Original | Odaily Planet Daily ( @OdailyChina )

Author: Azuma ( @azuma_eth )

Ethereum (ETH) has been at the center of market discussion recently.

From Vitalik’s own remarks on DeFi, to his personal selling actions, and the many criticisms surrounding the entire Ethereum Foundation, ETH seems to be facing the most negative market sentiment since The DAO incident.

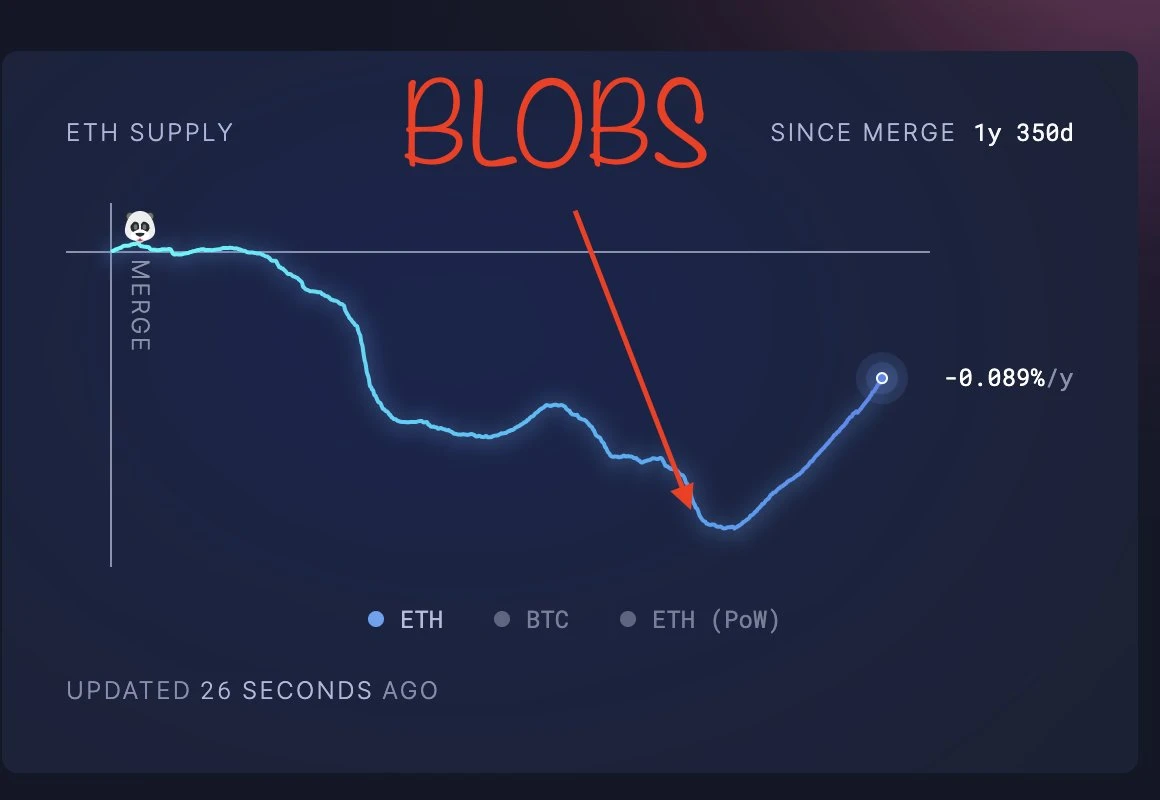

In the following article, we will not focus on these relatively subjective topics, but hope to discuss another objective numerical issue that has been put on the table - since the Cancun upgrade, ETHs long-term deflationary trend since the Merge has been reversed. If the current trend continues, ETHs supply may return to the level of the Merge two years ago within a few months and continue to inflate.

In the view of some market analysts, ETH’s recent inflation trend is the fundamental reason for the token’s poor performance - it has encountered a significant increase in supply while demand has not changed significantly, and the imbalance between supply and demand has led to a decline.

