Original|Odaily Planet Daily ( @OdailyChina )

Author: Wenser ( @wenser 2010 )

At the end of The Evolution of Crypto Venture Capital Cycle (Part 1): Rebuilding a New World , after experiencing the IC0 wave led by Ethereum, the public chain investment boom, DeFi, GameFi and other crazes, crypto venture capital is about to enter the industry pain period in which NFT completes the last dance and ends quickly: on the one hand, there are frequent black swan events in the industry that no one expected, such as LUNAs thunder, 3ACs collapse, FTXs sudden collapse, and Genesiss bankruptcy; on the other hand, there is the joint encirclement and suppression and relentless pursuit of the crypto industry by government departments such as the US SEC and CFTC.

During the bear market, the reduction in liquidity meant that the industrys development could only rely on the alternating hype of sector rotation. The Bitcoin ecosystem and L2 ecosystem became one of the few narrative-level positives in this stage. Although subsequent market performance varied, to a certain extent, it also laid the foundation for the achievement of compliance milestone events such as the subsequent Bitcoin spot ETF and Ethereum spot ETF.

In 2024, the 15th year after the creation of the Bitcoin Genesis Block and the successful completion of the fourth halving of Bitcoin, as the cryptocurrency market, including Bitcoin, becomes increasingly connected with the U.S. stock market, the U.S. economy, and the world’s political and economic situation, the vision of “a peer-to-peer payment electronic currency system” envisioned by Satoshi Nakamoto is becoming increasingly unattainable. From this perspective, perhaps cryptocurrency is heading towards a lost future—the sovereign individualism, the concept of a cyber state, and the mission of decentralization are gradually being left behind, and what awaits us is the “centralized assimilation” that is already doomed and of unknown progress.

Following a brief review of the crypto venture capital cycle from 2016 to 2021 in the previous article of this series, Odaily Planet Daily will sort out and summarize the representative industry events and crypto venture capital trends in 2022-2024, that is, this cycle, for readers to communicate and refer to.

This article is quite long, so for your convenience, the TL, DR (too long, don’t read) version is as follows:

NFT became Ethereum’s last crypto glory, and the sale of Monkeyland in May 2022 became the “closing moment”;

UST, LUNA, 3AC, and FTX have all exploded, turning the crypto industry into a “serial bomb arsenal”;

After the darkest moment, Bitcoin ecology and Meme coins have become new hotspots in the crypto industry;

Bitcoin and Ethereum ETFs have been approved one after another, and industry compliance milestones may become industry tombstones;

Three ways to break the path dependence of venture capital: outlier monitoring, internal monster alliance, and external advisory mechanism;

A detailed list of active investment institutions in 2022-2024: exchange venture capital departments and gaming tracks are at the forefront;

The major trend of encryption: the public chain has grown from one to many, the industry structure has risen in the west and fallen in the east, but liquidity is eternal.

The Last Crypto Glory: The Non-Fungible Token (NFT) Boom

As time enters 2022, NFT is still an absolute hot track at that time - Chinese celebrities and IP companies are rushing in, and NFT projects related to Jay Chou, Shawn Yue, Edison Chen, and Wilber Pan have appeared one after another and were quickly eliminated by the market; Azuki has become another phenomenal NFT project after BAYC with its highly recognizable comic style; dozens of brands including Paco Rabanne, Dolce Gabanna, Etro, Tommy Hilfiger, Dundas, Cavalli, Nicholas Kirkwood and Elie Saab attended the First Metaverse Fashion Week held in Decentraland; Moonbirds was a great success due to the identity of the project founder Kevin Rose as a well-known investor and the previous Proofs series NFT, which once had a floor price of up to 100 ETH; the sports shoe NFT props related to the GameFi game STEPN, which focuses on the Move To Earn concept, have also become a hype target that breaks the circle.

As the largest NFT trading platform at the time, OpenSea also ushered in its peak moment - on January 5, 2022, Opensea completed a US$300 million Series C financing round with a valuation of US$13.3 billion, led by Paradigm and Coatue.

In contrast, BAYC is unparalleled - Yuga Labs (the parent company behind BAYC) announced in March that it had completed a new round of financing of US$450 million at a valuation of US$4 billion, led by a16z, and participated by Adidas Ventures, Animoca Brands, Samsung, Google Ventures, Tiger Global, FTX Ventures, Coinbase Ventures, Moonpay, etc. This round of financing was the largest financing in the NFT industry at that time. At that time, Yuga Labs had completed the airdrop and launch of ApeCoin tokens. A new round of FOMO was ready to go under the news of the OtherSide metaverse game project. Owning a BAYC NFT became the capital of showing off for countless crypto players, but when the floor price fell from 120 ETH at its peak to less than 30 ETH in the future, it also became an unforgettable painful memory for countless holders.

It is worth mentioning that veterans of the domestic Internet venture capital circle, such as Zhu Xiaohu of Jinshajiang and Cai Wensheng of Meituan, are also among them.

Zhu Xiaohu, managing partner of Jinshajiang Venture Capital, purchased BAYC#9279, which was regarded as a peak signal

On the other hand, STEPN, which has been iteratively updated based on the Axie Infinity model and advantages, has made rapid progress: the public beta version was launched in December 2021; in January 2022, a $5 million seed round of financing was completed, led by Sequoia Capital India and Folius Ventures; on April 6, Binance announced a strategic investment in StepN. Half a year after its establishment, its global monthly active users have exceeded 3 million. Driven by the crazy wealth-making effect, sports shoes NFT has become a topic of conversation for countless sports enthusiasts and the only goal of daily exercise. Folius Ventures has also made a lot of money, and has since determined the subsequent investment route of focusing on encrypted C-end applications and investing in projects with the mission of industry Mass Adoption.

In the first half of 2022, at the end of the bull market, countless people thought that Mass Adoption had begun to see the light of day driven by the development of many NFT and GameFi projects, but they didnt know that it was already the afterglow of the cycle. According to statistics , there were 1,660 investment and financing events in 2022, with a total amount of funds exceeding US$34.8 billion. Compared with the 1,351 investment and financing events of different rounds announced in 2021 and the total amount of US$30.5 billion disclosed, the number of projects that received financing increased by 22.87% year-on-year, and the total scale of funds increased by 14.08% year-on-year.

There were 426 investment and financing events in the DeFi track that year, with a total financing scale of US$1.6 billion. Among them, the US$165 million Series B financing completed by Uniswap Labs, led by Polychain Capital and participated by a16z and other institutions, was the only financing with a scale of over 100 million yuan.

There were 334 NFT and Metaverse investment and financing events with a total financing scale of US$4.4 billion. There were 10 events with a scale of US$100 million or more. The largest one was the US$450 million seed round of financing completed by Yuga Labs mentioned above, led by a16z.

