TL;DR

-With the improvement of the underlying infrastructure, both institutions and individuals have shown new interest in crypto payments and brought a new impetus to the rise of PayFi.

-PayFi has many advantages such as improving capital efficiency, and serves as a central hub to closely connect traditional financial institutions, merchant networks, DeFi and RWA.

-PayFi brings the most significant marginal improvements to cross-border payments and subscription billing, and is therefore most likely to be the first mover area.

More than four years have passed since the DeFi summer of 2020, which was triggered by liquidity staking. The political wave of Republican presidential candidate Donald Trumps re-election and majority in both the Senate and the House has reactivated the enthusiasm of the cryptocurrency market. In 2024, can PayFi, a relatively new concept and track, stand out in this round of bull market?

1. Crypto Payments and PayFi

1.1 Blockchain’s transformation of the payment system

On November 1, 2008, Satoshi Nakamoto published an article titled Bitcoin: A Peer-to-Peer Electronic Cash System, which directly pointed out that the original intention of Bitcoin was to completely revolutionize the traditional payment system and create a decentralized electronic transaction system without the need for mutual trust between the two parties. Although Bitcoin is currently more regarded as a value storage tool rather than a currency for daily transactions.

In the field of payment, blockchain technology is closer to this original intention. By reducing intermediaries, accelerating transaction processing and reducing costs, blockchain has brought significant innovations in payment methods. Traditional payment systems rely on banks or payment processors to complete transactions and settlements, which not only prolongs transaction time, but also brings higher fees. Especially in cross-border payments, the complex network of agency banks further increases costs and reduces efficiency. Blockchain realizes peer-to-peer payment through distributed ledgers. Users only need to provide the other partys wallet address to directly send cryptocurrency. The entire payment process is transparent and traceable, which greatly reduces the intermediary links, increases payment speed and significantly reduces costs.

In addition, blockchain technology also has significant advantages in privacy protection and data security. Since transaction records are encrypted and distributed, transaction information can not only be verified in all nodes of the network, but also effectively avoid the risk of information leakage and tampering in traditional payment systems. This decentralized and distributed payment method solves several core problems in traditional payment systems: low transparency, long transaction time, and high costs caused by multiple layers of intermediaries. Therefore, the application of blockchain in the payment field has significantly improved the users payment experience and increased the efficiency of capital circulation.

1.2 The prosperity of the crypto payment market is the spring breeze of PayFi narrative

As we approach the end of 2024, blockchain payments have suddenly accelerated. Many mainstream financial institutions have begun to increase their support for blockchain payments:

On September 26, BlackRock partnered with Ethena to issue the US dollar stablecoin USDb.

On October 3, PayPal worked with EY to complete the first stablecoin commercial remittance using its self-issued PYUSD.

On October 3, VISA announced the VTAP platform to help institutions independently issue and operate stablecoins.

Also on October 3, SWIFT announced that it will launch digital currency and digital asset trading experiments in 2025.

On October 16, Internet payment giant Stripe announced a partnership with Paxos to support stablecoin payments.

On October 19, Societe Generale issued the euro stablecoin EUR CoinVertible.

On October 21, Stripe announced the acquisition of stablecoin payment startup Bridge for US$1.1 billion.

On October 22, the BRICS Summit in Kazan, Russia announced the BRICS Pay payment system, which will compete with SWIFT.

On October 24, Coinbase and A16Z jointly invested in Skyfire, a blockchain payment company that integrates AI technology.

In addition to the real money investments of a number of traditional financial institutions and crypto market investors, the general public has also supported crypto payments with their own choices. As of November 20, 2024, the market value of global stablecoins has increased significantly by 46% this year, with a total market value exceeding US$190 billion. According to a report released by Visa in September 2024, more than 20 million addresses conduct stablecoin transactions on public blockchains every month. In the first half of 2024 alone, the settlement amount of stablecoins exceeded US$2.6 trillion. Stablecoins have significant advantages over existing payment systems: on-chain programmability, strong auditing capabilities, transaction settlement, self-custody of funds, and interoperability.

