Original author: Biteye core contributor Louis Wang

Original editor: Biteye core contributor Crush

This year can be said to be a big year for Layer 2 (this article mainly refers to rollup). Nearly ten Layer 2s have been launched on the mainnet.

On March 24, zkSync era was launched

On March 27, Polygon zkevm launched mainnet Beta

On July 17, Mantle announced the launch of the mainnet Alpha version

On July 18, Linea went online

Base mainnet launched in August

On September 12, Manta launched its Layer 2 mainnet Pacific

On October 10th, Scroll mainnet was launched...

What can be clearly felt is that Layer 2 is developing rapidly. Whether it is Op rollup or ZK rollup, which we thought was far away, they are all emerging at a spurt. You must know that it has only been more than half a year since the Arb airdrop.

The original vision of Layer 2 technology is to solve the expansion needs of Ethereum and improve transaction throughput. At the same time, it relies on Ethereum to maintain decentralization and security. It is a better user experience for users and is far lower than the handling fees of the main network. and smaller latency congestion.

This article aims to let readers understand some of the patterns and aspects of Layer 2 competition through on-chain data comparison.

01 Layer 2 Overview

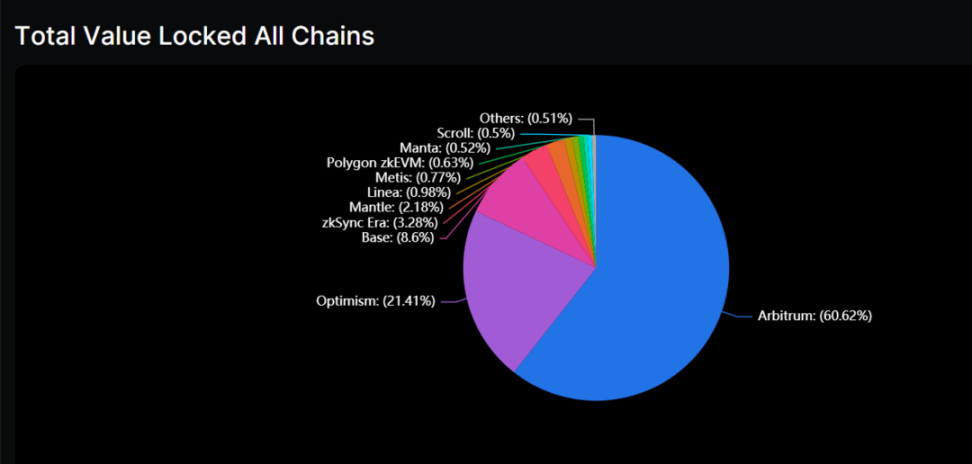

(Source: https://defillama.com/chains/Rollup)

According to DeFiLlama data, the current total locked-up volume of Layer 2 rollup is approximately $3.4 B. The first Arbitrum is far ahead with a TVL of $2.06 B, accounting for 60.62%, followed by Optimism, accounting for 21.41%.

Arbitrum and Optimism have first-mover advantages on the Layer 2 track and were the first mainnets to be launched. Together, they have captured more than 80% of the market share.

The TVLs of Base and zkSync era are more than $100M, while the TVLs of other public chains are less than $100M.

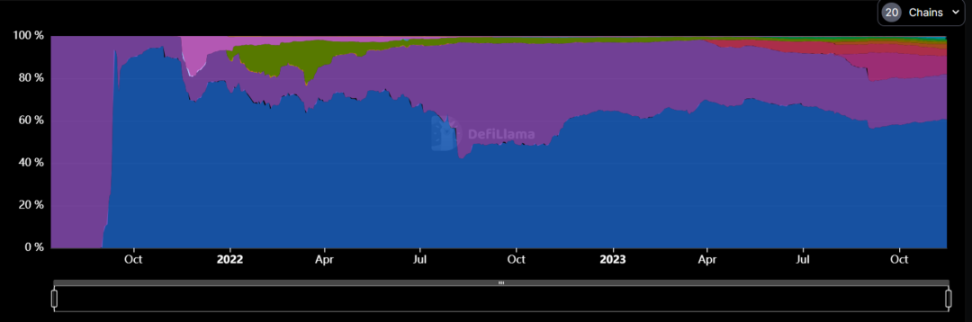

(Source: https://defillama.com/chains/Rollup)

Observing with a time scale, the diversity of the Layer 2 market has increased significantly since this year. Based on January this year, Arbitrums market share has been stable at around 60%, and has not been affected by latecomers, while Optimisms share has increased from 32% dropped to 21%.