There were 334 investment and financing events in the GameFi track, with a total financing scale of US$4.4 billion, and 7 events with a scale of US$100 million or more; game developer and venture capital company Animoca Brands became the big winner in the track, completing three different rounds of financing, including US$358 million, US$75 million, and US$110 million, with a total financing amount of more than US$540 million;

There were 208 investment and financing events in the CeFi track, with a total financing scale of US$9.6 billion. There were 27 events with a scale of US$100 million or more, accounting for 13%. Large-scale financing accounted for the highest proportion among all tracks. It is worth mentioning that FTX US announced in January of that year that it had completed a US$400 million Series A financing round with participation from SoftBank, Temasek, Paradigm, Multicoin Capital, Lightspeed Venture Partners, etc., with a valuation of US$8 billion;

There were 426 investment and financing events in the Infra track, with a total financing scale of US$12.5 billion. There were 35 events with a scale of US$100 million or more. The largest was the US$1 billion financing completed by Luna Foundation Guard (LFG) through the over-the-counter sales of LUNA, led by Jump Crypto and Three Arrows Capital (3AC).

Starting from May 2022, words such as LUNA, UST, 3AC, and FTX will become an indelible shadow over the entire crypto venture capital industry.

The Darkest Year: A series of thunderstorms

On May 1, 2022, the Otherside NFT minting event, a new metaverse project launched by BAYCs parent company Yuga Labs, successfully concluded after burning $170 million worth of ETH Gas fees. Another industry storm is brewing - the cryptocurrency industry will usher in its own Lehman moment in just a few days, and this is only the first of the year.

From May 7 to May 13, the leading algorithmic stablecoin UST experienced two decouplings. The left foot on the right foot model that Terra Labs and South Korean cryptocurrency leader Do Kwon had previously painstakingly maintained eventually fell into a death spiral. Both LUNA and UST collapsed, and the coin price fell more than 100 times in a short period of time.

On June 13, Celsius, a crypto lending platform, announced the suspension of withdrawals. It was later discovered that its use of on-chain leverage and derivatives stETH led to insolvency and a vicious cycle. On July 14, Celsius filed for bankruptcy protection.

On June 14, there were rumors that Three Arrows Capital (3AC) was insolvent and in a liquidity crisis. On June 15, 3AC co-founder Zhu Su responded that we are communicating with relevant parties and working hard to solve the problem. But in the end, affected by the Luna crash, because 3AC had previously heavily invested in GBTC and stETH, on July 2, it had no choice but to file for bankruptcy protection. According to subsequent court documents , it owed 27 companies a total of US$3.5 billion.

On July 6, 3AC creditor Voyager Digital announced that it had filed for bankruptcy protection, mainly because 3AC suffered huge losses due to its default on a $670 million loan.

On August 8, the crypto lending platform Hodlnaut announced that it would cease trading and seek creditor protection in Singapore on August 16.

On November 2, CoinDesk, a cryptocurrency industry media under DCG, revealed that there were great risks in the balance sheet of crypto market maker Alameda, which caused market panic. At that time, FTX, the worlds second largest cryptocurrency exchange, fell into a liquidity crisis. On November 8, FTX announced that it would stop withdrawals. On the evening of November 9, Binance, which originally planned to acquire FTX, announced that it would abandon the transaction, and FTX collapsed completely. On November 11, FTX filed for bankruptcy.

On November 10, BlockFi suspended withdrawals due to the crisis of its creditor FTX and filed for bankruptcy protection on November 28. Earlier on June 17, cryptocurrency analyst Otteroooo said that BlockFi is likely to fall into a liquidity crisis due to the US SEC fine, Luna collapse, and loans from Three Arrows Capital.

On November 14, due to the liquidity crunch caused by the collapse of FTX, the crypto broker Genesis sought a $1 billion emergency loan and suspended withdrawals on November 16. On November 21, Genesis said it had no immediate plans to file for bankruptcy, and then on December 8 said it would take several weeks to resume withdrawals. Finally, in January 2023, Genesis officially filed for bankruptcy.

If the Russia-Ukraine war in February of that year set off a regional hot war around the world, then these successive institutional bankruptcies are like nuclear bombs that bring destruction and pain to the cryptocurrency and venture capital industries.

Many people no longer have confidence in cryptocurrencies due to the collapse of FTX. The price of FTT tokens also plummeted hundreds of times in just a few days. Just like LUNA before, it has completely become an alternative bankrupt concept meme coin. FTX, which was valued at $32 billion only three years after its establishment, was reduced to zero overnight and swept into the dust of history. The star exchange that was once favored by a number of well-known investment institutions such as Paradigm, SoftBank Group, Sequoia Capital, and Temasek has since become a thing of the past.

This shows the dangers of the venture capital boom in the cryptocurrency industry.

Combined with the endless security incidents at that time, the crypto industry was in a state of distress. According to incomplete statistics , there were approximately 427 security incidents related to the cryptocurrency industry in 2022, causing direct economic losses of more than US$3.5 billion and a total amount of more than US$75.3 billion .

Overview of major security events in 2022

According to Coingecko data , in November 2022, affected by events such as the FTX collapse, the price of Bitcoin fell below US$16,000, to around US$15,800; the price of Ethereum fell below US$1,100, to around US$1,090; the market value of cryptocurrencies fell below US$1 trillion, to around US$820 billion.

Cryptocurrency market cap lows

Despite this, according to relevant data, the investment and financing market in the first quarter of 2022 still topped the single-quarter investment and financing record since the birth of Bitcoin with a total financing amount of over US$10 billion, and set an industry record of 7 consecutive months of positive growth. During this period, the capital increase was as high as more than US$26 billion, which can be called an unprecedented golden age of crypto venture capital.

In addition , public chain projects such as Near, Polygon, Aptos, Sui, and zkSync (now renamed ZKSync) have successively received more than 100 million US dollars in financing. The news that Dapper Labs, the developer behind the well-known NFT project NBA Top Shot and Flow public chain, received 305 million US dollars in financing also continued to stimulate the development of L1 and L2 network-related projects, laying the foundation for subsequent large-scale airdrops and the L2 craze.

Ethereum, once the “new king of cryptocurrencies”, also successfully produced its first PoS block on September 15 of that year, and the consensus mechanism officially switched from PoW to PoS, laying the groundwork for what was to come.

The Return of the Crypto King: Bitcoin Ecosystem and Meme Coin Ecosystem

After experiencing the darkest year of 2022 with ice and fire, crypto venture capital re-entered the recovery period after the pain in 2023.

The most obvious manifestation of this is that the scale of industry financing has dropped significantly: according to RootData data , the total financing amount of the crypto industry in 2023 was US$9.043 billion, which is much lower than the data in previous years. According to a panoramic analysis report on crypto investment and financing in November 2023 , 1,957 investors conducted approximately 641 rounds of financing for 617 projects that year, with a cumulative financing amount of only US$5.58 billion. The fact that the most popular round of financing type was the seed round once again proved that crypto venture capital was not very active at that time, and even from a data perspective, it can be said to be extremely bleak. According to statistics from TheBlock , the investment scale of venture capital institutions in 2023 was only US$10.7 billion, a decrease of 68% compared to 2022 (US$33.3 billion).

