Original author: Will Awang

Original source: Web3 Lawyer

From ancient times to the present, shells, chips, cash, deposits, e-wallets, etc. are all carriers or forms of expression of currency. These carriers and forms of expression are constantly changing in line with the times, just like the digital currency form derived from blockchain technology in todays digital economy era, and the Web3 payment ecosystem built on this basis.

As the latest currency carrier or form of expression, stablecoins have spread to all aspects of ordinary users financial lives after being initially used as collateral or medium of exchange for crypto assets. With the rise of stablecoins in the past five years and their continuous penetration into the global economy, the endowment of blockchain as a financial infrastructure will inevitably be explored and fully utilized by the traditional financial world outside the crypto market.

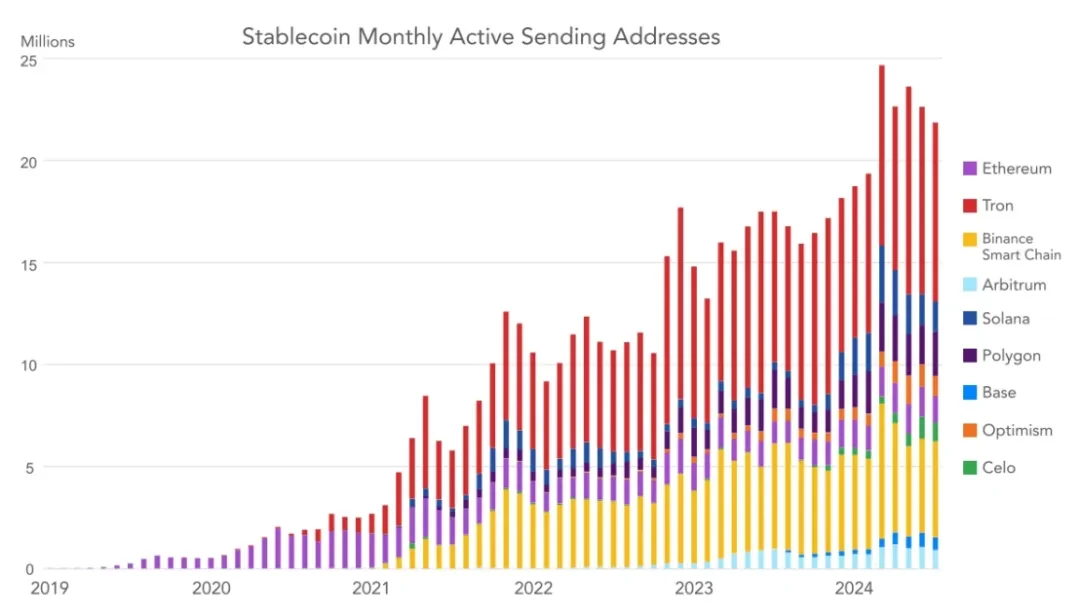

VISAs stablecoin report provides us with the following data: The total supply of stablecoins is about $170 billion. They settle trillions of dollars worth of assets every year. About 20 million addresses on the chain conduct stablecoin transactions every month. More than 120 million addresses on the chain hold non-zero stablecoin balances. These figures all show that stablecoins are a currency that runs parallel to traditional financial infrastructure - it just started from close to zero five years ago.

Therefore, we can no longer limit our vision to the use cases of stablecoins in the native crypto market, but should look at the use cases of stablecoins in non-crypto native scenarios from a completely new perspective. Who is using stablecoins? What are they used for? How has it penetrated our global economy, used for remittances, cross-border payments, international trade settlements, and regarded as a savings tool for ordinary people?

VISAs stablecoin report is of great significance. So far, research on cryptocurrency adoption has mainly focused on general cryptocurrency penetration, and no survey has been conducted specifically on stablecoin adoption and use cases. In particular, research on use cases in non-native crypto markets will have a profound impact on the traditional financial payment system and indicate the future development path of Web3 payments.