In recent days, many leading players in the Ethereum ecosystem (including researchers, project founders, VC representatives, etc.) have had heated discussions on this issue and have formed sharply opposing views.

Discussion Premise

To understand this debate, we need to turn the clock back to March of this year.

On March 13, Ethereum officially activated the Dencun hard fork upgrade (hereinafter referred to as the Cancun upgrade) at the Beacon chain slot height 8626176. The focus of this upgrade is EIP-4844, which will add an additional data space Blob to the Ethereum block specifically for processing L2 related transactions.

For more information, please refer to Cancun upgrade is finally here, which stocks will benefit?

Looking back, the Cancun upgrade performed quite well in reducing fees . With the introduction of Blob, the transaction fees of the L2 network were significantly reduced, and as L2-related transactions that were squeezed in the calldate with ordinary transactions were moved to Blob, the transaction fees of the Ethereum mainnet itself also decreased to a certain extent. This was originally a happy thing, but as time went on, some observers found that the supply trend of ETH had changed - from deflation to inflation.

The reason for this situation is that Ethereum has introduced a supply adjustment mechanism of directly destroying part of the transaction fees since the implementation of EIP-1559 three years ago , in order to permanently reduce the ETH in circulation and reduce Ethereums inflation level.

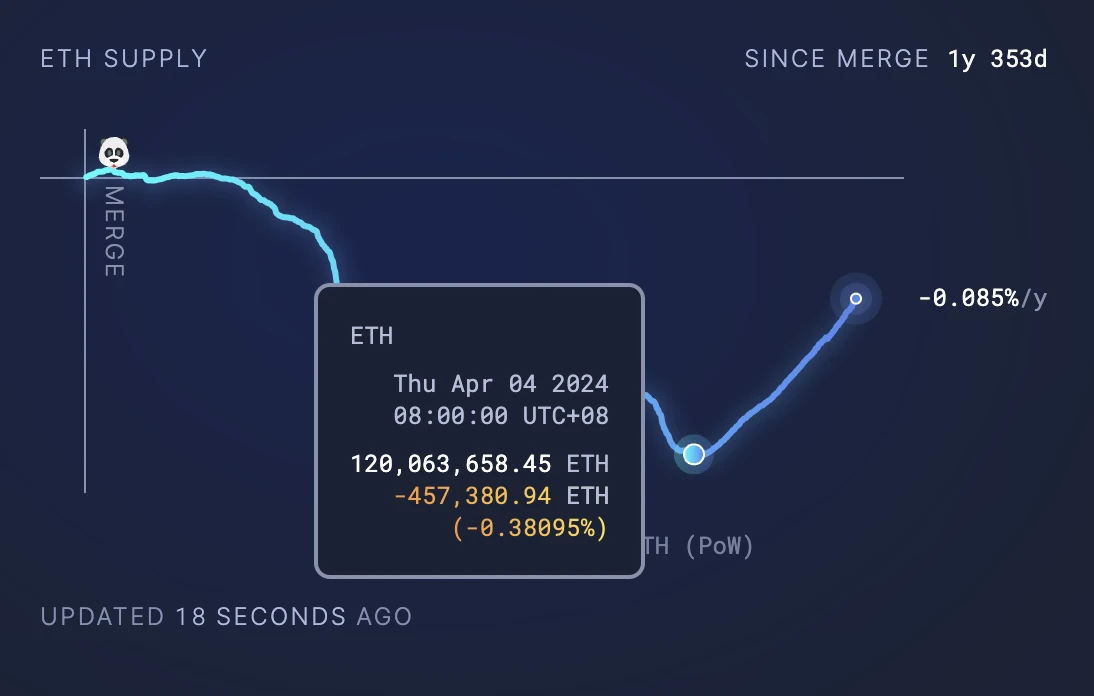

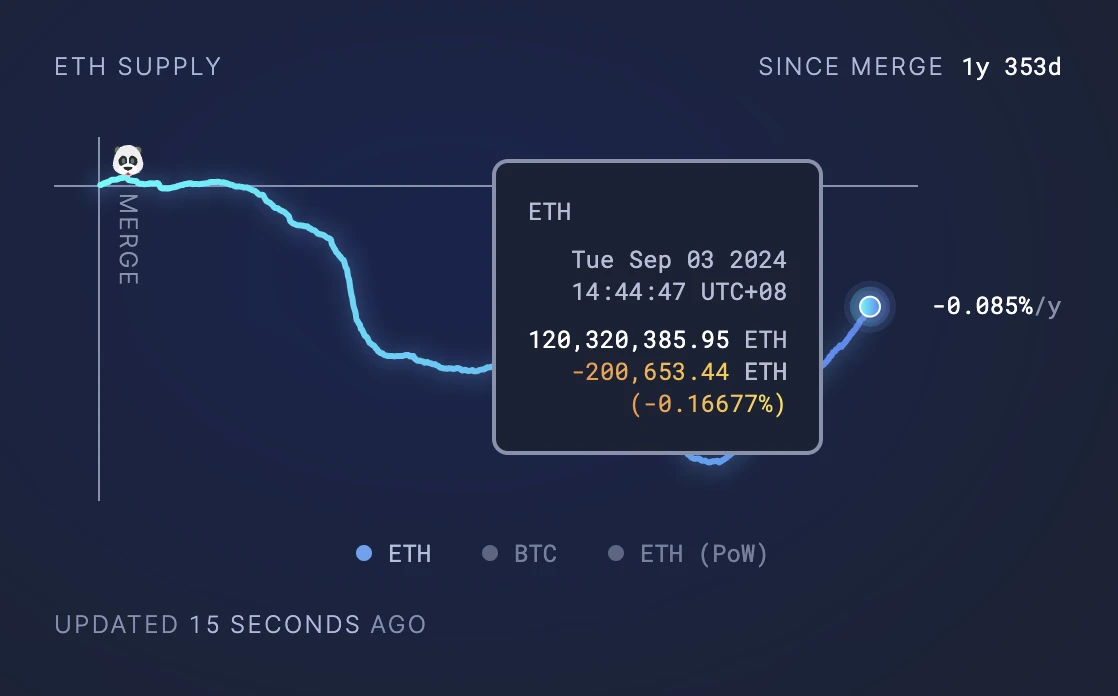

According to ultrasound.money data, in early April this year (shortly after the activation of the Cancun upgrade), the net deflation of ETH (with Merge as the reference standard) once reached a peak of about 457,000, but due to the introduction of Blob, the transaction fees of L2 and L1 have been significantly reduced. Since then, the number of ETH destroyed has dropped significantly, and the net deflation has shrunk to about 200,000 - This means that the supply of ETH has increased by more than 250,000 since the upgrade.

As of the time of writing, based on data from the past 30 days, it is estimated that ETH may issue 944,000 more coins within a year, but only 151,000 coins can be destroyed. After comprehensive calculation, ETH is already in a state of inflation, and the implemented inflation rate is 0.66%.

Combining the above data, we can intuitively conclude that, at least in the past six months, the emergence of Blob has reversed ETHs long-term deflationary trend. Based on this background, the market discussion focuses on whether this trend will continue? Does the DA service (Blob) have a value-added effect on ETH? Can the growth of L2 transactions drive the increase in Blob demand, and then push ETH back to a deflationary state?

