Original title: Weekly: Feeling the Heat

Original author: David Han (Institutional Research Analyst)

Release date: April 12, 2024

Key takeaways

Markets continued to trade sideways amid higher-than-expected inflation data and fewer expectations for a rate cut by the Federal Reserve this year.

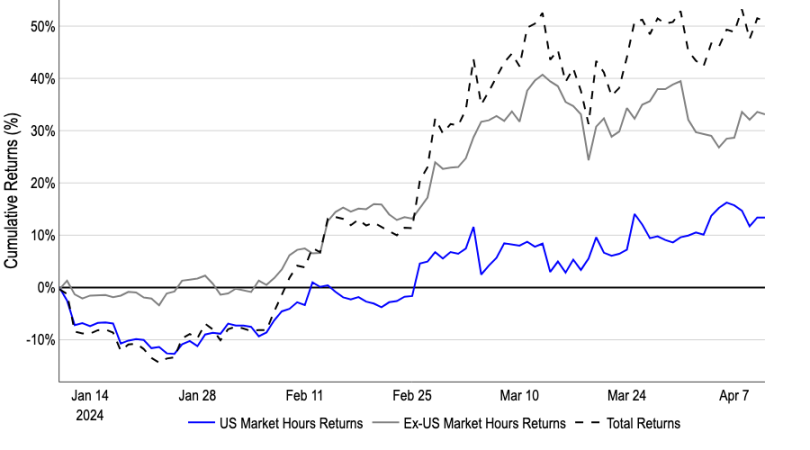

Economic conditions and outlook expectations outside the United States have played a significant role in Bitcoin’s overall price discovery, as most of the net buying of BTC since the approval of the U.S. spot ETF has actually occurred outside of U.S. trading days.

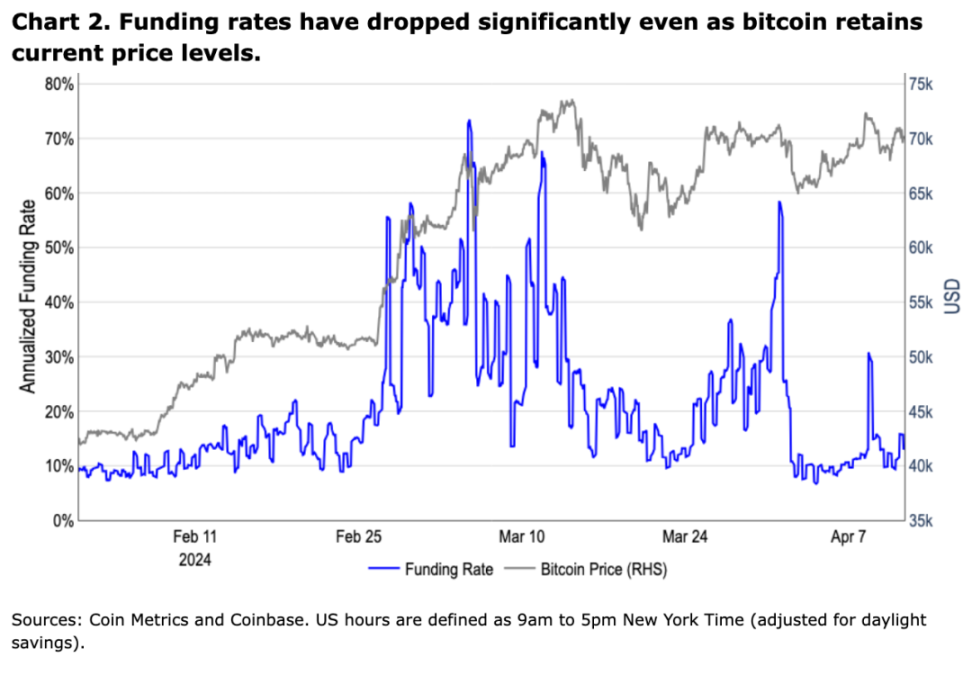

While Bitcoin’s returns have been roughly flat for a month, the perpetual funding rate has fallen from 66% annualized to about 12% annualized, indicating a decline in market excitement.

