Original author: David Han, Institutional Research Analyst

Original compilation: DAOSquare

quick overview

Following the approval of a U.S. spot Bitcoin ETF, the impact of the New York trading session on price volatility and volume became more apparent.

While stablecoin usage appears to be more evenly distributed between European and U.S. daytime hours, the distribution of on-chain transaction volume and fee data is more skewed toward U.S. time.

We believe this skewed activity highlights the huge demand for Crypto in the United States and the potential for further industry growth and capital inflows.

Although Crypto is a global industry, trading volumes during the US market session (as well as the second half of the European session) have a significant impact on the markets liquidity and price volatility. This was true before the U.S. spot Bitcoin ETF was approved and has since become even more apparent, especially among centralized exchange (CEX) platforms. The increased volume also translated into greater price action during the U.S. and European trading sessions, as well as wider market gains throughout the day.

On-chain metrics reflect a similar situation. The transaction volume of Bitcoin and Ethereum both reached peaks during the US period. Compared with off-peak periods, transaction costs during peak periods may increase by 50%. Decentralized exchange (DEX) trading volumes also echo those of CEX, although U.S. dominance on the chain is less clear. Regarding the use of stablecoins, trading volume and the number of active users are evenly distributed between US and European hours.

Overall, we believe that despite regulatory challenges, the data clearly demonstrates the significant U.S. influence in transactions and on-chain activity. The success of the US Spot Bitcoin ETF and its significant impact on the broader Bitcoin market further confirms that regulatory clarity in the US plays a key role in unlocking new capital inflows into the Crypto market.

Centralized exchange

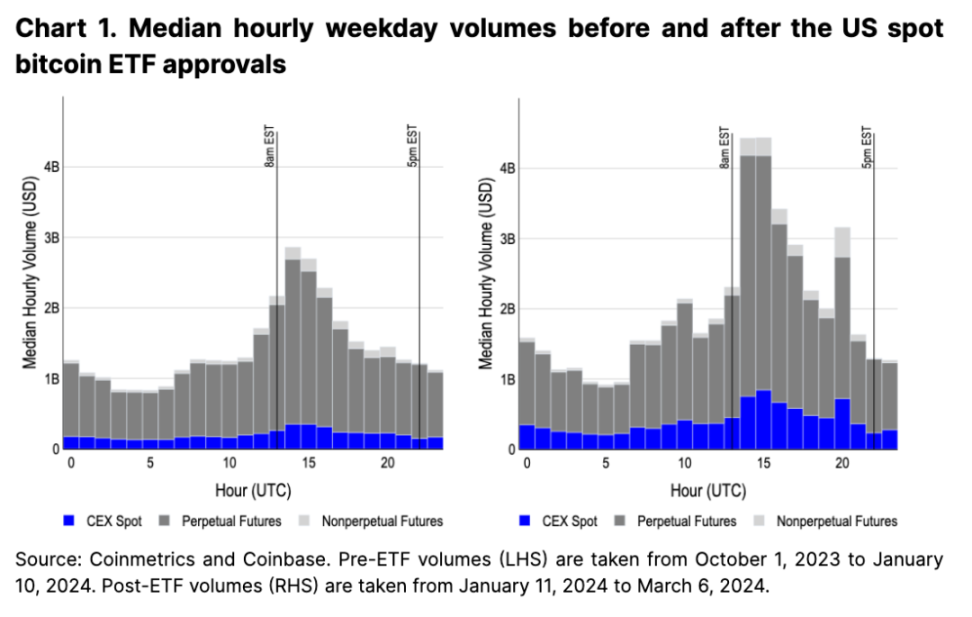

In addition to access to new institutional capital pools, a second-order effect of a U.S. spot Bitcoin ETF is an increased concentration of CEX trading volume during U.S. hours. Prior to the ETF approval, volume peaked during the opening hours of the U.S. market (9 a.m. to 10 a.m. ET), which was approximately twice that of the opening hours of Asian and European markets (see Figure 1). However, with the introduction of spot ETFs, trading volume for all spot, perpetual futures and non-perpetual futures products in the United States has risen to nearly three times that of other market trading hours.