In the report, VISA starts with on-chain data on the widespread use of stablecoins and conducts in-depth surveys of recognized crypto users in five major emerging market economies (Brazil, India, Indonesia, Nigeria, and Turkey). In addition to on-chain data and survey results, VISA also provides in-depth insights into companies that actually operate in these markets. Together, these on-chain data, survey data, and qualitative local insights provide us with a panoramic view of global stablecoin usage to fully understand the use of stablecoins around the world, with a particular focus on the use of stablecoins for non-crypto purposes, such as remittances, cross-border payments, payroll, trade settlements, and B2B transfers.

Full report from VISA: Stablecoins: The Emerging Market Story

https://castleisland.vc/writing/stablecoins-the-emerging-market-story/

1. Why VISA?

Money is not coins, cash or credit cards, which are just forms, not functions. The function of money is usually a tool for measuring equal value and a medium of exchange. Money will become a digital representation of letters, and it will move around the world at the speed of light through infinitely different paths at minimal cost. - Dee Hock, founder of VISA.

When Dee Hock founded VISA more than fifty years ago, the original vision was to be more than just a card network; he wanted VISA to be the world’s foremost exchange of electronic value, regardless of the form of value or the underlying technology.

Although Dee Hock passed away in 2022, many of his thoughts and expressions are so profound and have transcended history. Every change in the carrier or form of currency will also be accompanied by huge changes, just like the digital currency form derived from blockchain technology in todays digital economy era, and the Web3 payment ecosystem built on it. This also guides VISA, a global financial infrastructure company, to explore new value circulation paths.

VISA believes that stablecoins are a payment innovation that has the potential to provide safe, reliable and convenient payments to more people in more places. Thinking about how to incorporate digital currency/payment forms derived from blockchain technology into VISAs territory is more about how VISA can enter the game and find its own ecological positioning.

VISA currently provides technology services that enable consumers, merchants, financial institutions, fintech companies and governments to securely transfer value around the world. VISA has more than 4.5 billion credit cards worldwide, and its products cover more than 130 million merchants, approximately 14,500 financial institutions and more than 200 countries and regions. In the past year alone, VISA facilitated more than 296.8 billion transactions and $15.5 trillion in transaction volume.

Today, VISA supports more than 50 wallet partners, enabling users to quickly and securely pay with VISA cards at more than 130 million merchants worldwide. VISA is also piloting the use of stablecoins such as USDC to expand the settlement capabilities of global issuers and acquirers, providing greater flexibility for fund management.