market

Markets continued to trade sideways amid higher-than-expected inflation data and fewer expectations for a rate cut by the Federal Reserve this year. Less than three months ago, Fed Funds Futures had priced in six rate cuts in 2024, with them expected to begin in March. Now, as we approach publication, the fed funds futures market is pricing in less than 2 rate cuts in 2024, expected to begin in September. While concerns about reflation and “longer-higher” interest rates are often seen as transitional catalysts for a risk-off environment, Bitcoin (and risk assets more broadly) have actually outperformed.

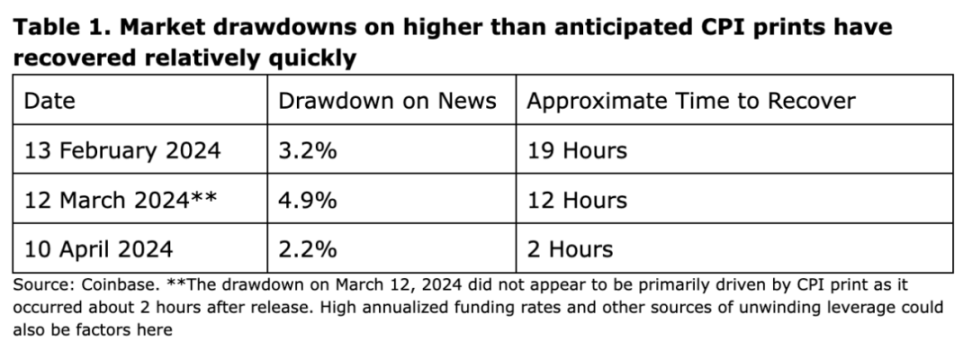

The market sentiment towards the rising CPI data is mainly reflected in the short-term market trend, and the market trend recovers relatively quickly (see Table 1). It can be seen from the historical CPI data that the first three Bitcoin declines all returned to the price before the CPI data was released within 24 hours. This is not to say that we think markets are ignoring inflation risks. In fact, we believe continued strength in gold prices, setting a new weekly high and breaking above last weeks highs, underscores the markets repricing of inflation risks (as well as other sources of geopolitical uncertainty).

We believe that part of the reason for Bitcoins continued strength is the marginal impact of global markets on the price of the asset class. That said, economic conditions and outlook expectations outside the United States play an important role in Bitcoin’s overall price discovery. Although Bitcoin’s trading volume and hourly price differential are largest during U.S. market hours, the majority of net buying actually occurs outside of U.S. trading days (see Figure 1). The potential approval of a Hong Kong spot Bitcoin ETF next week could exacerbate this trend and give BTC access to a wider pool of funds.

In addition, we also believe that the liquidation of bankruptcy proceedings mainly occurred on US exchanges, which also led to the negative price performance in the US session after the launch of spot ETFs. However, most of these technical hurdles have been cleared, creating a more favorable outlook for next week’s halving.

That said, regional differences in Bitcoin buying don’t fully explain the continued strength in risk assets. For example, although the Nasdaq 100 also declined following the release of CPI data on April 10 (although the recovery came against the backdrop of lower-than-expected PPI data), it remains close to all-time highs. We believe there are several confounding factors at play here, including expectations of AI deflation, weakness in the commercial real estate sector, and rising Treasury payments and threats to fiscal dominance, all of which are likely to be controversial against the backdrop of the 2024 general election. Taken together, we think there is reason to believe that quantitative tightening may soon begin to taper off, which would be a net positive for the market. Uncertainty over the continuation of tight monetary policy amid an executive change may also play a role in expectations of larger future interest rate cuts in 2025.

