What on-chain derivatives protocols have you used recently?

This is almost an embarrassing footnote to the DeFi derivatives track. To be honest, if Hyperliquid, with the giant whale James Wynn as the best on-chain spokesperson, had not had the holy grail status of dYdX and GMX in the past two years, their rapid decline would have almost ended the on-chain derivatives narrative.

The reason is that they have long been trapped in the identity of CEX imitators: they copied the contract logic and leverage mechanism of centralized platforms, but carried higher risk exposure and lower user experience. There is still a clear gap with CEX in key dimensions such as liquidation mechanism, matching efficiency, and transaction depth. Until the emergence of Hyperliquid, it has reconstructed product form and user value based on on-chain characteristics, which is a rare possibility for further evolution in this track:

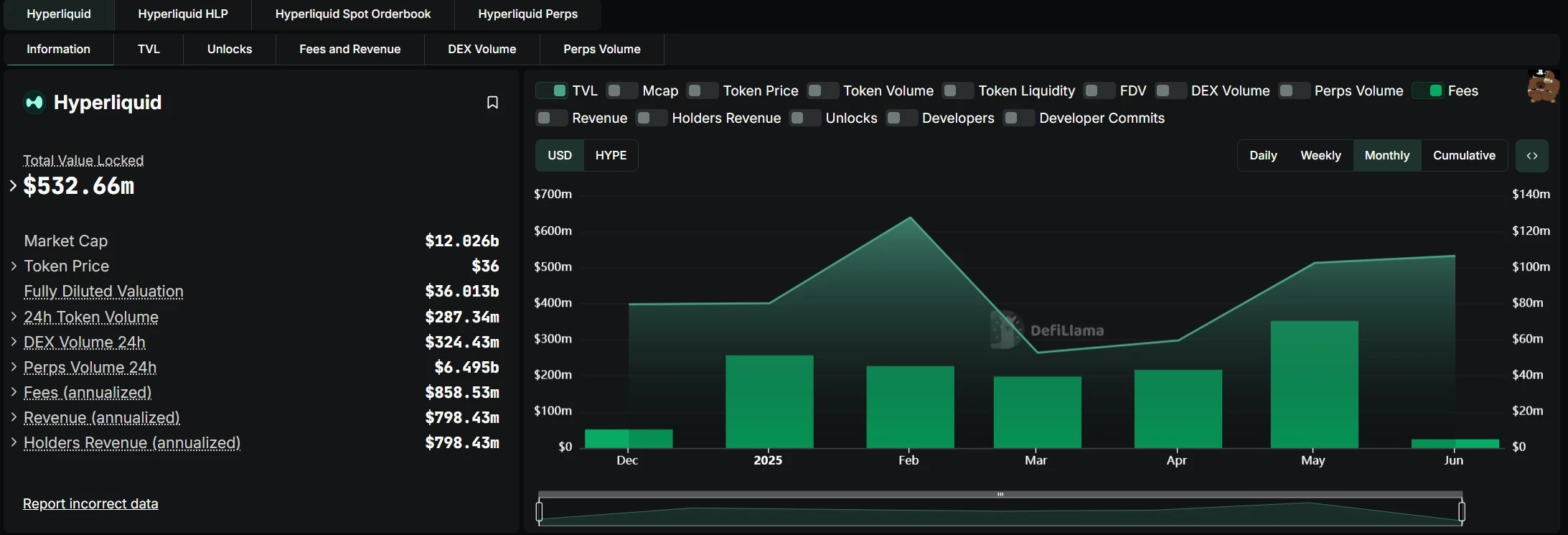

In the past May, Hyperliquid perpetual contract trading volume reached US$248.295 billion, a record high for a single month, equivalent to 42% of Coinbases spot trading volume in the same period. Protocol revenue also reached US$70.45 million, also breaking the record.

However, from a longer-term perspective, the Hyperliquid structure still follows the typical contract trading model, and has only taken the first step in the transition from optimizing “existing solutions” to exploring “native solutions”. This article also wants to delve into deeper issues from the dilemma of on-chain derivatives and the development context of Hyperliquid:

What is the next step for on-chain derivatives? Will it continue to optimize the centralized logic template, or will it move towards a more differentiated product innovation path based on the openness of the chain and the characteristics of long-tail assets?

The “New Ticket” of Decentralized Derivatives

From a data perspective, no matter how the market changes, cryptocurrency derivatives will always be a super big cake that continues to expand in size - but the knife and fork for cutting the cake are still firmly in the hands of CEX.

