1. Background: Demand for stablecoins continues to grow

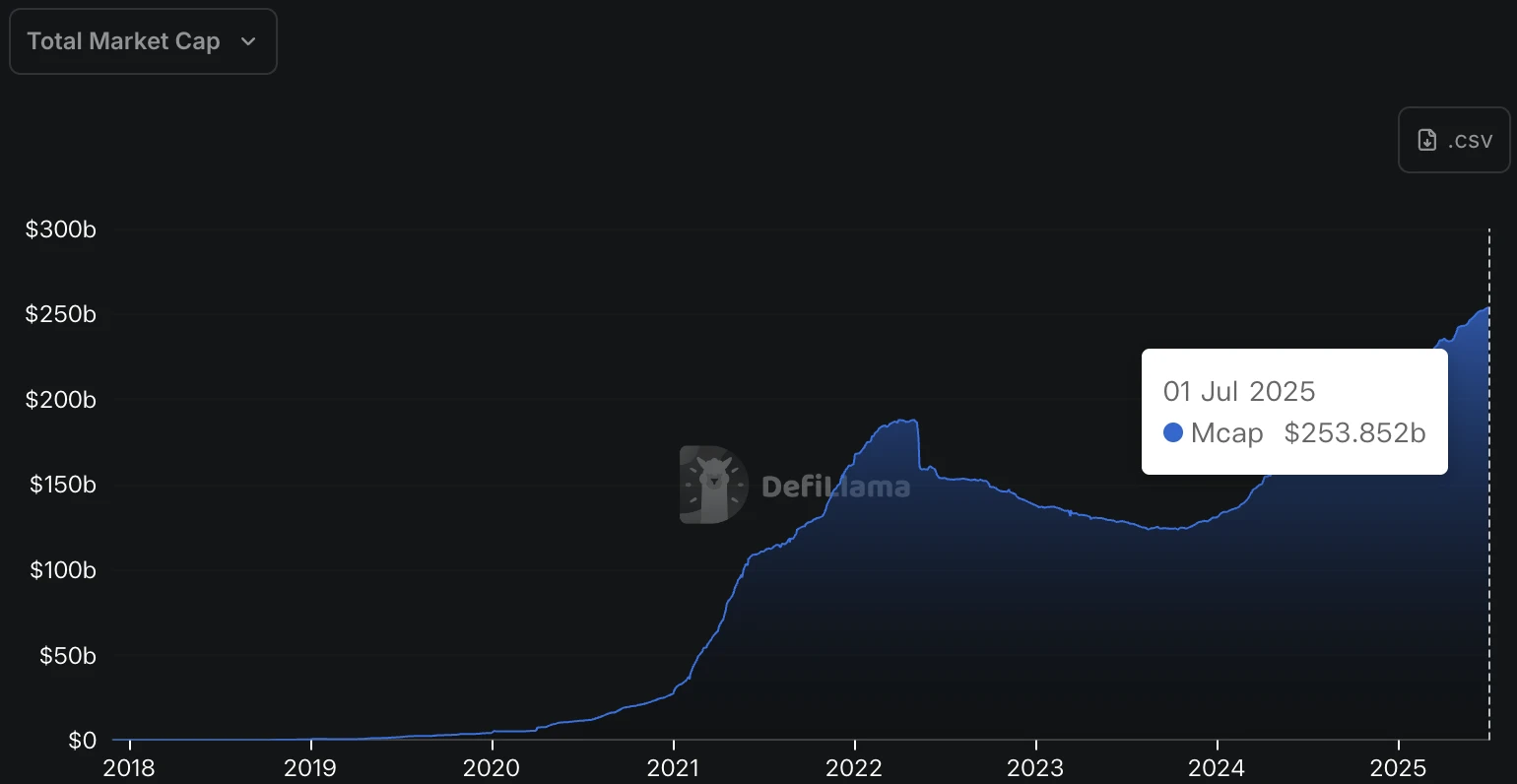

In the past, stablecoins were only seen as an important tool in the crypto world, mainly used for on-chain transactions and asset hedging. Today, the role of stablecoins is undergoing a profound transformation. The total market value of stablecoins has increased from US$650 million at the end of 2018 to over US$250 billion by 2025, an explosive growth of 384 times in just 6 years. Stablecoins represented by USDT and USDC have long been comparable to Bitcoin in daily trading volume, even exceeding Bitcoin and Ethereum. Stablecoins are not only the US dollar in the crypto world, but are also becoming a key bridge connecting Web2 and Web3.

Figure 1. Stablecoins total market cap. Source: https://defillama.com/stablecoins