Since January 11, spot CEX trading volume during the US session has increased by 130-200%, much higher than the 80-120% growth in trading volume in Asia and Europe. Perpetual futures peak-hour trading volumes in the United States also increased by nearly 70% (from 2.3 billion to 3.8 billion), while Asian and European peak-hour trading volumes increased by 20% and 50% respectively (from 1.0 billion to 1.2 billion respectively). billion, 1 billion to 1.5 billion). The growth in perpetual futures trading volume is particularly notable because these instruments are traded almost exclusively outside the United States. We believe this may indicate that offshore players may be taking advantage of stronger spot liquidity during U.S. hours, or that U.S. traders are using offshore entities to access these markets.

The launch of spot ETFs also resulted in a new surge in trading volume across all product categories at 3pm New York time. This is largely because ETF issuers want to align the prices of their funds with their benchmarks, and 6 of the 10 spot ETFs track the CME CF Bitcoin Reference Rate between 3pm and 4pm New York time - New York changes Body (BRRNY). As such, this is where authorized participants aim to acquire underlying Bitcoin as part of a cash creation (and redemption) model, typically hedging their positions through regulated products such as CME Bitcoin futures (for those without access to foreign perpetual markets ). In fact, the time period between 3 pm and 4 pm New York time is the time period with the largest trading volume for CME Bitcoin futures, with its trading volume exceeding other times by more than 60%.

Changes in earnings

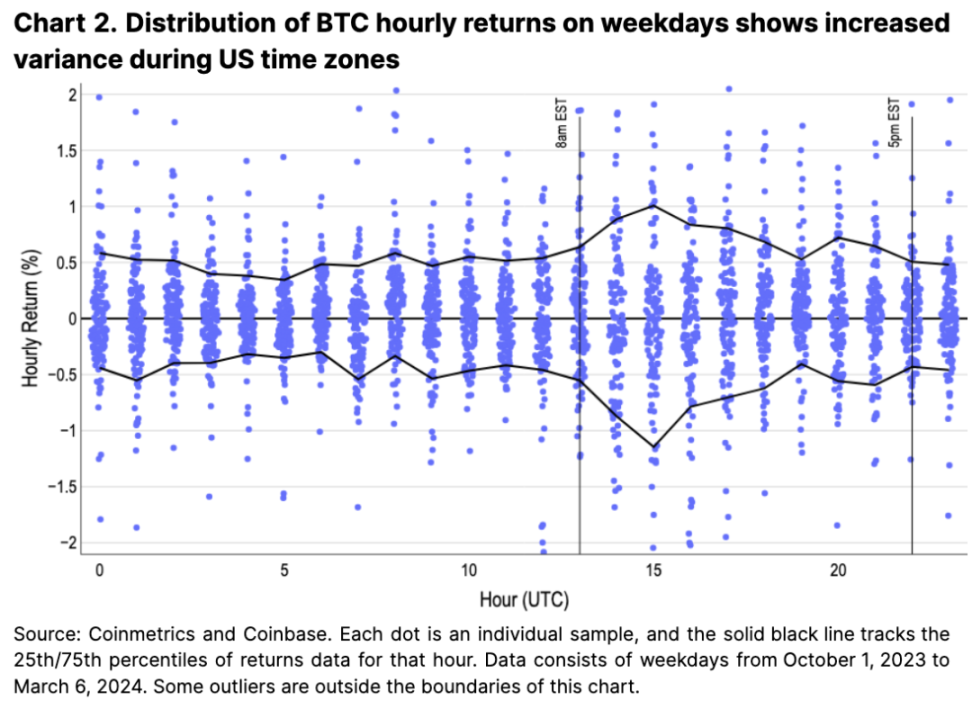

Bitcoin’s liquidity dominance in the United States is also reflected in its price performance. The blue portion of Figure 2 depicts a strip plot of hourly returns (showing the density distribution of returns), with the boundary between the 10th and 90th percentiles delineated by the black line. Periods with a wider range of returns correspond to earlier volume charts, indicating that high early trading volumes in U.S. markets often manifest into larger price moves. This suggests that early US markets offer the best opportunities for day traders in terms of liquidity and volatility.