Since 2020, CEX has used contract futures as an entry point and gradually reconstructed the original market structure dominated by spot trading. Combined with the latest data from Coinglass, it can be found that in the past 24 hours, the 24-hour trading volume of the top five CEX contract futures has reached the level of tens of billions of US dollars, and the leading Binance has exceeded 60 billion US dollars.

If we broaden our horizons, we can more intuitively perceive the penetration of derivatives trading. For example, TokenInsight statistics show that the current daily trading volume of Binance derivatives accounts for 78.16% of the total daily trading volume of spot + derivatives (US$500 billion), and this proportion is still continuing to rise. In short, the current daily trading volume of CEX derivatives is almost 4 times that of spot trading.

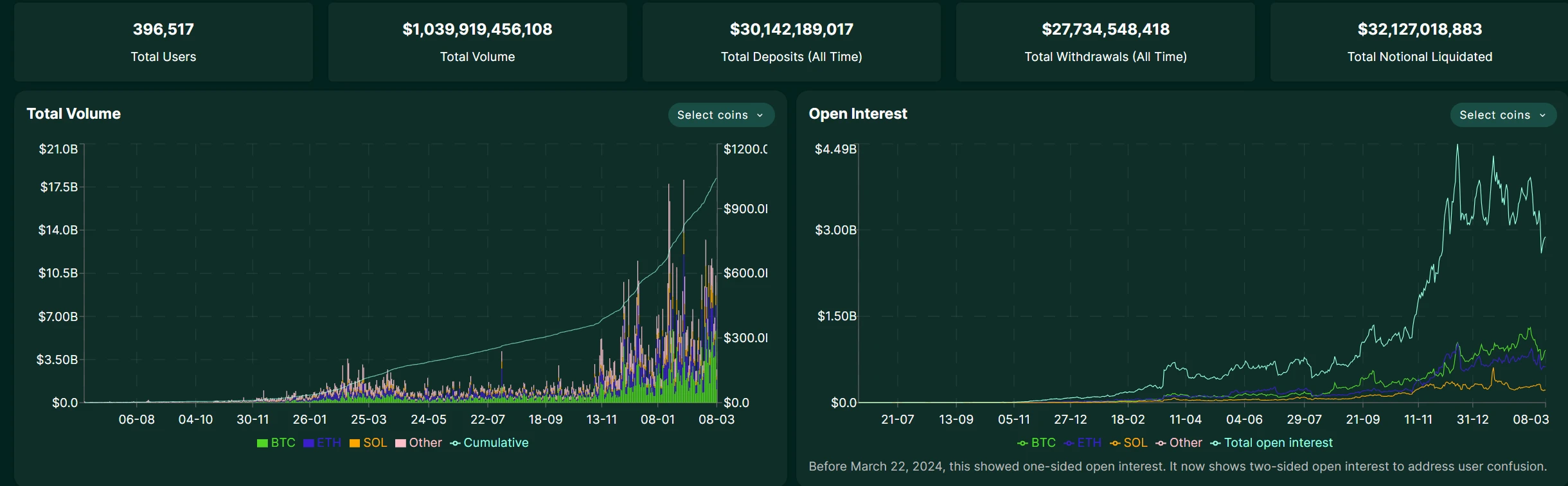

However, on the chain, although the DEX spot trading volume has remained at the billion-dollar level, decentralized derivatives have never been able to open up a market gap: dYdXs average daily trading volume is about 19 million US dollars, and the once-popular GMX has seen its holdings and 24-hour trading volume both fall below 10 million US dollars, and has been almost forgotten by the market.

The only surprise is that Hyperliquid, which has recently been regarded as a victory of progressive decentralization, broke the deadlock as the new king of on-chain derivatives protocols. The daily trading volume of derivatives once exceeded US$18 billion, accounting for more than 60% of the on-chain perpetual contract market.

Its revenue scale exceeds that of most second-tier CEXs, and it has maintained a 50%+ month-on-month growth rate for three consecutive months. If we carefully observe the rise of Hyperliquid, we will find that the key to its success lies in its reconstruction of value logic through vertical integration architecture:

The deep integration of the order book engine and the smart contract platform enables on-chain derivatives to compete head-on with CEX in terms of transaction speed and cost for the first time, and establish structural advantages in terms of cost, auditability, and composability (I personally think it is somewhat similar to the structural advantages that BYD has in the new energy market).

This also proves that there is no lack of demand for on-chain derivatives, but a lack of product forms that are truly adapted to the characteristics of DeFi. To put it bluntly, traditional perpetual contracts rely on a margin mechanism, high leverage leads to frequent liquidations, and user risks are difficult to control. Previous on-chain derivatives have been slow to create value that CEX cannot replace.