Geoff Kendrick, head of digital asset research at Standard Chartered Bank, and Nick Philpott, co-founder of Zodia Markets, pointed out that the application of stablecoins is expanding from trading collateral to cross-border payments, salary payments, trade settlements and remittances, especially in emerging markets such as Brazil, Turkey, Nigeria, India and Indonesia. Blockchain payments are becoming a force that cannot be ignored in the global financial system with their ability to cross trust boundaries, greatly improved efficiency, reduced costs, and broad support from the younger generation.

Crypto payment is the foundation of PayFi. Without popularized and convenient crypto payment, there will be no real PayFi. The resurgence of the crypto payment market is the spring breeze of PayFi.

1.3 PayFi’s New Narrative

Based on blockchain, especially Solana blockchain, PayFi innovatively proposed a new payment finance (PayFi) model. This model combines blockchain and smart contracts to manage fund flows through digital assets and decentralized finance (DeFi) tools. The core concept of PayFi is to maximize the Time Value of Money (TVM) and significantly shorten the settlement cycle with the help of decentralized technology. Unlike traditional payment methods, PayFi is not only a payment tool, but also aims to create an open and decentralized financial ecosystem.

PayFi highlights its disruptive philosophy through the concept of Buy Now, Pay Never. This concept allows users to deposit funds into a decentralized lending platform, earn interest through smart contracts, and use these earnings to pay daily expenses without touching the principal. This model not only enables users to benefit from the time value, but also effectively subverts the concept of cash flow-based traditional payments. PayFis time value maximization model is particularly suitable for users who want to manage their funds more efficiently. Through liquidity management and incentive mechanisms, PayFi not only has advantages in payment efficiency and cost, but also further expands the application scenarios of payment finance, presenting a more efficient and intelligent payment experience.

1.3.1 Advantages of PayFi

Improve capital utilization efficiency

The core concept of PayFi is Time Value of Money (TVM). Users can lock their funds on the lending platform to generate interest, and use the interest to pay daily expenses without using the principal. This model effectively improves the efficiency of fund utilization, allowing users to obtain continuous returns on their funds without using them.

Fast, low-cost payments

Traditional payment systems (such as SWIFT) usually take several days to settle and are expensive. Based on blockchain technology, PayFi automates the payment process through smart contracts, achieving transaction processing in seconds at extremely low costs. For businesses and individuals who need fast capital turnover, PayFis high efficiency significantly improves the payment experience.

Supporting the tokenization of real assets

PayFi tokenizes real assets (such as real estate and accounts receivable) to facilitate the efficient flow of global capital. Tokenization improves the liquidity of physical assets and simplifies cross-border payment processes. Especially for small businesses, by using accounts receivable as collateral for financing, they can obtain cash flow faster and relieve funding pressure.

Decentralization and openness

PayFi has built an open decentralized financial ecosystem that does not rely on traditional banks or financial institutions. Any user can use payment and financial services within the system. This decentralized model gives users greater financial autonomy while enabling financial services to reach those who lack bank accounts.

Innovative cross-border payment solutions

With the growth of international trade, the demand for cross-border payments continues to increase. PayFis decentralized cross-border payment solution does not require cumbersome intermediary processes, can achieve fast settlement, and reduce the risks brought by exchange rate fluctuations. It is especially suitable for enterprises and individuals who frequently conduct cross-border transactions.

1.3.2 PayFi’s Ecosystem Development

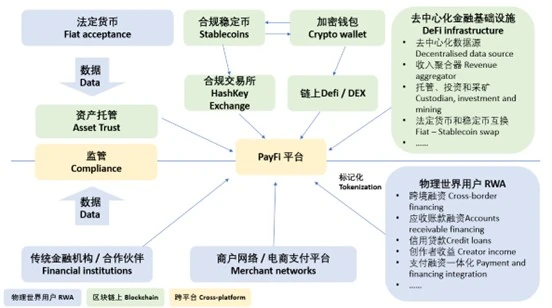

The PayFi platform serves as a central hub that closely connects traditional financial institutions, merchant networks/e-commerce payment platforms, DeFi infrastructure, and physical world assets (RWA).

