summary

summary

Bancor is the pioneer of AMM DEX, but after the emergence of AMMDEX such as Uniswap and Sushiswap, Bancors market share has decreased. thenBancor chose to solve the problem of impermanent loss as a starting point to improve the protocol. In the v2.1 version, LP providers basically do not suffer impermanence loss.

The core of its v2.1 version is BNT elastic supply, and there are two features:

1) Support single currency to provide liquidity and reduce risk exposure;

2) Support liquidity protection. The protocol adopts 2 protections, first using the protocol transaction fee to compensate the impermanent loss of the liquidity provider, and forging BNT for compensation when the transaction fee is insufficient. Liquidity protection requires a 100-day lock-up period to achieve nearly 100% coverage, and there is an upper limit on the amount of the liquidity pool.

After the v2.1 version is deployed, it presents several features:

1) The liquidity in the Bancor agreement has increased significantly, but the market share of trading volume has not expanded;

2) There are very few trading pools with sufficient liquidity, and some liquidity pools have poor liquidity;

3) The liquidity of some trading pairs is better than that of Uniswap and other DEXs, enabling Bancor to capture a certain market share;

4) The liquidity pools of stablecoins and some long-tail currencies are limited by the upper limit of the quota, and their liquidity pools cannot be expanded.

In order to gain a better foothold in the DEX field and expand market share, Bancor will make improvements based on the v2.1 version, and will release the v3 version to optimize the impermanent loss solution (increasing the upper limit of the liquidity pool, etc.), while improving other performance of the protocol, the main improvements include:

1) Remove the upper limit of liquidity protection. In the v2.1 version, the BNT provided by the protocol has a set upper limit, and users must provide BNT to expand the fund pool.After the upper limit of liquidity protection is lifted, the liquidity in the agreement may increase again, which is conducive to the formation of a positive cycle of high liquidity, low slippage, increased transaction volume, and increased handling fees to attract more liquidity, especially for the currently affected Stablecoin pools and some long-tail currencies limited to liquidity limits.It should be noted that after lifting the upper limit of liquidity protection, the amount of BNT forged in the agreement will increase, but the impact on the actual circulation is very small;

2) To achieve instantaneous liquidity protection, users can deposit and withdraw at any time, no longer need to wait 100 days to achieve 100% impermanence loss protection, and improve the flexibility of fund use. V3 impermanence loss calculation may use oracle machine quotations, so there may be arbitrage differences, and the pressure of impermanence loss compensation in the agreement increases, which may increase the possibility of using forged BNT for compensation;

3) Release the BNT summary pool, so that token transactions no longer need to be transferred through BNT, which can reduce slippage and Gas fees;

4) Allow BancorDAO to guide liquidity distribution. The protocol will introduce the concepts of trading liquidity and superfluidity. Trading liquidity is used for market making. Superfluidity can be used as trading liquidity or other charging strategies. Trading liquidity The scale is still decided by the DAO. Tokens that exceed the transaction liquidity can be used for super-liquidity strategies, which can accumulate additional value for protocol participants.

In addition, the agreement also adds functions such as automatic compound interest of liquidity mining rewards, bilateral rewards, support for third parties to share impermanent losses, and the composability of LP tokens, aiming to increase user benefits and improve the utilization rate of underlying funds.

At present, the competition in the DEX sector is fierce, and the head effect is obvious.From the example of Curve, it can be seen that adopting a differentiated product strategy has the opportunity to compete for more market sharesecondary title