Beyond this, we believe an undervalued factor driving continued risk-on positioning is the lack of a clear value proposition that would allow capital to move toward alternatives such as longer-dated bonds. On October 19, 2023, when the U.S. 10-year Treasury bond yield reaches 5%, the number of implied interest rate cuts by the end of 2024 is 2.4. Although the number of implied rate cuts by the end of 2024 has now fallen to 1.7, the 10-year Treasury yield currently stands at 4.58% (when the US 10-year yield last reached this level on November 13, 2023, 2024 The number of implied interest rate cuts is 3). Given that $6.4 trillion has been deposited in US money market funds, there seems to be no clear relative value here.

All in all, we think this could strengthen support for Bitcoin around current price levels. In fact, while Bitcoin’s returns have been essentially flat since a month ago, perpetual contract funding rates have fallen from 66% annualized to about 12% annualized (see Figure 2). When the market maintains these price levels with lower funding rates, it indicates to us that there is more demand for more liquid spot and less excitement in the market. This may reduce the likelihood of liquidation amplifying the downward trend, and indeed we have seen dip buying become more aggressive. We further believe that given the positive narrative surrounding Bitcoin and broader cyclical positioning, Bitcoins normalization at these price levels has allowed the market to transform the decline from being seen as a moment of panic selling into a buying opportunity.