Authors note: There is a big difference between DeFiLlama data and L 2B eatsTVL data. Taking Arbitrum as an example, L 2B eats ($7.5 2B) is even more than 3 times that of Defillama ($2.06 B).

This is due to the different statistical methods of the two platforms. L2B eats counts the cross-chain value, that is, how much money has been transferred to the target chain through the cross-chain bridge; while DeFiLlama counts the total amount locked in each dApp on the target chain. Sum.

To put it simply, the difference of $5 B is not used in any dApp on Arbitrum (maybe to store coins in the wallet), at least not in the dApp counted by DeFiLlama.

02 Arbitrum

(Source: https://defillama.com/chain/Arbitrum?users=false&txs=true&tvl=true)

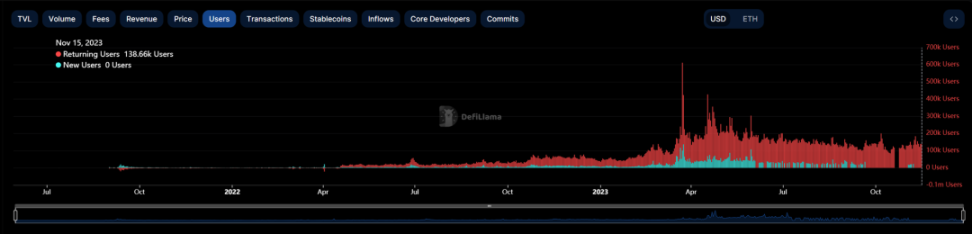

Arbitrum currently has more than 14.29 M independent addresses and has conducted a total of 418.45 M transactions with TPS 6.3.

The activity on the chain reached its peak during the airdrop in March, with more than 3M txn transactions in a single day. After the airdrop, the activity on the chain also maintained a good level and was not affected by this years market downturn.

(Source: https://defillama.com/chain/Arbitrum?users=true)

Arbitrum has many ecological signature projects, such as GMX, which accounts for 23% of TVL, the native DEX+LaunchPad project Camelot, the chain game TreasureDAO, etc.

Coupled with a number of projects that have migrated from the main network, the DeFi system is complete and innovative, and the overall ecological richness is high. Therefore, user retention is good, and nearly 3/4 of daily active users are repeat customers.

03 Optimism

(Source: https://defillama.com/chain/Optimism?txs=true)

Optimism has 57.66 M unique addresses and 177 M transactions, TPS 4.6. After the airdrop last June, OP’s activity still maintained a good growth momentum.

The native signature project Velodrome currently has a TVL of $145M, and most of the remaining TVL is supported by Synthetix and DeFi projects in its ecosystem, such as Lyra and Thales.

(Source: https://www.theblockbeats.info/news/44039)