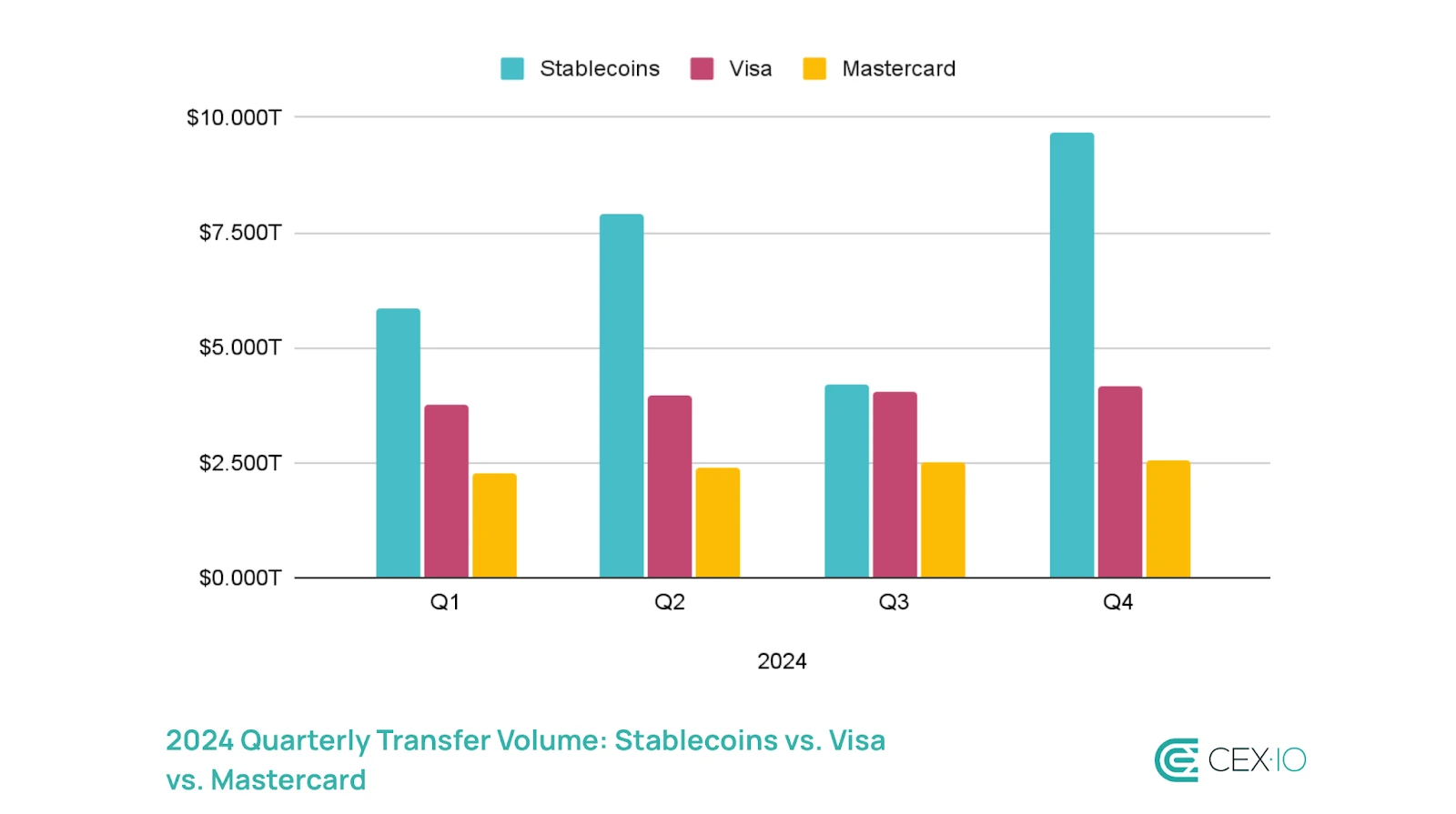

The rapid rise of stablecoins is not accidental. Against the backdrop of high costs and slow payment of global cross-border payments, traditional Web2 companies and institutions are urgently looking for new payment solutions that are more efficient and compliant. According to CEX.IO statistics, the total annual transaction volume of stablecoins in 2024 exceeded 27 trillion US dollars, exceeding the total annual transaction volume of Visa and Mastercard for the first time. Whether it is cross-border e-commerce, international logistics, or global financial services, there is a real demand for stablecoins.

Figure 2. 2024 Quarterly Transfer Volume: Stablecoins vs. Visa vs. Mastercard. Source: https://blog.cex.io/ecosystem/stablecoin-landscape-34864

At the same time, the policy level is also sending positive signals, such as the US Senate passing the GENIUS Act, the EU passing the MiCA policy, and Singapore and Hong Kong accelerating the promotion of a clear regulatory framework, all of which provide a good background for traditional companies to legally issue stablecoins. It can be seen that stablecoins are moving from the gray area of the crypto world to the sunny area of the global payment system.

It is in this context that traditional Web2 giants have entered the stablecoin market. Recently, institutions including Mastercard, JD.com, Ant Financial, and several leading banks in South Korea have announced their own stablecoin issuance plans or stablecoin-related cooperation. Stablecoins are becoming a hotly contested market among companies.

2. Traditional enterprises’ layout of stablecoins

2.1 Mastercard

2.1.1 Mastercard promotes closed-loop settlement on the chain

Partnering with Chainlink to support buying cryptocurrencies directly from the chain using Mastercard

On June 24, 2025, Mastercard announced a partnership with blockchain infrastructure giant Chainlink, and also joined forces with Shift 4, Zerohash, Uniswap, Swapper Finance, XSwap and other institutions to open up the process from bank card payment to on-chain asset delivery. 3.5 billion Mastercard credit cards around the world can directly purchase crypto tokens in DEX (such as Uniswap). This means that even if you don’t register an account on a centralized exchange, ordinary users can swipe their cards to buy coins just like swiping them for shopping, and seamlessly enter the Web3 world.

The entire payment process is completely on-chain, real-time and compliant. When a user initiates a transaction through the Swapper Finance front-end, the traditional payment gateway service provider Shift 4 will first submit the Mastercard payment request to complete the deduction of fiat currency (such as US dollars, euros, etc.). Subsequently, the cryptocurrency and stablecoin infrastructure provider Zerohash will exchange the fiat currency for the intermediate crypto asset USDC. At this time, Chainlink will verify the transaction instructions and send them to the Swapper smart contract. The Swapper contract will then call a DEX such as Uniswap to complete the final token exchange and send the crypto assets that the user wants to their wallet. The entire process is automatic, secure, and traceable, and can be completed within a few minutes.

Swapper Finance is now officially online, and users can purchase it through its official website (https://swapper.finance/). Mastercard also stated that it will continue to explore more on-chain payment scenarios with Chainlink in the future, so that on-chain assets can be used as conveniently as traditional currencies.