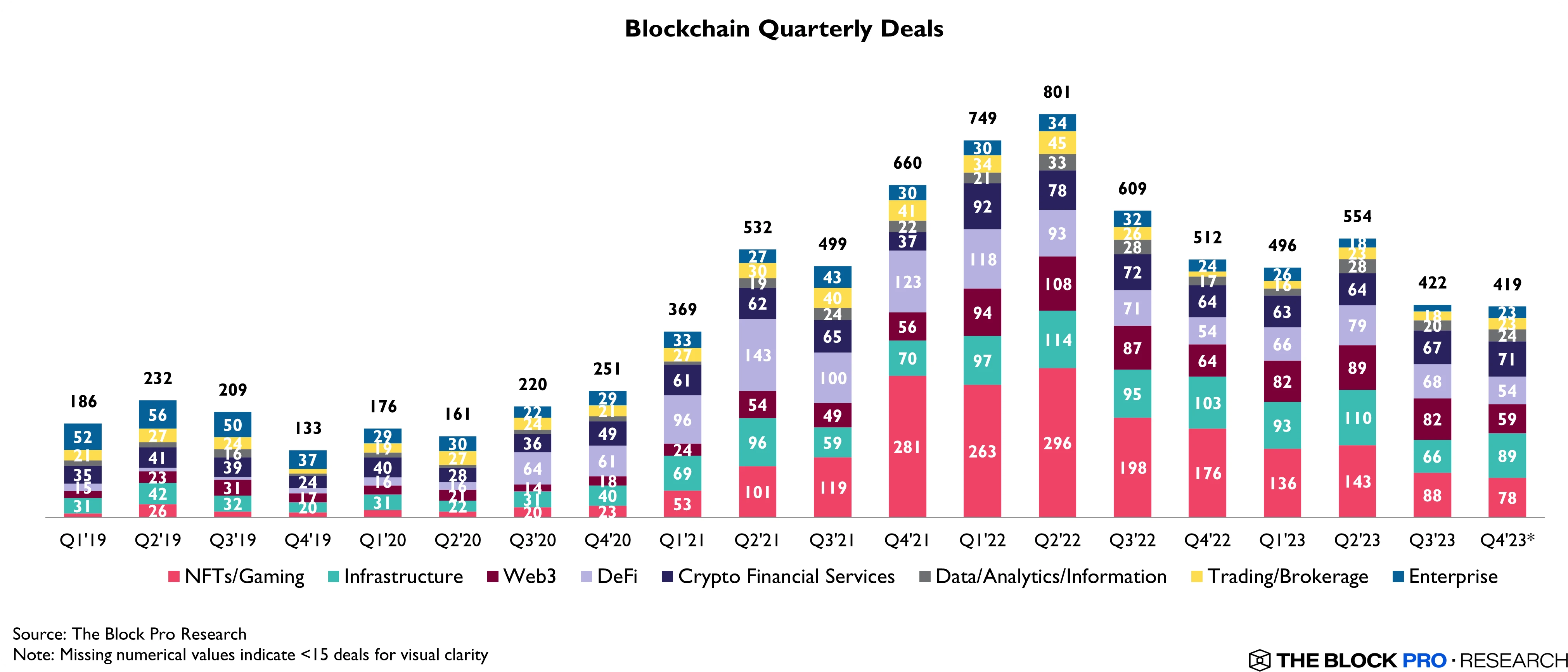

Statistics on the number of financings in each sub-sector in each quarter from 2019 to 2023

The main factor affecting this market performance may be attributed to the fact that the cryptocurrency industry has ushered in a new flower moment for old trees - the Bitcoin ecosystem and Meme coin ecosystem that emphasizes fair launch have regained vitality - the emergence of the Ordinals protocol and BRC20 , as well as the emergence of the famous Internet Meme PEPE Meme coin project and the Meme coin craze have provided some impetus for the return of Bitcoin and Ethereum prices. After all, Gas fees are an unavoidable part of on-chain operations. With a relatively increased usage, prices will also rise to varying degrees. Although this has limited benefits to the venture capital field, it still drives the financing and development of related projects.

List of large financings in Q1 2023

Later, the inscription fever gradually expanded to different blockchain network ecosystems, and even reached the stage of inscriptions must be mentioned. Many old public chains including AAVX and Injective attracted extremely high market attention in a short period of time due to the launch of the first inscription project. Although the project may not be reliable, I cant help but participate was the most real thought of countless market users at that time. In this wave of inscription tide, there are both a wave of Rug projects and many serious projects including Merlin.

If we count these projects, the leader among them is none other than Babylon. On December 7, 2023, Babylon completed a $18 million financing led by Polychain Capital and Hack VC, with participation from Framework Ventures, Polygon Ventures, OKX Ventures, and IOSG Ventures. In February 2024, Binance Labs announced its investment in Babylon; in May 2024, Babylon completed a new round of financing of up to $70 million led by Paradigm. Another Bitcoin ecosystem project invested by Paradigm is the old NFT trading platform Magic Eden. After it integrated the Bitcoin wallet entrance, it also became one of the heavyweight players in the Bitcoin ecosystem NFT sector, with trading volume catching up with the OKX Bitcoin NFT trading market.

In addition, the implementation of L1, L2 and even L3 concept-related protocols and applications has also created conditions for high-value financing of cross-chain bridges.

Ethereum scaling project Scroll completed a new round of financing of US$50 million in March. Polychain Capital, Sequoia China, Bain Capital Crypto, Moore Capital Management, Variant Fund, Newman Capital, IOSG Ventures, Qiming Venture Partners, and OKX Ventures participated in the investment. Its total financing amount reached US$83 million. According to sources, its valuation was as high as US$1.8 billion.

Blast, an L2 network based on Optimistic Rollup, completed a US$20 million financing in November, with participation from Paradigm, Standard Crypto, eGirl Capital, Mechanism Capital co-founder Andrew Kang, Lido strategic advisor Hasu, and The Block CEO Larry Cermak.

The cross-chain protocol Wormhole completed a $225 million financing in November 2023, with a valuation of $2.5 billion, becoming the highest-funded project of the year. Another star player in this track is LayerZero , which competes with the four major L2 king-level projects including Starknet and ZKSync. At that time, it completed a $135 million A1 round of financing (valued at $1 billion) and a $120 million B round of financing (valued at $3 billion, a16z Crypto, Sequoia Capital, OKX Ventures, Circle Ventures, Samsung Next, OpenSea and Christies, etc.) in March and April, respectively. Therefore, it is highly expected by the market, and it is speculated that it may surpass Wormhole and take up the banner of the cross-chain track. But everyone knows how it ended. After nearly two months of vigorous “anti-witch movement”, the ZRO airdrop ended with a “pitiful number” of tokens as small as single digits or even less than one, which attracted a lot of criticism.