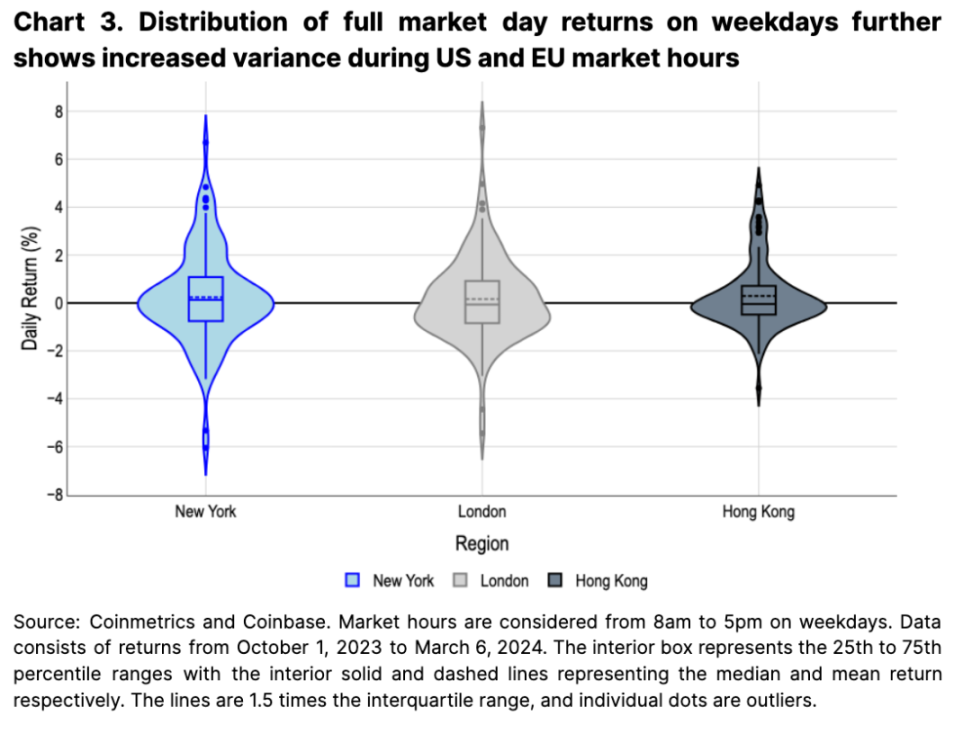

Measuring market-wide daily returns across different financial center time zones (from 8am to 5pm) can also reveal regional differences more broadly. The violin plot in Figure 3 shows that the returns for New York and London time are widely distributed (the plot shows the return probability using kernel density estimation, where the width of the violin represents the probability of obtaining that return). In comparison, returns during the Hong Kong session are much more concentrated. We believe this further highlights the importance of traders in the US (and to an extent Europe, whose closing times overlap with the US open) in driving Bitcoin prices.

