Original title: Weekly: Chaotic Crossroads

Original author: David Han (Institutional Research Analyst)

Release Date:April 19, 2024

Key Takeaways

The sharp drop following the intensification of conflict in the Middle East over the weekend and continued lower has washed out a lot of leverage in the space, even as the Bitcoin halving approaches.

The BTC perpetual contract funding rate briefly turned negative for the first time since October 2023 and has remained near zero since then.

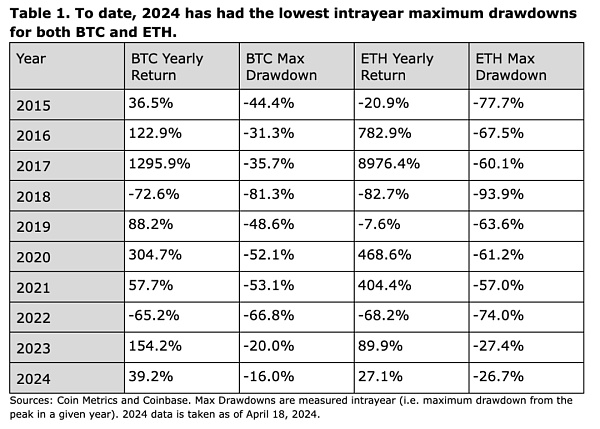

So far, the 2024 BTC declines have been the smallest so far, at 16% and 27%, respectively, and are even lower than the record levels in 2023. Therefore, more room may open up to the downside, and traders have been positioning themselves accordingly based on options and on-chain data.

market

Leverage has largely been cleared out of the market as the halving approaches. Bitcoins sharp drop following the intensification of conflict in the Middle East over the weekend, combined with continued lower movement over the past week, caused the BTC perpetual futures funding rate to briefly turn negative for the first time since October 2023. Since then, the funding rate has remained near zero and has crossed the zero mark several times in recent days. We believe this may indicate some temporary short bias, but there is no large-scale panic effect. We believe this directional uncertainty illustrates our view on Bitcoins dual role as a risk-on asset and a safe haven asset. While marginal sellers appear to be mainly reducing risk, strong buying has also occurred between $60,000 and $62,000.

However, this is not to say that the market cannot potentially go further lower. From a maximum retracement perspective, 2023 was the best year for cryptocurrencies, with peak retracements of 20% for BTC and 27.4% for ETH. Prior to this, the smallest maximum retracement for BTC was 2016 at 31.3%, and the smallest maximum retracement for ETH was 2021 at 57% (see Table 1). The retracement so far in 2024 is even smaller than that in 2023, and given the elevated realized volatility levels year-to-date, further downside is entirely possible.

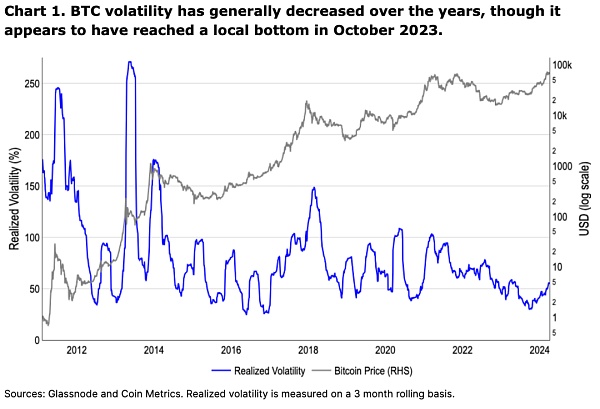

Volatility in the asset class has generally been declining since its launch 15 years ago, although a local bottom in 3-month realized volatility was reached in October 2023 (see Figure 1). Since then, prices have steadily reversed upward as volatility has increased. We believe that if we continue to have a hawkish risk-off environment, those who view Bitcoin as a risk-on asset may continue to sell until they reach equilibrium with the group that views Bitcoin as a safe-haven asset.

Indeed, short-term traders on Deribit appear to be anticipating further downside in the near term, so they are hedging the implied volatility premiums for options below the strike price. Interestingly, however, for longer-dated options expiring in June 2024 and beyond, these premiums are skewed to the upside. We believe this reflects broader cyclical sentiment, and we appear to be far from a cyclical peak, but there is risk of further downside in the near term.