It is worth mentioning that since the launch of ChatGPT in November 2022, a series of AI applications have sprung up like mushrooms after a rain, followed by a large number of crypto AI projects that have emerged and become an important part of the crypto venture capital industry in 2024. Representative projects such as the Web3 artificial intelligence platform MyShell completed a US$11 million Pre-A round of financing in April 2024, led by Dragonfly, with participation from Delphi Ventures, Bankless Ventures, Maven 11 Capital, Nascent, Nomad Capital and OKX Ventures. Angel investors also include former Coinbase CTO Balaji Srinivasan, NEAR Protocol co-founder Illia Polosukhin, former Paradigm investment partner Casey Caruso and former Parafi partner Santiago Santos. The UBI project Worldcoin has also become an alternative AI concept coin due to the participation of OpenAI founder Sam Altman. The development company behind it, Tools for Humanity, completed a US$115 million Series C financing in May 2023, led by Blockchain Capital, with participation from a16z, Bain Capital Crypto and Distributed Global.

Finally, many VC coins including Starknet and ZKSync are about to enter the final step of completing the historical mission - TGE and corresponding token airdrops.

At the end of 2023, representatives of a number of investment institutions made many forecasts for 2024. At that time, most people had high expectations and optimistic attitudes towards the investment and financing track in 2024.

In November, the Bank of America Global Monthly Fund Manager Survey showed that investors remained cautious about the macroeconomic outlook but expected a soft landing in 2024, along with lower interest rates and a weaker dollar;

In December, DWF Labs announced the launch of its 2024 angel investment plan, which will focus on GameFi, SocialFi, Meme, RWA, derivatives and innovative DeFi solutions; a spokesperson for Coinbase Ventures said : “Our view is that the confluence of increasing regulatory clarity (primarily outside the US), maturity of protocol infrastructure, institutional participation, and innovation in how users interact with on-chain products sets the stage for a bright outlook in 2024. Our commitment is global and unwavering, and we expect investment activity to grow in 2024.”

Animoca Brands co-founder Yat Siu said he is very optimistic about the future and expects the cryptocurrency financing environment to be much healthier by 2024. As the crypto market rebounds, the momentum has changed, which may represent the beginning of a new bull cycle in the crypto market, and games and artificial intelligence with Web3 components may attract more investment in 2024.

Early-stage investment firm Shima Capital is cautiously optimistic about crypto industry financing in 2024, with its gaming director Alex Wettermann saying that infrastructure, gaming and tokenization verticals are expected to receive more investment in the coming year.

Polygon Ventures CEO Abhishek Saxena said : Web3 financing may have bottomed out and the new year will attract more investment. A positive indicator is that even in the bear market, we have seen resilient developer activity, which highlights that infrastructure construction is still continuing. In addition, he expects investment and financing in consumer-oriented use cases (including social, financial services and entertainment) to pick up, and new leaders may emerge in these areas.

Although the speeches at that time were still full of the same old clichés of path dependence, the subsequent success of Meme coins, AI concept coins, Solana DePIN, Base ecosystem, and many other social products including Farcaster, which is valued at US$1 billion, have indeed proved the foresight of this group of industry veterans.

But it is clear that the main theme of the market has quietly changed.

New progress in industry compliance: milestone or tombstone?

On January 10, local time, the U.S. Securities and Exchange Commission (SEC) announced that it had officially approved the first Bitcoin spot exchange-traded fund (ETF), and corresponding trading began the next day. After years of grievances and disputes, the cryptocurrency field has finally taken this historic step. For details, see the article Historic Moment: Bitcoin Spot ETF Finally Approved, Will the Opening of Cryptocurrency Be a New Starting Point for Long Bull Markets? written by Odaily Planet Daily author jk.

Just the night before, a ridiculous incident occurred. The official account of the SEC’s X platform was hacked and a tweet saying “Bitcoin spot ETF has been approved” was posted. Later, SEC Chairman Gary Gensler clarified that the SEC’s official account was stolen and “unauthorized messages” were posted. The SEC did not actually approve the spot Bitcoin ETF, which caused the price of Bitcoin to fluctuate by more than $3,000 in half an hour, and the long and short positions in the contract market exploded.

Perhaps due to this influence, the good news was digested in advance, and the price of Bitcoin did not react strongly after the ETF was passed, and even fell at one point; on the contrary, Ethereum rose sharply as the market focus shifted to Ethereum spot ETF expectations.

With the achievement of this compliance milestone, the cryptocurrency market, including Bitcoin, has become increasingly connected with the U.S. stock market, the U.S. economy and the world economic system. This also indicates to a certain extent that the cryptocurrency industry can no longer remain immune as it did in the past and become the preferred target of safe-haven funds.

In February, the Starknet Foundation announced that the STRK airdrop has been opened for application, and the deadline is June 20. So far, Starknet, one of the Four Heavenly Kings of L2 that once raised $261 million and was valued at $8 billion, has come to an end in stages. Market users are beginning to look forward to the performances of projects such as ZKSync, LayerZero, and Blast - no one would have expected that this would be the last glory of the VC coin.

ZKSync official tweet may also be a hint of the subsequent market trend

In March, after the initial dumping and high-volume transactions, the market sentiment of Bitcoin spot ETF gradually recovered and successfully hit a record high of around US$73,000 on the 14th. A large amount of funds preferred to invest in Bitcoin spot ETF and Bitcoin, and the new liquidity was increasingly tightened. At the same time, a number of mainstream exchanges including Binance, OKX, and Coinbase also started a new round of listing tides under the impetus of the crazy market conditions. The Solana Meme craze led by BOME, which achieved the achievement of listing on Binance in three days, also gradually swept across the country. Solana Ecosystem One-click Coin Issuance Platform pump.fun also went through the initial trough and gradually got on the right track. In the following months, it gradually became the biggest protagonist of the Meme Coin Cycle, and the protocol revenue quickly exceeded US$90 million after 5 months.

