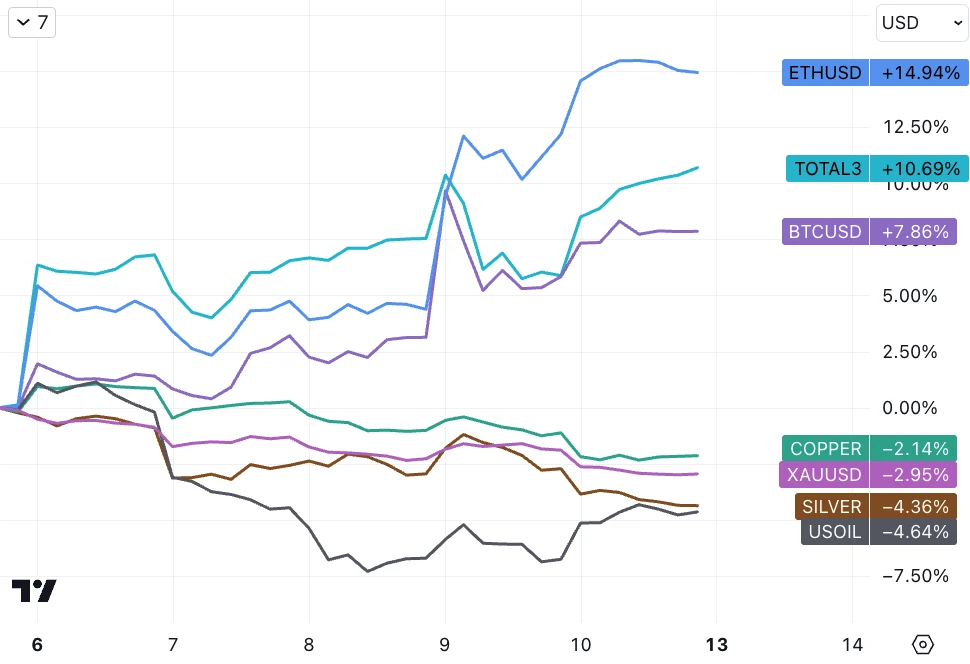

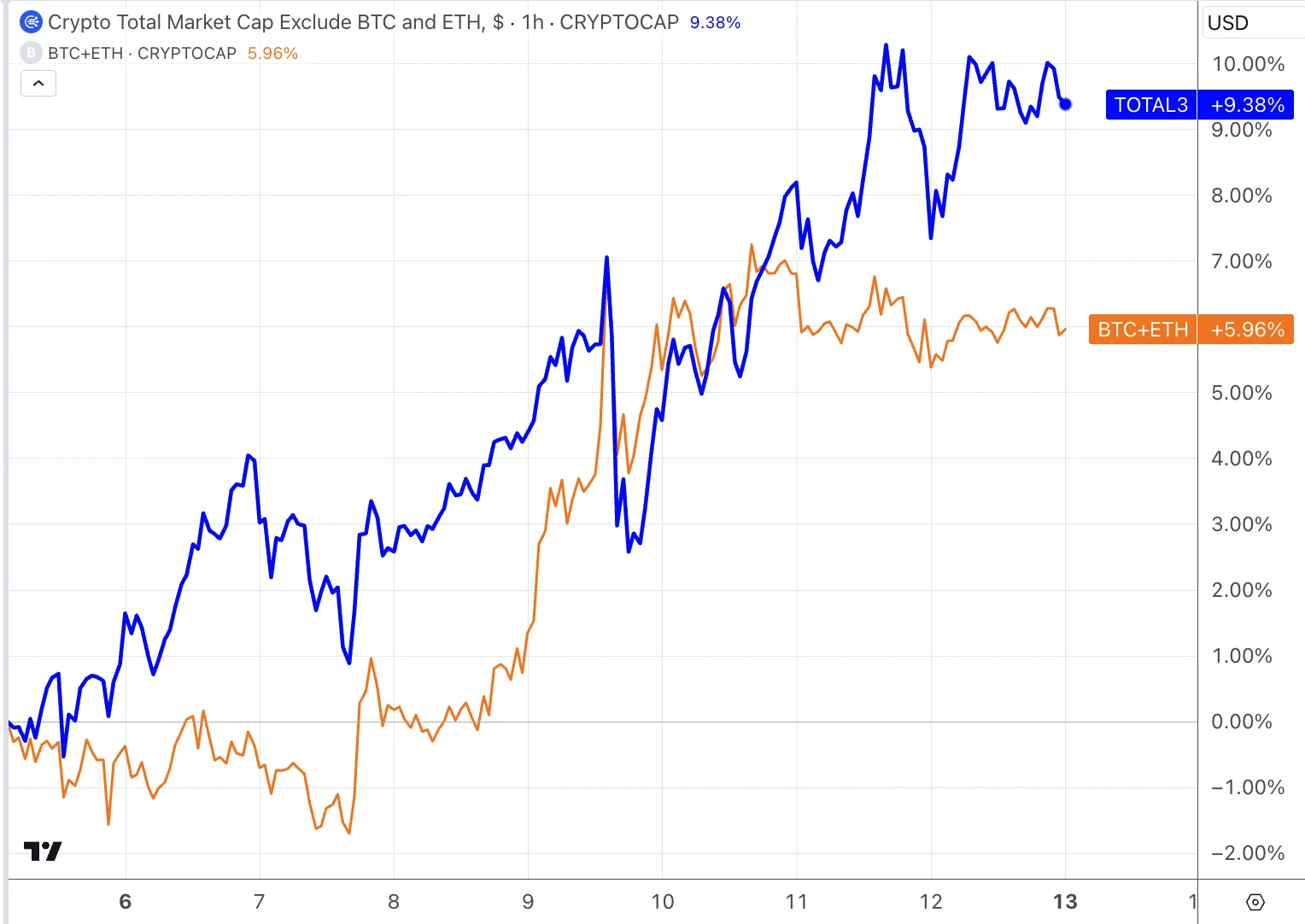

Asset management giant BlackRock registered the creation of an Ethereum trust, triggering the markets association with ETH ETFs. Earlier this year, BlackRock registered a Bitcoin trust in the same way, and a week later submitted a proposal to the SEC to launch a spot Bitcoin ETF. Apply. ETH led the crypto market higher last week; as the vanguard of alternative allocations, gold prices fell 3% as market yields rebounded late last week; the easing of geopolitical fears led to a third consecutive weekly decline in oil prices:

The restlessness of altcoins continues to ferment. Although the market breadth is still relatively poor, the exaggerated gains of a few assets combined with the inflow of US dollar stablecoins still allow the performance of encrypted exBTCETH to surpass BTC+ETH. However, if the breadth cannot be increased, such a rise may gradually cool down. , the crypto market is currently facing resistance such as the rebound in U.S. dollar and U.S. bond interest rates, declining inflation expectations, strong expectations of economic slowdown, cooling geopolitical risks, and the beginning of the altcoin bubble bursting (for example, GAS fell from 30 to 10). Maintaining the current upward trend requires new Theme introduction (the risk-reward of betting on the left side is still not high enough, so the current view on the market has changed from positive to neutral, at least not bearish this week):

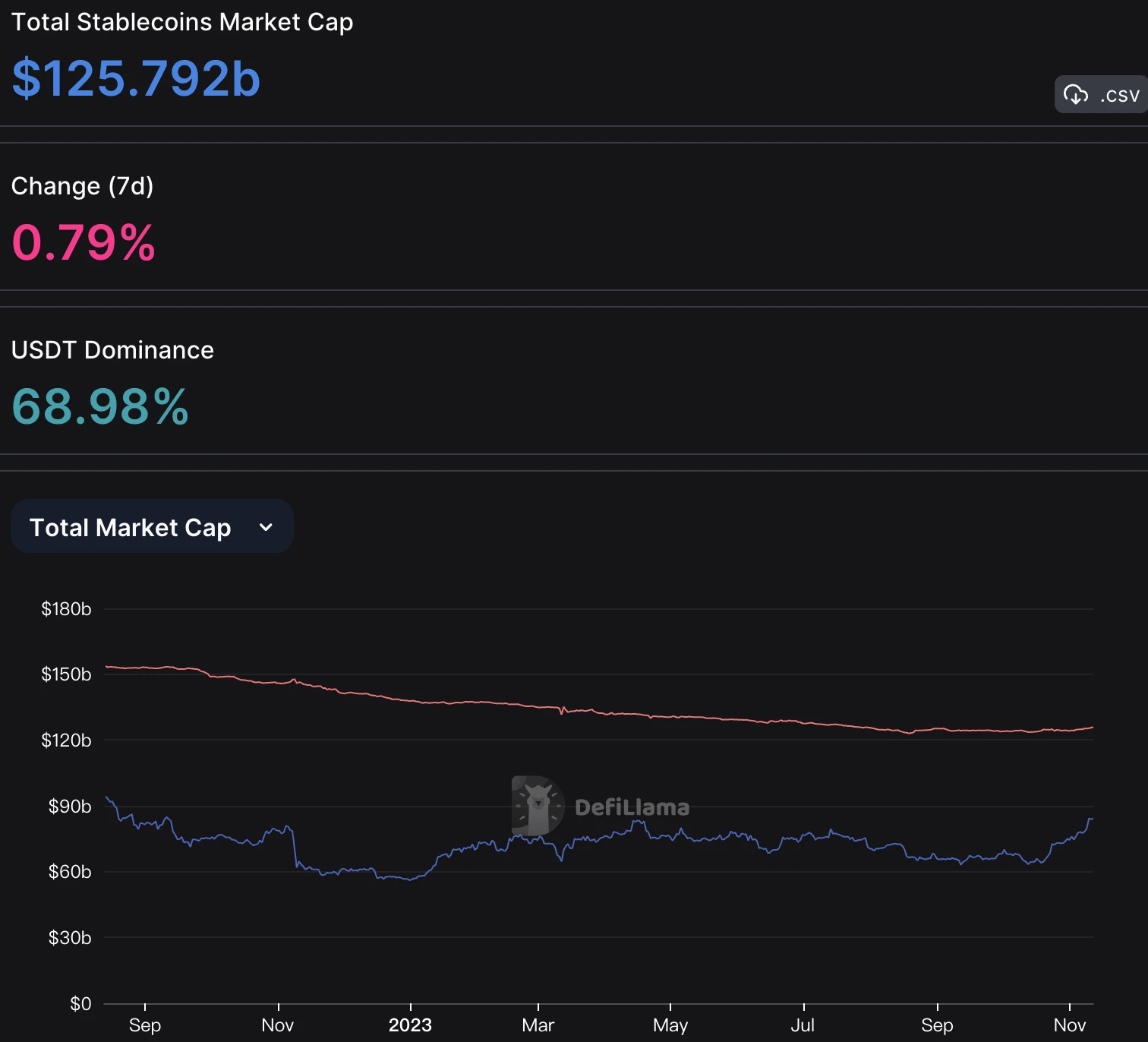

The stablecoin market has seen inflows of nearly $2 billion in the past month (red line in the chart below):