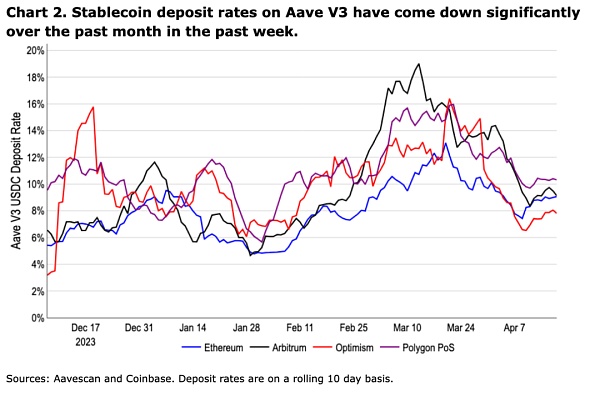

Leverage measures on-chain also reflect this positioning. The stablecoin deposit rate on Aave has fallen by more than 50% from its peak in March, but remains above this year’s lows in late January 2024. We believe this suggests that traders still retain some leverage (and are therefore constructive in the long run), but have reduced their position risk somewhat in order to take advantage of short-term downside.

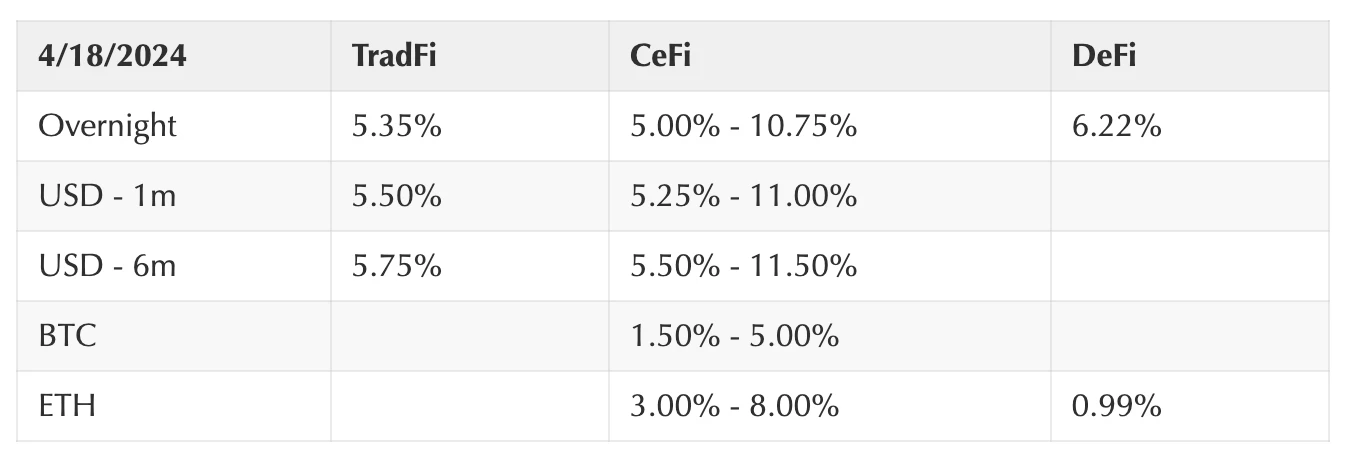

Crypto and Traditional Financial Data

(As of 4 p.m. ET April 18)

Source: Bloomberg

Coinbase Exchange and CES Insights

Volumes picked up over the weekend and remained elevated during the week. On Saturday and Sunday, traders focused on geopolitical uncertainty. This focus quickly shifted mid-week after Jerome Powell hinted that interest rates could remain higher for longer, giving the market another reason to sell. Together, these events were enough to clear most leverage from the market and bring funding rates close to zero for both BTC and ETH. While lower leverage is constructive for the market, we are entering a seasonally difficult period and it remains to be seen if prices can hold firm here. We are seeing near-equal liquidity for majors and altcoins from trading desks.