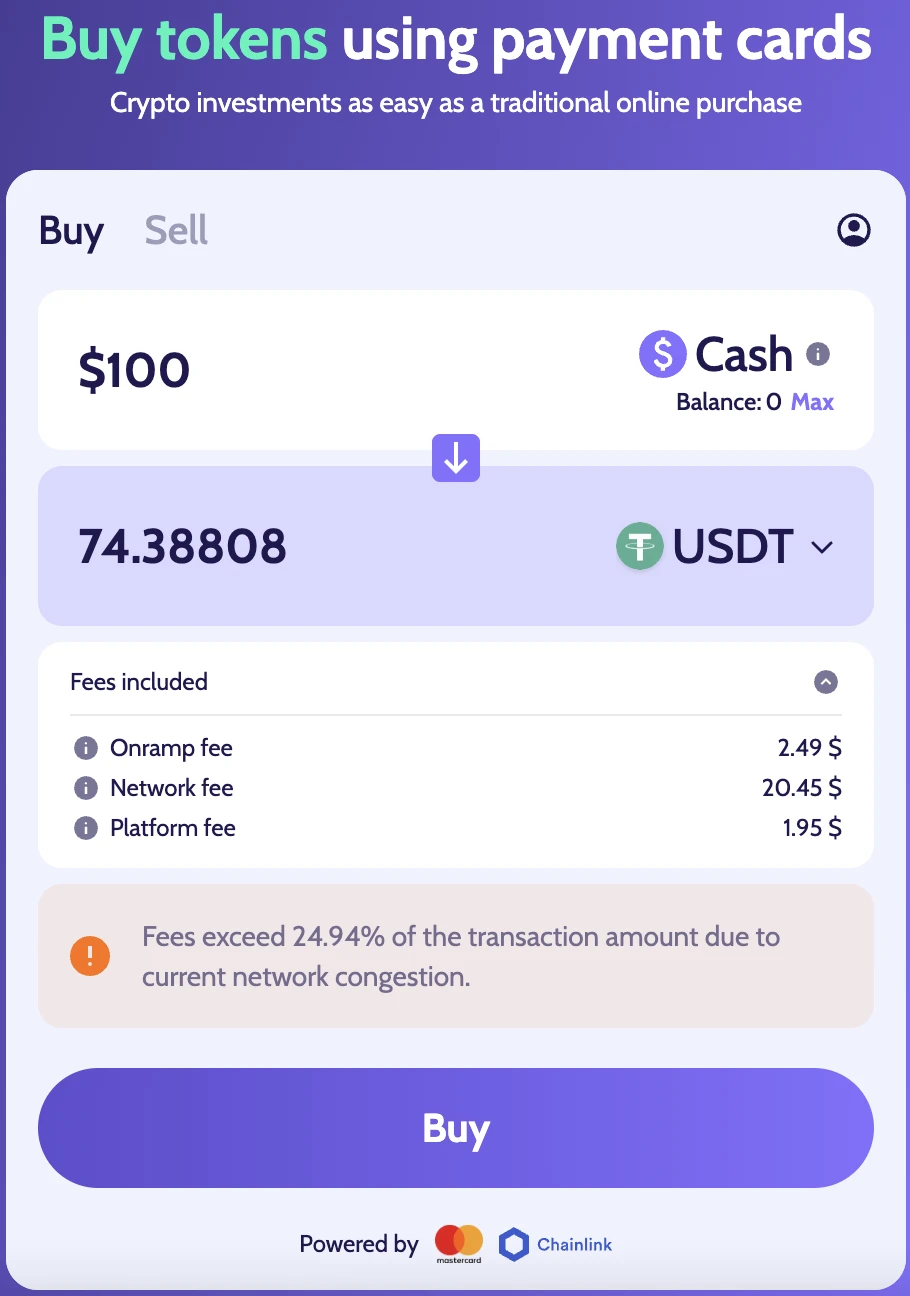

Swapper Finance Coin Purchase Transaction Fee Structure

It is worth noting that when you use Mastercard to buy coins on Swapper Finance, you will see three fees: Onramp fee, Network fee and Platform fee.

Onramp fee: The fiat-related service fee generated by swiping a card to pay from a bank or credit card channel. This fee mainly occurs when using a bank card for payment, and is collected by the payment channel (Shift 4) and the clearing agency (Mastercard). It covers credit card transaction fees, cross-border settlement fees, currency conversion fees, etc. In addition, there are service providers such as Zerohash that are responsible for converting the fiat currency swiped by users into on-chain stablecoins, and they will also charge a part of the service fee.

Network fee: includes the Gas consumed by executing transactions on the chain (such as stablecoin exchange for ETH), which is determined by the blockchain network where the on-chain transaction initiated by the user is located.

Platform fee: Fees charged by the platform. This part is charged by Swapper Finance itself and its partners such as XSwap and Chainlink, etc., to cover the costs of transaction matching, user interface, oracle verification, technical security, etc. For example, Chainlink will verify whether the users transaction request matches, and XSwap will complete the real asset exchange on the chain through DEX such as Uniswap. The platform packages these functions through a unified interface to provide a simple experience of swiping a card to buy coins, but each layer of service behind it involves costs.