Globally distributed network

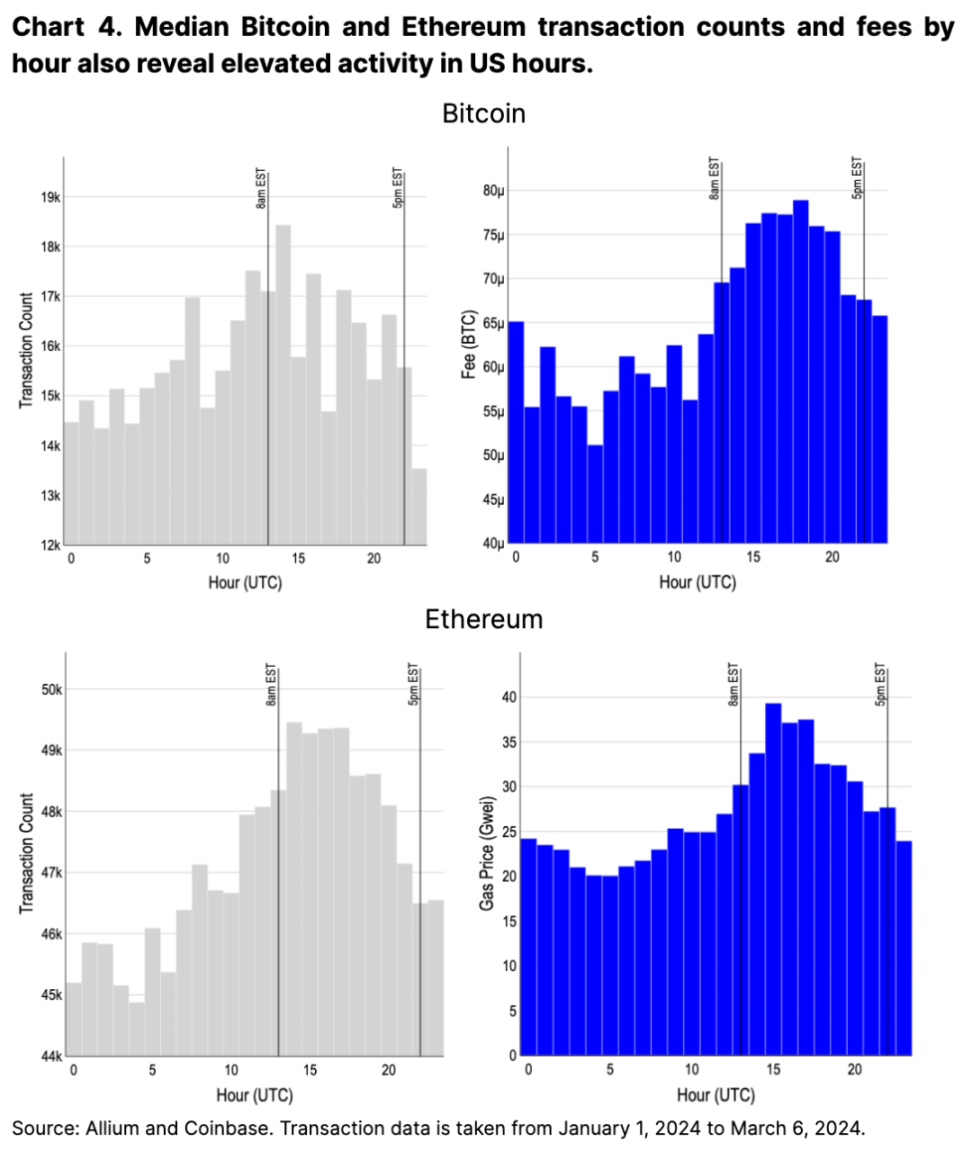

Despite their global accessibility and decentralized nature, Bitcoin and Ethereum also see peak activity during the U.S. time period. This is demonstrated by the fact that transaction costs during the US session increased by more than 50% from the lows (see Figure 4). On the one hand, we believe the rise in time slot usage in the U.S. is due to its large population being tech-savvy and well-capitalized compared to the rest of the world. We also believe that this activity may be partially caused by US traders managing positions in various wallets and exchanges (consistent with the increase in CEX trading volume during this time period).