Coinbase platform transaction volume (USD)

Coinbase platform transaction volume (asset ratio)

Funding Rate

Notable Crypto News

mechanism

Web3 Investments Grow 55% in Q1 as Crypto VC Interest Rebounds (CoinTelegraph)

Hong Kong spot Bitcoin ETF may be launched as early as this month (The Block)

Supervision

Tether and Circle disagree on how to address global jurisdiction of stablecoin rules (Coindesk)

conventional

Runes will help Bitcoin DeFi close the gap with Ethereum and Solana (Decrypt)

Coinbase

Coinbase Derivatives has successfully launched Bitcoin Cash and Litecoin futures contracts and is preparing to launch Dogecoin futures later this month (Coinbase blog)

global vision

Europe

EUs MiCA rules will have little impact on European Crypto market, regulator says (Coindesk)

The UK will enact new legislation on stablecoin and cryptocurrency staking, trading and custody by June or July this year (Coindesk)

Germanys largest federal bank, Baden-Württemberg State Bank, plans to start providing cryptocurrency custody services in cooperation with Bitpanda exchange (Bloomberg)

Barclays, Citigroup, Other Banks Testing Tokenized Deposits in the UK (Bloomberg)

Asia

Hong Kong approves first spot Bitcoin and Ethereum ETFs in push to become crypto hub (The Block)

Hong Kong-based First Digitals $3 billion in stablecoins moves to Sui Network to boost DeFi (Coindesk)

RBA suggests Australians won’t value privacy or security of retail CBDC (Cointelegraph)

Vietnam has not banned cryptocurrencies, says Ministry of Justice official, calls for legal framework to be established (VNExpress)

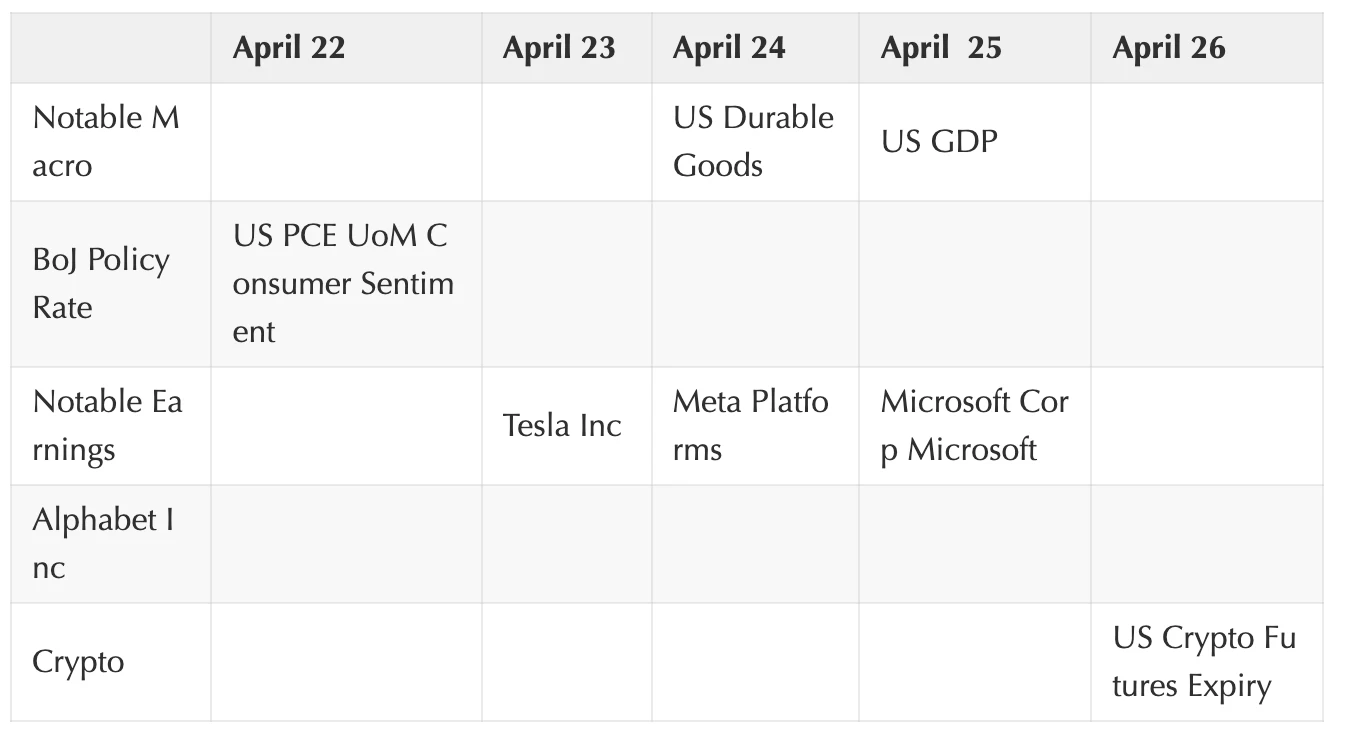

Big events in the coming week