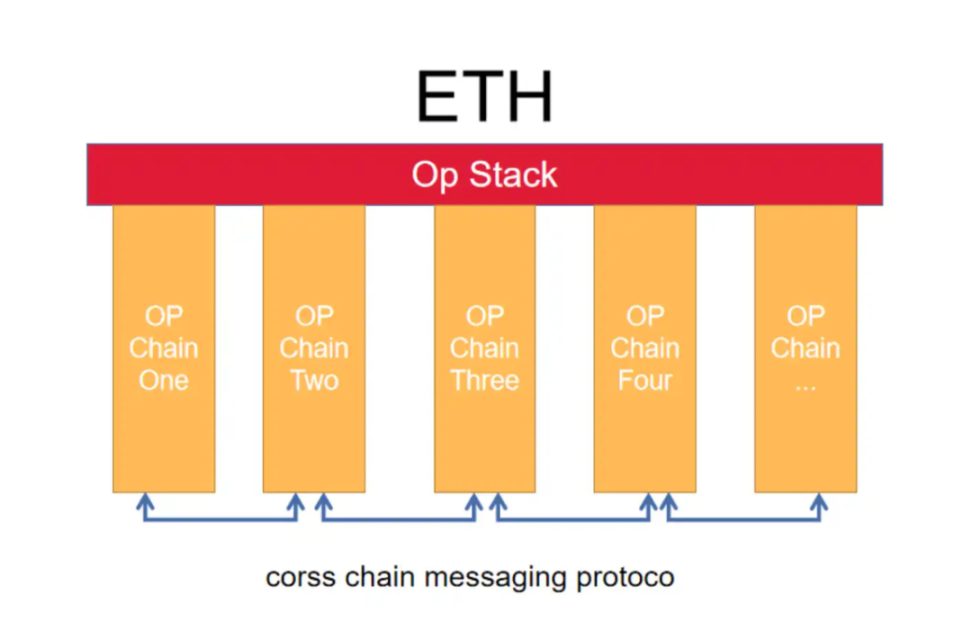

After OP upgraded bedrock, released the modular blockchain solution OP Stack, and proposed the vision of a super chain, it has obviously found its own path.

OP Stack allows developers to select and assemble the execution layer, DA layer, etc. according to their own scenarios and needs, and customize their own Layer 2 network, reducing the difficulty of launching a chain.

Adopters include Coinbase’s Base, BitDAO’s Mantle, BN’s opBNB, NFT-focused Zora, and more. Chains using OP Stack will also feed back OP to a certain extent. For example, Base will give part of its income to the OP treasury.

With the grand vision of super chain, OP soft-binds the project parties that use OP Stack to launch the chain, achieving the effect of prosperity and prosperity.

04 Base

(Source: https://defillama.com/chain/Base?txs=true)

As mentioned earlier, Bases Coinbase is based on Layer 2 issued by OP Stack. It currently has 2.4 M users, 67 M transactions, and TPS 3.8.

Its focus mainly comes from the phenomenal dApp, FriendTech. In the last 30 days, FriendTech generated protocol fees of $5.4M, and Base generated revenue of approximately $1.32M during the same period.

When the enthusiasm for SocialFi was at its peak, FriendTechs protocol revenue was even second only to Ethereum and Lido.

In addition to FriendTech, the native project that Base can play is Aerodrome, which is a fork of Velodrome on OP. It currently ranks first with TVL$ 55.53 M.

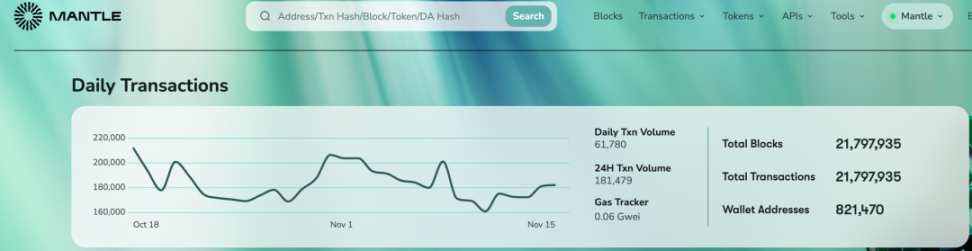

05 Mantle

(Source: https://explorer.mantle.xyz/)

Mantle designs Layer 2 based on the Optimism OVM architecture, adopts a modular design, and uses EigenDA as the data availability layer to significantly reduce the cost of rollup.

Currently, there are 820,000 addresses on Mantle and 21M transactions have been conducted.