2. Overview of the Stablecoin Market

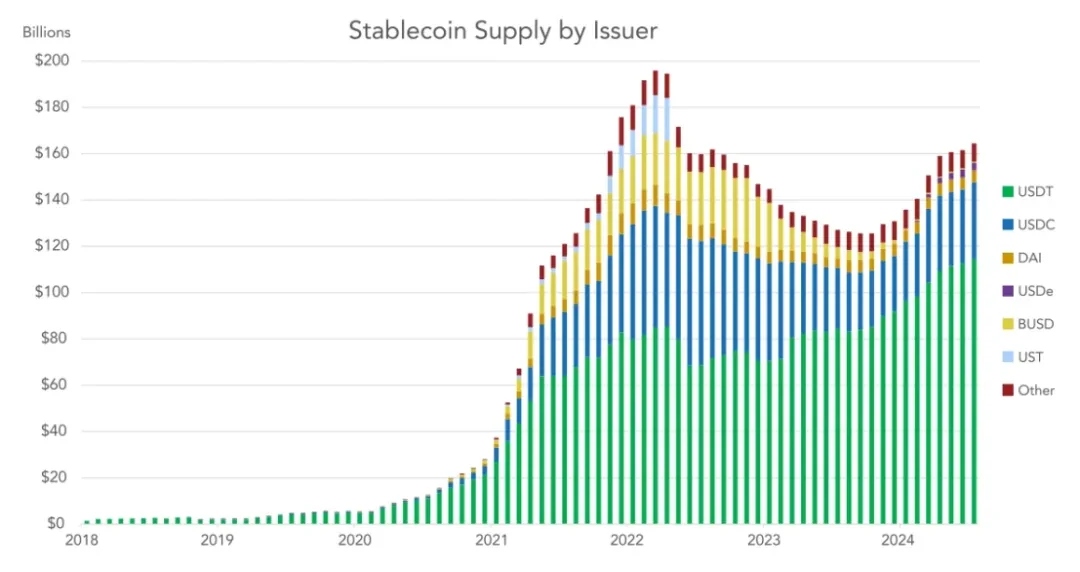

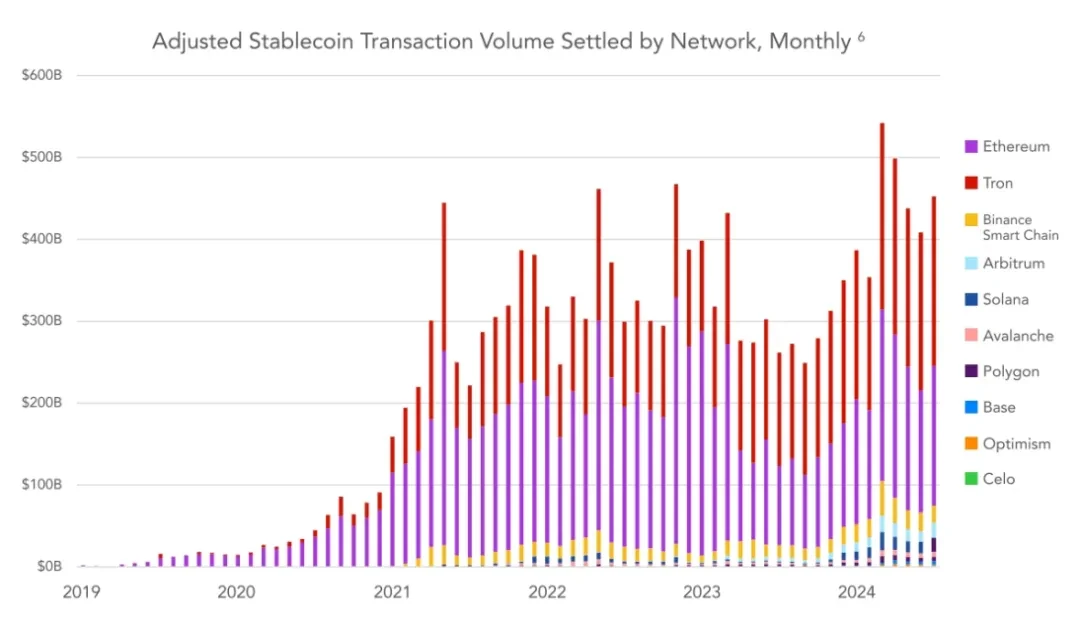

Stablecoins, as tokenized representations of fiat currencies circulating on blockchains, are undoubtedly the killer app of the crypto market so far. There are currently more than $160 billion in stablecoins in circulation, far higher than the billions in 2020. More than 20 million addresses trade stablecoins on public blockchains every month. In the first half of 2024, the value of stablecoin settlements exceeded $2.6 trillion.

Stablecoins have significant advantages over existing payment systems, including open and transparent ledgers, instant settlement, self-custody of funds, on-chain programmability, and interoperability. Although stablecoins were initially used by traders and cryptocurrency exchanges as collateral or medium of asset trading, they have now broken through the circle and have been widely adopted in the global economy.

Today, global users value the ability to hold fiat currencies directly themselves (primarily USD stablecoins) rather than relying on unreliable or inaccessible bank accounts. Stablecoins are also used for cross-border payments, wages, trade settlements, and remittances. There are also a growing number of stablecoin-based yield products, either as interest-bearing stablecoins themselves or through decentralized DeFi protocols. In emerging markets, the adoption of stablecoins for payments, currency substitution, and access to high-quality yield forms is accelerating.

Based on the differences between stablecoin activity and crypto market cycles, it is clear that stablecoin adoption has expanded beyond just serving cryptocurrency users and asset trading use cases.

If stablecoins were used simply as a form of settlement between traders and crypto exchanges, then stablecoin settlement volume, transaction counts, and monthly active addresses should be largely correlated with crypto market cycles. However, the sluggish performance of crypto exchange trading volumes in 2022-2023 suggests that stablecoins have real-world uses beyond pure speculative purposes.

Stablecoins have indeed seen growth in non-crypto transactional uses, especially in emerging markets. They are used for currency substitution (to escape volatile or depreciating local currencies), as alternatives to dollar-based bank accounts, for B2B and consumer payments, to access various forms of yield products, and for trade settlements.