1. Basic overview

1.1 Project Introduction

first level title

2. Project details

2.1 Founders and Contributors

2.2 Funding

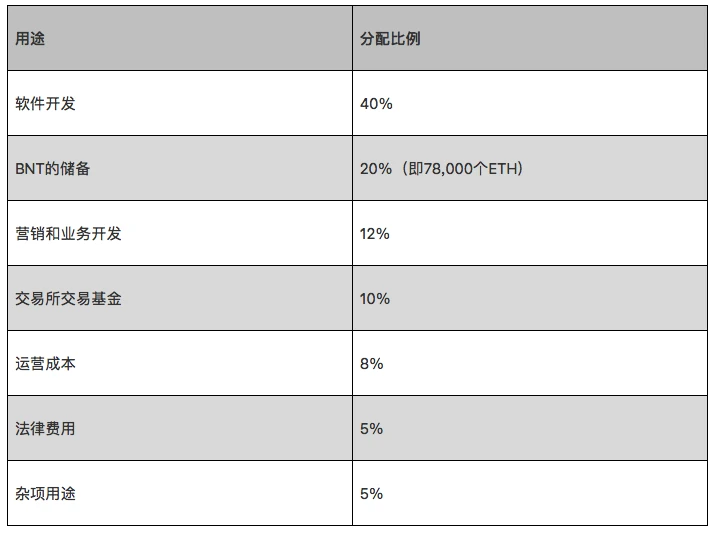

The Bancor ICO raised 390,000 ETH, totaling $152.3 million at the current ETH price. The price of ICO is 1BNT=0.01 ETH. At that time, a total of 79,323,978 BNT were generated. Half of the total tokens were sold to ICO participants, and the remaining 20% was allocated to ecological rewards, 20% to the Bancor Foundation, and 10% to Bancor contributor.

Use of ETH funds:

The team did not provide further updates on the subsequent use of its funds.

2.3 Products

In terms of time, Bancor is the earliest AMM DEX on the market. It is currently in version v2.1 and will be upgraded to v3 soon.