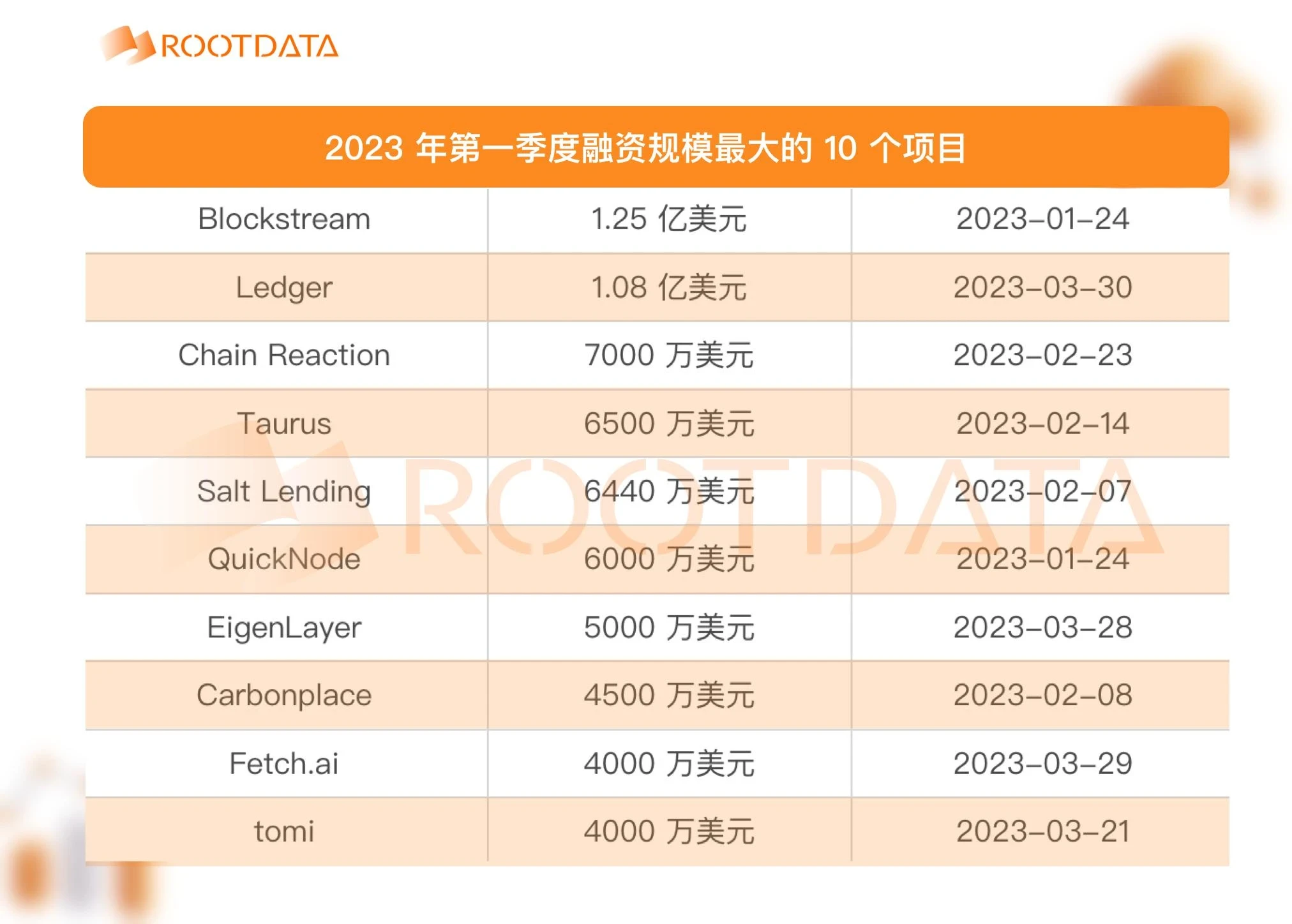

According to Rootdata data , the Web3 primary market generated a total of 459 financing events in the first quarter of 2024, a year-on-year increase of 28.7%, and the total financing amount reached US$2.545 billion, a year-on-year increase of 4.7%. Among them, infrastructure, DeFi and CeFi are the three tracks with the largest investment and financing amounts; the number of early financing projects increased by 10.5% compared with 2023, and there are still many unverified technologies and solutions in the market. It is worth mentioning that CeFi and DAO tracks have hardly received the favor of the top 10 active investment institutions in Q1, perhaps because the market has been saturated at a certain stage, or due to compliance issues, commercialization difficulties and other reasons.

EigenLayer ($100 million in Series B), HashKey Group ($100 million in Series A), Optimism ($89 million in OTC), Zama ($73 million in Series A), and Figure Markets ($60 million in Series A) are among the top five projects in terms of financing in Q1. Thanks to the popularity of the re-staking track, DeFi has become one of the popular choices at this time, but in the following months, many people will regret joining the ranks of the staking army.

In April, market speculation began to shift to the Bitcoin halving event. Countless Bitcoin ecosystem participants, including retail investors and investment institutions, placed high hopes on this, expecting Bitcoin prices to soar after the fourth block reward halving at block height 840,000.

But there were some different views in the market at that time. For example, Binance founder CZ wrote that Bitcoin halving is different from stock splits. Some people asked such questions, which shows that we are still in the early stages. Based on the experience of the previous three halving events, he judged that the price will not double overnight after the halving; within a year after the halving, the price of Bitcoin will hit a record high many times. Coinbase analyst David Han believes that cryptocurrency may be largely affected by exogenous factors, including increased geopolitical tensions, rising long-term interest rates, reflation, and rising national debt. Looking at it today, a few months later, after experiencing the Middle East situation such as the Iran-Israel conflict and the Hamas movement, as well as the impact of the US stock market, Nikkei, and South Korean stock markets on Bitcoin prices, these views have been fulfilled.

In addition, according to BlocksBridge Consultings analysis of the financial returns of 12 listed Bitcoin mining companies, 10 of them raised a total of $2 billion through equity financing activities, and profitability is expected to decline after the halving. These companies raised $1.25 billion in Q4 2023. Marathon Digital, CleanSpark and Riot Platforms were the companies with the most financing in the first quarter of this year, accounting for 73%. As of the end of March, Marathon, CleanSpark and Riot held a total of $1.33 billion in cash and more than 32,200 bitcoins.

After entering the second quarter, the social track became a star track, Bitcoin ETF became an important part of the market, and the number of investments by investment institutions also increased significantly.

According to the RootData: 2024 Q2 Web3 Industry Investment Research Report , the total financing in the second quarter of 2024 reached 2.75 billion US dollars, a year-on-year increase of 38.9%. The total financing of the social track increased by 650% month-on-month, mainly due to Farcasters completion of a $150 million financing at a valuation of $1 billion, led by Paradigm, and participated by a16z crypto, Haun, USV, Variant, Standard Crypto, etc.

The total net inflow of Bitcoin spot ETFs reached US$2.394 billion, a decrease of 80% month-on-month, and the total amount of assets under management decreased by 12.4% month-on-month.

Financing data shows that the total amount of financing for mid- and late-stage projects increased by 20.7% month-on-month. In the current increasingly stable market environment, most investment institutions may prefer to make strategic large investments in advance. Animoca Brands became the most active institution in the quarter with 36 investments, and the top ten institutions investment in the GameFi track increased by 71% month-on-month.

The star projects in the second quarter also include two L1 public chains: Monad announced the completion of US$225 million in financing, led by Paradigm, with participation from Electric Capital, SevenX Ventures, IOSG Ventures and Greenoaks. With the main concept of challenging public chains such as Solana and Sui, Monads financing has become the largest cryptocurrency financing in 2024; Berachains main concept is community-driven L1 public chain. In the B round of financing in April, the amount of financing increased to US$100 million, with a valuation of up to US$1.5 billion. It was jointly led by Brevan Howard Digitals Abu Dhabi branch and Framework Ventures, and participated by institutions such as Polychain Capital, Hack VC and Tribe Capital.