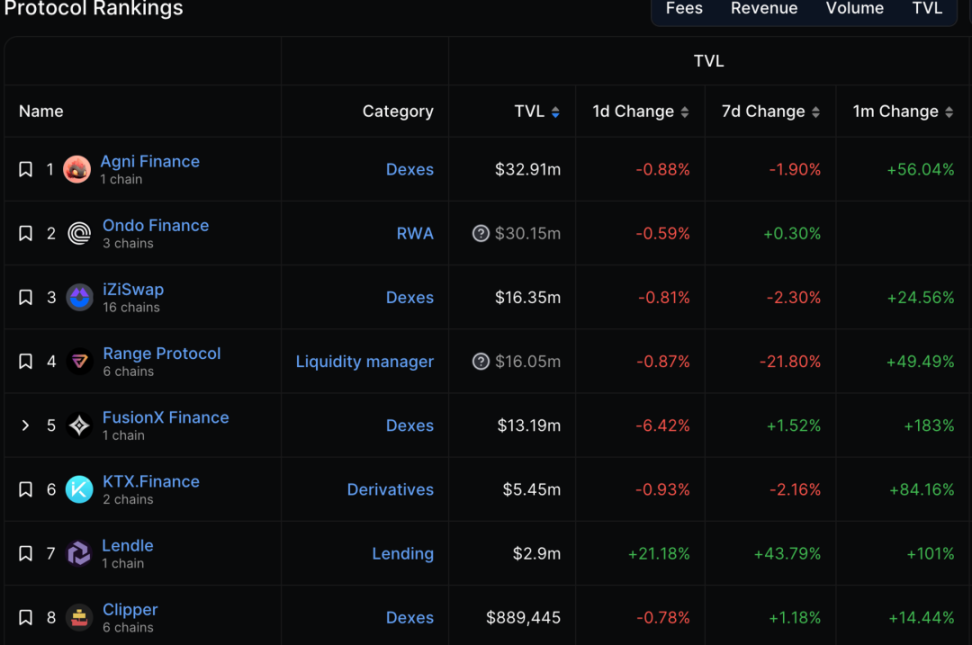

(Source: https://defillama.com/chain/Mantle)

Among Mantle TVLs leading projects are many native DEXs, such as Agni and FusionX. Mantle has extremely strong financial backing.

The reserve value in Mantle Treasury exceeds US$2 billion, including more than 220,000 ETH. It has the advantages of deposit scale and liquidity, laying a solid foundation for its subsequent LSD track project.

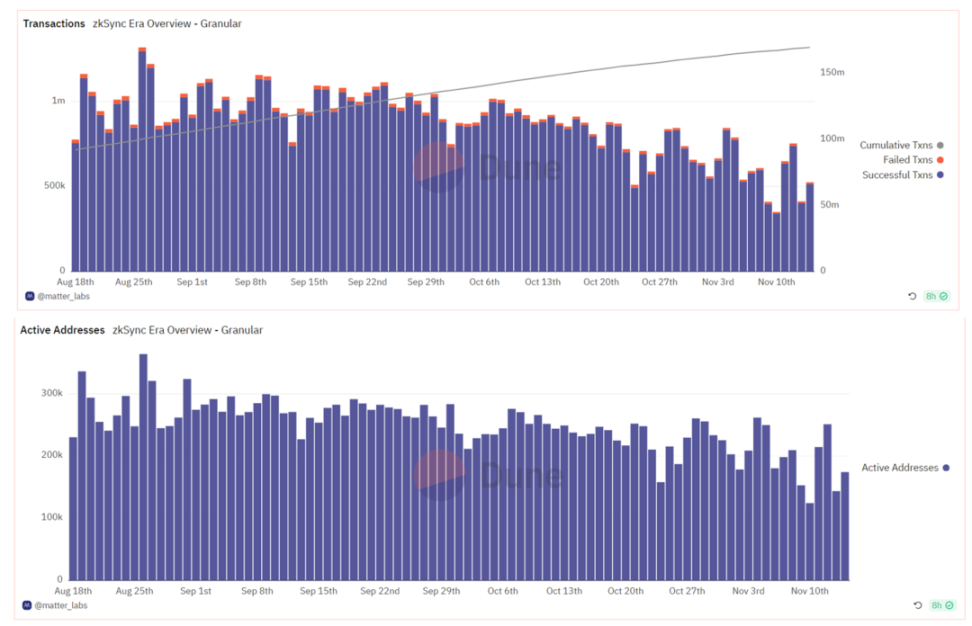

06 zkSync Era

(Source: https://dune.com/matter_labs/zksync-era-overview)

zkSync is a veteran leader in the zk series, developed by the MatterLabs team.

Version 1.0 Lite only supports token payment scenarios, while version 2.0 era is an EVM-compatible universal mainnet with more than 4.67 M independent addresses.

zkSync originally used the zkSTARK algorithm. On July 17, it announced the launch of a new proof system Boojum, transitioning from zkSNARK to the zkSTARK proof algorithm.

(Source: https://dune.com/matter_labs/zksync-era-overview)

The launch of zkSync Era follows the Arb airdrop, so users have great enthusiasm and expectations for zkSync. In just over half a year, 4.6 M independent addresses and 165 M txn have been accumulated. zkSync has built-in native account abstraction and does not require the use of ERC 4337 solutions.