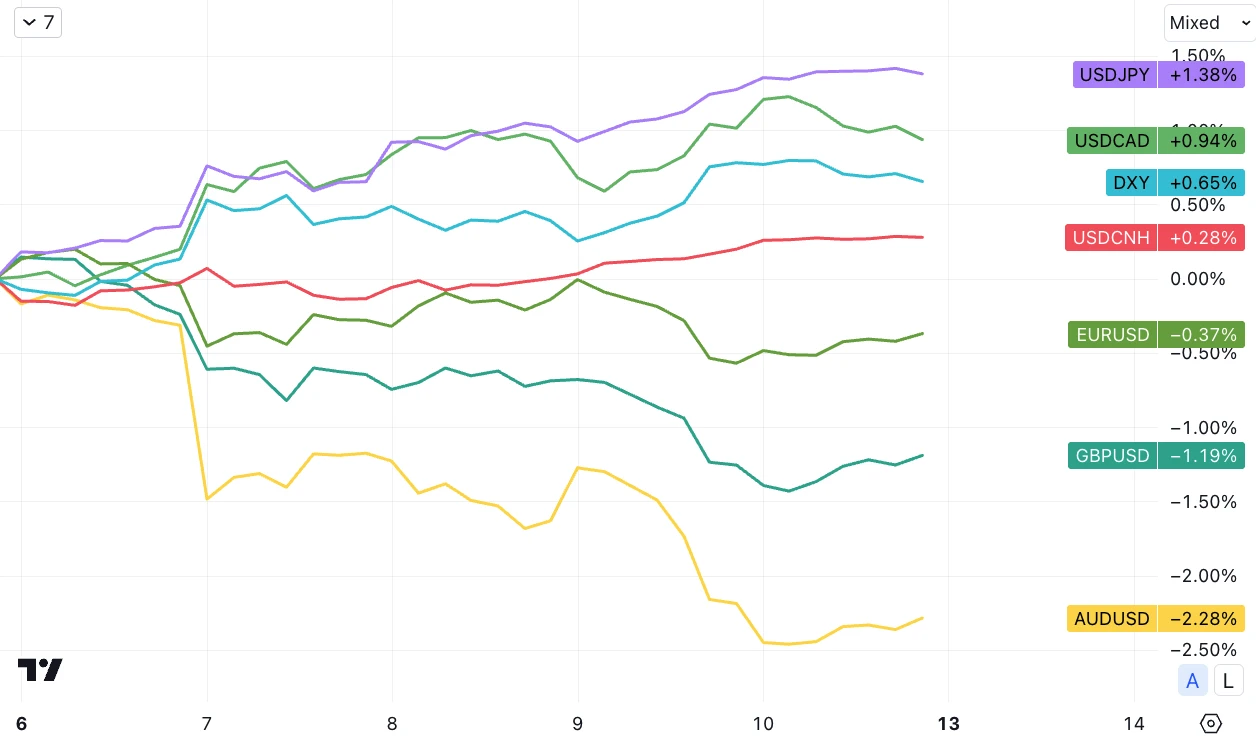

The dollar continues to rebound

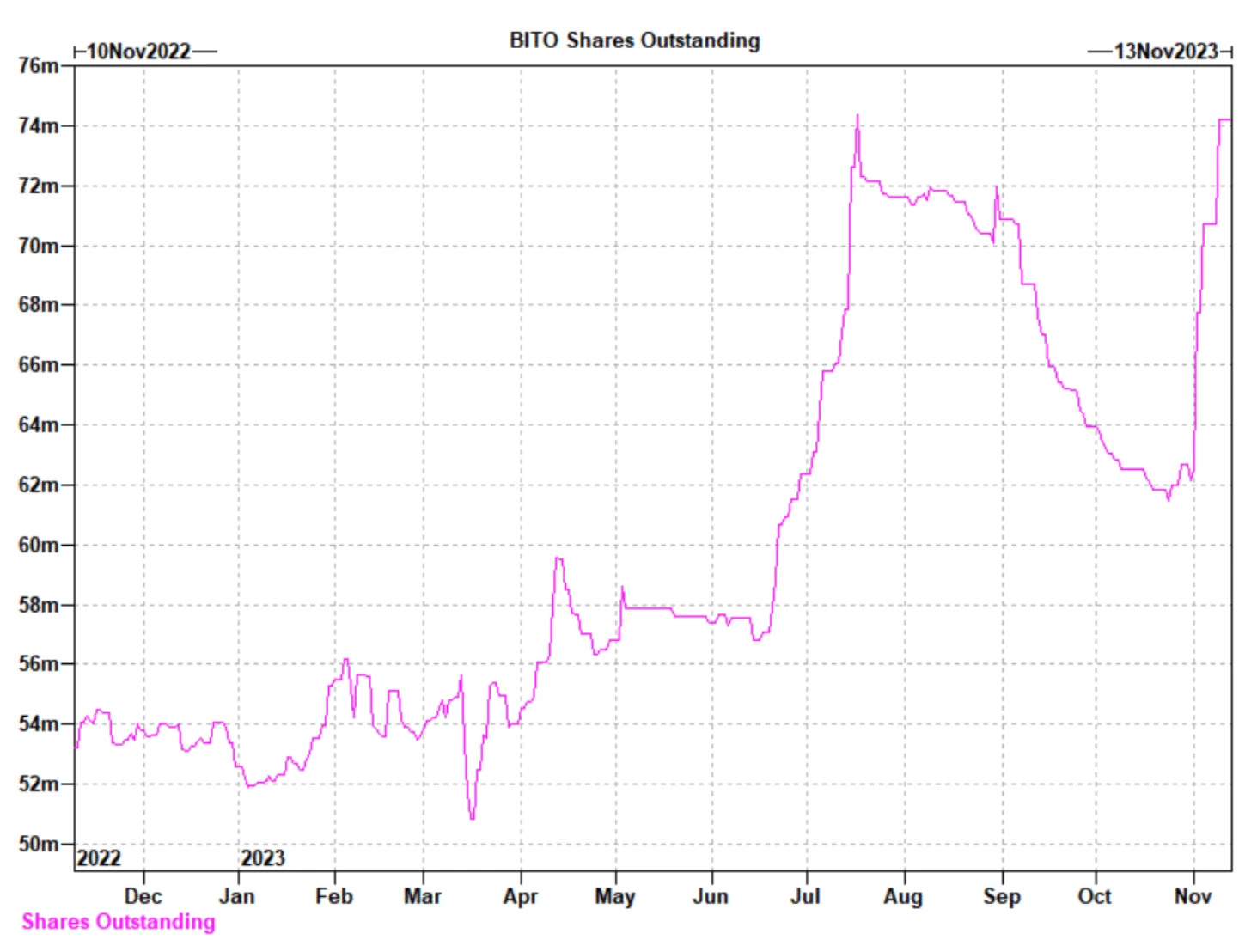

Bitcoin ETF fever continues

BITO (backed by futures) trading volume hit a record 40 million shares ($750 million) on Thursday, with AUM up 60% in a month to over $1 billion. In addition, BITO positions accounted for 24% of November CME futures positions and 70% of December CME futures positions. Last week, the amount of CME futures open interest exceeded Binance (4.2 billion vs 3.9 billion). It can be seen that US stock buyers contributed at least half of the increase.

Subsequent SEC decision deadlines are November 17, January 15 and March 15

Gensler seemed to express a certain compromise on digital assets on Friday:

Theres nothing about crypto that is incompatible with the securities laws. The purpose of securities laws is to protect your audience and the investing public so that they get proper disclosures and people dont use their funds on their behalf…

If Tom or anyone else wants to get into this space, I would say do it within the law. Build investor trust in what youre doing and make sure you have appropriate disclosures and make sure youre not commingling all those functions , transact with your clients or use their crypto assets for your own purposes.”

Investors responded to these remarks, with FTT Token more than doubling at one point on Friday, with the price exceeding $5 in the short term.

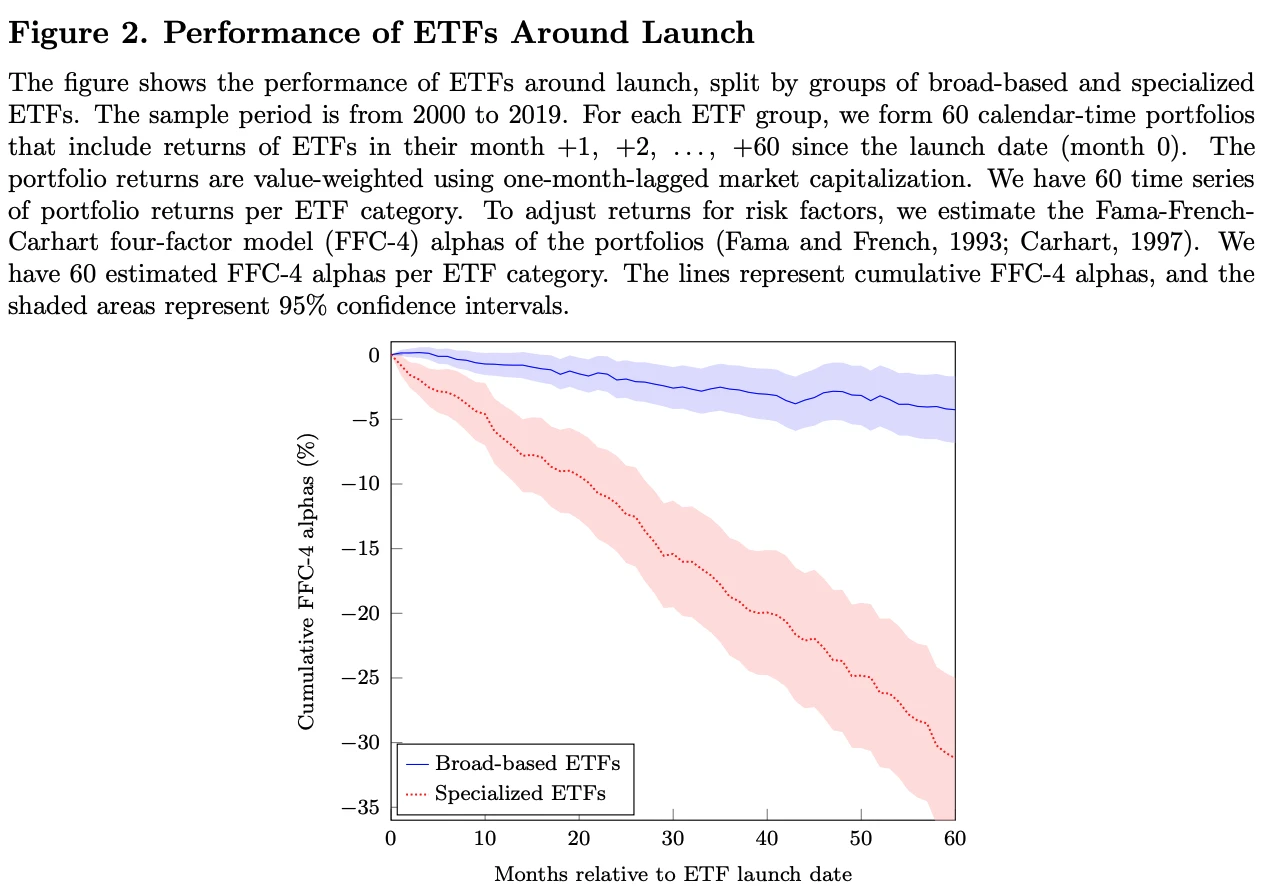

Study suggests spot Bitcoin ETFs may underperform

A recent study found that niche/specialty ETFs typically underperformed the broader stock market in the five years after their launch, with risk-adjusted annualized returns of about -6%.