Stablecoins are particularly attractive when U.S. dollar banking is non-existent or difficult to obtain, in countries with high inflation, and in countries where a fiat financial system is lacking.

3. On-chain stablecoin data

The following is a data panel provided by VISA, which you can study if you are interested:

https://visaonchainanalytics.com/transactions

3.1 The stablecoin market is growing year by year

The total supply of stablecoins has grown rapidly since 2017, when total stablecoins in circulation were still below $1 billion. The total supply of stablecoins peaked at approximately $192 billion in March 2022, before Terras UST collapsed and the credit crunch, which suppressed crypto-native interest rates, depressed crypto trading volumes, and hurt the balance sheets of crypto-native companies. After the credit crisis largely subsided, stablecoin supply began to recover in December 2023 as major crypto assets began to rise ahead of the approval of a Bitcoin ETF in the United States.

In recent months, a variety of new forms of stablecoins have emerged as various regulators have passed clear stablecoin legislation in the hope of attracting issuers. Some of the most active jurisdictions in developing stablecoin regulatory frameworks include the European Union, Singapore, Dubai, Hong Kong, and Bermuda.

As crypto-native and sovereign interest rates rise, certain stablecoin issuers are beginning to experiment with models that pass yields on to holders, either through on-chain programming or through third-party revenue-sharing arrangements. The presence of programmable (and in some cases permissionless) yields in stablecoins — whether crypto-native or based on U.S. Treasury securities — adds a new value proposition for end users who do not have easy access to U.S. dollar money market funds.

3.2 Data needs to be corrected and adjusted

The on-chain stablecoin data clearly shows the trend of stablecoins continuing to grow. However, on-chain data is usually overestimated and needs to be de-noised and carefully interpreted.

VISA extends existing methods to estimate the total settlement volume of stablecoins. Nominal (total) figures are not reliable estimates of settlement volume because the nature of blockchains and how certain agents (exchanges, mixers, and various robots) use them can lead to significant overestimation, causing settlement volume to be inflated by an order of magnitude. Therefore, a lot of noise removal work must be done.

Adjusted settlement volume remains a difficult number to estimate, and there is no definitive “ground truth” – only projections and best guesses. VISA does not consider its own estimates authoritative.

Based on the adjustments, VISA estimates that the total settlement amount of stablecoins in 2023 will be conservatively estimated at US$3.7 trillion, US$2.62 trillion in the first half of 2024, and the total settlement amount for the whole year of 2024 is expected to be US$5.28 trillion.

Notably, despite the sell-off in crypto assets and declines in exchange volumes in 2022 and 2023, stablecoin settlement volumes have been growing steadily throughout the market cycle.

This again shows that stablecoins have attracted a new group of users who are interested in using them for more than just exchange settlements. As of June 2024, the most popular blockchains by settlement value are Ethereum, Tron, Arbitrum, Base, BSC, and Solana.

The growth of monthly transfer addresses has been similar or even more stable. VISA prefers this metric to transaction counts because it is generally more resistant to manipulation (but not completely impervious to manipulation).

The most popular blockchains for stablecoin transfers are Tron, BSC, Polygon, Solana, and Ethereum. Ethereum generally has a higher fee burden, which means that there tend to be fewer addresses and transaction volumes than Tron or BSC, but Ethereum still leads in terms of value settlement.

3.3 Dollarization of Stablecoins

The story of the “dollarization” of blockchain emerges when stablecoin settlement volumes are compared to native crypto assets. While Bitcoin and Ethereum have historically been the dominant medium of exchange on public blockchains, stablecoins — and those almost exclusively pegged to the U.S. dollar — have steadily gained market share. Today, stablecoins account for approximately 50% of all value settled on public blockchains, having reached 70% in the past.

Stablecoins remain closely tied to the U.S. dollar. The second most popular currency used in stablecoins is the euro, which has a supply of $617 million as of June 2024, or 0.38% of the entire stablecoin market. While there are stablecoins using the lira, Singapore dollar, yen, and several other fiat currencies, there are no stablecoins in any currency other than the U.S. dollar or euro that have more than $100 million pegged to them.