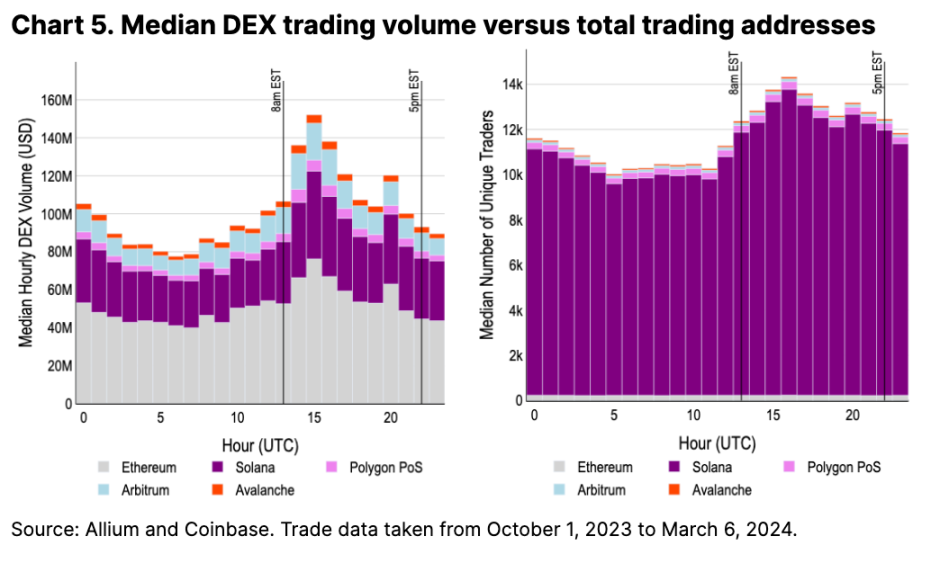

On-chain DEX trading volumes further corroborate the model of peak activity during U.S. market trading hours, although the difference is less pronounced compared to CEX. DEX trading volume surges significantly during the opening hours of the Asian market (UTC 0), which is approximately 70% of the US peak hour, while CEX trading volume is less than 30% of the US peak hour (see Figure 5). This volume ratio did not change significantly before and after ETF approval.

We believe that because DEX is a relatively new product, coupled with the differences in the market structure that supports it (such as traditional centralized limit order books and automated market makers), the difference in trading volume of DEX is not as obvious as that of CEX. This creates a newer, more level playing field that has only really begun following Flash Boys 2.0’s seminal paper in 2019, which discussed advantageous on-chain transaction strategies (and more broadly, maximum extractable value) .

Additionally, we do not believe that the number of unique transaction addresses is a clear proxy for zone usage. These numbers are skewed by airdrop expectations, especially on Solana where transaction fees are cheap. Solana’s airdrop from leading DEX aggregator Jupiter has released only the first of four rounds. It has yet to set exact dates for the next rounds, so we think the metric may continue to deviate quite a bit for some time.