Because they tend to be listed when investor enthusiasm for the underlying benchmark assets they track or their respective investment themes is high. This in turn means that the securities in which these ETFs invest tend to be overvalued. Higher fees for such ETFs can eat into returns. And professional ETFs are more popular with retail investors, who are more likely to hold wrong expectations and participate in positive feedback transactions.

Whether this will happen if a spot Bitcoin ETF is approved remains to be seen, but investors should continue to heed this historical lesson.

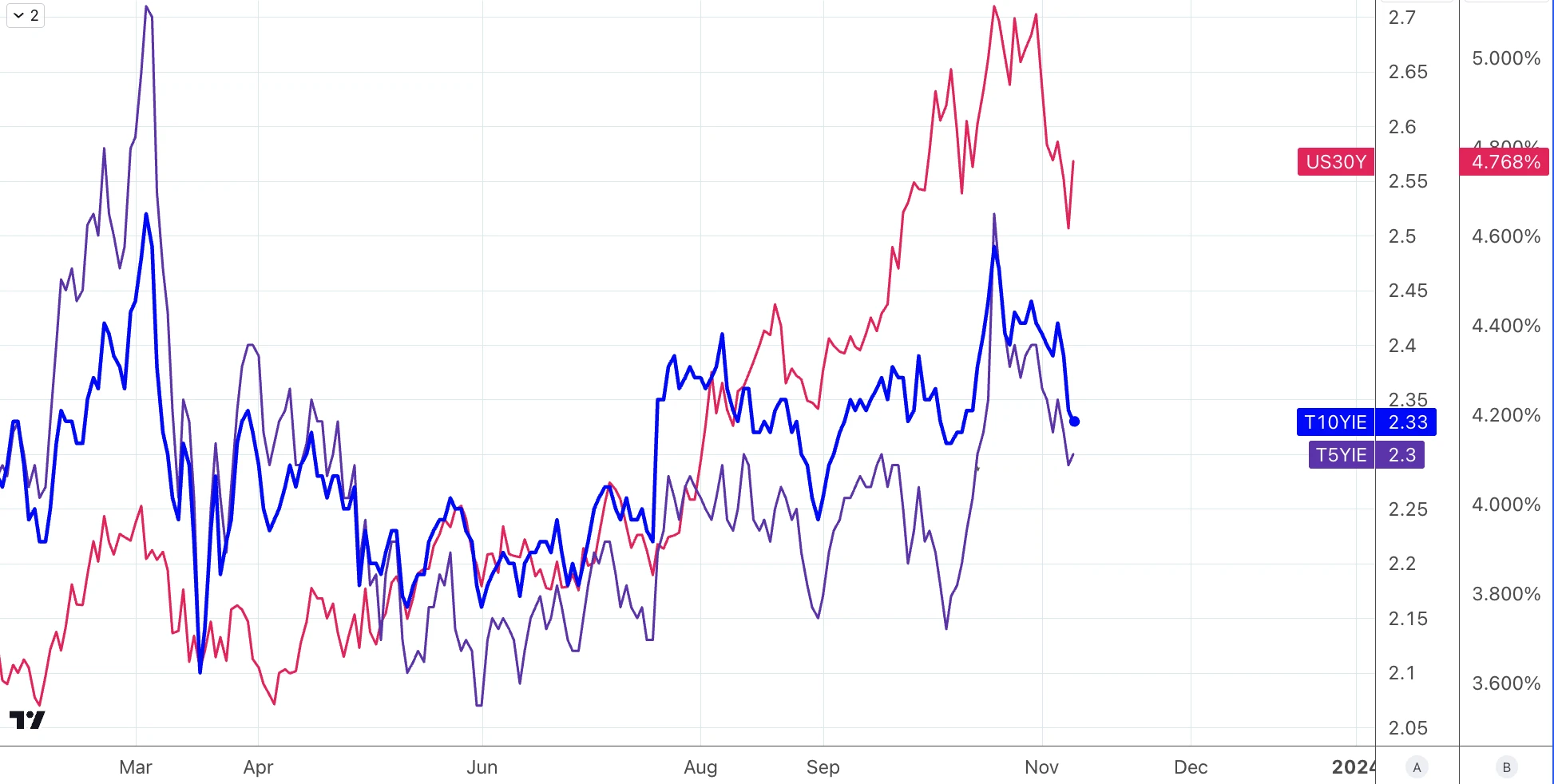

Shift in interest rate market attention

Although most believe that the Fed has reached the end of raising interest rates, long-term interest rates are still rising/hovering at high levels, which may reflect the markets shift of attention from inflation to fiscal deficits due to changes in inflation expectations in the secondary market after August 10 Not large (+4 bp Vs + 40 bp), and has fallen rapidly since the end of October.

Because fiscal revenue is now reduced, the Fed is shrinking its balance sheet, and the largest overseas investors are reducing their corresponding U.S. debt investments, there is reason to expect that this year’s deficit of 1.7-1.8 trillion will continue for several years. Moreover, investor interest is still mainly on the short-end Bill side. As Treasure continues to increase long-term issuance, the term premium will be further raised, thereby significantly increasing the cost of debt.

The U.S. Treasury’s own forecast is for net issuance, including bills and coupons, to be at $2.4 trillion and total issuance at $4.2 trillion in 24, and they believe there is room for further rises in term premiums.