Affirmative view: Wait for the turning point

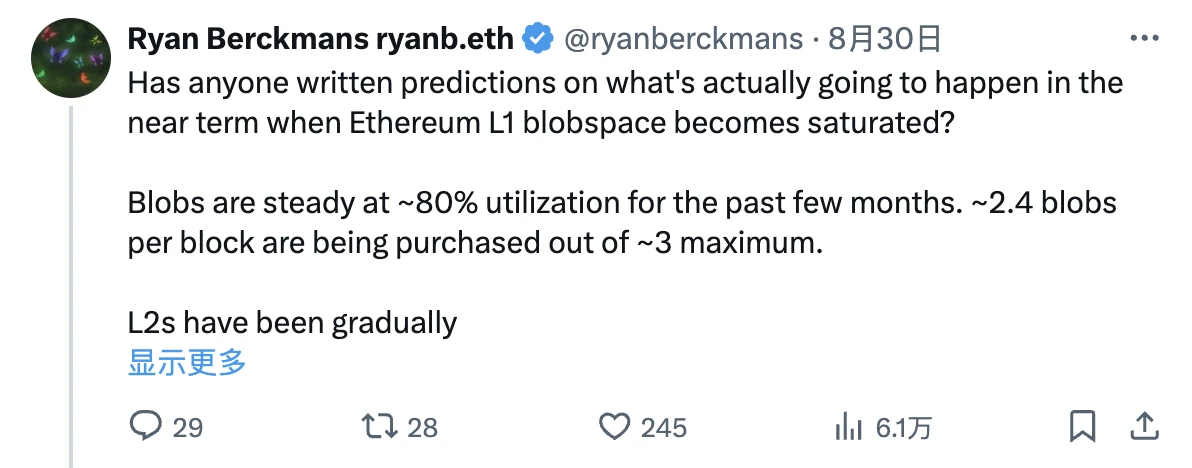

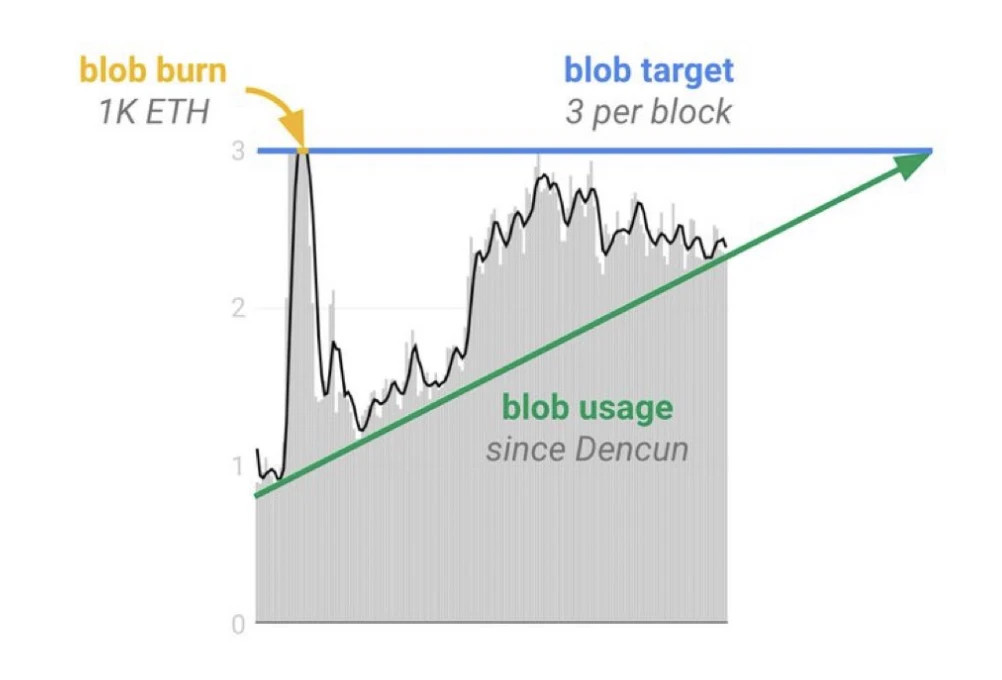

In this debate, Ethereum ecosystem investor Ryan Berckmans can be regarded as a representative of the affirmative side. His core point of view is: the current utilization rate of Blob is not saturated, but with the increase in L2 demand, after Blob is saturated, the market will bid for the limited Blob space, thereby increasing the proportion of Blob fees and then increasing the amount of destruction, pushing ETH back to deflation.