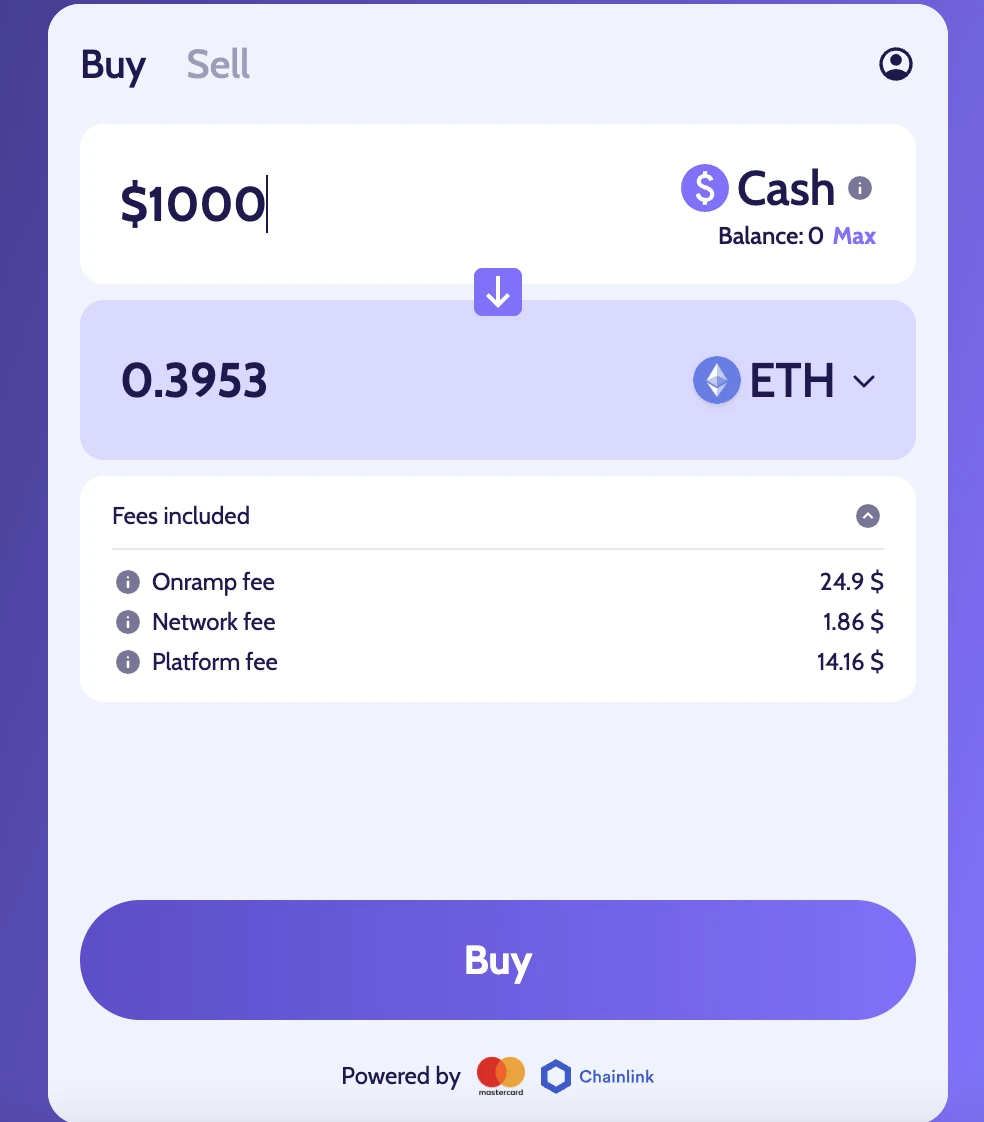

In the case of network congestion, when using the platform to purchase $100 of USDT, the transaction fee ratio is as high as 26%, indicating that the highest fee comes from the gas fee (US$20.45) caused by network congestion.

Figure 3. Swapper trading page. Source: https://swapper.finance/

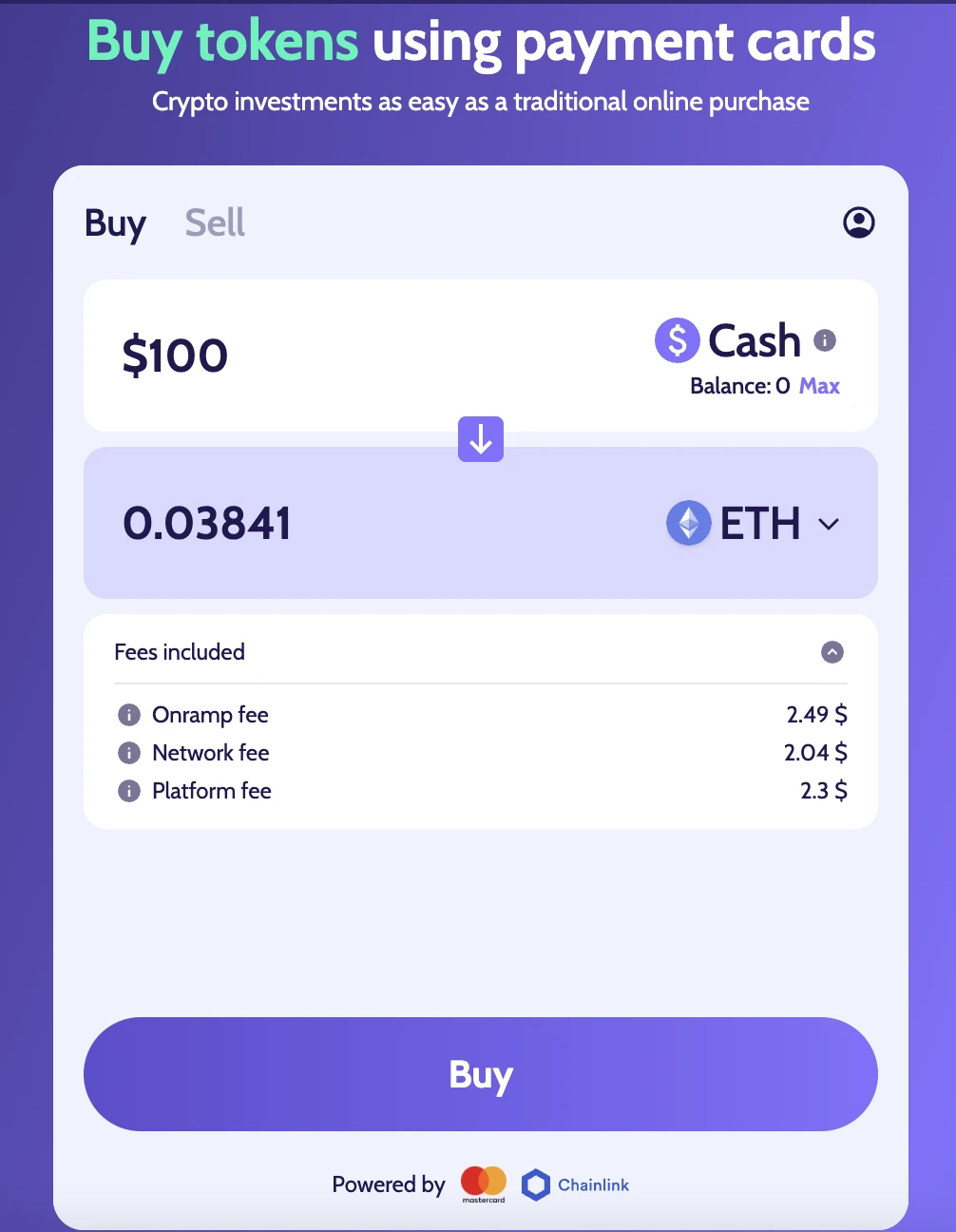

When the network is not congested, the handling fee generated when using $100 to buy ETH is about $6.8, which is about 6.8% of the handling fee. Under the same network conditions, when using $1,000 to buy ETH, the handling fee generated is about $40.92, which is about 4.09% of the handling fee. It can be seen that the handling fee will change in real time according to the congestion of the network and the amount purchased. Under the same network conditions, the smaller the amount purchased, the higher the handling fee ratio.