The fiat acceptance, data management, asset trust and compliance modules in the traditional financial system show the connection between PayFi and banks and other financial institutions. This integration enables PayFi to better utilize the liquidity of traditional finance and meet the payment needs of fiat currency .

Stablecoins and crypto wallets provide users with decentralized payment and trading services through compliant crypto exchanges (such as HashKey Exchange) and on-chain DeFi/DEX. This part supports cross-border payments and low-cost transfers.

The DeFi infrastructure module includes decentralized data source , revenue aggregator, custody, investment, etc. These components provide technical support for PayFi and enhance the decentralized properties of the platform.

The Real World Asset User (RWA) module shows how PayFi can be applied to real-world scenarios, such as cross-border financing, accounts receivable financing, and credit loans, to provide users with real financial services. Overall, the PayFi ecosystem connects blockchain technology and traditional financial services at multiple levels, providing users with flexible and efficient payment and financing solutions.

2. Similarities and differences between DeFi and PayFi

PayFi is not completely equivalent to DeFi. The essence of payment is based on the transfer of value (value exchange) in the real world - exchanging money for goods/services. Therefore, PayFi is more about the process of sending and settling digital assets rather than the mainstream transaction behavior of DeFi. In addition, seamlessly connecting Web3 payments with DeFi through blockchain and smart contract technology is also an important advancement for creating payment-related financial derivative services such as lending and wealth management.

However, PayFi is a new thing based on the modular development and revenue flow of DeFi business, that is, PayFi is a new business built on the composability and revenue generation of DeFi. However, the liquidity pool in DeFi business needs to be contributed by liquidity providers (LPs), whose incentives often need to be paid in tokens in the past, while the liquidity pool in PayFi business is generated by the cash flow locked in the payment process.

3. Analysis of PayFi’s specific application scenarios

The PayFi model combines payment and financial services (such as loans, savings, remittances, etc.) to provide a one-stop solution through stablecoins and blockchain technology. Its main features include: (1) Low-cost and efficient payment: Payments made through stablecoins, especially in the field of cross-border payments and remittances, have significant cost advantages over the traditional financial system. PayFi helps individuals and businesses reduce transaction fees and improve the efficiency of fund transfers through stablecoin payments; (2) Integration of financial services: In addition to payment functions, PayFi also provides more financial services to businesses and consumers, such as micro loans (MicroLending), cryptocurrency salary payments (Payroll), and income-generating stablecoins. These services can attract more users and increase customer stickiness.

A. Tokenize real assets and create a payment framework through stablecoins

PayFi uses stablecoins as a key tool to move traditional payment logic to the blockchain, which has a wide range of applications. Stablecoins such as USDT, USDC, PYUSD, etc. combine the value of fiat currency with cryptocurrency, providing a more stable and low-volatility payment method. Unlike speculative activities such as high-yield lending or liquidity mining in DeFi platforms, stablecoins focus on the smoothness and wide application of payments.

Application examples:

Stablecoin payments: Users can use stablecoins for daily payments, especially on a global scale, where stablecoins provide a convenient, low-cost option for cross-border payments. For example, with stablecoins USDC or USDT, users can make payments almost instantly and at low cost anywhere in the world. PayFis strength lies in its ecosystem integration. Through automated compliance tools and transparent blockchain technology, PayFi improves payment speed, security, and significantly reduces transaction costs.

DeFi Integration: Stablecoins are not only payment tools, but also core assets of DeFi. They can serve as a source of funds for liquidity pools, enabling DeFi protocols to provide efficient trading and lending functions. By depositing stablecoins into liquidity pools, users can earn transaction fees before payment. This capture of time value not only provides passive income, but also enhances the liquidity of the payment process.

In these application scenarios, the biggest advantage of stablecoins lies in their programmability and compatibility with other blockchain applications. Users can automate payment and reward mechanisms through smart contracts, further improving the level of intelligent and automated payment.