In practice, this means that when individuals in emerging markets use stablecoins pegged to the U.S. dollar, they are indirectly purchasing U.S. debt instruments, such as short-term Treasury bills. Regulators in some countries with high cryptocurrency penetration, including Nigeria, which was implicated in the VISA survey, are concerned that their local currencies could be at risk if cryptocurrency dollarization continues unabated.

Why stablecoins are so overwhelmingly dollarized remains an interesting question. The U.S. dollar is the global reserve currency, but in no other usage category is the dollar as dominant as it is in stablecoins.

Stablecoins referencing alternative currencies have been around for years but have yet to gain traction. The overwhelming dominance of the U.S. dollar in the stablecoin space likely reflects the fact that most states have not set up any local barriers to the use of U.S. dollar stablecoins, and users simply prefer the most liquid tokens, such as USDT and USDC. In addition, the strength of the U.S. dollar against most other sovereign currencies remains a motivation for cryptocurrency users to favor dollar-pegged stablecoins, even outside the United States. It remains to be seen whether regulation will hinder U.S. dollar stablecoins and encourage the growth of local currency-backed stablecoins.

IV. Emerging Market Survey Report

However, despite these observations, the prevalence of non-crypto use cases among emerging market stablecoin users has not been quantified to date. Therefore, VISA conducted a study of crypto users in five major emerging market countries (Brazil, India, Indonesia, Nigeria and Turkey) to better understand the frequency of stablecoin use and the ways in which emerging market users use these tools.

VISA surveyed approximately 500 people in each of Nigeria, Indonesia, Turkey, Brazil, and India, for a total sample of 2,541 adults. The general picture from the survey data is of increasing adoption of stablecoins, more frequent transactions, significantly higher portfolio penetration, and heterogeneous stablecoin usage beyond pure cryptocurrency trading use cases.

Key findings:

While the top motivation for using stablecoins is to acquire cryptocurrencies (50%), acquiring USD (47%), yield generation (39%), and non-crypto uses are also popular motivations;

Stablecoins are preferred over USD banks due to benefits, efficiency, and lower likelihood of government intervention;

57% of users reported an increase in stablecoin usage over the past year, and 72% believe they will increase their stablecoin usage in the future;

In the case of Tether being preferred, the main reason reported was its network effect, followed by user trust, liquidity, and track record relative to other stablecoins;

Among non-transaction use cases, currency conversion (converting to USD) was the most reported activity, followed by paying for goods, cross-border payments, and paying or receiving salary;

Ethereum is the most popular blockchain among sampled users, followed by BSC, Solana, and Tron;

The most popular wallet among respondents is Binance, followed by Trust Wallet, Metamask, Coinbase Wallet, Crypto.com, and Phantom Wallet.

4.1 Types of Stablecoin Activities

VISA is most interested in determining the goals of users using stablecoins. Although stablecoins were initially seen as collateral for exchanges and a means of transaction settlement, the usage patterns and use cases have expanded.

The most popular goal for stablecoin users in the sample was to trade cryptocurrencies or NFTs, but other non-cryptocurrency uses were not far behind. Overall, 47% of respondents said one of their main goals was to save dollars, 43% mentioned better currency conversion rates, and 39% said to earn a yield.

The findings are clear: non-cryptocurrency uses account for a large portion of stablecoin usage patterns across the countries surveyed.

By far the most popular use case was currency exchange, followed by shopping and cross-border transactions. Notably, the majority of respondents in all countries in the sample said they had used stablecoins for non-cryptocurrency transaction use cases. Stablecoin usage is growing in all countries surveyed. The majority of respondents said their usage had increased over the past year, with an even larger percentage saying they would increase their usage further in the coming year.

4.2 Penetration of Stablecoins

Regarding the penetration of stablecoins in user portfolios. At the national level, Nigerians have a much higher proportion than other groups in the sample, followed by Turkey and India. In the Indian user sample, respondents in the wealthiest group also said that their financial portfolios have a larger proportion of stablecoins.

Findings by country:

VISA found that Nigerians had the highest affinity for stablecoins among all countries surveyed — much higher than any other country. Nigerians had the highest transaction frequency, stablecoins made up the largest portion of respondents’ portfolios, reported the highest percentage of non-cryptocurrency transaction uses for stablecoins, and had the highest level of self-reported knowledge of stablecoins.