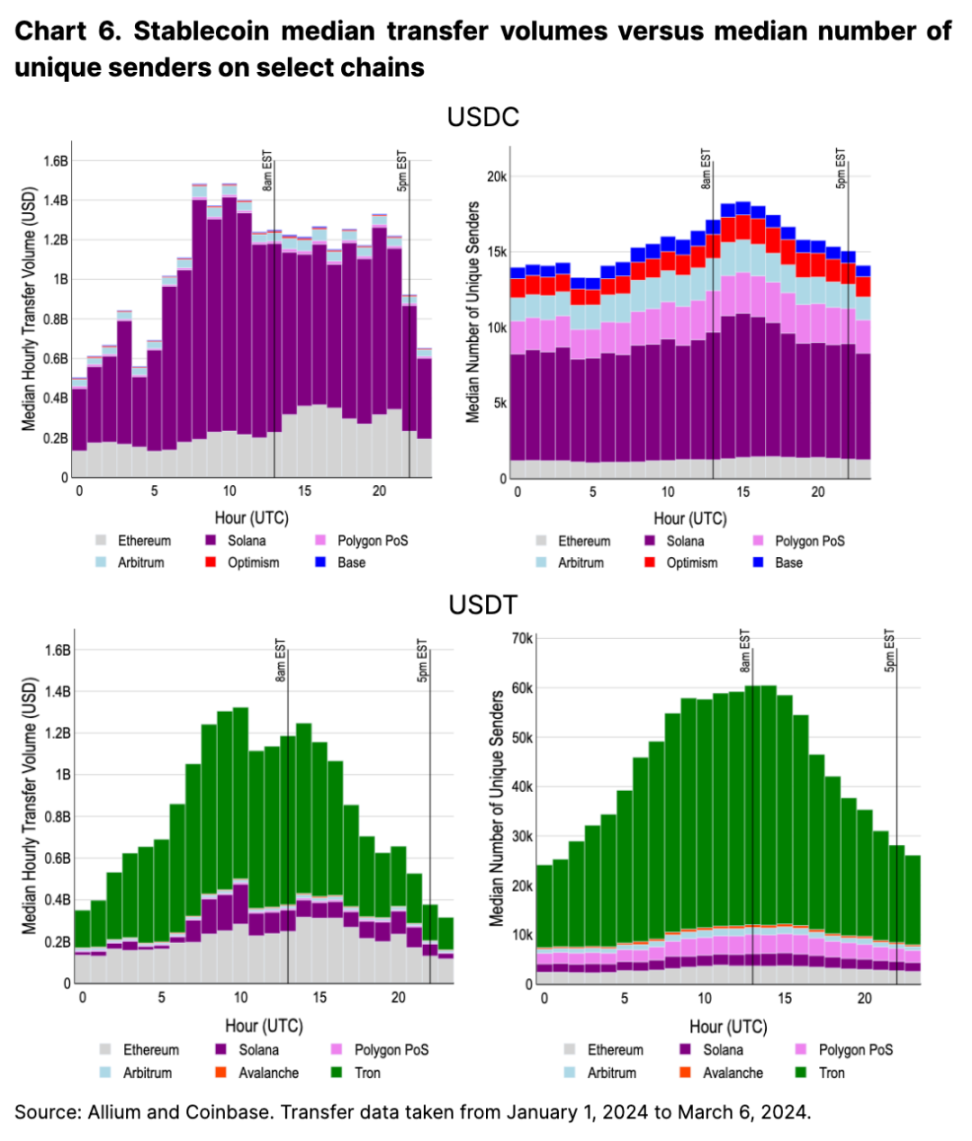

In addition to DEX, we believe stablecoin transfers are another key indicator of Crypto usage based on time zone. Importantly, usage statistics for stablecoin transfers are generally not skewed by short-term airdrop incentives in the same way that DEX activity is. What’s also interesting is that this is the first activity that isn’t heavily tilted toward U.S. market times.

Solana USDC transfers, which account for most of the transaction volume, peaked during the European session, but Ethereum-based transaction volume was more biased towards the US session (see Figure 6). That said, although not by much (the peak was 17,000 active transfers per hour, and the low was 13,000), the total number of transfers did appear to have a soft peak early in the US session. USDT trading volume also peaks during European market trading hours, while the number of transfers reaches sustained highs during European daytime hours. This shows us that the adoption of USD-denominated stablecoins has reached more global penetration, especially in regions where USD assets are not seamlessly integrated into local financial systems.

in conclusion

The overall dominance of the U.S. (and to a lesser extent Europe) in the cryptocurrency market is perhaps somewhat surprising given the generally challenging regulatory environment in the U.S. over the past few years. However, we believe that the United States’ outsized influence in Crypto has broader significance given its strong capital base, market investment culture, and technology-savvy population.

The landmark approval of a spot Bitcoin ETF in the United States opens up an important new source of funding and draws further market attention to U.S. activity. We believe this highlights the importance of US regulations and policies in shaping the Crypto market. We also believe these findings highlight the relevance of U.S. investor sentiment as a key driver of market movements relative to other regions. As the approval of the U.S. Spot Bitcoin ETF shows, we believe that further U.S. regulatory clarity and more frictionless access to crypto may continue to increase U.S. dominance of the Crypto market.