As for the VC coin that many people are concerned about, it has once again become the focus of market discussion with the title of high FDV low circulation project. Bankless DAO founder David Hoffman , Dragonfly managing partner Haseeb Qureshi , cryptocurrency trader and KOL Jordan Fish (nicknamed Cobie on the X platform) have expressed their views on this. Hack VC partner Ro Patel also discussed the possible solutions to this problem from a VC perspective in July, believing that the lock-up mechanism based on liquidity and milestones may alleviate this problem, but the market, which is deeply trapped in the FOMO and Meme craze, is obviously not satisfied with this answer, so it is difficult for the project party to strictly implement this strategy.

From past experience, when a project is about to launch TGE, the search volume on various platforms will reach a peak, and then it will drop off a cliff. For many people, including project owners, peaking at the time of launching a token is not a joke, but a cruel and helpless reality.

The second quarter was also the peak period for Binance listings, and the competition among various projects waiting to be listed entered a white-hot stage: the average valuation of Launchpool projects reached US$217 million, but the investment rate of institutions was less than 2%. At that time, the market expected that more than 30 large projects would conduct TGE in the third quarter, but in the face of the current wide-ranging monkey market, many projects that were eager to try and wait for listing have stopped.

In addition, the approval of the Ethereum spot ETF in July could not conceal the downward trend of Ethereum prices against the backdrop of a declining global economic situation and turbulent political situation in some regions. It was only recently that it achieved positive weekly capital flow growth for the first time .

Finally, from the perspective of fundraising by investment institutions, public data since 2015 shows that there have been 177 fund-raising events in the cryptocurrency field, with a total fundraising amount of more than US$39.6 billion. The bull market from 2021 to 2022 benefited from this, and high-valuation projects such as Starknet and ZKSync were also at that time.

In the first half of 2024, cryptocurrency-related Web3 funds raised a total of $1.38 billion. Paradigm announced in June that it had raised $850 million, making it the largest fund-raising event in the second quarter and even in the first half of this year. Unfortunately, more and more investors have realized that there are fewer and fewer projects to invest in, more and more homogeneous projects, and new narratives and new technologies are becoming increasingly scarce resources.

Cryptocurrency investors, including retail investors in the market, are like mice trapped in a cage, and can only run quickly along the predetermined wheel. What awaits them in the future is not sure whether it will be the next milestone or a tombstone with the epitaph The industry ideal is dead.

Revelation of the venture capital cycle: Path dependence is the only obstacle

Looking back at several representative success stories in the past, Xiao Feng and Wanxiang Lab, the “key man of Ethereum”, Multicoin Capital, an early investor in Solana that believes “success or failure is due to the same source of profit and loss”, and Folius Ventures, an Asia-Pacific-focused investment institution that received excess returns from investing in STEPN and believes that “consumer applications will lead Mass Adoption”, we can see that one very obvious feature is path dependence.

As we have mentioned in many previous articles: What makes you successful can also hinder your progress.

When an investment institution obtains excess returns in a track field or a certain project, due to the limitations of perspective and the dividends of the times, it often regards this return as a reward for its investment strategy, vision for people, track model, personal connections and other advantages, and then falls into the copying mentality and expects to invest in the next XXX.

Public chains, DeFi, GameFi, NFT, SocialFi, Infra, DApps, Bridge, DID, and other sub-tracks are all no exception. The reason for this, in addition to the requirements for the stability of business models and profit models, to a certain extent, also reflects the mental inertia and curse of knowledge of human beings - when you know that one road can successfully reach the other side, it is difficult to try to find a second road, and to return to the ignorant state of not knowing this road and imagine how those who have never reached the other side will find new paths.

In traditional venture capital fields such as Web2, this phenomenon is called by many investors as a manifestation of the endowment effect, and some people also associate it with the genetic determinism of major Internet companies - just like the sayings Tencent is not good at e-commerce, Ali cant do social networking, and Baidu is not good at operations.

In order to break through the blockade of path dependence, I personally think that venture capital institutions can try to make changes from the following perspectives:

Establish an outlier monitoring mechanism. Just as the sudden rise of the TON ecosystem in this cycle is due to the fact that game projects with Meme coin attributes such as NotCoin have developed a Tap2Earn model based on the previous GameFi field and combined with the Telegram ecosystem. This can be seen from the previous data of the NotCoin project, and this often represents new opportunities;

Establish an internal monster alliance. Just like the monsters in Journey to the West who take responsibility for their own lives, each investment institution may also consider setting up a small number of monster departments that are responsible for their own profits and losses, using a small amount of affordable funds as a lever to leverage a wider range of innovative projects and technologies, and establish a corresponding personnel promotion and elimination system and project incentive evaluation system, so as to increase the probability of internal innovation and avoid going down a dead end;

Introduce an external advisory mechanism. As the cryptocurrency market has developed to this point, the market segments have become increasingly complex, and investors in investment institutions are not all-knowing and omnipotent. Micro-innovation often requires cross-border thinking and the introduction of external perspectives. Investment strategies, track research, project analysis and other matters can also obtain new information gaps by exchanging perspectives with external consultants to obtain greater vision dividends.

In short, the first principle to break path dependence is to recognize the limitations of path dependence and to find new opportunities and possibilities while consolidating existing advantages.

The “rainmakers” in the crypto venture capital cycle

In the business world, those who can bring new business opportunities and win new customers to a company are called RainMakers. They often bring new economic breakthroughs to a company through innovative business activities, just like being able to bring rainy seasons unexpectedly with the help of magic. Investment institutions that bring new funds and attention to the cryptocurrency field can also be regarded as rainmakers who create miracles.

Looking back at this cycle, Odaily Planet Daily will briefly sort out the list of major active investment institutions, as shown below:

In 2022, based on the institutional activity evaluated by the number of investments, the top ten investment institutions are Coinbase Ventures, Animoca Brands, Shima Capital, GSR, Spartan Group, Dragonfly, Solana Ventures, Alameda Research, a16z, and Jump Crypto.

Source: Rootdata

2023 can be regarded as a low point for venture capital. Despite this, veteran capitals including a16z Crypto, Paradigm, Sequoia Capital, Polychain Capital, Shima Capital and exchange venture capital departments such as Coinbase Ventures are still making frequent investments; the already grown Solana Ventures, Circle Ventures, and Polygon Ventures are also not to be outdone and have embarked on their own venture capital journey; market makers such as DWF Labs have also become an important part of cryptocurrency venture capital.

In terms of the number of lead investments , a16z, Polychain, Bitkraft Ventures, Dragonfly, 1kx, Hack VC, Shima Capital, Jump Crypto, and ABCDE Capital are among the top 10 investment institutions, having led investments at least 8 times.

In addition, major institutions actively participating in Bitcoin ecosystem investment include the venture capital departments of mainstream exchanges such as Binance, OKX, and KuCoin, as well as ABCDE, Waterdrop Capital, and LK Ventures.