China data

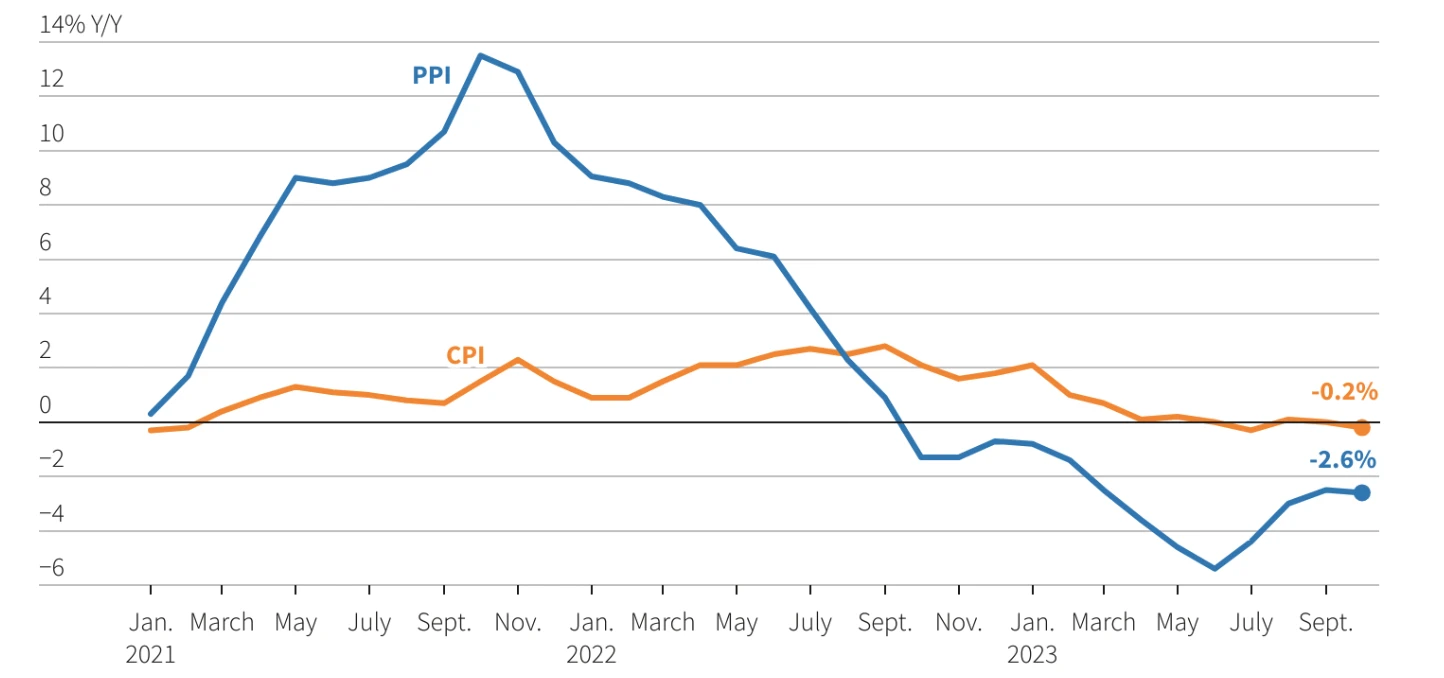

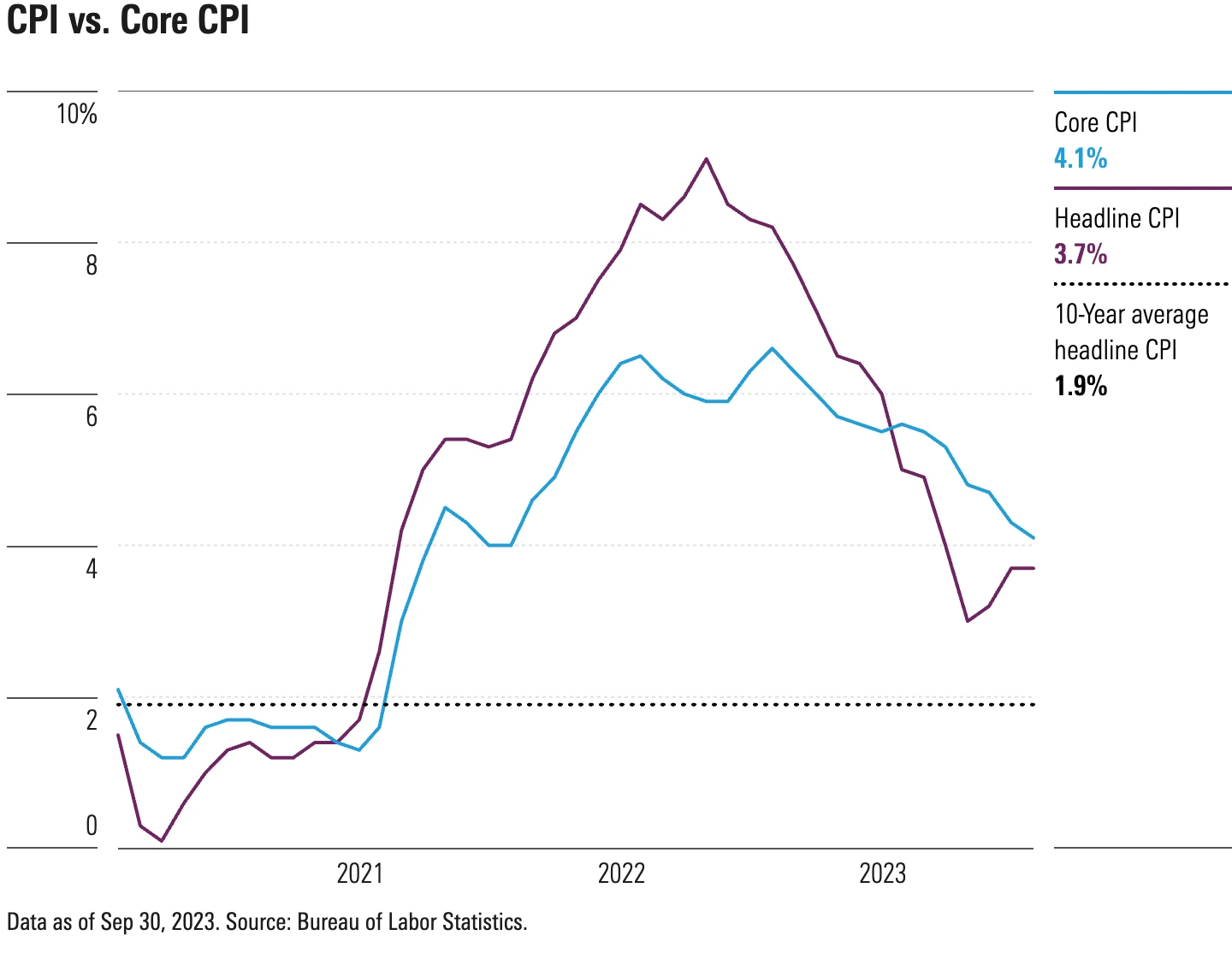

Chinas CPI fell back into negative territory in October, with key domestic demand indicators showing weakness not seen since the pandemic, while deflation intensified in factories, casting doubt on the chances of a broad economic recovery:

The CPI in October was -0.2% year-on-year, and it was 0.0% in September.

The CPI in October was -0.1% month-on-month, and it was +0.2% in September.

The PPI in October was -2.6% year-on-year and -2.5% in September.

Core CPI, which excludes food and fuel prices, slowed to 0.6% in October from 0.8% in September

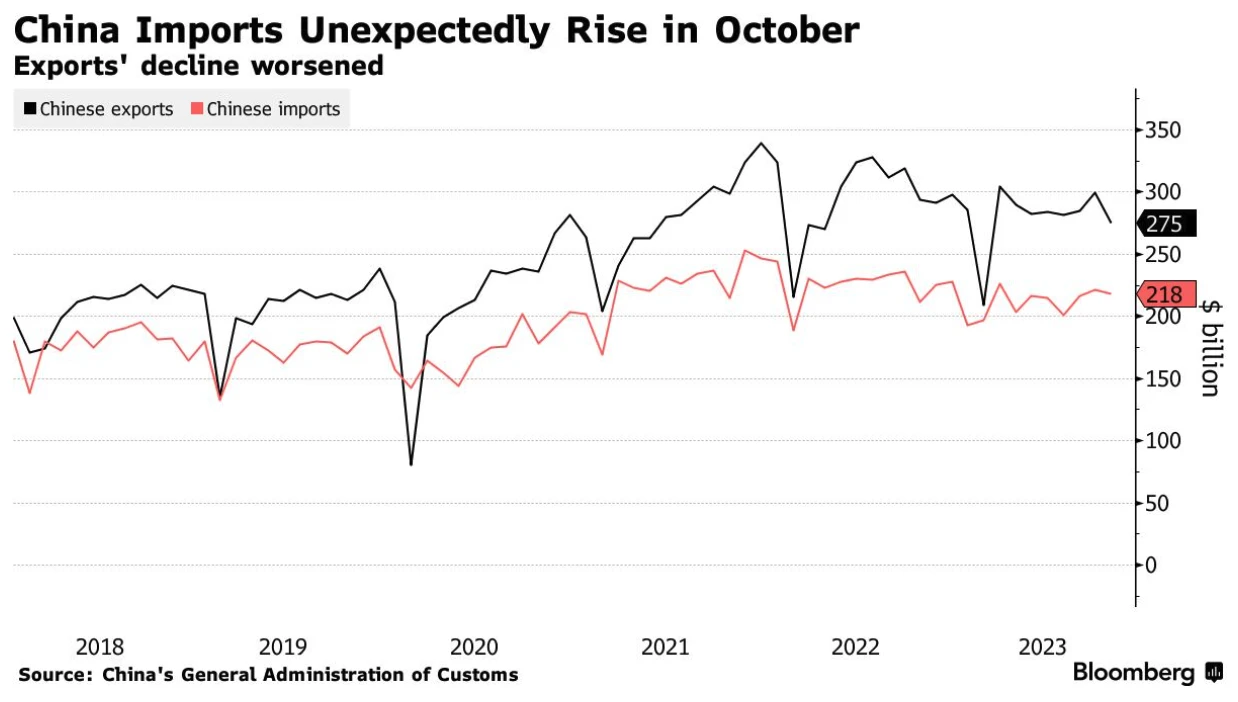

Chinas imports rose 3% year-on-year in October, the first increase in eight months and defying expectations for a decline. Exports, on the other hand, fell sharply by 6.4%, much lower than analysts forecast of a 3% decline. This is the sixth consecutive year-on-year decline in exports, disappointing the market.

Originally, everyone expected exports to pick up and the global supply chain to recover, but todays data confirms from the side that most developed economies will experience a mild recession or weak GDP growth in the short term, reflected in their declining demand for foreign goods.

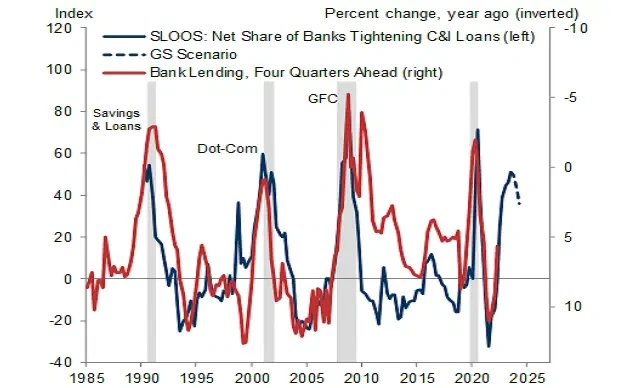

Loan investigation

According to the Federal Reserves Senior Credit Officers Opinion Survey (SLOOS), lending standards in the U.S. banking industry continued to tighten in the third quarter, but the pace of tightening slowed and loan demand was weak.

Goldman Sachs analysis shows that when SLOOS surveys show banks becoming more cautious in their lending practices, it tends to precede actual lending declines, which often leads to recessions.