B. Payment Tokens - Tokenized Financial Assets

In the process of generating the time value of money, a claim is formed between the seller of goods or services and the buyer. This claim can be re-financialized before it is repaid, which minimizes the occupation and demand for funds and stimulates asset liquidity (see undiscounted bank acceptance bills). When the claims are packaged and traded again to form financial products such as undiscounted bank acceptance bills, the financial attributes and liquidity of the Payfi ecosystem will be stimulated to a greater extent. The payment token model represents the tokenization of traditional financial products (such as U.S. Treasury bonds, money market funds, etc.) and the introduction of blockchain, which not only provides new income opportunities for investors, but also provides capital efficiency for payment scenarios.

Application examples:

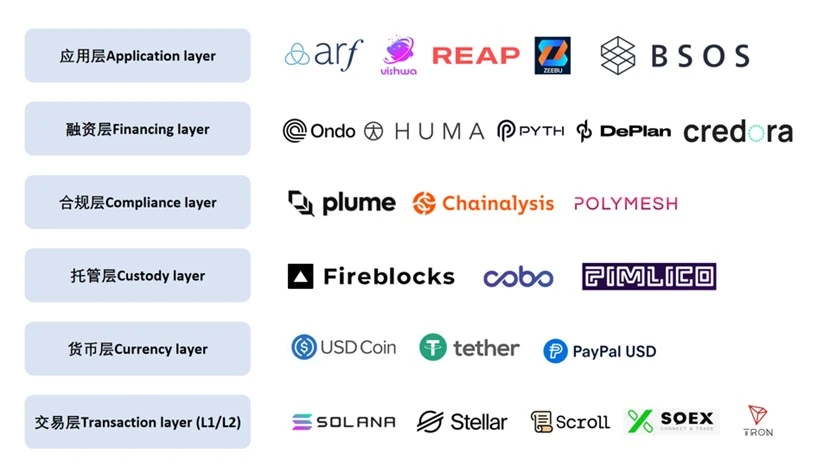

Ondo Finance created the Ondo US Dollar Yield Token (USDY) by tokenizing low-risk, stable-yield financial assets such as short-term US Treasury bonds. This tokenized product allows users to not only participate in stable-yield investments, but also use these tokens for more capital operations in DeFi platforms. Ondo Finance also provides risk-graded financial assets such as government bonds and corporate bonds on the blockchain, so that investors can allocate funds according to their own risk preferences.

USDY tokenization: USDY is a token secured by short-term U.S. Treasury bonds and demand bank deposits. Investors can buy USDY and enjoy the benefits of tokenized notes. Compared with traditional bank deposits or low-risk investments, USDY provides users with high liquidity, and users can use it to combine and increase capital on DeFi platforms. For example, USDY holders can use USDY as collateral to obtain loans on lending platforms to increase the liquidity of funds. This asset tokenization method provides high liquidity and payment convenience.

USDYs APY: Ondo Finance adjusts the annual percentage yield (APY) of its tokens according to market conditions. Taking USDY as an example, investors can get continuous returns based on the yield of the USDY they hold. Unlike traditional financial instruments, USDY can be embedded in DeFi protocols in the form of smart contracts, making investment returns automatic and programmable. Users can get a stable annualized yield (APY) while paying. This combination of investment income and payment functions helps users achieve capital appreciation and flexibility in transactions.

In this way, Ondo Finance not only provides investors with the opportunity to tokenize U.S. Treasuries, but also further improves capital efficiency and flexibility through DeFi integration, helping users to operate capital in the decentralized financial ecosystem.

C. DeFi lending and real-world asset (RWA) financing

Huma Finance demonstrates how to finance real-world assets (RWA) through DeFi lending and enable transparent and efficient payments on the blockchain. In this model, Huma Finance tokenizes real-world assets such as accounts receivable of enterprises, allowing enterprises to obtain financing and solve capital flow problems through cross-border payments.

Application examples:

Asset Tokenization: Huma Finance tokenizes RWAs such as accounts receivable and future revenue, thereby improving asset liquidity. In this way, companies can raise funds from investors at a lower cost and with higher transparency. These tokenized assets can be used as collateral for loans, further facilitating capital mobility.