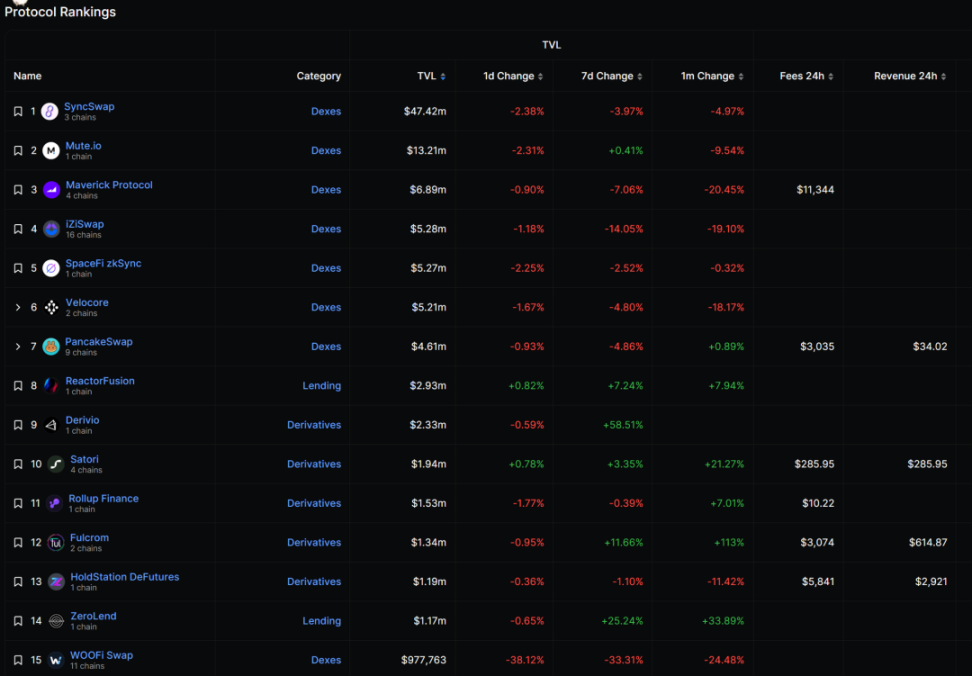

There are very few migrations of leading projects on zkSync, such as Uniswap and AAVE, which gives more opportunities to native projects and some new projects, such as SyncSwap, Mute, Maverick, etc. The current applications are concentrated in DeFi.

(Source: https://defillama.com/chain/zkSync%20Era)

07 Scroll

(Source: https://blockscout.scroll.io/)

Scroll, the zkevm project known as the light of the Chinese people, announced the mainnet launch on October 10. In just a few weeks, the TVL reached $17M, and more than 2M addresses have completed 4.7M transactions.

Before Scroll announced its mainnet, there were overwhelming pictures alluding to Scroll on Twitter, including many project parties and KOLs. The entire marketing atmosphere gave people a high-profile impression.

Within a week, Layer 0 announced support for the Scroll mainnet, Orbiter supports the Scroll mainnet USDT and USDC cross-chain, OKX wallet is connected to Scroll, and NFTScan supports the Scroll mainnet. The overwhelming response proves the influence of Scroll.

As early as the testnet period, 100+ project tests were deployed on Scroll, covering various tracks.

There are currently more than 30 projects deployed on the mainnet. The situation is similar to zkSync. The multi-chain deployed projects are basically 50-50 split with native projects.

(Source: https://scroll.io/ecosystem)

08 Starknet

(Source: https://defillama.com/chain/Starknet)

Starknet is a general-purpose public chain that adopts the zk-Stark proof method and runs Cairo-VM instead of the EVM compatibility pursued by most Layer 2.

There is no concept of EOA on Starknet. All are native AA accounts. Currently, more than 2.9M accounts have been deployed.

The contract language used on Starknet is Cairo instead of the more familiar solidity, which brings considerable technical obstacles to project migration.

Starknet restarted its mainnet this year with the major update of Cairo 1.0 and began official business. TVL has steadily increased to more than $40M. After the Palestinian-Israeli conflict, TVL experienced a period of rapid decline (StarWare is headquartered in Israel) and is currently stable at $ 30M.