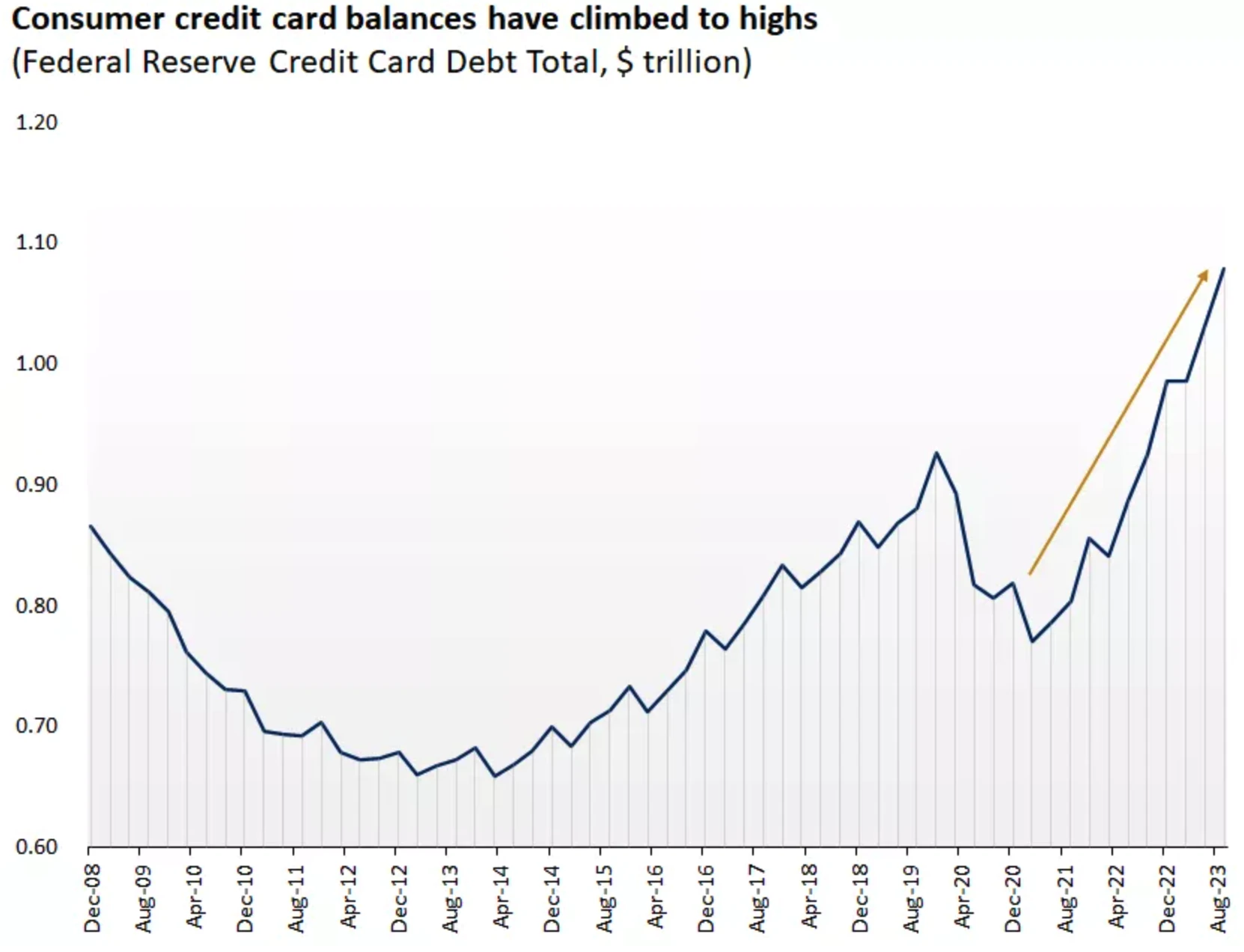

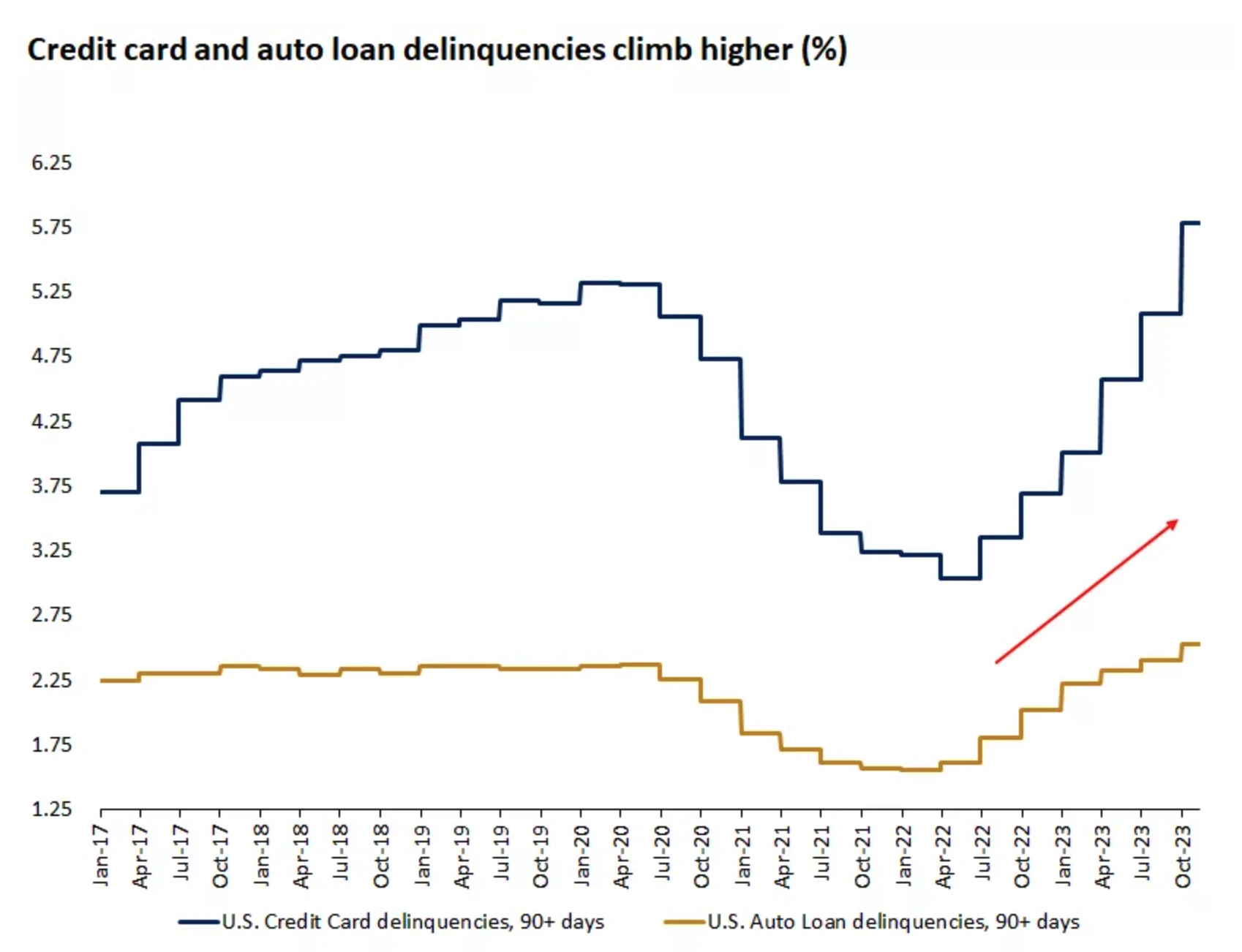

Also worth noting is that consumers total credit card debt has increased. As of the third quarter of 2023, total U.S. credit card debt has risen to more than $1 trillion, the highest level on record (left chart). As household credit card balances increase, so do delinquency rates in areas such as credit cards and auto loans, which have surpassed their COVID-19 peaks (right chart):

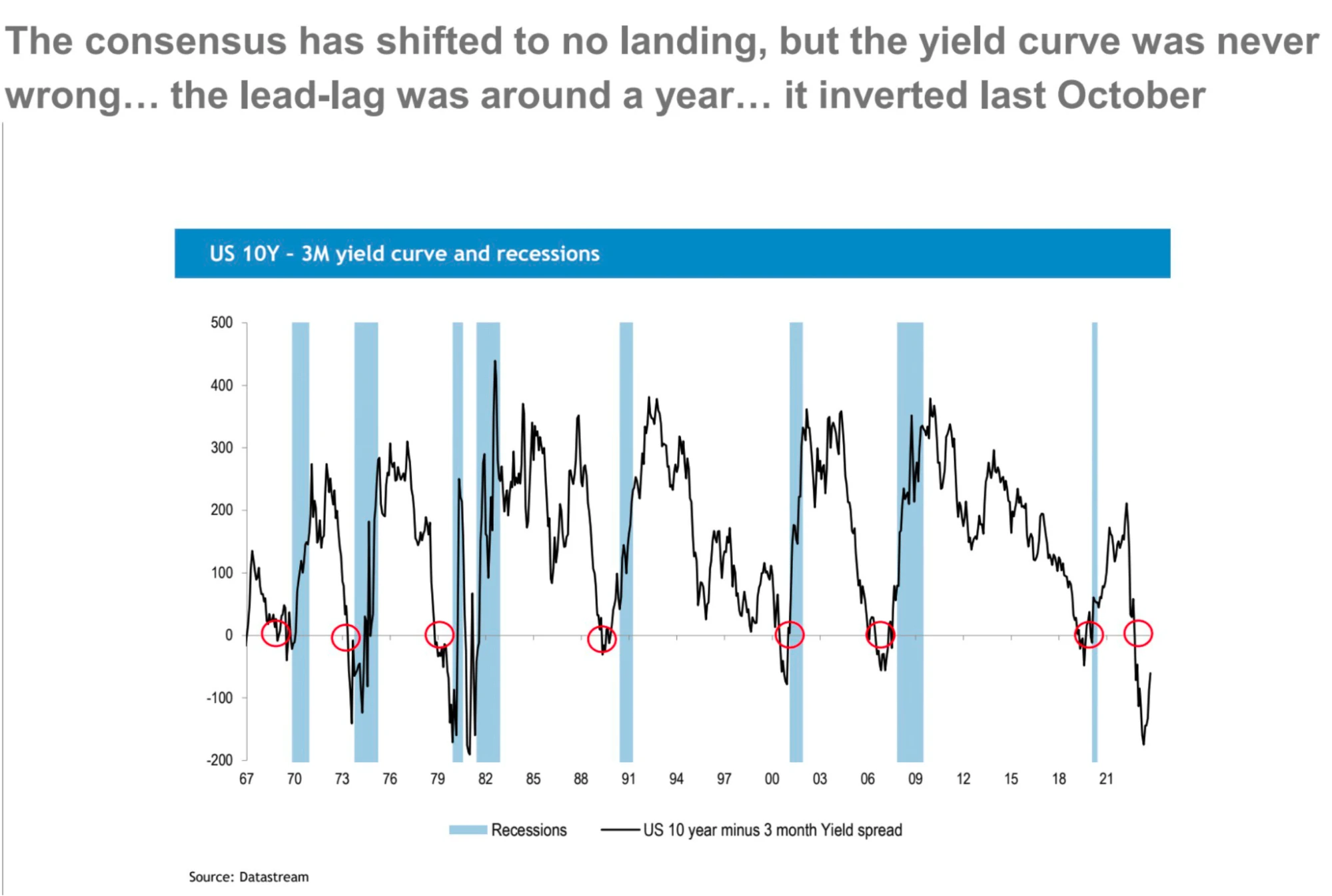

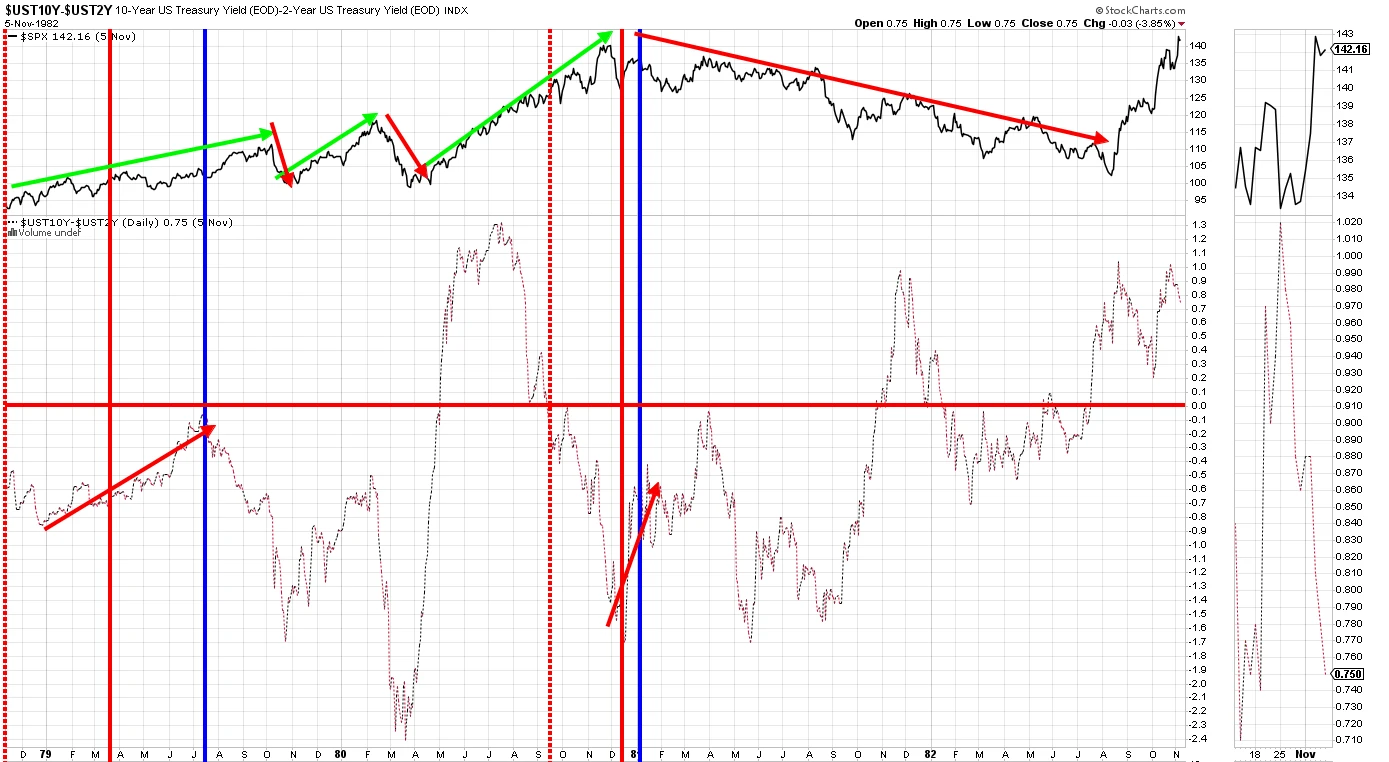

yield curve inversion

Over the past fifty years of yield curve inversions followed by recessions, this indicator has never failed:

However, there are also limitations to using the yield curve to predict economic recession and stock market performance, because there are positive and negative situations in the performance of the stock market after the yield curve inverts, with large differences in time and magnitude.