Cross-border payments: Huma Finance solves the pain points of cross-border payments for global enterprises through integration with the Arf platform. Enterprises can use tokenized accounts receivable as collateral to apply for USDC credit lines, thereby avoiding pre-locking of funds. After the cross-border payment is completed, the enterprise needs to repay the loan in a short period of time, which not only improves the efficiency of fund use, but also simplifies the cross-border transaction process.

Low-risk, high-return lending model: Through cooperation with Arf, Huma provides a low-risk, high-return lending model. In this model, investors can obtain a relatively high annualized rate of return by providing funds to support corporate cross-border payments, while companies can use this mechanism to solve the problem of liquidity shortage.

Investor Protection: Huma Finance protects investor rights by introducing a risk grading model, such as allocating high-risk assets to investors who are more willing to take risks, while providing low-risk assets to attract more conservative investors.

This RWA tokenized lending model not only enhances the practical application of the DeFi platform, but also provides a stable and efficient financing solution, which is especially important for small and medium-sized enterprises and cross-border payments.

D. Payment Incentives and Creator Benefits

Application example: SOEX

SOEX tokenizes traditional exchange trading behaviors, allowing users to earn rebates through small transactions when participating in exchanges (such as Binance, OKX, etc.). This social mechanism encourages ordinary users to participate, increases the trading volume of the exchange and optimizes the distribution of rebates.

Socialized rebates: Traditional exchanges usually offer higher rebates to institutional investors, while retail users find it difficult to obtain the same benefits. SOEX integrates retail trading behaviors to form a larger trading pool, thereby obtaining higher rebates, and distributes rebates based on each users contribution. This mechanism greatly improves the participation and profit opportunities of ordinary users in the exchange.

Application example: DePlan

DePlan provides users with flexible subscription payment options by tokenizing unused subscription services. Users can rent out their unused subscription time to other users who need temporary use and earn revenue from it. This innovative model not only solves the problem of resource waste under the traditional subscription system, but also provides users with a more efficient payment method.

Tokenization of subscription time: DePlan allows users to tokenize the unused portion by tracking the actual usage time of their subscription content. Each token represents a certain amount of unused time, and users can rent these tokens to other users and earn corresponding income.

Pay as you go: For those who only need temporary access to an application or service, DePlan provides a pay-as-you-go option. This flexible payment method allows users to choose the most suitable payment plan based on their actual needs, avoiding the long-term fixed fees of traditional subscriptions.

DePlan provides consumers with greater payment flexibility through this innovative Web3 payment method, and also solves the waste and inefficiency problems in traditional subscription services through blockchain technology.

4. PayFi’s potential first-mover areas

According to Newtons third law, the greater the action, the greater the reaction. The most likely scenario for PayFi is in those business sectors where crypto payment businesses will bring huge cost savings and decentralization advantages after they take root.

Cross-border payments

Currently, Payfi, which is based on blockchain payment, has its vitality first in payment. The most vibrant area of blockchain payment is cross-border payment. The so-called cross-border payment is actually not simply understood as payment and settlement across different nation-states or administrative boundaries, but is closer to settlement barriers across different financial systems, different nation-states, and even different organizations. If we abstract from a macro perspective, the original cross-border payment and settlement system is a process of aggregating individual transaction needs into a centralized system, and then different centralized systems interact with information flows and capital flows, and finally the centralized system feeds back each transaction demand to the individual.

In the field of cross-border payments, the traditional financial system faces many challenges, especially in terms of currency controls, capital flow restrictions, and long settlement cycles. Cross-border payments usually rely on systems such as correspondent banks and SWIFT, which require layers of audits and intermediary verification, extending settlement time and increasing costs. In this process, traditional financial institutions usually use prefunded accounts to provide a real-time payment experience. However, this model leads to a large amount of capital being locked up, limiting the time value of funds. According to Arfs research, more than $4 trillion of funds in prefunded accounts around the world will be illiquid in 2022. This not only leads to a lot of waste of time value, but also makes cross-border payments more expensive and inefficient.