Interestingly, the main goals of stablecoin users vary by country. Across the entire sample, cryptocurrency trading was the most common goal for stablecoin users, but there were differences by country. In Turkey, the most common goal was to obtain yield, followed by cryptocurrency trading. For Indonesians, better currency exchange rates, followed by cryptocurrency trading and USD savings. For Nigerians, USD savings was the top goal, followed by cryptocurrency trading and obtaining better currency exchange rates.

The countries with the most active stablecoin use in the sample are Nigeria, India, Indonesia, Turkey and Brazil. In terms of stablecoin portfolio share, Nigeria once again stands out (with a significant lead), followed by India, Turkey, Brazil and Indonesia.

VISA also categorized respondents into different income brackets to understand the role affluence plays in stablecoin adoption. However, given the uneven sampling of income brackets in most countries in the sample, VISA could only produce useful results for India. The results for India by income bracket are quite clear: wealthier respondents have greater stablecoin penetration in their portfolios, they are more inclined to use stablecoins for a wider range of use cases, including non-crypto use cases, and they are more likely to trust stablecoins over bank accounts.

Survey results by age:

Overall, the results by age are consistent with expectations: Younger people use stablecoins at a higher rate. Younger people are more likely to have tried multiple different stablecoins and hold a higher share of stablecoins in their overall financial portfolio.

While there are no clear age differences in most usage categories, younger people are more likely than older respondents to use stablecoins to save in USD, convert local currency to USD, and enter the crypto economy. Younger age groups use stablecoins more frequently across all non-crypto use cases: paying for goods/services in stablecoins, sending remittances, and receiving wages in stablecoins.

Among respondents who said they exchanged their national currency for stablecoins, 34% of younger people (18-24 years old) did so weekly and 38% monthly, compared to only 15% of the oldest respondents (55+) weekly and 46% monthly. Younger respondents also expressed greater trust in stablecoins compared to U.S. dollar-denominated bank accounts.

4.3 Tether’s preference for USDT

Tether is widely considered the most popular stablecoin among users in emerging markets. VISA wanted to understand its enduring advantages. Users most often reported that they preferred Tether due to network effects, followed by greater trust in it, and that Tether maintained the best liquidity.

As for which blockchain networks users prefer (if any), and which wallets they use. VISA surprisingly found that Ethereum is the most popular blockchain network in all regions, followed by BSC, Solana, and Tron. This was unexpected because Ethereum fees have always been too high for smaller retail payments.

VISA also lets users choose whether to trade only on exchanges (some exchanges allow users to make peer-to-peer transfers, with transactions settled on their internal ledgers). 18% of the sample admitted to transferring stablecoins in this way. This trend toward using exchanges directly rather than blockchains was also evident in VISA’s questions about wallets.

The most popular non-custodial wallets are Trust Wallet, MetaMask, and Coinbase Wallet. Half of all respondents said they use Binance as a wallet, more than any other non-custodial wallet. Notably, 39% of Nigerians surveyed admitted to using Phantom Wallet (primarily Solana client).

5. In-depth insights from market players

These practical players who have penetrated into emerging markets have made the data no longer cold, and presented us with real and vivid use cases of stablecoins. Although we may find it difficult to understand in developed countries, this is a real demand.

5.1 Mountain Protocol — Interest-bearing Stablecoin

Mountain Protocol is the first state-regulated (Bermuda) and permissionless issuer of an interest-bearing stablecoin. Due to its yield-earning nature, USDM is more suitable for use where there is working capital.

This can include serving as collateral for reinsurance policies, such as those issued by Nayms, where real-world risks are covered by crypto collateral.

Another use case is as collateral for loans. In most emerging markets, banks are reluctant to issue unsecured loans to businesses and want collateral. However, borrowers do not want to have USD in the local banking system due to trust risks in certain jurisdictions. Companies like Aconcagua solve this problem by storing USDM in a multi-signature contract, acting as an escrow agent, and allowing banks to issue such loans in a secured form, thereby expanding credit capacity.

Finally, remittance companies are converting their working capital into USDM.

This shift is still in its early stages as accepting USDT is still king. With interest-bearing stablecoins, these companies can increase profitability by holding yielding assets.