The situation in 1979 – 1982 from inflation to stagflation was somewhat similar to today, with 10 y-2 y being deeply negative for many years, which confused investors and the market. Much like today. It reversed in 1979, and the market fell twice a few months after the breakout reversal. Before entering the 1981-82 Great Bear Market, which was also the most severe recession after World War II, the yield curve inverted and then inverted at least three times, including two corrections of more than 10%. Now we just experienced our first upside down flip in October.

Positions and Fund Flow

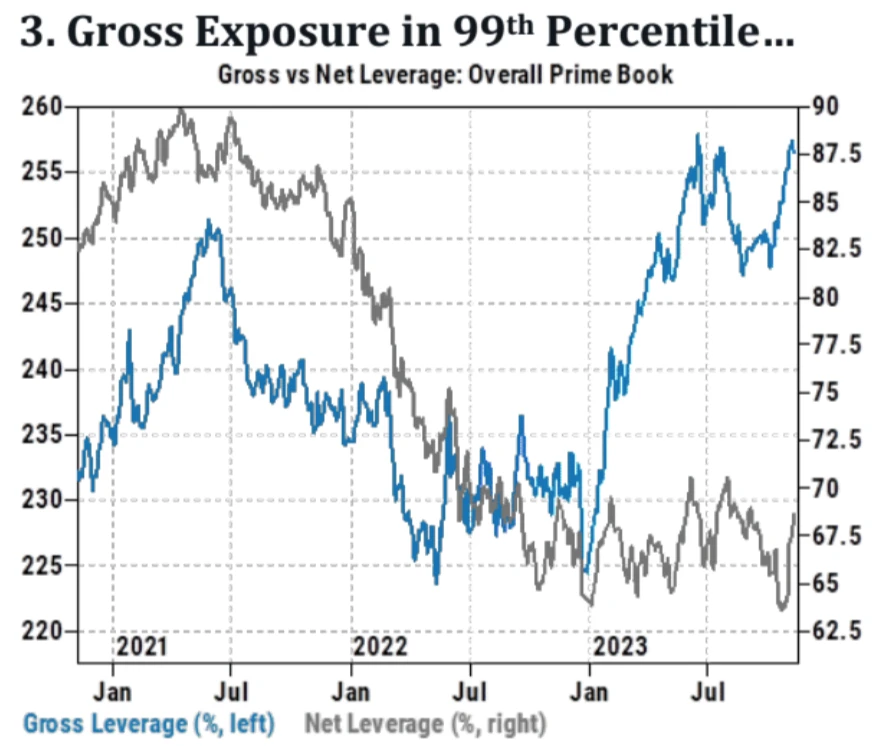

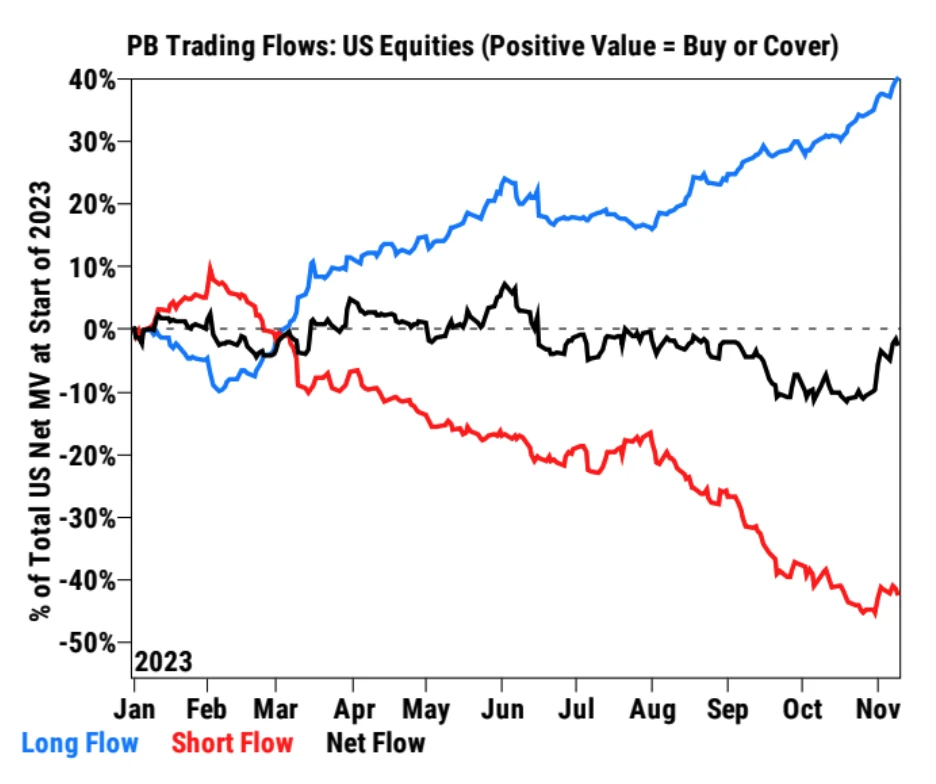

Goldman Sachs Prime data: The total leverage ratio of U.S. stocks has risen to the 99th percentile of history, but the net leverage ratio is not high yet; the willingness of short sellers to close positions is suspended, and bulls are actively adding positions.

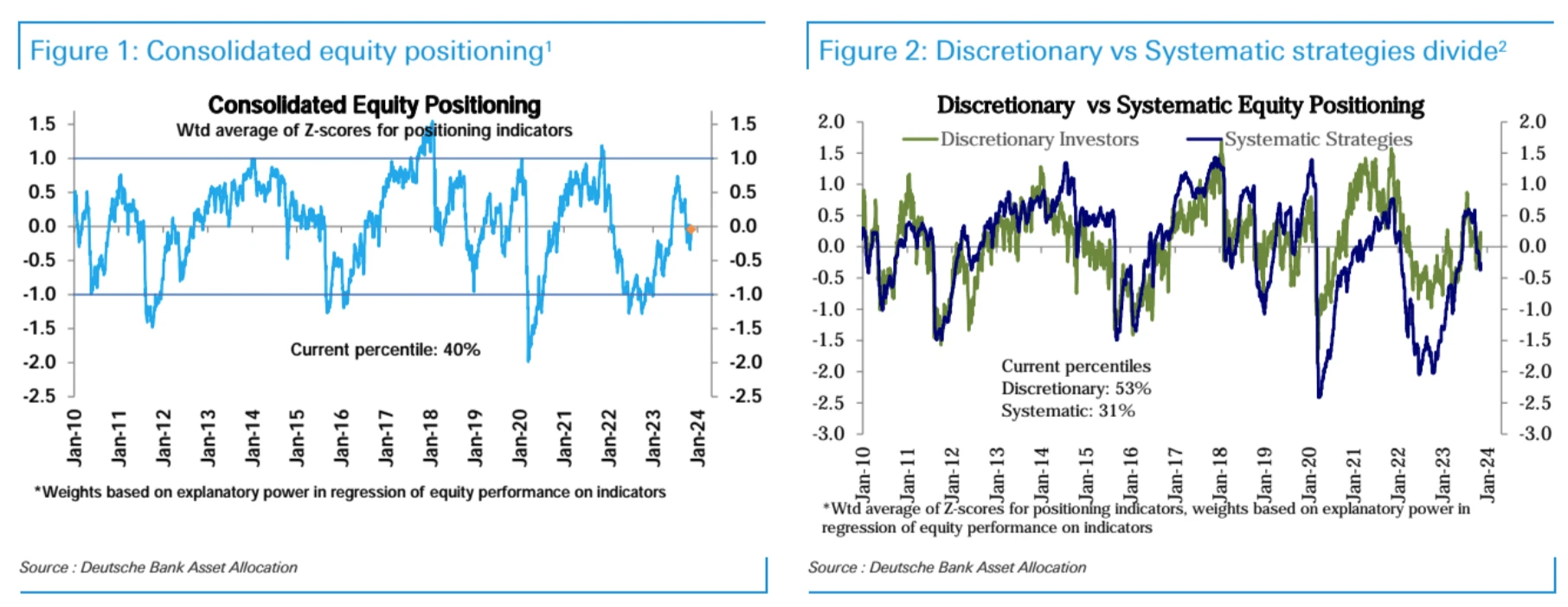

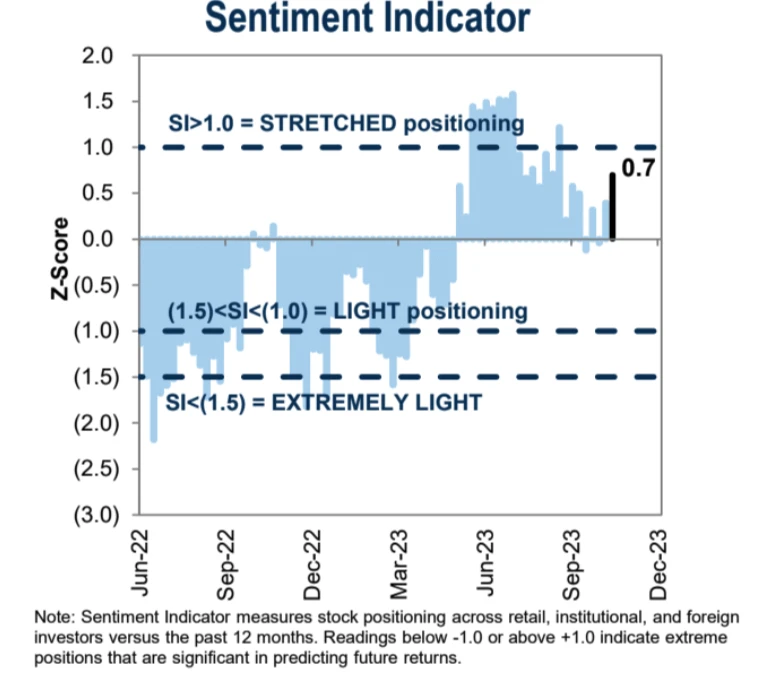

Overall stock positioning rebounded to neutral levels, mainly as subjective investor positions rebounded from below neutral levels to slightly overweighted. Systemic strategic positions also increased slightly but remain slightly underweight.