Once users find that they have to bear the same risk of liquidation when trading on dYdX/GMX, but cannot obtain the liquidity depth and trading experience of Binance, their willingness to migrate will naturally be zero.

Because of this, decentralized derivatives were inevitably demystified from the holy grail in the last round of narratives. Their decline is essentially the deep contradiction between the decentralized framework and the demand for financial products - there is only a decentralized narrative, but there is no product ticket that users must use. This is also the core factor that Hyperliquid was able to overtake others.

So on the surface, CEX’s overwhelming advantage stems from its user base and liquidity depth, but the deeper contradiction lies in the fact that on-chain derivatives have never been able to solve a core proposition: how to balance risk, efficiency and user experience under a decentralized framework? Especially when the industry enters the deep waters of derivatives innovation, how to minimize the entry threshold for new users and maximize the release of asset efficiency?

In fact, the event contract launched by Binance not long ago provides a new idea for reference - it is essentially a variant of the options product, which confirms the markets popular demand for simple and easy-to-use non-linear returns.

This is also true from my personal perspective. If you want to jump out of the competitive red ocean of perpetual contracts, for the general public, options may be an antidote that is more in line with the characteristics of the chain - its non-linear return characteristics ( limited buyer losses and unlimited potential returns ) naturally fit the high volatility of cryptocurrencies, and the small prepayment of premiums mechanism can significantly meet the simple trading needs of general users who want to make a small investment for a big return.

From contracts to options, the promised land of on-chain derivatives?

Objectively speaking, in the field of on-chain derivatives, options with the characteristics of non-linear returns are actually the most suitable product form: not only do they naturally avoid the risk of liquidation, but they also achieve a better risk-return ratio than futures contracts through time value leverage.

However, since options have complex components such as exercise date and exercise price, they are not as intuitive as perpetual contracts for retail investors. In particular, there is always a structural contradiction between the complex exercise rules of traditional options (such as expiration date, spread combination) and the retail investors pursuit of simple and instant transactions, and this mismatch is particularly obvious in on-chain scenarios.

Therefore, for decentralized options products, the problem lies in how to build an on-chain options system that can balance Crypto capital efficiency and product friendliness. It is worth mentioning here the coin-based perpetual options mechanism proposed by Future - attempting to reshape the underlying logic of on-chain derivatives through de-complication and asset efficiency revolution.

If we break down the structure of coin-based perpetual options, the key point actually lies in its literal meaning: coin-based and perpetual options.

Only currency standard can maximize the capital efficiency of long-tail assets

The core starting point of the coin standard is to maximize the capital efficiency of users on-chain Crypto assets. After all, in the context of the meme coin wave and the explosion of multi-chain ecology, most users on-chain assets are highly fragmented, such as being scattered on different chains and long-tail token assets.

However, existing protocols mostly require settlement in stablecoins, which forces users holding long-tail assets such as BTC, ETH, and even meme coins to either be unable to directly participate in transactions or passively bear exchange losses (currently mainstream CEXs also use USDT/USDC as settlement currencies, and have minimum transaction limits), which is essentially contrary to the DeFi concept of asset sovereignty and freedom.

Take Fufuture, a decentralized coin-based options protocol that is currently exploring similar products, for example. It allows users to directly use any on-chain token as margin to participate in BTC/ETH index options trading, thereby eliminating the redemption step and activating the derivative value of dormant assets. For example, users holding meme coins can hedge against market volatility risks without cashing out, and even amplify returns through high leverage.

From the data, as of May 2025, among the margin transactions supported by Fufuture, the margin positions of meme coins such as Shiba Inu (SHIB) and PEPE accounted for a high proportion of the active positions on the entire platform, proving that users do have a strong demand to use non-stablecoin assets to participate in option hedging and speculation, and also indirectly verifies that the coin-based margin is indeed a significant market pain point.