5.2 Bits — Cryptocurrency Exchange

Bitso is a cryptocurrency exchange with official offices in Argentina, Brazil, Colombia, and Mexico. According to Bitsos Crypto Trends Report, Bitcoin and stablecoins dominate purchases in Latin America, showing that Bitcoin remains the preferred cryptocurrency among users. However, digital dollars also have an important place in the portfolios of ordinary users, and stablecoins were the fastest growing cryptocurrency last year.

Why stablecoins are attractive to users in emerging markets:

Latin American users prefer the sense of stability that comes with assets pegged to strong fiat currencies, as inflation and exchange rates in Argentina and Colombia are highly volatile.

While retail users of the platform still buy Bitcoin more frequently than stablecoins in Mexico, the use of stablecoins for remittances is growing in importance and appeal among remittance companies, which are turning to stablecoins for cost-effective and fast cross-border payments, leveraging regulated providers such as Bitso.

Using stablecoins can bring the following benefits:

Stablecoins offer multiple benefits for cross-border payments. They eliminate intermediaries, making transactions more transparent, efficient, and cheaper.

Stablecoins offer advantages over traditional cross-border payment systems, which can take days, are costly, opaque, and have limited accessibility. One of the reasons for these inefficiencies is that multiple intermediaries and currencies are involved in the process, which increases fees and delays. Stablecoins allow cross-border payments to be completed in a more cost-effective manner, in just minutes, any day of the week.

For digital companies that use the U.S. dollar as their settlement currency, stablecoins provide a valuable hedge. Businesses operating in multiple countries benefit from stablecoins to manage cash flows in different currencies and to pay international employees, customers or suppliers.

Investors are also attracted by the opportunity to earn yield, with Bitso offering up to 4% on stablecoins. In addition, cryptocurrencies are increasingly used in daily transactions and as a means of payment. As the advantages of stablecoins become more widely recognized across different industries, their use in cross-border payments is expected to increase significantly.

5.3 Pintu — Cryptocurrency Trading Platform

Pintu is one of the largest cryptocurrency platforms in Indonesia, offering a variety of fiat-backed stablecoins pegged to the US dollar, euro, and rupiah.

Why users prefer stablecoins:

Most retail users primarily use stablecoins for cryptocurrency and trading use cases, including but not limited to accessing Web3 platforms and global exchanges and finding arbitrage opportunities.

Other use cases used by a subset of users, typically OTC clients (high net worth individuals and corporates), include B2B payments and arbitrage.

Efficiencies gained from using stablecoins compared to other financial instruments:

For many Indonesian users, stablecoins are more accessible than U.S. dollar banks. Registration requirements for local cryptocurrency exchanges are simpler than those for creating a U.S. dollar bank account, so users have a lower barrier to entry.

Users can exchange IDR for stablecoins and vice versa around the clock, while some local banks’ platforms only allow users to exchange IDR for other foreign currencies during banking hours.

Many local banks and money changers have minimum and maximum amount limits for foreign exchange transfers, while Indonesian users can trade from/to stablecoins through cryptocurrency exchanges at prices starting at $1 with almost no maximum amount limits.

Most common usage patterns:

Pintu users can use stablecoins to earn interest through the Pintu Earn feature. Pintu Earns yields range from 2.5% to 6%, while local banks typically offer less than 2% annual interest on US dollar deposits.

Many Pintu users use stablecoins for transaction purposes. A large portion of the total transaction value on Pintu consists of USD stablecoin transactions.

The number of on-chain transfers of USD stablecoins accounts for almost half of Pintu’s on-chain transfers, while IDRT accounts for about 10% of the total on-chain transfers.

Ethereum remains the most relied-on USD-based stablecoin on-chain transfer network for Pintu users (~50%), followed by Binance Chain (~25%), Tron (~8%), and Solana (~4%).

In terms of the number of on-chain transfers by users, USDT is more popular than USDC, accounting for more than 90% of the total.

5.4 DolarApp——Financial Application

DolarApp is using stablecoins to build a global financial app for Latin America. The most common ways users use DolarApp include receiving payments from the U.S. at the best exchange rate, paying with international cards at the best exchange rate, and dollarizing savings.