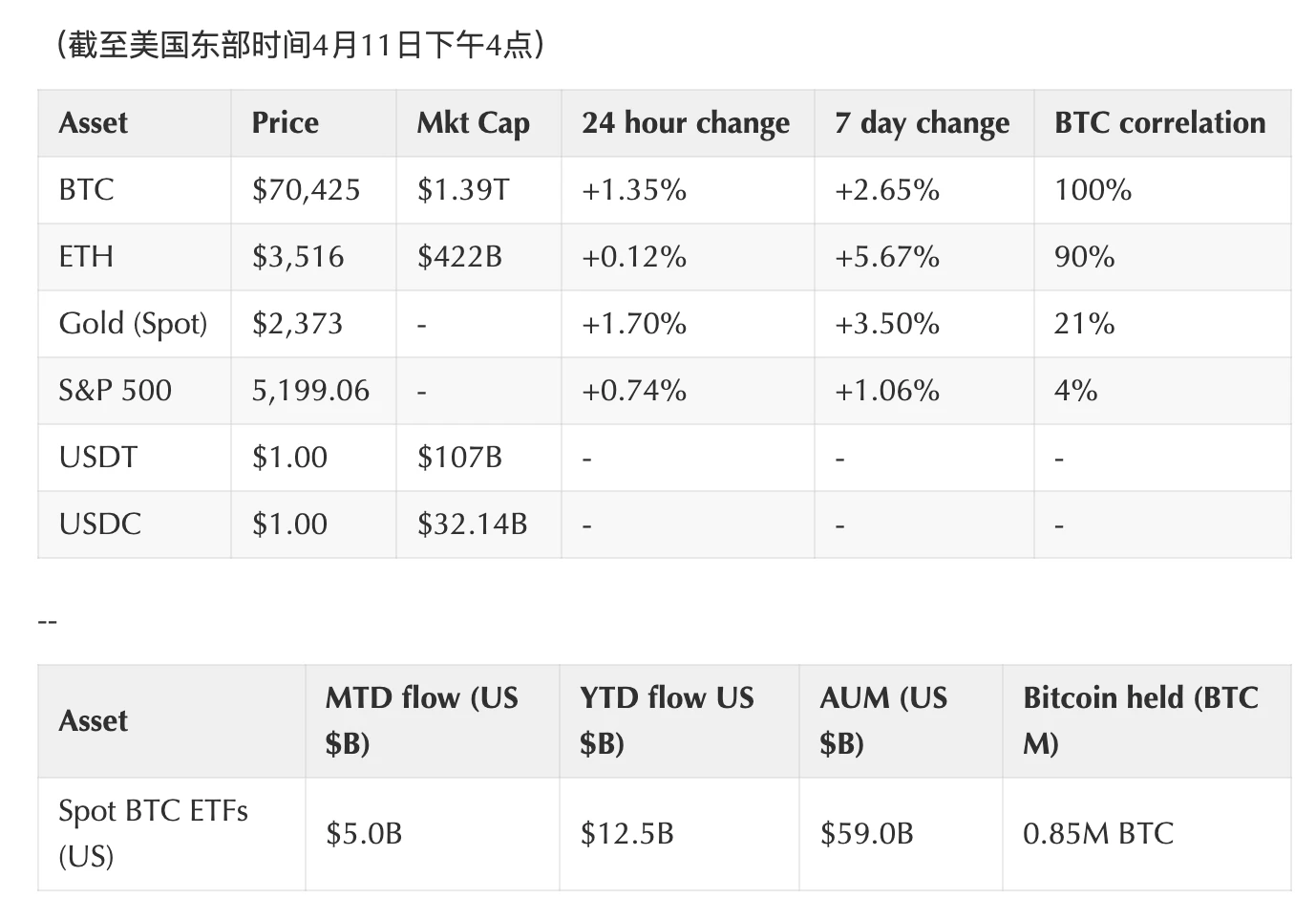

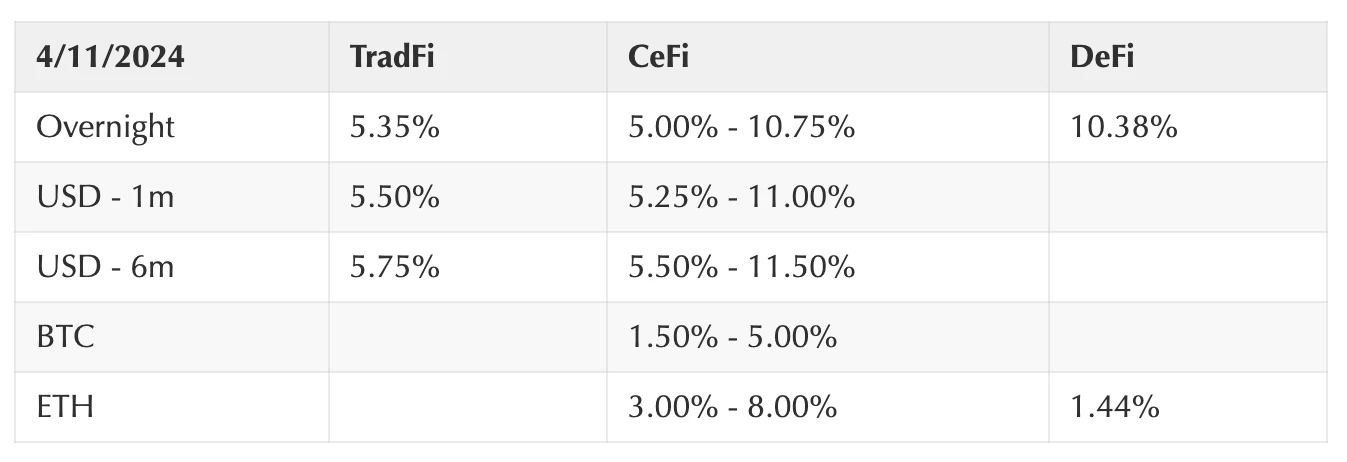

Crypto and traditional financial data

Source: Bloomberg Source: Bloomberg

Coinbase Exchange and CES Insights

Crypto markets have been range-bound for much of the week. Funding rates have come down from their highs and are now ~12% for mainstream coins and close to 20% for altcoins, suggesting that the excitement we saw last month has dissipated. Interestingly, cryptocurrencies traded well following the release of higher-than-expected CPI data. It seems that as long as there is no talk of raising interest rates, traders can safely go long. Price action also suggests that long positions are not being stretched as bargain hunting continues. BTC’s halving, set for later next week, doesn’t seem to be attracting the attention expected. It rarely comes up in trader conversations, which makes us wonder, what is it currently priced on? What are the value factors given to this pricing?