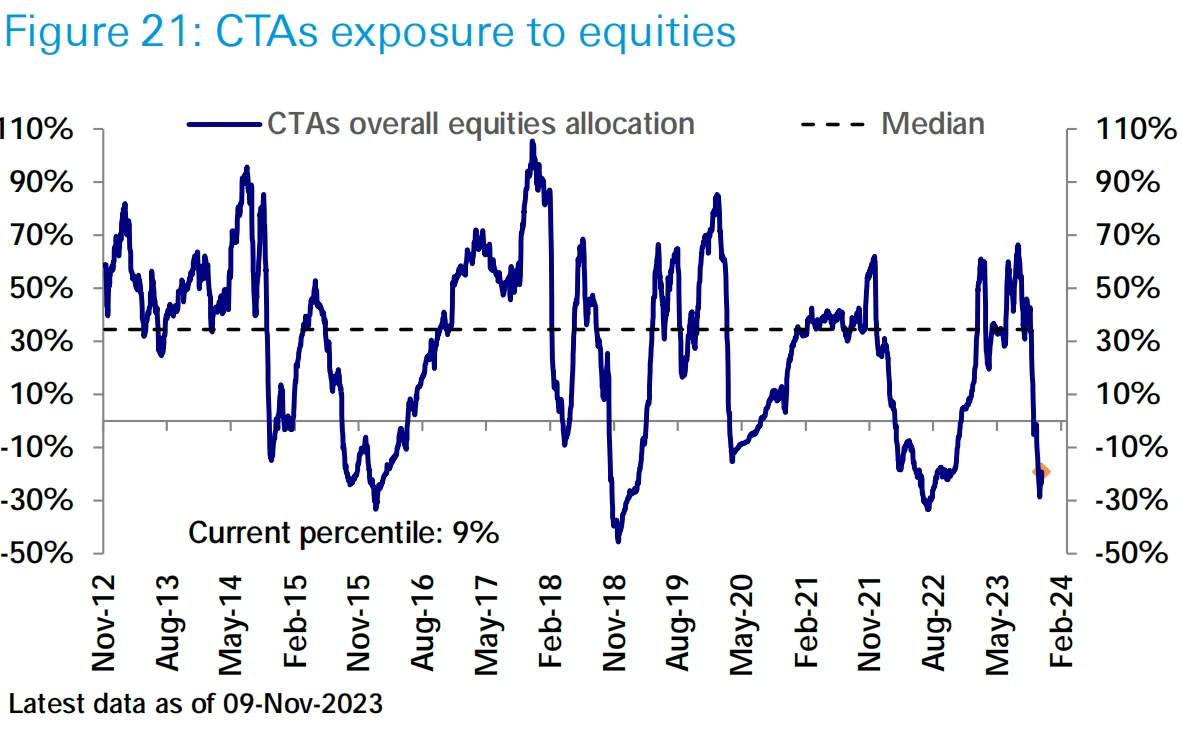

CTA fund stock positions increased slightly last week, but remain low by historical standards (6th percentile).

Supported by a rebound in equity and bond markets, equity funds ($9 billion) saw strong inflows this week for the first time in more than a month, with U.S. ($11 billion) inflows rising to a six-week high.

Inflows into bond funds ($11 billion) accelerated to a four-month high. Money market funds ($77.7 billion) saw their biggest weekly inflows in seven months, and high-yield bonds ($6.3 billion) saw their biggest weekly inflows since June 2020, reflecting investors increased pursuit of riskier assets.