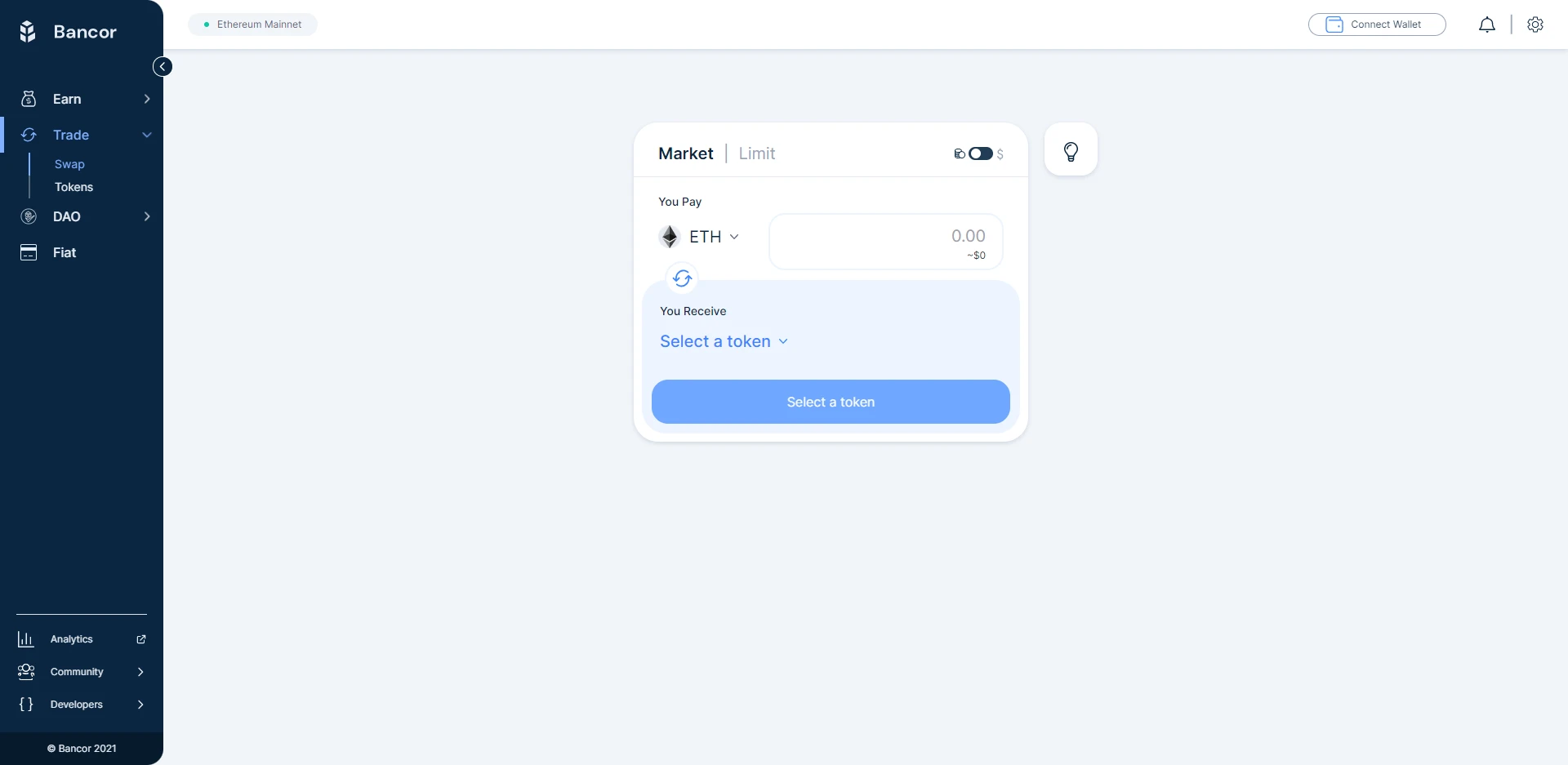

AMM (Automated Market Maker) uses algorithms to replace the manual quotations of traditional market makers, and uses a token pool as the users transaction object. The token pool contains two or more trading pairs, each of which has an algorithm that provides users with real-time token exchange rates. Traditional market makers can still participate by adding a large number of tokens in their hands to the token pool. Because this token pool brings together the liquidity of market makers, AMM is also called a liquidity pool (LP, LiquidityPool).

image description

image description

Figure 2-2 Liquidity pool interface

2.3.1v2.1 version

v2.1 is the current version, with two main features:

1) Single currency market making, reducing risk exposure;

2) Liquidity protection.

v2.1 adopts the mechanism of the above two characteristics realized by BNT elastic supply (elasticBNT supply).

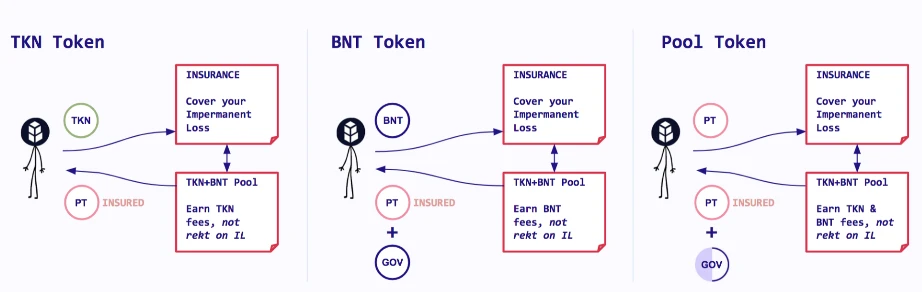

Bancor plan:

a. When a user adds TKN to the TKN (example) token whitelist pool, the protocol will automatically mint new BNT, and the value of the newly minted BNT is equal to the value of TKN, which will lead to an increase in the total supply of BNT.

b. When users use the pool for transactions, part of the transaction fee will be paid by TNK, and part of the transaction fee will be paid by BNT.

c. At this time, if another user provides 100 BNT to the pool, the original 100 BNT in the pool will be destroyed, and the transaction fee corresponding to the 100 BNT will also be destroyed.

d. When the whitelist pool expires and the user is about to withdraw liquidity, the protocol will calculate the impermanent loss.

e. The protocol will use transaction fees to compensate for the impermanent loss, and judge whether it is necessary to use newly forged BNT to compensate for the loss.

f. After the loss is compensated, the remaining BNT tokens related to the TKN pool will be destroyed.

In order to protect the entire network from being greatly affected by the newly added BNT, the following restrictions have been made: 1) The total amount of a single currency added and the number of BNT minted due to the addition of a single token have an upper limit in the entire network; 2) Liquidity There is a limit to the protection rate (you need to withdraw liquidity after the 100-day period to cover 100% impermanent loss).