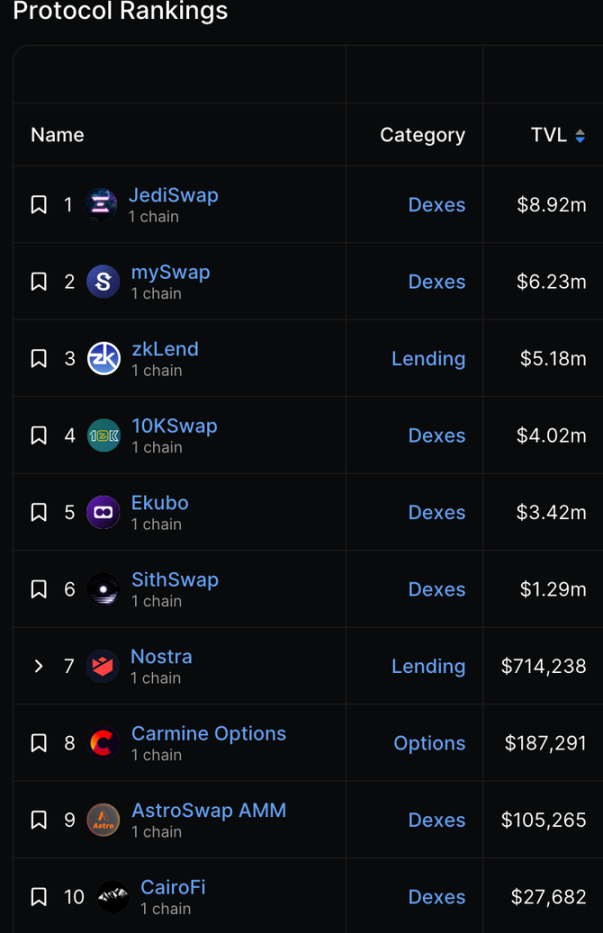

The top TVL projects on Starknet are all old projects that have been deployed during the Beta mainnet period, such as JediSwap, mySwap, etc.

A project worth mentioning is Ekubo, which ranks fifth in TVL but accounts for 75% of the total transaction volume on Starknet. Recently, UniSwap DAO passed a proposal to provide 3 million uni worth about 12 million US dollars to support the development of Ekubo in exchange for 20% of Ekubos token share.

(Source: https://defillama.com/chain/Starknet)

09 Manta Pacific

(Source: https://defillama.com/chain/Manta)

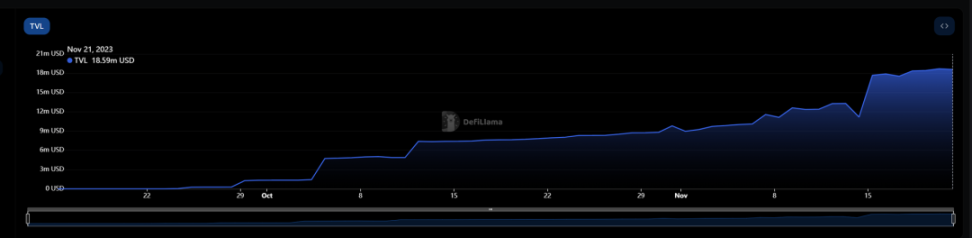

Manta Pacific is a zk general-purpose Layer 2 launched by Manta. In the future, it will use Celestia as the data availability layer to minimize user interaction costs.

Since its launch in September this year, TVL has raised $18.59M in two months, with 166k independent addresses and 2.16M transactions completed.

Manta initially considered adopting the OP Stack solution, and later migrated to Polygon CDK and became part of the Polygon ecosystem.

Over 300,000 zkSBT have been minted on Manta’s NPO website, with over 200,000 wallet installations.

(Source: https://defillama.com/chain/Manta)

Aperture Finance is the industrys leading liquidity management platform with an intent-based architecture that allows users to fully automate strategies.

Its project ApertureSwap is the native DEX on Manta. Like Uni V3, it allows users to provide centralized liquidity. It currently ranks second with TVL$ 4.95 M.

10 Linea

Linea is a zkevm Layer 2 solution launched by ConsenSys, the parent company of Little Fox Wallet.

As one of the most important infrastructures of the blockchain, MetaMask has 30 million monthly active users. These users can all become potential users of Linea. Coupled with the strong background of the founding team, investors and a valuation of US$7 billion, they can Let Linea become the hottest Layer 2.

Less than half a year after its launch, it has accumulated 1.68 M independent addresses and generated 18.36 M transactions.

(Source: https://defillama.com/chain/Linea?volume=true&tvl=true)

Lineas current TVL has exceeded $27M. SycnSwap and Velocore, which rank first and fourth, are native DEXs on zkSync and have been migrated to Linea.