2023 Q1 Crypto Investment and Financing Report

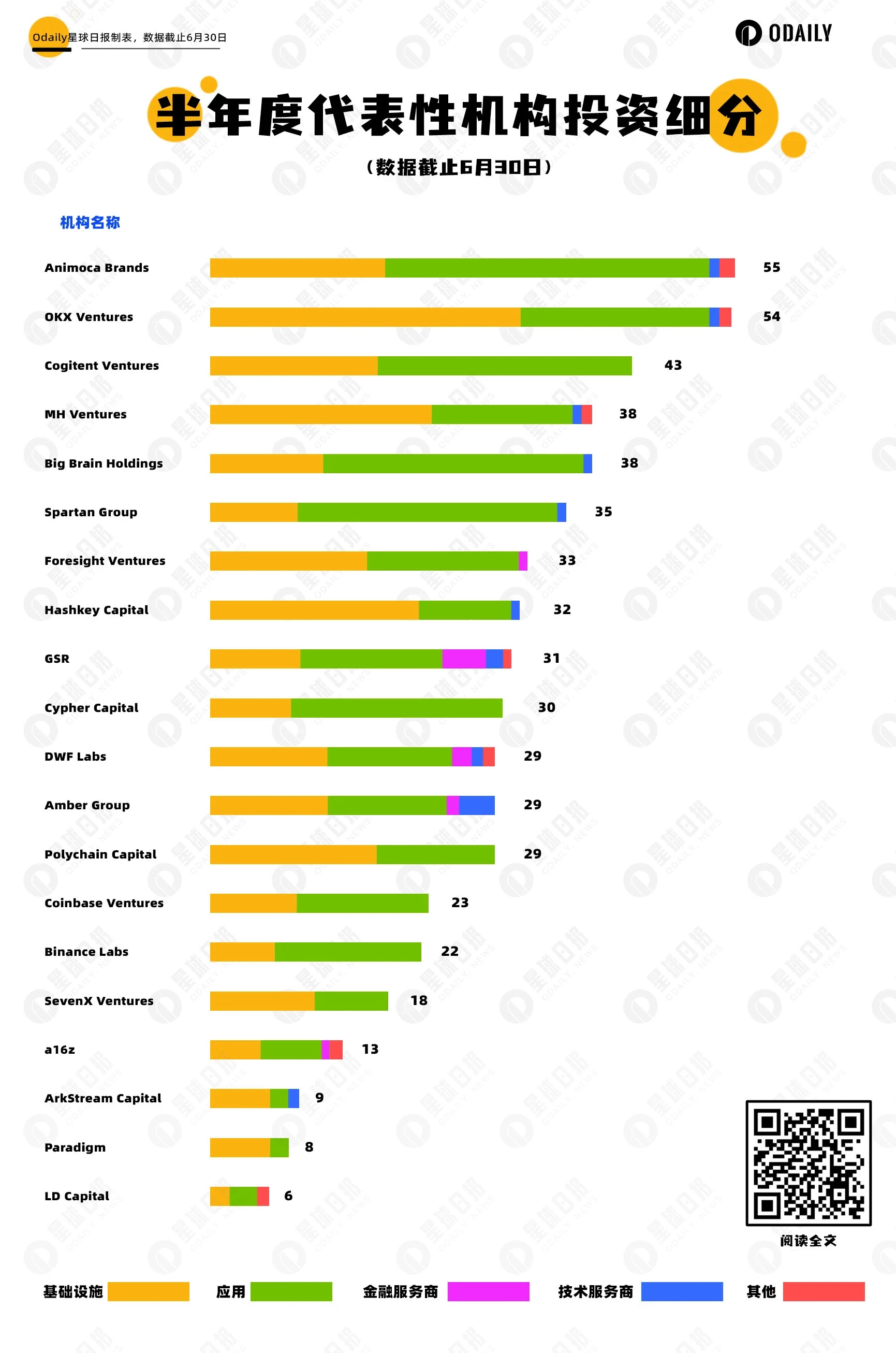

In the first half of 2024, representative investment institutions include Animoca Brands, OKX Ventures, Cogitent Ventures, MH Ventures, Big Brain Holdings, Spartan Group, Foresight Ventures, Hashkey Capital, GSR, Cypher Capital and other organizations. Games, social networking and infrastructure construction have become popular investment targets for institutions.

List of 20 active investment institutions in the first half of 2024

Cryptocurrency Trends: From One to Many, From East to West

Finally, let’s briefly talk about the “evolutionary” trend in past venture capital cycles. From the perspective of the public chain landscape and the evolution of discourse power, we can summarize it in eight words: from one to many, from east to west.

Public chain structure: from one to many

After Ethereum, built on the Solidity language, became the benchmark ecosystem of the public chain in the cryptocurrency industry, the L2 network built on ZK Rollup and Optimism Rollup has expanded with the expansion of Ethereum. According to statistics from the L2 Beat website , the number of L2 networks has exceeded 70, reaching 71, with a total TVL of over 37.46 billion US dollars.

Subsequently, Solana, built in the Rust language, focused on the concept of Ethereum killer. After a series of twists and turns, it finally achieved a phased overtaking - in July, the Solana ecosystem DEX transaction volume surpassed Ethereum for the first time, reaching US$55.876 billion (Ethereum was US$53.868 billion); the number of active addresses on the Solana chain reached 54.33 million, a record high, a significant increase of 151% from 21.6 million at the beginning of 2024, and the number of non-voting transactions reached a peak of 1.3 billion, and on-chain activities were very active; in addition, according to Qiao Wang, founder and core contributor of Alliance DAO, in the past 6 to 12 months, a large number of application developers have switched from Ethereum to Solana, and almost no migration in the opposite direction has been seen.

At the same time, based on the Rust language, blockchain networks such as Aptos, Sui, Linera built on the Move language, and Movement Labs, which previously raised more than 40 million US dollars in financing, have also been on the right track and have received continued support from star institutions such as a16z and Polychain.

It can be said that although we are still some distance away from the day when “ten thousand chains are launched simultaneously”, the multi-chain ecosystem is a foregone conclusion.

Evolution of discourse power: from east to west

As for the evolution of discourse power, the subjects and levels involved are more complicated.

In the early days of the cryptocurrency industry, Bitcoin mining resources, which are related to the industrys discourse power, were mainly in the hands of Eastern industry insiders. Companies that are well-known to industry insiders, including Canaan Technology, Antminer, and Bitmain, were recognized as the backbone of the industry at the time. After all, the situation at the time was whoever controls the mining machines (computing power resources) controls Bitcoin.

However, with the development of the industry, especially the rise of Ethereum and various sub-tracks based on the development of the Ethereum ecosystem, more and more attention is paid to the support of investment institutions in terms of funds, resources and platform endorsement. Although Eastern industry players occupy a leading position in the exchange field with their strong technical strength, first-mover advantage and operational means, they are affected and pressured by the regulatory level, and project development and investment activities are much worse than before. As a result, the current situation has resulted in the situation where the right to speak is mainly controlled by Western capital.