The income of a Bancor pool is divided into 2 parts:

1) The cost of protocol forging BNT (Protocol-Owned BNT). The fee generated by the protocol forging BNT is used to compensate the impermanent loss of the liquidity provider, and if there is still a remaining fee after the compensation, it will be destroyed. If the agreement fee is not enough to compensate impermanent loss, the agreement will be used to forge BNT for subsidy;

2) The fees generated by TKN (example) tokens are allocated to liquidity providers.

The liquidity protection mechanism means that the longer the user stays in the pool, the more protected it will be. In about 3 months (100 days), 100% of impermanent losses can be covered.

Under the Bancor single-currency market-making scheme, assuming that there is no impermanent loss and no BNT provider, the transaction fees obtained by the pool are partially paid in TKN and partially paid in BNT. When the end user withdraws all TKN liquidity, the value of TKN will be greater than the initial value, so the BNT automatically destroyed by the agreement will also be greater than the previously minted amount. So eventually, the total supply of BNT will decrease, which will increase the scarcity of BNT. But the assumption of this conclusion is almost impossible to hold, impermanence loss can be mitigated but cannot be avoided. According to Bancors impermanence loss insurance mechanism, it is possible that the system needs to newly mint BNT tokens to compensate liquidity providers. In this case, the total supply of BNT will increase. As for the specific increase/decrease, it depends on Bancors trading volume and market fluctuations.image description

Figure 2-3 Operation process

As shown in the figure above, after the TKN token provider provides the token, it will generate a proof token (Pool Token (PT)) that provides liquidity. Users who provide BNT to the whitelisted pool will get vBNT to represent their protection. BNT liquidity, and for community voting.

Bancor Vortex

Banco Vortex actually sells BNT liquidity to provide the function of proving vBNT, thereby increasing BNT leverage. The Bancor protocol will charge 5% of the transaction fee income for repurchase and destruction of vBNT, the purpose of which is to allow vBNT to exist for buyers.

Votex is a last resort solution in v2.1. vBNT represents the deposited liquidity and transaction fees, while mining revenue and vBNT are separate. The vBNT under v3 binds liquidity, handling fee and mining income, so all income can be compounded.

Can be improved:

· In Bancor 2.1, the transaction still needs BNT as an intermediate token. For example, if ETH buys ENJ, it needs to go through ETH-BNT-ENJ conversion, the transaction fee and slippage increase, and the contract processing is relatively complicated, which also increases the Gas fee;

· The premise of ensuring 100% coverage of impermanent losses is that liquidity must be provided for 100 days, and users cannot deposit and withdraw at any time, which reduces the utilization rate of funds.

· There is an upper limit for the expansion of liquidity in some currencies.

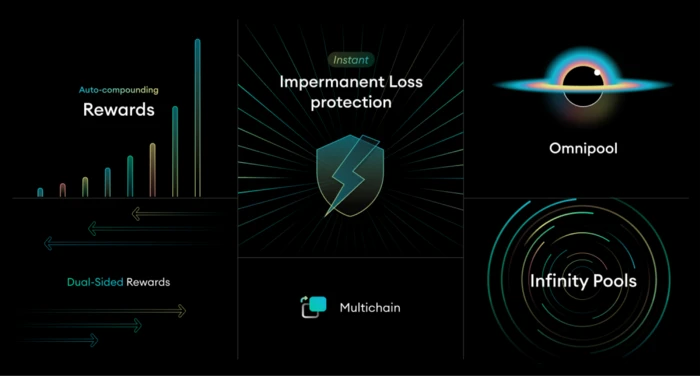

2.3.2v3 version

image description

Figure 2-4 v3 publicity map

The Dawn stage mainly updates 5 features:

1) Instantaneous protection against impermanence loss: no need to wait for the end of the 100-day period like the v2.1 version. Liquidity providers can obtain liquidity protection even if they deposit and withdraw at any time. However, when the impermanent loss is protected instantaneously, there may be an arbitrage gap, which increases the pressure on the system to cover the impermanent loss, and increases the possibility of the system issuing additional BNT tokens to compensate liquidity providers. The new mechanism has been deployed, which can more effectively use the existing liquidity of the protocol and flexibly use the pools handling fee to cover the non-permanent loss of the liquidity pool in the network.