Blockchain payment, on the other hand, completely deconstructs the macro-centralized financial payment and settlement system into a transaction payment system between micro-individuals through blockchain technology. In this deconstruction process, the original transaction costs (including contract costs, time costs, rent-seeking space and seigniorage) all disappear, and what is obtained is a decentralized and flat transaction payment system. If this system can be implemented in the field of cross-border payment, where the contract costs and time costs are extremely high, traditional financial intermediaries are entrenched, and seigniorage is high, it will bring great marginal improvements and release a large amount of deposited funds in the cross-border payment system. PayFi reduces the need for intermediaries in cross-border payments through blockchain technology, allowing payments to be completed faster and at a lower cost. The PayFi system can realize decentralized capital flow without the need for complex intermediary processing like traditional systems, thereby speeding up settlement and reducing the cost of using funds. Simply by reducing the fee extraction of intermediary links and releasing the liquidity locked in cross-border clearing accounts, Payfi will provide a huge pool of funds.

Subscription Billing Model

Traditional subscription services require users to pay regularly regardless of actual usage. In the traditional subscription service model, users usually need to pay a fixed fee regularly regardless of their actual usage. This model is not only inflexible, but also cannot be adjusted according to the actual usage needs of users. PayFi has introduced a pay-per-use model through the innovative DePlan project, allowing users to pay according to their actual service usage, thereby achieving a more flexible consumption method.

Liquidity Management

Supply chain finance is an important part of global business, but traditional supply chain financing often leads to slow capital turnover due to complex legal processes and approval links. For enterprises, this inefficient financing method limits capital liquidity and increases operating costs. PayFi uses decentralized liquidity pools to enable enterprises to obtain funds more quickly, improve the speed of capital circulation, and reduce dependence on traditional banks. In supply chain finance, PayFis decentralized model allows enterprises to accelerate capital turnover, reduce the problem of capital occupation caused by long payment cycles, and alleviate the financing pressure of small startups.

5. Current challenges that hinder PayFi’s widespread adoption and operational efficiency

5.1 Complexity of cross-border payments

While PayFi aims to simplify cross-border transactions, it still faces unresolved issues with regulatory hurdles, currency controls, and enterprise-level integration.

The first is regulatory barriers. Each country has different regulatory policies on currency flows and cross-border transactions, which makes cross-border capital flows complicated and time-consuming. The high costs and inefficiencies caused by inconsistent regulations and differences in compliance requirements in different regions increase transaction complexity and management difficulties. The second is the issue of currency control. For example, many countries have strict foreign exchange controls on the entry and exit of funds, and if PayFi wants to expand its business globally, it needs to adapt to the policies of different countries and regions. This puts higher demands on the fund settlement process, and it is also necessary to ensure compliance with local foreign exchange regulations, otherwise it may face huge fines or even be banned from operating.

Cross-border payments also involve technical challenges. For example, real-time payment technology (RTP) has been implemented in many countries, such as the PIX system in Brazil and the ASEAN low-value cross-border system in Southeast Asia. However, the fact that payment systems in different countries are not fully interoperable has caused fragmentation of cross-border payment networks, affecting the immediate liquidity of funds. Although many fintech companies are using artificial intelligence and real-time processing technologies to optimize payment routing and reduce operating costs, compatibility issues between different systems remain prominent. Finally, the difficulty of enterprise-level integration has also hindered the further popularization of PayFi. Enterprise users often need to achieve seamless integration with their existing ERP systems, CRM systems, etc. to meet business needs. However, such integration is usually time-consuming and technically demanding. In cross-border payments, enterprises are particularly dependent on efficient integration between systems to ensure the accuracy and timeliness of payments, but this deep integration is a heavy burden for small and medium-sized enterprises, so their demand for PayFi has not yet been fully released.

5.2 Adoption of subscription billing model

PayFi offers an innovative pay-per-use model, but market penetration is low due to technological limitations and low user awareness.

One of the main obstacles to the promotion of PayFis subscription billing model is technical limitations. Traditional payment systems lack flexibility in the pay-per-use model. For blockchain payment solutions like PayFi, it is complex to achieve automated real-time billing and payments, especially when it needs to be integrated with traditional banking systems or existing financial infrastructure. This is especially important when processing micropayments (i.e. small, regular payments), which require high-frequency processing of smaller transactions, which generally requires the system to have higher stability and accuracy. To this end, PayFi needs to invest a lot of resources to optimize its technical architecture to meet market needs in terms of security, accuracy, and timeliness.