After U.S. mining companies became the main force of Bitcoin computing power, the leading stablecoin issuers Tether, Circle and Coinbase became the first U.S. stock exchange to be listed, and other events have further strengthened the influence of Western capital on the development of the industry. Including the Web3 boom from 2021 to 2022, it is also inseparable from the advocacy and dissemination of American capital such as a16z.

In the end, Western capital, which holds more capital power, has the right to speak in upstream project investment in the industry, and thus takes the initiative in the market structure; although the Eastern community is good at the development of exchanges, its industry role eventually shifts to downstream ecological niches such as market users. The successive approval of Bitcoin ETF and Ethereum ETF in the United States has once again boosted this situation.

Just as Zweig said, all the gifts of fate have already been secretly marked with a price. Todays venture capital landscape is a concentrated reflection of the foreshadowing of yesterday.

To some extent, Asian capital is more focused on projects related to the Mass Adoption track, which is also a helpless choice. After all, compared with the Western market that is good at promoting narratives and leading innovation, Eastern forces are better at applications and operations. This is one of the reasons why some Eastern capital chooses to bet on the TON ecosystem that focuses on operations.

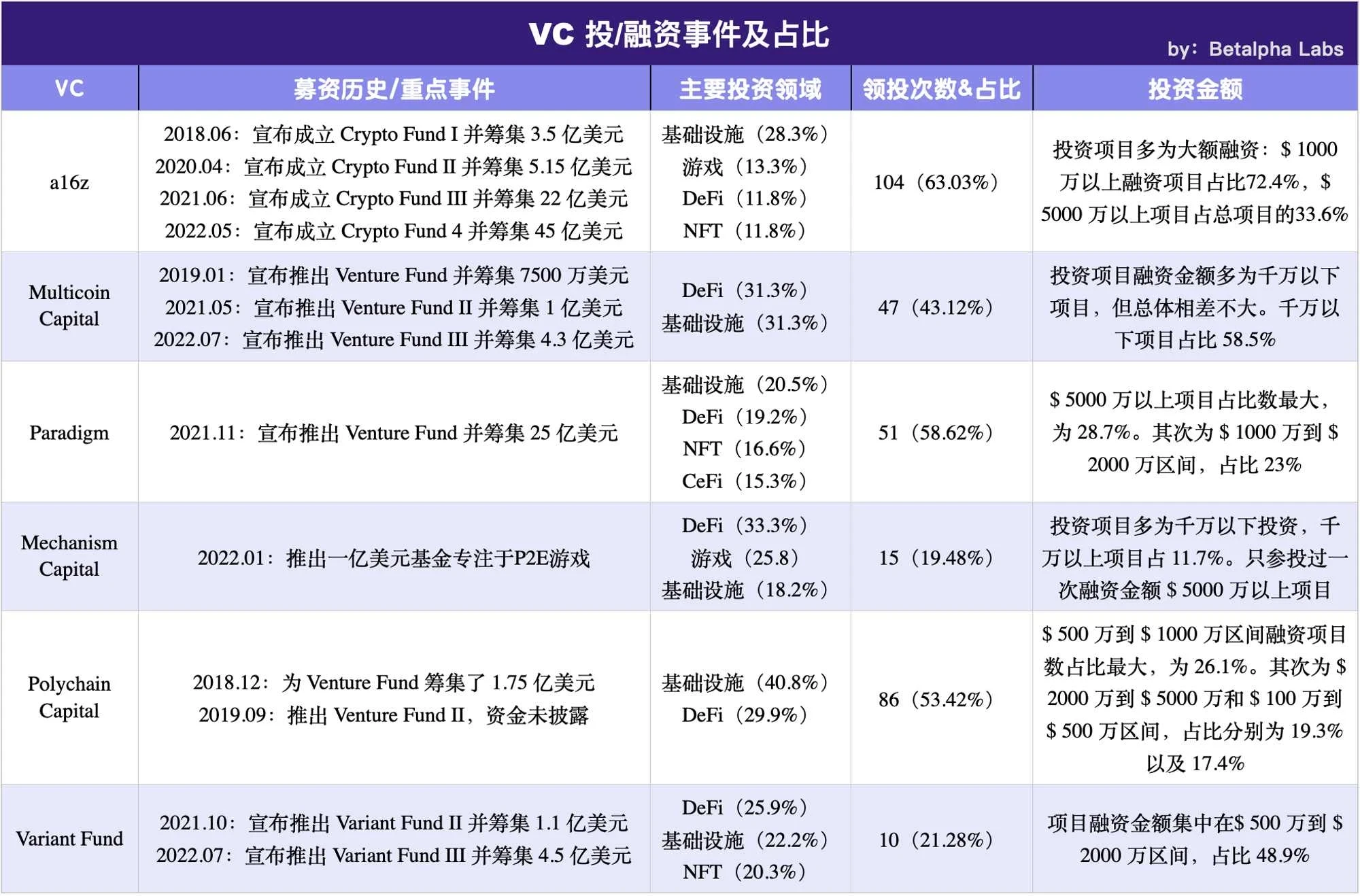

Summary of investment preferences of six top VCs

Conclusion: Everything for liquidity, everything for liquidity, everything for liquidity

Finally, please allow me to end this article with a classic syllogism: Looking back at the venture capital cycle of the cryptocurrency industry, individuals, institutions, and projects that can see through the theory of evolution are all focused on the word liquidity. The so-called asset distribution, technological innovation, track evolution, and resource allocation are essentially for the purpose of developing liquidity, undertaking liquidity, guiding liquidity, and retaining liquidity. Only in this way can the vitality of DeFi be preserved and it can become an evergreen tree in the cryptocurrency market.

However, fields such as NFTFi, SocialFi, GameFi, and DAO organizations, due to lack of liquidity, inefficiency, and lack of positive externalities, can only become countless fine grains of sand in the surging market wave, and are gradually falsified. Including the highly PVP market such as Meme Coin, if the lack of liquidity is not unbearable, the number and scope of participating players will be far less than it is now.

As the market has high expectations for the Feds rate cut and hopes that it can bring about another violent bull market, where will the cryptocurrency industry go next? Perhaps only time can tell us the answer. In any case, the cryptocurrency wave led by Bitcoin is far from over and will continue.

Thanks to Mandy, the founder of Odaily Planet Daily, for her reference, thanks to Fang Zhou, the editor-in-chief of Odaily Planet Daily, for the editing and correction, and thanks to Erin, the business director of YBB Capital, for the additional information. This article took more than a month to write, but due to my limited writing skills, I can only give a one-sided summary of past history. If there are any errors or omissions, please forgive me.

Reference articles:

10,000-word analysis of the investment profile and strategic layout of six top crypto VCs

RootData: 2023 Web3 Industry Development Research Report and Annual List