2) Publish BNT summary pool: In v3, the BNT pool is a centralized pool. In Bancorv2.1, each transaction pair pool requires a BNT pool (such as ETH/BNT, DAI/BNT). Contributors said that after BNT becomes a summary pool, token transactions no longer need to be transferred through BNT, thereby reducing users Gas and slippage.

3) Automatic compound interest: When users provide liquidity, the income usually comes from transaction fees and liquidity mining rewards. Both liquidity mining and transaction fee income can be automatically compounded. In v2.1, the transaction fee can be automatically compounded, but the user must manually compound the mining reward. In addition, in v3, both the project party and Bancor can provide tokens as a reward for providing liquidity (both bilateral rewards allow automatic compounding).

4) Cancel deposit limit. It is beneficial to increase the total liquidity of DEX, thus providing better liquidity depth and price. As the liquidity of the protection increases, the long-term economic model viability can only be maintained if the transaction volume increases and the income (including transaction fees and other strategy income) increases. The protocol will introduce the concepts of transaction liquidity and superfluid liquidity, transaction liquidity is used for market making, superfluid liquidity is used for transaction liquidity and other fee-based strategies. The scale of transaction liquidity is still determined by the DAO, and tokens exceeding transaction liquidity can be used for super-liquidity strategies, which can accumulate additional value for protocol participants. In essence, it is a matter of prioritizing the allocation of underlying liquidity, which is used to obtain more returns through flexible strategies while meeting the liquidity needs of transactions.

5) BancorDAO not only has the right to decide how the BNT forged by the agreement will help the agreement to obtain additional fees, but also can vote on whether the amount of BNT forged in the white list will be reduced, or whether the forged BNT liquidity will be transferred to other pools In order to optimize the cost of Bancor agreement, BNT holders and LP acquisition.

Extra features:

1) Reduce Gas Fee

2) L2 deployment. The current DEX basically adopts a multi-chain deployment solution. After the improvement of the Bancor contract, it is easier to migrate.

3) One-click liquidity migration, which can migrate v2 liquidity to v3, or migrate the liquidity on DEX such as Uniswap and Sushiswap to Bancor v3.

4) Composable pool tokens: Bancor v2.1 pool tokens are bound to positions and are not composable. Bancor v3 will introduce a new LP token model, hoping to improve the utilization rate of user funds, or the Bancor protocol will help users use LP tokens to obtain combined benefits. According to the teams AMA information, in the v3 version, if the LP token holder sells the LP token (for example, vBNT), then the user will no longer enjoy the benefits of liquidity mining. At present, the mainstream lending products on the market and the LP tokens of DEX are actually free to trade, but only a small part of LP tokens are fully utilized in practical applications. Curve’s LP tokens currently have a higher utilization rate of LP tokens, and a series of ecosystems based on Curve have emerged, including aggregation income agreements and so on. Bancors LP tokens can be combined to increase the possibility of compound income, but the specific situation needs to be combined with market acceptance and cooperation with relevant project parties.

5) Third-party liquidity protection: In v2.1, impermanent losses are compensated through transaction fees and additional issuance of BNT tokens, which can basically keep BNT in a micro-inflation state (without considering liquidity mining). As long as the impermanent loss is greater than the transaction fee income, BNT will remain in a state of inflation. v3 cancels the upper limit of liquidity protection, and adopts instantaneous liquidity protection, the pressure of impermanent loss compensation may be further increased, the token project party can provide tokens as compensation for impermanent loss, and share the pressure for Bancor.

6) Front-end improvements.