(Source: https://defillama.com/chain/Linea?volume=true&tvl=true)

11 Comprehensive comparison

The basic data of each Layer 2 is summarized in the following table:

(TVL data is taken from DeFiLlama, TPS is taken from the average data of L 2B eats on November 17, and the remaining data is taken from various blockchain browsers)

Regarding the data from the Ethereum main network to each Layer 2 cross-chain, you can refer to Chaineye’s data dashboard, which has data and proportions that change over time for easy comparison and viewing:

(Source: https://chaineye.tools/)

12 Summary

It used to be said, Fat protocol, thin application, which means that most of the blockchain value is captured by the protocol layer, and a small part is distributed in the application layer. The public chain grabs most of the profits by selling block space.

However, as the infrastructure continues to improve and various Layer 2 public chains continue to emerge, there is suddenly a feeling that there are redundant protocols and insufficient applications.

The liquidity in a bear market environment is inherently limited. At the same time, this liquidity is also split between the two layers due to the Layer 2 arms race.

Each chain is looking forward to incubating native innovative applications, but there is often a rare moment of inspiration, and more often it is a multi-chain fork of a successful project.

The emergence of FriendTech has introduced a lot of attention, funds and users to the Base chain. You can see that TVL has soared with the explosion of FT.

Base has stated that it will not issue its own tokens. It can be understood that the proportion of on-chain users interacting for Base airdrops is relatively low. To a large extent, users and funds are attracted by the phenomenal application of FT. The contribution and impact of a killer app on the public chain can be seen clearly.

When users make profits on such dApps, the profit funds are likely to spill over to other projects in the ecosystem, benefiting the entire public chain.

At the same time, FTs protocol revenue is much higher than Bases public chain revenue, and the peak value is even more than 5 times different. Therefore, in addition to bringing about a wave of SocialFi craze, the emergence of FT also makes us think about whether it is due to the maturity of the infrastructure. , have truly good consumer applications become scarce?

Future applications no longer need to revolve around well-funded public chains, just like the explosion of DeFi on Ethereum is due to the large amount of funds deposited.

The mature Layer 2 and supporting cross-chain infrastructure can already meet the demand for smooth migration of funds and can pursue good applications. In the future, it may gradually move from thin applications to fat applications.

(Source: https://defillama.com/protocol/friend.tech? fees=true&tvl=false)

This is why after FT became popular, every public chain tried to support its own chain’s SocialFi projects, such as Linea’s TOMO, Avalanche’s SA, etc. Regardless of whether these projects were ultimately successful or not, we can clearly see from the attitude of the public chains. , for native star projects, it is what all public chains desire.

(Source: https://defillama.com/chain/Base)

For Layer 2, the need to capture users, retain users and keep funds active cannot rely on airdropped PUA.

Take the two most mature Layer 2, Optimism and Arbitrum, as examples. After the airdrop, the user activity and transaction volume on the chain did not weaken, but became stronger and stronger. They have their own native star projects, such as GMX on Arb, Velo on OP, etc.

The two public chains are also constantly launching incentive plans, such as Arbs short-term incentive project STIP, and OPs round after round of retroactive incentives.

How to maintain long-term vitality of the public chain is a very difficult and complicated matter. It requires the efforts of the public chain project team to implement the plan, and also requires the participation of more developers and funds.

From a higher strategic perspective, what really drives a Layer 2 to stand out is the narrative level.

For example, OP promotes the narrative of super chain and the open source modular solution OP Stack, which attempts to form a galaxy that shines brighter than Cosmos on the second layer of Ethereum, and has gained a lot of supporters;

Similarly, Polygon also launched the zk modular blockchain solution Chain Development Kit (CDK), with adopters including Polygon zkEVM, Manta, Canto, etc.;

Arbitrum announced the chain development tool for the Layer 3 blockchain Arbitrum Orbit, and zkSync immediately launched the open source toolkit ZK Stack and said it would also support the construction of Layer 3;

Starknet fully promotes full-chain games; Zora specializes in NFT and rebate economy...

Each chain is promoting new narratives from all angles, because with the implementation of Layer 2, Layer 2 itself has become difficult to hype as a narrative.

In short, competition between Layer 2 is always a good thing for users. While enjoying the security of the Ethereum network, they can also enjoy low handling fees. Only with the maturity of all infrastructure can large-scale applications be made possible. Let’s look forward to the future of Layer 2 together!