Figure 4. Fees when buying $ 100 worth of ETH. Source: https://swapper.finance/

Figure 5. Fees when buying $ 1000 worth of ETH. Source: https://swapper.finance/

Account registration and identity verification are required to meet compliance requirements

Although Swapper Finance is a decentralized trading platform, its process of buying coins by swiping a card still involves a KYC (identity verification) process similar to that of centralized exchanges (CEX) to meet its fiat currency payment and compliance requirements.

Although the final transaction of Swapper is completed on the chain, the initial payment is made by swiping a bank card with fiat currency, which involves the regulatory requirements of the traditional financial system. To ensure that these transactions comply with legal compliance (especially anti-money laundering AML and know your customer KYC regulations), the platform must verify the identity of the user. This process is usually handled by Zerohash, its cooperative compliance service provider, and requires users to register an email address and upload identity documents (such as a passport or ID card).

But compared with centralized exchanges, Swapper Finance still embodies strong Web3 principles in user experience and asset control. First of all, transactions are completed entirely on decentralized exchanges (DEX), such as Uniswap, rather than reconciled in the platforms internal database. Secondly, the digital assets purchased by users go directly into the on-chain wallet. Swapper does not hold users funds and does not involve withdrawal steps. Moreover, it uses Chainlinks oracle to execute and verify orders, ensuring that the transaction process is open, transparent and decentralized.

Advantages and Disadvantages of Swapper Finance

As an innovative service that connects the Web2 payment system with Web3 on-chain transactions, Swapper Finance does have many highlights, but it also has some limitations.

Swapper Finance allows users to purchase on-chain assets directly with Mastercard bank cards. Assets do not need to be custodied to the platform, nor do they need to go through the cumbersome CEX withdrawal process. Users only need to connect their wallets, verify their identities, and pay by card to receive digital currencies directly into their on-chain wallets. For users who are new to the crypto world, this is a very friendly and easy entry point.

Its biggest advantage is convenience and compliance. Transactions are completed through decentralized exchanges such as Uniswap, and assets will not be managed by the platform, which is safe and transparent. At the same time, it relies on compliance institutions such as Mastercard, Zerohash and Shift 4 to achieve seamless connection between legal currency payment and on-chain transactions. The overall process is clean and neat, which is very suitable for early users.

But Swapper also has some obvious limitations. For example, the handling fees are relatively high, including the fiat currency conversion fee (onramp), gas fee and platform service fee. In addition, in order to meet regulatory compliance, the platform also requires users to complete KYC (upload identity proof), which makes it not much different from CEX in terms of privacy.

In addition, the selection of on-chain assets and chains supported by Swapper is not rich enough at present, and due to its high fees and on-chain transaction delays, it is more suitable for new users who are entering with small amounts or buying coins for the first time, but it may not be the best choice for professional trading users who pursue privacy or low transaction fees.

What the launch of Swapper Finance means for Mastercard

The birth of Swapper solved the problem that has long plagued new users. Swapper Finance integrates multiple compliance infrastructures such as Mastercard, Chainlink, and Zerohash, making it possible to buy coins on the chain by swiping a card directly, truly handing the entrance to decentralized finance to ordinary users, and bringing a huge potential new user group to the crypto market. It can be seen that traditional financial institutions have significantly improved their acceptance of blockchain technology and are accelerating their entry into the on-chain world.

2.1.2 Mastercard’s other plans for stablecoins

Promote in-depth cooperation with Fiserv and integrate FIUSD into the global payment network

On June 24, 2025, Mastercard announced that it would officially start in-depth cooperation with Fiserv to integrate its upcoming stablecoin FIUSD into the Mastercard global payment network. This means that more than 150 million merchants around the world will support payments with FIUSD, bringing more diverse payment options to users and merchants, and also marking the official entry of stablecoins into the mainstream payment system.

One of the focuses of the cooperation between the two parties is to optimize the two-way exchange experience between fiat currency and FIUSD. In the future, users can more easily convert US dollars in their bank accounts into FIUSD, and can also quickly exchange FIUSD back to fiat currency, improving the flexibility and liquidity of use.

At the same time, Mastercard plans to support global acquirers to use FIUSD as the settlement currency for merchants. In other words, no matter how consumers pay, merchants can choose to settle in FIUSD. In the current mainstream payment system, whether it is WeChat, Alipay, or Visa, merchants usually cannot choose the settlement currency independently. Take WeChat Pay as an example. Even if the user uses an overseas bank card or a foreign currency account to scan the code to pay, the system will automatically convert the foreign currency into RMB, and the final settlement to the merchant is still RMB. Merchants cannot say I want to receive US dollars or I only accept stablecoins. This option is not in the hands of merchants. The same mechanism also exists in international card organizations. For example, when you use Visa to swipe your card abroad, the merchant receives its local currency, and the exchange and settlement are completed by the acquirer and the clearing bank in the background. In cross-border payment scenarios, this single legal currency settlement mechanism is even more cumbersome. Consumers use US dollars or euros. After clearing through multiple layers of intermediaries (acquiring banks, issuing banks, card organizations, etc.), the merchant may eventually receive funds in local currency. The payment cycle often takes 2 to 3 working days, and the exchange rate losses and settlement fees incurred in the middle are difficult to estimate, leaving merchants in a completely passive position.

This new mechanism that Mastercard is promoting in cooperation with payment technology company Fiserv will bring an important change: for the first time, merchants will be able to choose to settle with stablecoin FIUSD. This means that in the future, whether consumers use credit cards, debit cards, Apple Pay or on-chain assets such as USDC, merchants can set I only accept FIUSD, and the system will automatically convert the received funds into FIUSD and deposit them into the merchants account after the payment is completed. Doing so not only simplifies the exchange and settlement process, but also increases the speed of arrival (on-chain settlement can be close to real-time), and significantly reduces costs.