Summary: At present, many details of v3 are still being discussed. The current v3 Dawn stage emphasizes performance as impermanence loss compensation and increased income. Improvements for impermanent loss compensation include: 1) Instantaneous compensation; 2) Third-party (project party) compensation; 3) Cancellation of the upper limit of liquidity protection. Improvement points for increasing income include: 1) Liquidity allocation through DAO to improve the utilization rate of underlying assets; 2) Support for the composability of LP tokens; 3) Automatic compound interest.

secondary title

3. Development

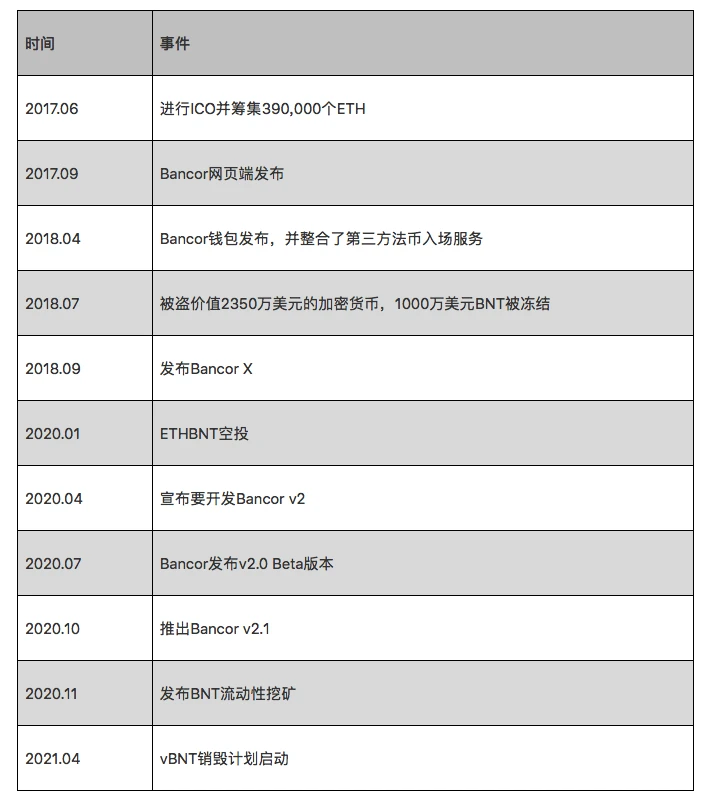

image description

Table 3-1 Major Events of Bancor

The Bancor team has been working on the Appcoin off-chain trading platform since 2012. The scale of its ICO in 2017 was also the largest at that time, and the actual scale far exceeded the teams financing plan. Bancor is the earliest AMM DEX. The original vision is to provide a trading market for long-tail tokens. The core is to create a liquidity pool bound to BNT for long-tail tokens and use algorithms to provide market quotes. Bancor is committed to the Ethereum ecology. In 2018, it cross-chained EOS and developed the cross-chain trading system BancorX, but the effect was not good, mainly due to the poor ecological development of EOS.

Since Bancor 1.0s algorithm needs to use BNT as the conversion token for token transactions, it needs to charge more fees and cause greater slippage. Therefore, compared with similar DEXs, Bancors transaction volume lags behind, and transactions on the Ethereum chain Most of the shares are concentrated on Uniswap. Bancor v1 has a small liquidity pool and large slippage, resulting in small transaction volume and low transaction fee income, which makes liquidity participants unwilling to provide liquidity, which also forms a vicious circle.

At the same time, it is also pointed out in the market that liquidity providers in AMM DEX are suffering impermanent losses (non-permanent losses), and AMM DEX usually does not support the provision of single-currency liquidity when providing liquidity, which also leads to the need for liquidity providers to Take risks on the price of multiple tokens.

As a result, Bancor hopes to improve its AMM model to make token conversion more efficient, increase transaction volume, and at the same time avoid multi-coin exposure risks and impermanent losses for liquidity providers. Bancor announced in April of the same year that it would launch v2.0. V2.0 initially used the oracle machine quotation scheme, but the AMM DEX scheme that has used the oracle machine to quote in the market proved that there were loopholes in this scheme. After Bancor released the v2.0 Beta version, it encountered some problems, and then suspended the upgrade, re-developed it, and directly entered the v2.1 stage. The v2.1 version realizes the non-permanent loss compensation and the liquidity provision function of a single currency.