Doomsday Options is the ultimate leverage strategy for sustainability

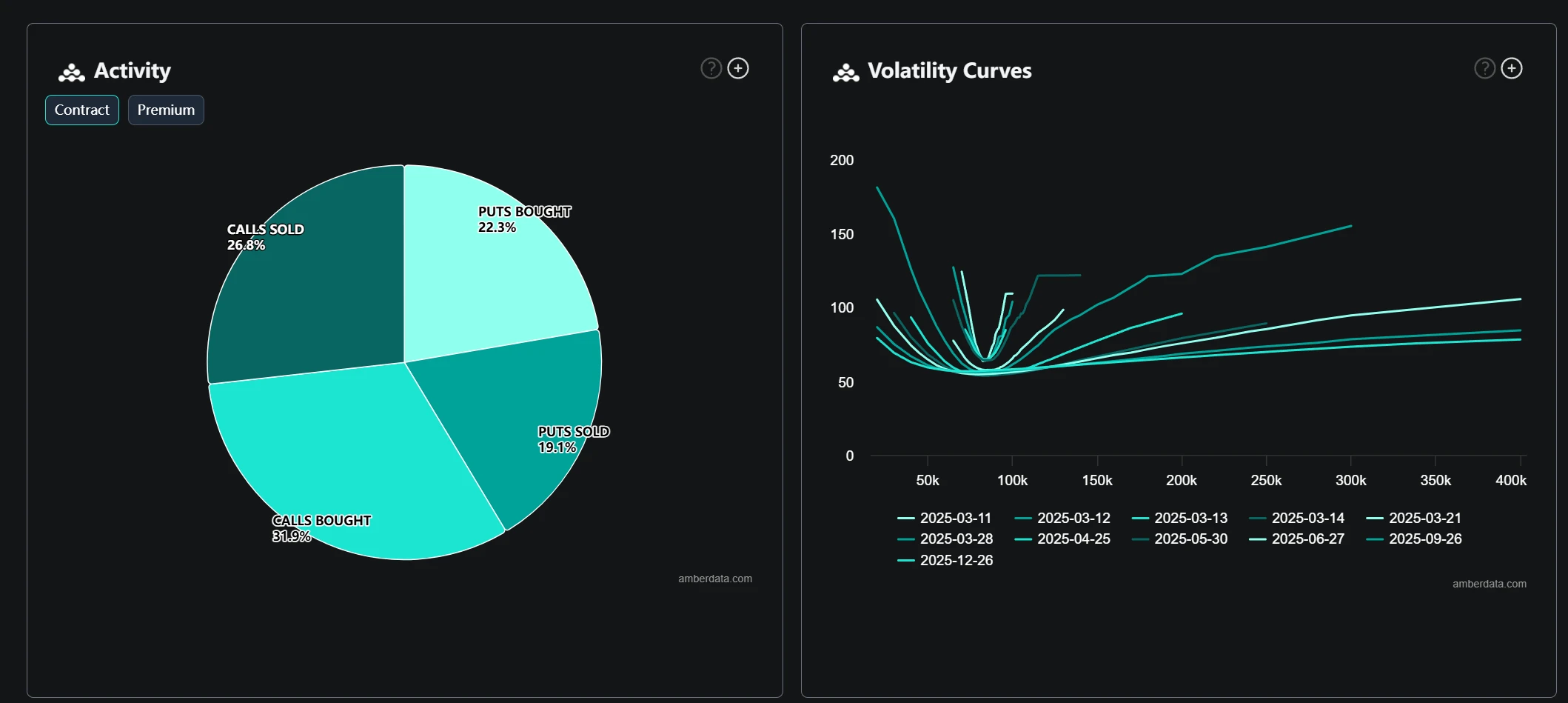

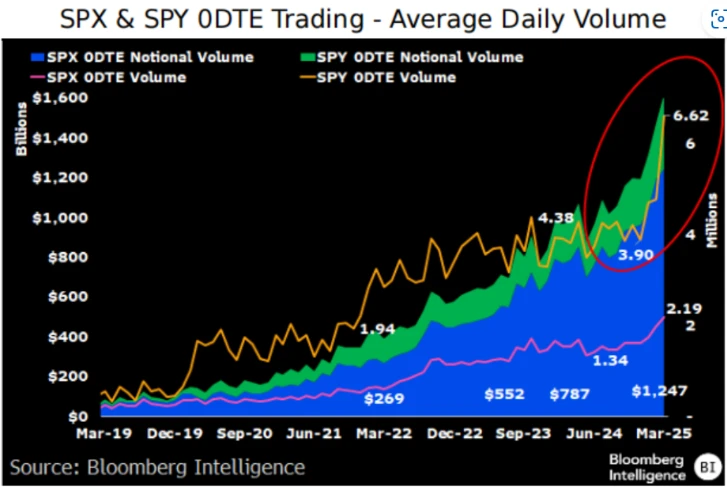

From another perspective, in recent years, people have become more and more fond of high-odds short-term transactions such as end-of-day options. Since 2016, small trading users have begun to flock to options in droves, with 0 DTE option transactions accounting for 43% of SPX option total trading volume, up from 5%.

Source: moomoo.com

The perpetuation of end-of-day options actually provides users with the opportunity to continue betting on high-odds end-of-day options.