In addition, the two parties also plan to launch a stablecoin co-branded card based on the Mastercard network. This card will allow users to integrate FIUSD with credit and debit card accounts, will be available globally, and will support flexible switching of payment methods (credit, debit, stablecoin balance) for transactions through Mastercards One Credential system.

This cooperation marks Mastercards official embrace of stablecoin applications. It is no longer just holding or issuing stablecoins, but deeply embedding them into practical applications such as payment, settlement, and user experience. Mastercard and Fiserv are promoting stablecoins to become a payment and settlement method as reliable and popular as the US dollar.

Expanding the integration of multi-currency stablecoin ecosystem

In addition to FIUSD, Mastercard also announced that it will integrate a variety of mainstream stablecoins into its global payment network, including PYUSD launched by PayPal, USDG led by Paxos, and USDC. This integration means that in the future, no matter which stablecoin consumers use, whether it is PYUSD, USDC, or even the upcoming FIUSD, they can pay seamlessly at merchants in the Mastercard network. Merchants can also choose the stablecoin they want to settle in the end according to their own preferences, such as accepting FIUSD, USDC or directly converting them into fiat currency.

By supporting multiple stablecoins, Mastercard is building a multi-currency, cross-platform payment and settlement system that combines the familiarity of Web2 users with the flexibility of Web3 assets. This high degree of interoperability not only enhances the payment freedom of users and merchants, but also creates a unified infrastructure for the future global adoption of stablecoins.

Launch stablecoin consumption card and wallet payment solutions

As early as April 2024, Mastercard reached a strategic cooperation with MoonPay, a crypto payment infrastructure platform, allowing users to bind stablecoins (such as USDC, USDT, etc.) in digital wallets to Mastercard cards and use them directly for offline or online consumption. Users do not need to convert stablecoins into legal tender in advance, but only need to let the system automatically complete the settlement when swiping the card, truly realizing the consumption of on-chain funds in the real world.

The technical logic behind this service is to map the on-chain stablecoin balance to a virtual or physical card within the Mastercard network. When making payments, the automatic deduction of stablecoins and the settlement of fiat currency are completed through the MoonPay and Mastercard interfaces. The entire process is almost imperceptible to users, and the experience is no different from traditional credit cards, but the source of funds is the encrypted assets on the chain.

At the same time, Mastercard is also accelerating its integration with crypto platforms. It has established cooperation with mainstream wallets and trading platforms such as OKX, MetaMask, Kraken, and Binance to promote the ability of digital wallets to directly connect to merchants for payment. This direct connection means that in the future, users can directly click to pay with Mastercard in the wallets of these platforms to complete the consumption of on-chain assets without transfer or cumbersome operations.

This strategy significantly lowers the threshold for crypto payments, while providing a path for traditional merchants to seamlessly access Web3, and also demonstrates Mastercard’s strong bet on the future of stablecoin payments. Simply put, Mastercard has turned the familiar act of swiping a card into a gateway that connects on-chain assets with real-world consumption.

Mastercard’s strategy and ambitions

From Mastercards series of actions in the field of stablecoins, we can clearly feel its layout strategy and ambition. It not only hopes to keep up with the wave of the crypto era, but also wants to firmly grasp the dominance of the future global payment infrastructure.

First, it integrates a variety of stablecoins into its own payment network, including PayPals PYUSD, Paxos USDG, Circles USDC, and Fiservs FIUSD, allowing users and merchants to choose which stablecoin to use for payment or settlement as needed. This means that Mastercard is building a highly compatible, globally applicable multi-currency payment system to turn stablecoins into mainstream consumption and settlement currencies.

In addition, through cooperation with wallets and platforms such as MoonPay, MetaMask, OKX, and Kraken, Mastercard allows users to pay with stablecoins in their wallets, just as easily as using a bank card. This integration connects Web3 users wallets with real-life merchant scenarios, greatly lowering the threshold for crypto payments and providing merchants with the ability to seamlessly access Web3 payments.

Overall, Mastercard is transforming itself from a traditional payment giant to a bridge between Web2 and Web3. Its goal is not to simply access the crypto world, but to become a key hub for the global circulation and clearing of stablecoins in the future, mastering the rules, standards and channels so that every card can become an entrance to the chain.

2.2 Fiserv plans to launch FIUSD

Fiserv is a global financial technology giant headquartered in the United States, providing services to more than 10,000 financial institutions and 6 million merchants, with an annual transaction volume of up to 90 billion. It has long provided back-end clearing, payment systems, risk control services and core banking infrastructure to banks, credit unions, POS merchants, etc. Against the backdrop of the accelerated evolution of financial digitalization, Fiserv is actively embracing blockchain and stablecoin technology and entering the Web3 era.

In June 2025, Fiserv announced that it would launch its own USD stablecoin FIUSD, which is scheduled to be fully launched by the end of the year. FIUSD will first be deployed on the Solana blockchain, featuring high performance, low fees, and 24/7 on-chain settlement experience. Unlike USDT or USDC for the general public, FIUSD is clearly positioned as a compliant stablecoin for institutional use only, focusing on serving the payment and settlement needs between banks, merchants, and financial service providers.

The goal of FIUSD is to allow banks and merchants to use stablecoins for on-chain settlement as smoothly as using US dollars. Fiserv provides SDK and interface support, and customers can integrate FIUSD into existing banking systems or merchant backends without having to develop blockchain applications from scratch. This means that even small and medium-sized banks or non-tech merchants can easily obtain on-chain payment capabilities. Through FIUSD, traditional financial institutions can migrate settlement processes that originally relied on bank ledgers to the chain, such as merchant collection, transfer, corporate payment, etc., to improve efficiency while retaining the original risk control system and customer experience.

FIUSD was designed with compliance in mind from the beginning. The issuer, Fiserv, is a US listed payment giant and is naturally under a strict financial regulatory framework. The use of FIUSD must go through identity authentication, anti-money laundering review and other processes to ensure that every transaction complies with regulatory requirements. This also makes it a trusted stablecoin designed specifically for institutions. It is not open to ordinary users for direct trading or investment purposes, but serves as a medium for clearing between financial institutions.