In addition, lack of user awareness also affects the adoption of PayFis subscription billing model. Since the concept of blockchain and crypto payments is relatively new to the general public, many consumers and merchants still have a low understanding and acceptance of this model. Compared with traditional payment methods, the pay-per-use subscription model requires users to have a deeper understanding of the fee structure and payment process. However, the current lack of relevant education and publicity in the market has led users to tend to choose familiar traditional payment methods when choosing a payment method. To solve this problem, PayFi needs to invest more resources in marketing to increase users understanding and acceptance of its pay-per-use model.

The low market penetration rate is also closely related to the difficulty of integration for merchants. For most merchants, adopting a pay-per-use model means updating and transforming the payment system. This not only increases the merchants technical investment and maintenance costs, but may also affect the existing customer experience. In addition, different merchants have different needs for pay-per-use. For example, some traditional enterprises may prefer an annual or monthly subscription model, and have a lower demand for instant billing. Therefore, when promoting the pay-per-use model, PayFi needs to adjust its product design and service solutions according to the needs of different merchants to better meet the diverse needs of the market.

5.3 Liquidity and capital flow issues

While PayFi simplifies supply chain financing, liquidity integration (RWA) with traditional finance is still developing, resulting in slow capital turnover for businesses.

The main challenge that PayFi encounters in liquidity integration is that the integration of real-world assets (RWA) with traditional financial institutions is not yet mature. RWA refers to physical assets in the real economy, such as real estate, commodities, or stocks, and its connection with digital finance is relatively complex. PayFi has currently simplified the process of supply chain financing, but the liquidity integration with traditional finance is still in its early stages, which directly affects the capital turnover efficiency of enterprises. Incomplete integration of RWA will not only increase the capital turnover cost of enterprises, but also lead to long settlement time, exposing enterprises to the risk of insufficient liquidity.

The capital efficiency problem in the blockchain financial system also limits the liquidity of PayFi. Due to the decentralized nature of blockchain itself, the liquidity of funds between different on-chain protocols is different, and different governance mechanisms and token standards are involved, resulting in limited capital circulation between different protocols. This means that when users try cross-chain operations on the PayFi platform, liquidity may be greatly affected, resulting in insufficient liquidity flexibility and difficulty in meeting the dynamic needs of enterprises.

At the same time, PayFi also has some difficulties in integrating liquidity pools and staking in cross-chain and multi-chain operations. Although liquidity pools can provide financial support for users, the implementation of cross-chain liquidity pools requires solving the interoperability problem between different blockchains, which is not yet fully mature. There are technical complexities in cross-chain liquidity management, which leads to higher operating costs and also makes users face higher risks when using liquidity pools. The instability of this liquidity pool not only limits PayFis liquidity supply capabilities, but also reduces users trust in its platform.

The limited flow of capital is also related to the performance of the blockchain infrastructure itself. Blockchain systems often face performance bottlenecks when processing high-frequency transactions, especially in scenarios with high liquidity requirements. For example, the high transaction fees and network congestion of the Ethereum network limit the efficient flow of large-scale funds. Although some emerging blockchains (such as Solana and Polygon) are committed to solving these performance issues, since PayFi must take into account the interoperability between different blockchains, its liquidity management is still affected by the performance of the infrastructure.

5.4 Usability and Integration Barriers

Regular users still struggle to manage wallets across multiple blockchains and encounter difficulties with liquidity pools and staking.

PayFis promotion is subject to many usability and integration limitations, especially in terms of user management of cross-chain wallets and the use of liquidity pools and staking. Although the platform aims to provide simplified payment solutions, the complexity of cross-chain operations makes it difficult for ordinary users to manage assets on multiple blockchains. Due to the large differences in protocols and operations of different blockchains, users often encounter technical barriers and inconveniences in actual operations. With the development of cross-chain technology, security issues still exist, which makes users worry about asset management.