After all, the exercise date setting of traditional options is seriously mismatched with the short-term trading habits of most users, and the frequent opening of end-of-day options is inevitably overwhelming. Lets take the design logic of Fufutures introduction of a perpetual mechanism in option products as an example - cancel the fixed expiration date and instead adjust the holding cost through a dynamic funding rate.

This means that users can hold put/call option positions indefinitely, and only need to pay a very small amount of funding fees every day (much lower than the funding rate of CEX perpetual contracts). This is equivalent to users being able to extend their holding period indefinitely, turning the high-odds characteristics of end-of-day options into a sustainable strategy while avoiding passive losses caused by time decay (Theta).

Let’s take an example to make this clearer. When a user opens a 24-hour BTC put option with USDT or other long-tail assets as margin, if the BTC price continues to fall, the position can be held for a long time to capture greater returns. If the judgment is wrong, the maximum loss is limited to the initial margin, and there is no need to worry about the risk of liquidation. At the same time, when the 24-hour option expires, you can freely choose whether to continue the extension.

This combination of limited losses + unlimited gains + time freedom essentially transforms options into low-risk perpetual contracts, greatly lowering the threshold for retail investors to participate.

In general, the deep value of the paradigm shift of coin-based perpetual options lies in that when users discover that any long-tail token in their wallet, even meme coins, can be directly converted into risk hedging tools, and when the time dimension is no longer the natural enemy of returns, on-chain derivatives will be able to truly break through the niche market and build an ecological niche to compete with CEX.

From this perspective, the new ticket potential demonstrated by coin-based perpetual options may be one of the important weights that may really start to tilt the balance of the game between on-chain and CEX.

Will on-chain options produce new solutions worthy of attention?

However, the large-scale popularization and penetration of options, especially on-chain options, is still in its very early stages.

It is visible to the naked eye that since the second half of 2023, new players in the on-chain derivatives market have been exploring new business directions: whether it is Hyperliquids on-chain native leverage or coin-based perpetual options such as Future, decentralized derivatives trading products are indeed brewing some seed variables for major changes.

For these new generation protocols, in addition to achieving direct competition with CEX in terms of transaction speed and cost, and releasing the capital efficiency of long-tail assets on the Crypto chain including meme, the key is that based on the on-chain architecture, the interests of the community, trading users and protocols can be fully bound together to the maximum extent possible - liquidity providers, trading users, and the protocols own architecture can form a shared honor and loss community of interests network (taking Fufutures protocol architecture as an example):

Liquidity providers obtain risk-stratified benefits through a dual-pool mechanism (high returns in private pools + low risks in public pools);

Traders can participate in high-leverage strategies with any asset and their losses are clearly capped;

The protocol itself captures the growth of ecological value through governance tokens;

This is essentially a complete subversion of the traditional CEX platform-user exploitative relationship. When the long-tail tokens held in the users wallet can directly become trading tools without relying on CEX, and when transaction fees and ecological value are distributed to ecological contributors through DAO, on-chain derivatives finally show what DeFi should look like - not only a trading venue, but also a value redistribution network.

This is actually the DeepSeek moment of on-chain derivatives that the market has been looking forward to for many years - allowing decentralized derivatives to break through the constraints of trading experience, gradually introducing on-chain native leverage and maximizing capital efficiency to DeFi, and no longer relying on CEX as a necessary link, which is expected to bring a larger leap to the market, give birth to more borderless innovations, and usher in a new DeFi summer.

Historical experience tells us that each round of narrative outbreak requires the resonance of correct narrative + correct time. Whoever can solve the most painful asset efficiency problem for users at the right time will be able to hold the scepter of on-chain derivatives.

Last words

I personally always believe that decentralized derivatives protocols are undoubtedly the holy grail on the chain and not a narrative false proposition.

From multiple dimensions, decentralized derivatives still have the potential to become one of the most scalable and profitable tracks in the DeFi ecosystem. However, it must truly step out of the shadow of centralized replacement and rely on the on-chain native structure and capital efficiency revolution to complete self-innovation of product form.

The key point is that for on-chain users, the value of decentralized derivatives lies not only in providing new trading tools, but also in whether they can open up a path of frictionless flow of assets - derivatives hedging - compound growth of returns.

From this perspective, when Meme coin holders can directly use tokens to participate in Crypto long-tail asset transactions, and when multi-chain assets can become margin without cross-chain, the form of on-chain derivatives is being redefined. This is also the transition idea of new generation players such as Hyperliquid and Future.

Perhaps, the ultimate goal of decentralized derivatives is not to replicate CEX, but to create new demand with the native advantages of the chain (open, composable, and permissionless), and the market may have taken a key step.