It is worth mentioning that FIUSD has received full support from Mastercard. Mastercard announced that it will include FIUSD in its global payment network. In the future, not only users can consume with FIUSD, but merchants can also choose to settle with FIUSD, even if customers use credit cards, debit cards or other payment methods. This is the first time that a traditional payment network has opened up the function of merchants choosing stablecoins for payment and settlement, which is expected to greatly improve the flexibility of the payment system and the efficiency of global circulation.

For ordinary users, FIUSD is not directly presented in the form of wallet balance, but is automatically completed in the background by banks, payment platforms or wallet service providers. For example, when you swipe your Mastercard, the background may automatically convert the fiat currency into FIUSD and complete the payment through the chain. The whole process is imperceptible and compliant for users, and has good traceability and security.

2.3 JD.com actively develops stable currency

JD.com founder Richard Liu revealed on June 18, 2025 that JD.com is applying for stablecoin issuance licenses in several major countries, aiming to launch stablecoins supporting the US dollar and the Hong Kong dollar, aiming to reduce cross-border payment costs by 90% and shorten the time to less than 10 seconds. At the regulatory level, JD.com CoinChain Technology (Hong Kong) entered the Hong Kong Monetary Authoritys stablecoin issuer sandbox in July 2024 and officially tested the JD.com stablecoin pegged 1:1 to the Hong Kong dollar.

According to JD.com’s response in May 2025, this move is mainly to solve the problems of low efficiency and high cost of cross-border payments, and to support the real economy and enterprise-level use, including logistics, supply chain, overseas merchants, etc. At the same time, Hong Kong is about to introduce a regulatory decree for stablecoins in August 2025, further paving the way for JD.com to issue legally issued stablecoins.

Overall, JD.coms stablecoin layout has a clear positioning and complete logic. Relying on its advantages in cross-border e-commerce and logistics, it gradually builds infrastructure in the compliance sandbox test, strives for a license through the Hong Kong governments policy window, and ultimately achieves the goal of global payment optimization. If the supervision goes smoothly, JD.com is expected to launch a formal stablecoin product by the end of 2025 for e-commerce payment, supply chain finance and overseas scenarios.

2.4 Ant Group plans to issue stablecoins in multiple locations

Ant Group is actively promoting its plan to issue stablecoins, mainly through its two subsidiaries, Ant International and Ant Digital Technologies. Ant International, headquartered in Singapore and responsible for international business, plans to apply for a license to issue stablecoins anchored to the Hong Kong dollar in Hong Kong. This application is expected to be made after the new Hong Kong Stablecoin Ordinance officially takes effect on August 1, 2025. At the same time, they also plan to apply for corresponding stablecoin issuance licenses in Singapore and Luxembourg, with the goal of supporting cross-border payments and corporate treasury management, and creating more efficient on-chain payment and settlement tools.

Ant Digits is mainly responsible for local business in China, and is also simultaneously advancing the application for a stablecoin license in Hong Kong. It has completed relevant regulatory sandbox tests and conducted multiple rounds of communication with regulators. Ant Group hopes to introduce stablecoins into the market in a compliant manner, reduce the cost and time of traditional cross-border payments, and achieve settlement in seconds, thereby building a digital payment ecosystem covering millions of merchants and users.

Technically, Ant Group uses its self-developed blockchain platform Whale to carry the stablecoin payment system, and combines it with the artificial intelligence-driven foreign exchange model Falcon to optimize the exchange rate and capital circulation efficiency. It is understood that this system has supported hundreds of billions of dollars in transactions. Overall, Ant Groups stablecoin strategy is to rely on compliance licenses and deploy digital currency businesses in multiple countries and regions, aiming to promote the deep integration of traditional finance and digital finance.

2.5 South Korea’s 8 major national banks form the Korean Won Stablecoin Alliance

South Koreas major banks are actively promoting the issuance of Korean won stablecoins, aiming to build a local digital payment system and strengthen the competitiveness of international trade finance. The plan was jointly initiated by 8 leading banks including Korea National Bank, Shinhan Bank, Woori Bank, Hana Bank, IBK Industrial Bank, Jeonbuk Bank, Suhyup Bank and Toss Bank. These banks have jointly established a joint venture company to focus on the development and issuance of Korean won stablecoins.

The core goal of the plan is to reduce cross-border payment costs, improve settlement efficiency, and provide more convenient international trade financial services for small and medium-sized enterprises by issuing Korean won stablecoins. In addition, the introduction of stablecoins will also help South Koreas international competitiveness in the field of digital currency and promote the development of financial technology.

Currently, the project is still in its early stages, and the specific launch time and technical details have not yet been announced. However, as the South Korean government gradually improves its regulatory framework for digital currencies, the plan is expected to be realized in the next few years.

2.6 Meta explores integrating stablecoins into social platforms

Meta, the parent company of Facebook, Instagram, and WhatsApp, is looking into integrating stablecoins into its social platforms. This time, Meta does not plan to issue new coins on its own, but wants to directly integrate mainstream stablecoins such as USDC.

Metas goal is to allow users to reward, transfer, and pay in chat software, just as easily as sending a message. In this way, not only will cross-border remittances be faster and cheaper, but content creators will also be able to receive payments directly and more conveniently, without having to rely on intermediary platforms or bank transfers.

This plan is expected to start around May 2025. Although Meta has not officially announced it yet, it has not denied it, saying that it is learning about the existing stablecoin mechanism and emphasizing that there is currently no plan to issue Metas own stablecoin. Many foreign media have reported that they are in contact with stablecoin issuers.

In general, Meta is going light this time. It no longer issues its own currency, but chooses to directly access existing stablecoins, which is more pragmatic. If it is officially launched in the future, it may make payments and rewards on social platforms as simple and fast as sending emojis.

3. The significance and value of stablecoins to traditional enterprises

In recent years, with the rapid development of blockchain technology and the digital economy, stablecoins have become an important bridge connecting traditional finance and digital assets. Traditional and technology giants such as Mastercards Swapper platform, JD.com, Ant Group, Fiserv, and Meta have all deployed stablecoins, hoping to use them to improve payment efficiency and reduce costs, especially in cross-border payments and international trade, where stablecoins can achieve settlement in seconds, significantly shortening the time it takes to transfer funds.