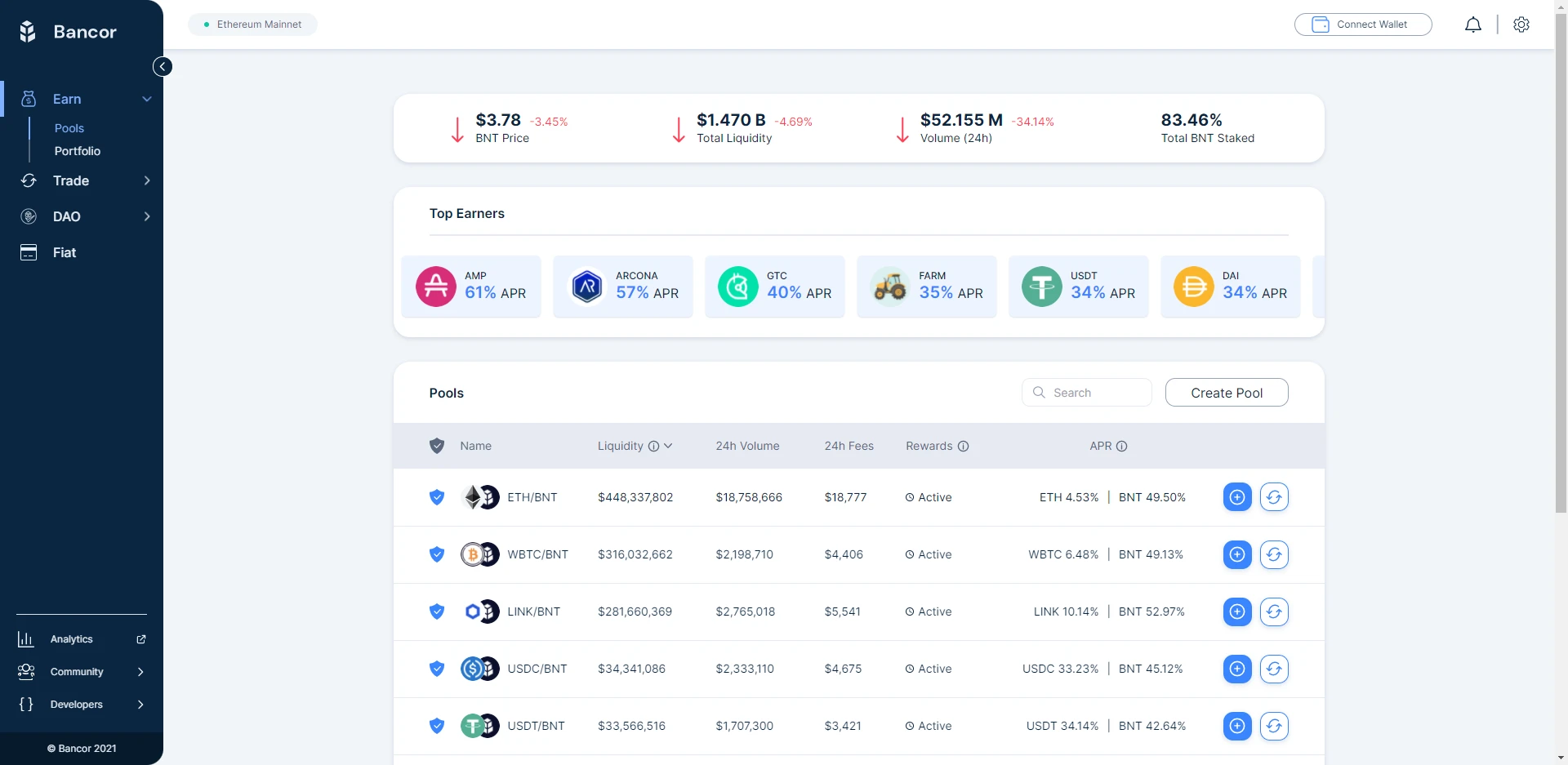

3.2 Status Quo

Bancor v2.1 has been running for 1 year. The following is the Bancor transaction data and relevant data since the operation of Bancorv2.