In a recent X article, Ryan mentioned that Blob utilization has stabilized at around 80% over the past few months, with each block purchasing approximately 2.4 blobs (up to a maximum of 3); at the same time, L2 itself is constantly improving Blob utilization efficiency.

Therefore, Ryan believes that although the demand for Blob has not increased significantly in absolute terms (the utilization rate remains at around 80%), this does not necessarily represent the actual situation, because the growth may be offset by the ongoing efficiency optimization of L2. From the results presented on the L2 beat data website, the demand above L2 has also maintained a good growth trend.

Based on this background, when the demand for L2 continues to grow and drives the utilization of Blob further, the limited supply of Blob will lead to L2 bidding, which will help drive the growth of fee income of Ethereum mainnet. In the long run, the fee income from DA (i.e. L2 Blob bidding) may even exceed the regular L1 income (i.e. the ordinary transaction execution fee on Ethereum).

Counterpoint: Value cannot flow back to L1

In response to Ryans views, Doug Colkitt, founder of DeFi protocol Ambient, gave a completely different opinion.

In the X article, Doug mentioned that many people hope to see the demand for Blobs continue to grow and achieve supply saturation, thereby reversing the ETH inflation trend after the deployment of EIP-4844. However, this may not be achieved because the saturation of Blobs is unlikely to lead to any substantial increase in the amount of ETH destroyed.

Doug explained that most marginal transactions on L2 are junk transactions with low amounts. If Blob reaches saturation and enters bidding mode, the transaction costs on L2 will inevitably increase significantly. Marginal transactions are often extremely sensitive to prices, so the increase in Blob costs will indirectly lead to a sharp decrease in small transactions on L2.

Doug went on to say that unless there is a surge in the number of L2 transactions with relatively large amounts, the growth in demand for Blobs will not drive the growth of ETH destruction, and thus will not be able to change the current inflation trend. As it stands, Ethereum will not be able to accumulate value for the mainnet through DA (Blob fees) in the foreseeable future.

Compared to who is right or wrong, the discussion itself may be more important

Just as few people could predict the changes in ETH supply before the Cancun upgrade, no one can give a conclusion yet on whether ETH supply will see new changes after Blob supply is saturated.

It should be emphasized that this article only focuses on the proposition of whether the growth of Blob demand can lead to changes in ETH supply. Whether changes in ETH supply are a factor affecting the price of the currency is another proposition. From the perspective of project development, under the premise that Blob can provide effective expansion, there is controversy over whether low fees + inflation or high fees + deflation is better or worse. In addition, after the saturation of Blob supply, the increase in operating costs and the internal changes of the L2 track are also subject to many uncertainties.

Ryan speculates in his article on some potential changes within the L2 circuit:

Will some L2s be forced out of business due to rising Blob costs?

Will there be an L2 shift to the validium solution?

Will there be L2s that move to L3 and share blob space with some other larger L2?

If Blob fees increase, how much would be a reasonable increase?

What proportion of the cost is expected to be?

If Blobs are too expensive, will there be an L2 fallback to using calldata?

… These are all unresolved issues that have not yet been fully discussed.

Doug also mentioned in his article that his point of view is only to refute the statement of some people that ETH will soon return to a deflationary state, but he does not know which situation is correct.

Some people believe that the Ethereum network should view L2 like a fast-growing startup, and view low-income DA services as a strategy to gain market share by losing money, and then consider profitability after the share grows. Others believe that Ethereum may never need to make a profit through L2, but should reach more user groups through L2 and make ETH a monetary asset.

These topics all require further exchanges of ideas. Perhaps compared to the result of whether the growth in demand for Blobs can trigger changes in ETH supply, the discussion around the current status and trends itself is more valuable.