At the same time, stablecoins also help these companies promote digital transformation and open up new business scenarios. JD.com can innovate e-commerce payment experience through stablecoins, and Meta plans to connect USDC to Facebook and WhatsApp to bring convenient digital payment functions to social platforms. Through stablecoins, traditional companies can better meet users needs for digital assets and convenient payments, and improve user stickiness and market competitiveness.

In addition, the global regulatory environment has gradually become clearer, which has also provided legal protection for the development of stablecoins. Ant Group, Fiserv and other companies have actively applied for stablecoin licenses in many places to ensure compliance operations and reduce risks. This allows traditional companies to safely carry out stablecoin business and expand their international market layout.

Traditional enterprises have entered the stablecoin market, which is not only the result of technological maturity and growing user demand, but also an inevitable choice in the face of competitive pressure and transformation needs. Through cooperation and innovation, they can not only improve the efficiency of financial services, but also seize new opportunities brought by the digital economy and build core competitiveness in the future.

4. Summary and reflections

Types of Stablecoins Layout by Web2 Companies

Web2 companies layout of stablecoins is mainly reflected in several directions. First, some companies actively apply for compliance licenses and plan to issue their own compliant stablecoins, such as JD.com, Fiserv, Ant Group and South Koreas eight major bank alliances. These stablecoins are aimed at specific markets or business scenarios to ensure compliance with laws and regulations. Secondly, stablecoins are widely used in cross-border payment and settlement optimization, taking advantage of their seconds-level arrival and all-weather service to significantly reduce the time and cost of traditional cross-border remittances and improve the efficiency of capital circulation.

Third, many companies directly connect stablecoins to their own platforms for payment and settlement. For example, JD.com explores stablecoin checkout in e-commerce scenarios, and Mastercard supports cardholders to directly purchase crypto assets with credit cards and promotes stablecoin consumer settlement services. Fourth, payment service providers such as Fiserv and Mastercard help merchants realize stablecoin collection and payment, and also support merchants to choose stablecoins as a settlement method to improve payment flexibility and efficiency. Finally, social platforms have begun to use stablecoins to reward creators and share revenue. Companies such as Meta are exploring the use of stablecoins to provide creators with a more transparent and fast incentive mechanism to promote the healthy development of the content ecosystem.

Overall, Web2 companies have deployed stablecoins in multiple dimensions, promoting their in-depth application in multiple scenarios such as payment, settlement, and incentives, and accelerating the integration of the digital economy and the traditional economy.

What potential impact will the entry of traditional companies into stablecoins have on Web3?

With traditional large companies such as Mastercard, Meta, JD.com, and Ant Group actively deploying stablecoins and on-chain payments, Web3 is gradually moving out of the circle of insiders and into the daily lives of ordinary people. This not only allows more users to purchase Web3 token assets without understanding blockchain technology, but also promotes the industry to become more compliant, secure, and standardized. At the same time, the funds, technology, and user resources brought by traditional enterprises may bring more practical scenarios and innovative cooperation to the Web3 ecosystem, accelerating the development of the industry. In the face of competition from large enterprises, Web3 projects must also improve product experience and quality. The industry will usher in the survival of the fittest and become healthier and more mature.

think

From the perspective of enterprises, traditional companies deployment of stablecoins represents their desire to seize future opportunities in the digital economy. Stablecoins can help enterprises improve cross-border payment efficiency, reduce transaction costs, and simplify settlement processes, which is very important for improving corporate competitiveness. At the same time, compliant stablecoins can also help enterprises better respond to regulatory requirements and reduce legal risks. In addition, through stablecoins, enterprises can develop more innovative business scenarios, such as digital rewards, on-chain financing, etc., to enhance user stickiness and business diversity.

From the users perspective, traditional companies entering the stablecoin field means that more people can use digital assets more conveniently and safely. Stablecoins provide a digital currency option with stable value and convenient circulation. Users do not have to worry about price fluctuations and can make payments and transfers more safely. At the same time, the companys compliance guarantees and technical support also provide users with a safer use environment. Users can also enjoy more innovative services, such as digital wallets directly using credit cards to buy coins, and using stablecoins for shopping and rewards, which reduces the threshold for contact and use.

In general, both enterprises and users are expecting stablecoins to become a bridge between traditional finance and the digital economy. Enterprises hope to improve efficiency and innovation capabilities, while users expect to have a more convenient, secure, and rich digital currency experience. In the future, the active interaction between the two sides will promote the healthy and rapid development of the entire ecosystem.

refer to

1. Mastercard and Chainlink enable on-chain crypto purchases using Mastercards 3.5 billion cards. Link: https://www.mastercard.com/us/en/news-and-trends/press/2025/june/mastercard-chainlink-crypto.html

2.Mastercard partners with Fiserv to accelerate mainstream stablecoin adoption. Link: https://www.mastercard.com/us/en/news-and-trends/press/2025/june/mastercard-fiserv-stablecoin-adoption.html

3.Fiserv Plans FIUSD Stablecoin on Solana for 10, 000 Banks. Link: https://deepnewz.com/regulation/fiserv-plans-fiusd-stablecoin-on-solana-10000-banks-76f5e8d7

4.Metas Stablecoin Ambitions: Is Crypto Integration Coming to Facebook and WhatsApp? Link: https://www.raininfotech.com/blogs/metas-stablecoin-facebook-whatsapp/

5.JD.com plans to apply for global stablecoin license, aiming at the trillion-dollar cross-border payment market. Link: https://cn.cointelegraph.com/news/jdcom-expands-into-global-stablecoin-licensing

6.Eight South Korean Banks Join to Establish Won-Backed Stablecoin, Plan Two Key Models. Link: https://cryptonews.com/news/eight-south-korean-banks-join-to-establish-won-backed-stablecoin-plans-two-key-models/

7.Ant unit plans to apply for stablecoin issuer license in Hong Kong. Link: https://www.reuters.com/world/asia-pacific/ant-unit-plans-apply-stablecoin-issuer-license-hong-kong-2025-06-12/