The main reason for the existence of DolarApp is that there is a huge demand for dollar-denominated financial services in Latin America, but the accessibility of dollar banking is limited. Stablecoins are attractive to the Latin American user base for the following reasons:

First, because users cannot easily access dollars. In Mexico, banks cannot offer dollar accounts to anyone who does not live within 20 kilometers of the U.S. border. In Colombia and Brazil, dollar banking is not allowed at all. In Argentina, dollar banking exists but is limited by transaction volume thresholds and uses an “official” foreign exchange rate that differs from the market rate. In countries with high inflation levels, such as Argentina or Venezuela, stablecoins allow people to save in a stable currency.

When it comes to cross-border transactions, you can’t hold a USD balance with a remitter, which means that whenever you receive a USD transfer, it is automatically converted to your local currency — making it easy for existing banks and remittance players to hide fees in large spreads. Once you have people holding USD stablecoins, they can convert them at will with full knowledge of the foreign exchange rate they are getting. The same logic applies to credit card payments.

In countries such as Brazil that impose high taxes on cross-border capital flows, stablecoins offer a more favorable tax regime than the fiat dollar.

Finally, because the restrictions of the fiat dollar do not apply to stablecoins, efficiencies are gained—both in terms of velocity of funds (e.g., staying on blue-chip bonds in Argentina for remittances) and in terms of taxation (e.g., Brazil’s IOF tax).

5.5 Felix Pago——Financial Payment Company

Felix Pago’s mission is to provide a seamless and accessible service to Latinos in the United States, making sending money to loved ones back home as easy as sending a text message. Felix Pago leverages artificial intelligence to provide a conversational platform that lets users interact with the Felix bot to send money. Felix Pago deposits fiat currency with end users, but uses stablecoins to power Felix Pago’s cross-border infrastructure.

The current cross-border infrastructure for these users is still outdated, dominated by banks or old-fashioned remittance companies, and the service is cumbersome, slow, and expensive. Felix Pago uses cryptocurrency for three reasons: first, access to the open currency platform through APIs; second, the ability to transfer funds instantly; and third, to keep costs as low as possible. But Felix Pago cannot expose the volatility risk of cryptocurrency to users, so Felix Pago chooses to use stablecoins. In general, users want reliability and credibility. This is why Felix Pago chose USDC because it is backed by US assets hosted by regulated US financial institutions and is regularly audited.

Felix Pago solves the problem that users currently want, which is to get local currency to pay for daily expenses. This makes exits in the region one of the biggest challenges for stablecoin adoption. That being said, Felix is making significant strides towards bringing more and more stablecoins to Latin America.

VI. Conclusion

In the report, VISA first demonstrated that the use of stablecoins is growing from the perspective of on-chain stablecoin data, whether measured by monthly active addresses, total supply, or settlement value. In particular, VISAs new transaction value is expected to establish stablecoins as a meaningful settlement medium, comparable to existing transfer networks, while avoiding the overestimation that has plagued on-chain data in the past.

VISAs survey results bring us a cognitive shift that stablecoins are no longer limited to tools for crypto asset investment and trading, but also have a trend of integration with the global economy. 47% of the crypto users surveyed listed US dollar savings as their stablecoin goal, 43% mentioned effective currency exchange, and 39% said it was income generation. Although gaining access to cryptocurrency exchanges remains the top use case for respondents, long-tail or ordinary (non-crypto) economic activities are also evident.

When asked about non-crypto stablecoin activity, the most popular use of stablecoins was currency substitution (69%), followed by payment for goods and services (39%) and cross-border payments (39%). It is clear that in the countries surveyed, stablecoins have evolved from being simply transaction collateral to a general digital dollar tool. In addition, the vast majority (about 99%) of stablecoins reference the US dollar.

Discussions about stablecoin regulation in the U.S. cannot ignore the fact that a large number of individuals and companies in emerging markets rely on these networks for savings, cross-border payments, remittances, and corporate cash management. In nearly all countries surveyed, these stablecoins increasingly serve as a substitute for scarce U.S. dollar banking. The potential benefits of billions of users in emerging markets efficiently accessing alternative hard currencies must have a place in discussions about the merits of stablecoins.