Liquidity pools and staking mechanisms are also full of technical barriers and uncertainties for novice users. These functions usually involve relatively complex mechanisms and operational steps. For example, users need to understand the potential risks and benefits of liquidity provision when participating in liquidity pools, while staking operations include relatively complex economic structures such as token locking and profit distribution. Many users, lacking sufficient blockchain knowledge, are prone to financial losses due to insufficient understanding. Therefore, these high-threshold functions further reduce the enthusiasm of ordinary users to participate and limit PayFis appeal to a wider user group.

In terms of enterprise applications, PayFi has also encountered significant challenges in connecting with traditional enterprise systems. The decentralized data structure of blockchain is difficult to be fully compatible with the centralized systems of traditional enterprises, especially when connecting with existing enterprise systems such as ERP, data format and security issues are particularly prominent. Enterprises often need to invest a lot of technical resources to solve these compatibility issues, which invisibly increases the integration cost and technical difficulty of the PayFi system, thereby hindering its application and promotion in traditional industries.

To address these challenges, PayFi can start from user-friendliness, simplified operations, and system compatibility. One direction to improve user experience is to provide a more intuitive user interface and simplify the cross-chain operation process. In addition, PayFi can also develop adaptation interfaces and reduce enterprise integration costs through in-depth cooperation with traditional financial systems. Such improvement measures will help enhance PayFis market competitiveness and further promote its popularity.

6. Summary

6.1 PayFi is a fusion of payment, RWA and DeFi

PayFi is not an innovative independent concept, but an innovative application that integrates Web3 encrypted payment, RWA and DeFi. This new business includes the payment and transaction of digital assets and off-chain goods and services, and also covers various financial activities such as lending, financial management, investment, etc., and stimulates new asset liquidity. Based on blockchain and smart contracts, the PayFi ecosystem has reshaped the global payment system while reducing the friction and costs brought by intermediaries in the traditional financial market.

6.2 PayFi relies on a high-performance settlement system and relatively stable APY

6.2.1 High-performance settlement system

A blockchain transaction settlement system with low latency, low transaction fees, and high computing speed is the common expectation of all crypto people. PayFi is a business that deeply integrates the three major sectors of crypto payment, RWA, and DeFi, and is also one of the transaction bridges between the two worlds of on-chain and off-chain. High-performance settlement is the premise for the large-scale promotion of the PayFi ecosystem, that is, PayFi relies on a blockchain system with low latency, low transaction fees, and high computing speed. In addition, the payment characteristics of PayFi itself include a large number of processing requirements with low transaction amounts and high immediacy requirements, which further puts forward higher requirements for low latency, low transaction fees, and high computing speed of the settlement system.

6.2.2 Relatively Stable APY

In terms of revenue sharing, the PayFi ecosystem has a huge pool of funds as its foundation, and it also needs to obtain relatively stable income cash flow to realize the time value of money. The investment targets required by the fund pool need to be relatively stable, because the previous goods or services have completed the physical transaction and are waiting for the funds sufficient to pay for the transaction to arrive. Therefore, the yield of the investment target will greatly affect the time to complete the redemption. Therefore, products with relatively stable yields are needed to be available. With the rise of the RWA wave, the tokenization of offline assets with relatively stable yields such as gold and treasury bonds will provide a relatively stable investment product portfolio for the fund pool aggregated in the payment process.

References

https://mp.weixin.qq.com/s/RlExUSYAGtxcnwGXGRgxPQ

https://www.techflowpost.com/article/detail_21806.html

https://www.panewslab.com/zh/articledetails/t6d5 7ner.html

https://www.aicoin.com/en/article/423326

https://www.bitget.com/news/detail/12560604205937

https://blog.huma.finance/payfi-the-new-frontier-of-rwa

https://www.chaincatcher.com/en/article/2148511

https://x.com/web3 caff_zh/status/1849653789126697088

https://www.panewslab.com/applyforcolumn/articledetails/ne7ekpvt.html

https://www.chaincatcher.com/upload/image/20241031/1730356285255-258770.webp

{kind=link}