Coinbase platform trading volume (USD)

Coinbase platform trading volume (asset class)

Funding interest rate

Notable Crypto News

mechanism

JPMorgan thinks high rates are actually driving inflation (Bloomberg)

Cumulative trading volume of spot Bitcoin ETF exceeds US$200 billion (The Block)

Grayscale CEO says Bitcoin ETF outflows are reaching equilibrium (Coindesk)

Supervision

Hong Kong says it may approve spot Bitcoin ETF next week (Coindesk)

conventional

EigenLayer and EigenDA launched on Ethereum mainnet (Coindesk)

Google Cloud and Coinbase join EigenLayer (The Block) as operators

Monad Labs raises $225 million in round led by Paradigm (The Block)

Base surpasses Arbitrum and sets the highest number of active addresses this month (Cointelegraph)

Coinbase

Coinbase Registers Restricted Dealer in Canada (Coinbase Blog)

Coinbase drives UK cryptocurrency adoption with Apple Pay integration (Cointelegraph)

global vision

Europe

A European fintech hub is preparing to take a tough stance on crypto companies (Bloomberg)

Bank of England and FCA target autumn 2024 as earliest start date for first UK digital securities sandbox cohort (The Block)

Europe’s upcoming DeFi rules may ban non-decentralized protocols (CoinTelegraph)

The Swiss National Bank believes retail CBDC could destabilize the financial system (Cryptoslate)

Asia

Singapore expands crypto rules to cover custody and transfers (Bloomberg)

South Korea to Tighten Cryptocurrency Exchange Listings with Upcoming Guidelines (The Block)

Hong Kong HashKey Group launches Ethereum Layer-2 chain (The Block)

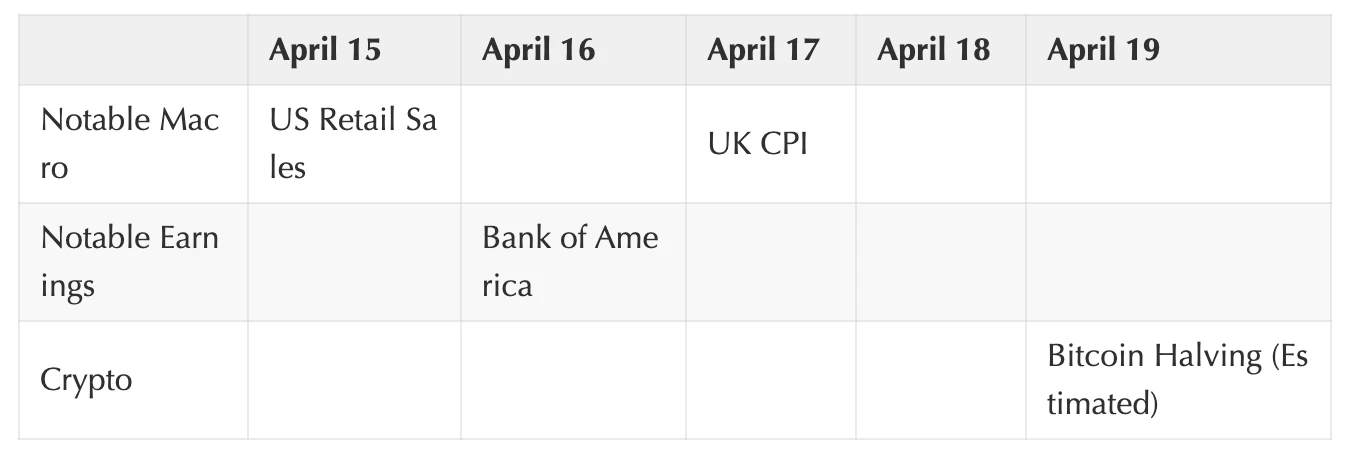

Big events for the week ahead