market sentiment

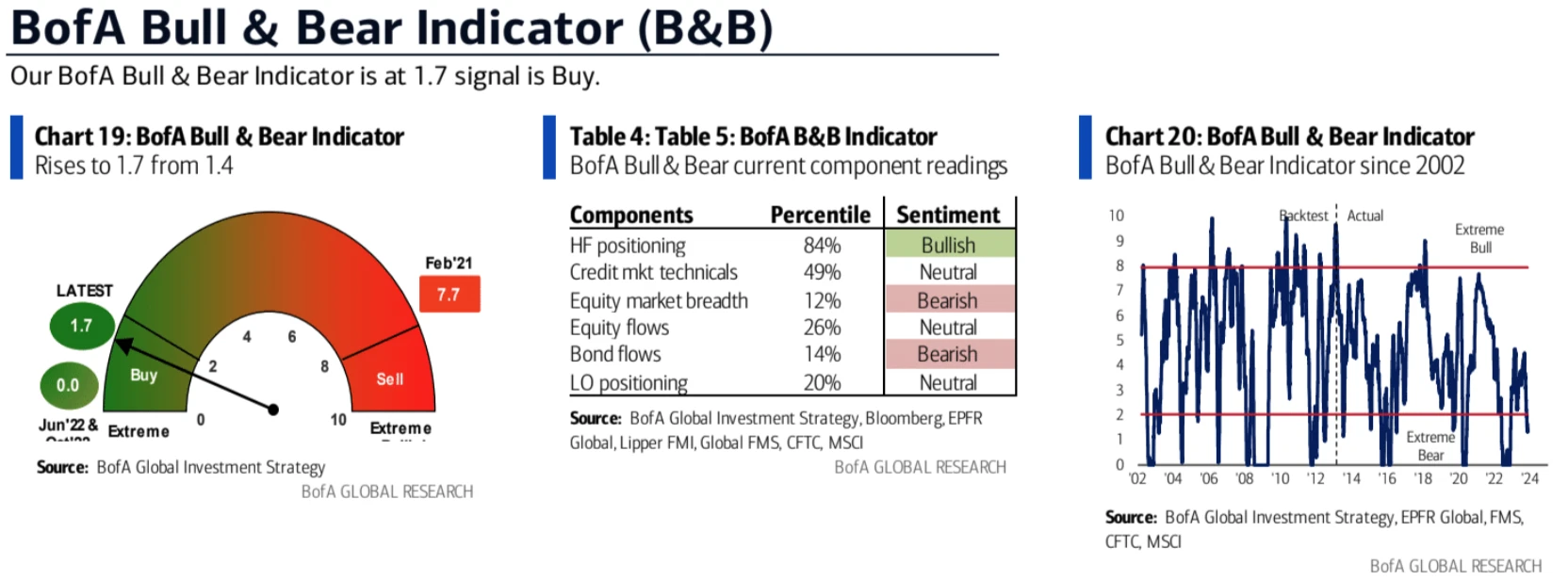

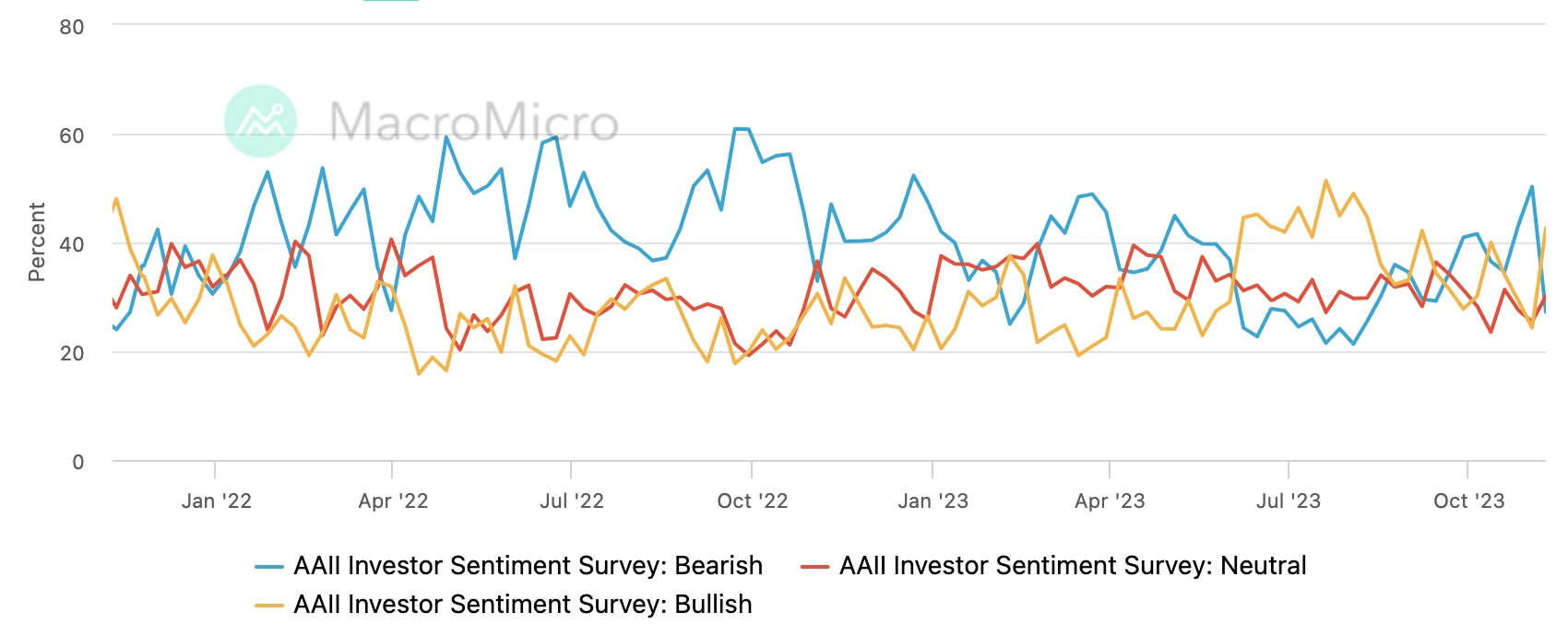

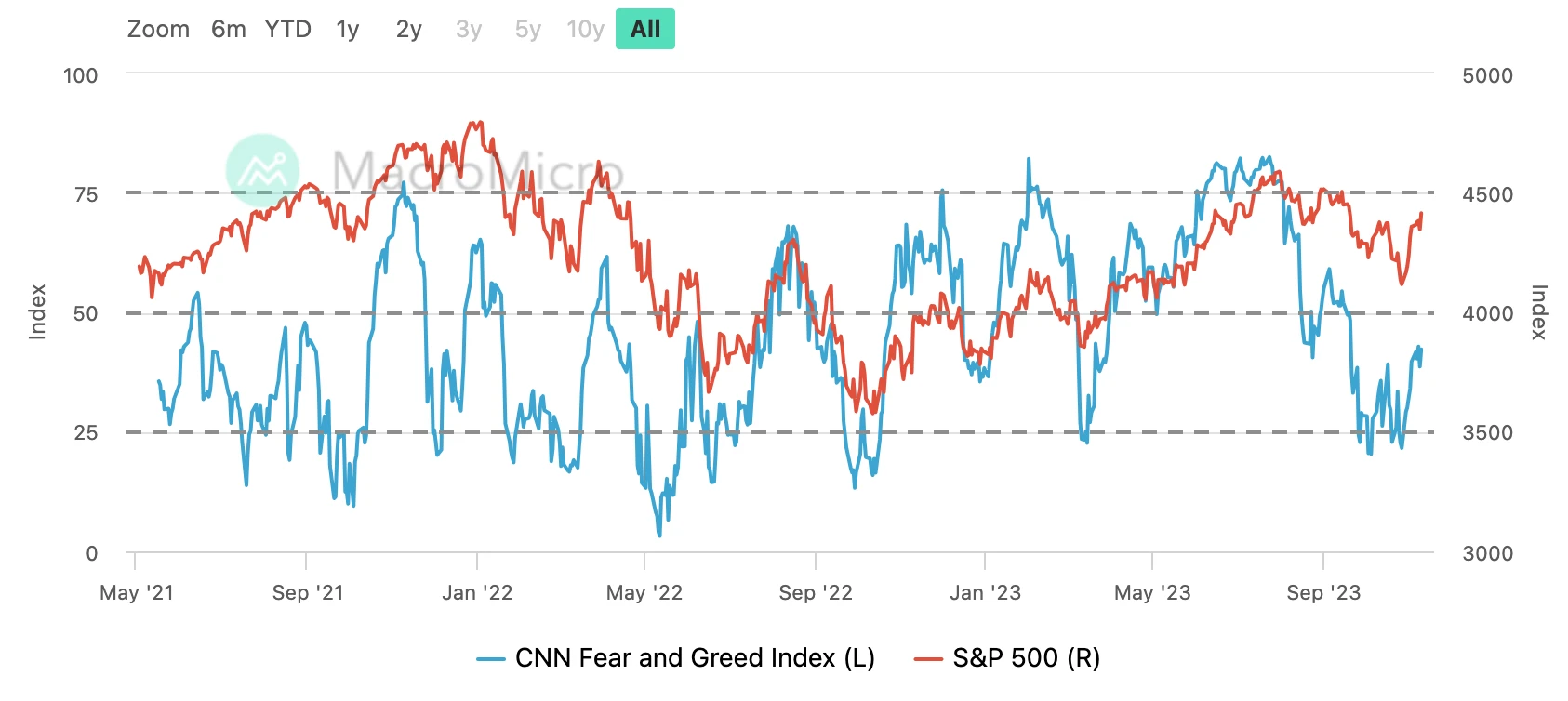

Consistent with the position data, it reflects that the repair process is still in progress and there is still room for improvement.

AAII short ratio dropped dramatically:

Follow this week

Apec summit (while shutting down, we must break ranks with China)

Wednesdays meeting between Biden and Xi was a complex event that spanned geopolitical, economic and human rights issues. Expectations for major breakthroughs are low, with the focus likely to be on improving communication and solving specific problems, such as blocking fentanyl. The United States aims to maintain its economic influence in the region, while China seeks to repair and strengthen its economic ties amid recent challenges. In addition, this week we may see a series of high-level contacts between Chinese and American companies and investors in an attempt to send a signal that both sides are open for business. Xi will have a dinner to address U.S. business executives, which may be more emotionally charged. Good things.

inflation data

According to current forecasts, headline CPI is expected to rise 0.1% month-on-month, down from 0.4% in September, and up 3.3% year-on-year, down from 3.7% last month. Core CPI is expected to rise 0.3% month-over-month and 4.1% year-over-year, both unchanged from the previous month. CPI data over the past few months have been largely in line with expectations. Energy is likely to be the biggest driver of the recent downward trend in prices, with the market also looking at a slowdown in rents and owner-equivalent rents. As in previous months, rising service prices will remain the main support for core inflation in October.

We believe that the markets focus will still be on core inflation. If it continues to hover at a level slightly above 4%, growth in the fourth quarter may also slow down significantly, which may trigger discussions of stagflation. GDP Now now forecasts Q4 +2.1%, flat at the lowest level in 5 quarters.

institutional perspective

Goldman Sachs has released its global economic outlook for 2024. Key views include:

Global economic growth will remain stable in 2024, and inflation in developed countries will continue to fall. Goldman Sachs predicts that global economic growth will be 2.6% (average annual growth rate) in 2024, and the U.S. economic growth may once again lead developed countries. With the exception of the Bank of Japan, most developed country central banks have completed their interest rate hike cycle, but the pause in interest rate hikes will extend into the second half of 2024.

The U.S. economic growth advantage will continue. Although U.S. real income growth will fall back to 2.75% in 2024 from 4% in 2023, this should be enough to support consumption and GDP growth of no less than 2%. Eurozone growth is expected to be 0.9% in 2024, but recent macro weakness may continue to constrain growth, and Italy faces the risk of fiscal stress.

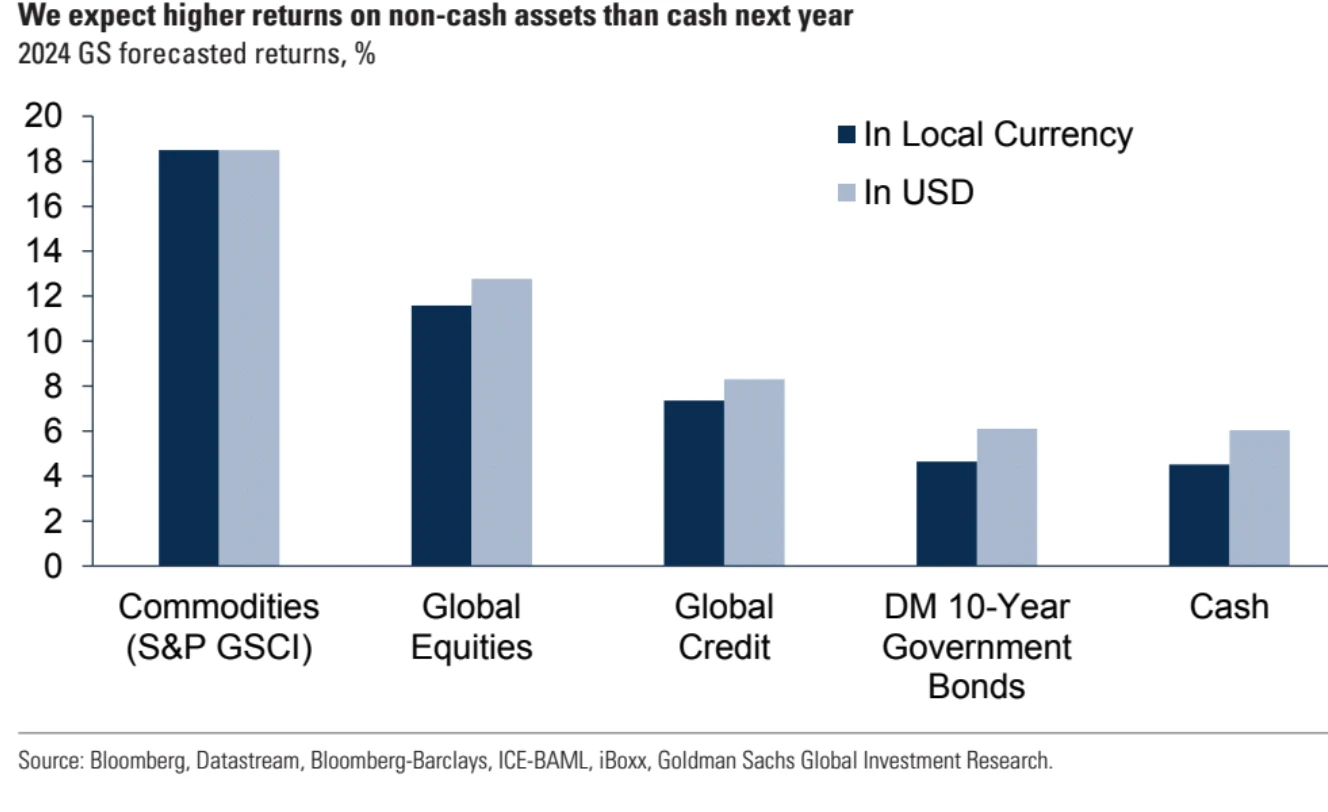

The key challenge for investors is that the optimistic macro view is fully reflected in market prices. At the same time, asset risk premiums have narrowed and valuations are not cheap. Therefore, asset allocation should be more balanced than this years portfolio focused on cash, as each asset class provides protection against at least one significant tail risk.

The era of low-yield equilibrium is over. 2024 should establish the notion that the global economy has emerged from the post-global financial crisis environment of low inflation, zero policy rates and negative real returns. While the transition from this environment has been uneven, expected real returns on most assets have turned positive again, and capturing higher returns is critical to portfolio construction.

Although the global economic outlook remains positive, there is also a dark side. Several major risks deserve attention, including the possibility that a higher yield environment will lead to an increase in emerging market sovereign risks, a further increase in sovereign pressure in the Eurozone, difficulties in the monetary policy trade-off between China and Japan, and rising geopolitical tensions.

The report suggests several ways to improve portfolio returns:

Increase duration risk. As current yields rise, investors gain a greater buffer of protection. In addition, yields have adjusted in price, and the value of bonds as a safe haven asset has increased.

Invest in cyclical stock sectors such as energy. In a benign growth environment, the earnings yields of these sectors are more attractive.

While cash yields still set a high bar, tight U.S. stock valuations may constrain gains, and emerging markets and credit assets are also worth considering. These assets could perform better if inflation falls more than expected and central banks cut interest rates sooner.

It is important to maintain a balanced asset allocation next year compared to allocating more cash this year. Because for example bonds: if the risk of recession rises, bond values rise; commodities (especially energy): if global growth is better than expected, oil prices could rise sharply; stocks and emerging market assets: if inflation falls more than expected, central banks cut interest rates faster , stocks and emerging markets could be strong

Morgan Stanley’s outlook for the economy and market prospects in 2024. Key views include:

Growth in advanced economies is expected to be below trend, while growth in emerging economies is expected to be polarized. Global growth is slowing and most advanced economies can avoid recession.

The policy interest rates of the Federal Reserve and other central banks have been basically stable in the first half of the year, and will only slowly decrease in the second half of the year. The Bank of Japan is moving towards policy normalization.

Many asset prices already price in expectations of favorable macro shifts. There is not much room for error, so be careful. U.S. assets fare relatively well, while emerging markets face greater challenges.

Falling yields provide opportunities for “income investing.” Government bonds, investment-grade bonds, and more can earn 6%+.

In terms of stocks, as corporate profits face a recession, the overall stance remains cautious, with a preference for defensive stocks.

The market environment in 2024 will be challenging, but unlike 2023, prudent strategies will be needed.

Similarity to Goldman Sachs’ view:

It is expected that the growth rate of developed economies will be lower than the trend, and global economic growth will slow down.

Everyone believes that inflation has peaked, but it will take time to fall back, and the policies of central banks in various countries have gradually turned to easing.

They are all optimistic about fixed income assets and believe that they can obtain higher returns.

Everyone is optimistic about the Japanese stock market

The difference is:

Goldman Sachs is more positive about emerging markets, while Morgan Stanley believes it faces greater challenges.

In terms of the stock market, Goldman Sachs has a positive outlook for stock market performance, while Morgan is relatively cautious.

Goldman Sachs believes that emerging markets have potential, while Morgan believes that emerging markets are relatively risky, mainly due to Chinas deleveraging.