image description

Figure 3-1 Bancor transaction volume (2019.01-2021.11)

image description

Figure 3-2 Market share of Bancor transaction volume (2020.01-2021.11)

image description

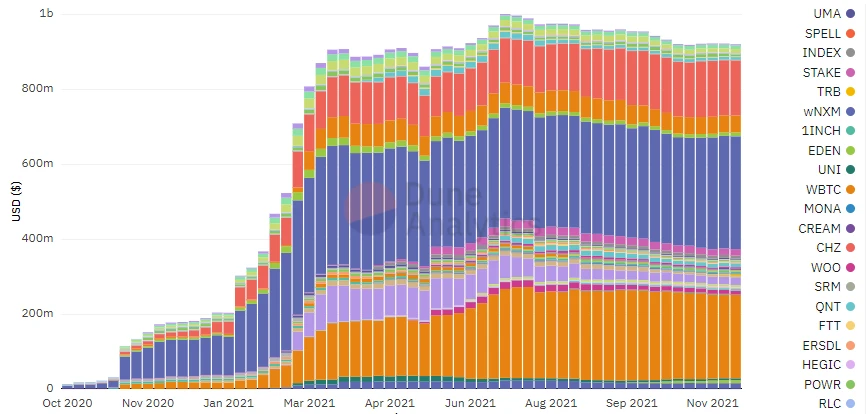

Figure 3-3 Total Liquidity Protection and Types of Tokens

According to Figure 3-3, currently Bancor supports about 80 types of tokens for liquidity protection. As of November 2021, the total amount of liquidity protection has reached nearly 1 billion US dollars, among which the most liquid tokens are: BNT (blue), WBTC (orange (bottom)), MATIC (purple), LINK (rose red) , ENJ (orange (top)), the total liquidity of these 5 tokens reached nearly 700 million US dollars.

image description

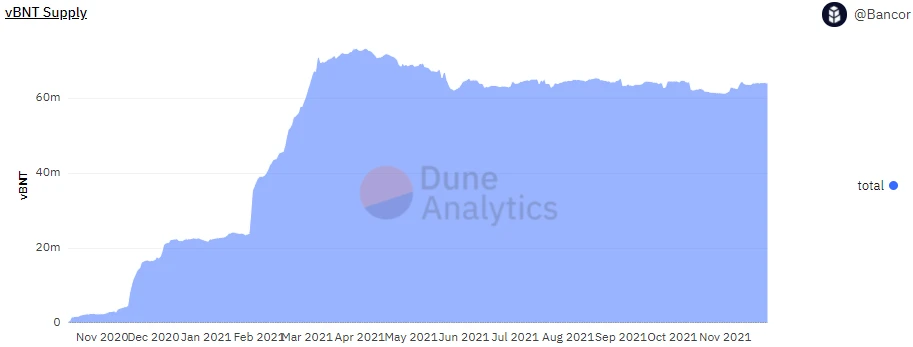

Figure 3-5 Total amount of vBNT

vBNT is approximately equal to the total amount of pledged BNT tokens. Starting from June 2021, the total amount of BNT deposits will enter a relatively stable stage. As of November 26, 2021,About 2% of the total vBNT has been destroyed, due to the small volume of vBNT/BNT transactions, the fee income is not much, and the vBNT destruction rate is not high. Combining with Figure 3-4, it can be speculated that after the release of Bancor v3, if the upper limit of liquidity protection is lifted and liquidity protection is realized at the same time, the total amount of BNT may rise rapidly for a period of time, but in Bancor After the total amount of liquidity in the pool reaches a relatively stable level, the total amount of BNT will also enter a stable period.

3.3 Future

According to the information disclosed by the team, Bancor will focus on v3 development and marketing activities in the past six months. The information currently disclosed is the first phase of Bancor v3, and the content of the second phase of v3 will be released later. The first phase of Bancor v3 is expected to be released in January 2022, the team will announce the second phase of v3 in February, and complete the second phase of development in March or April.

secondary title

4. Economic Model

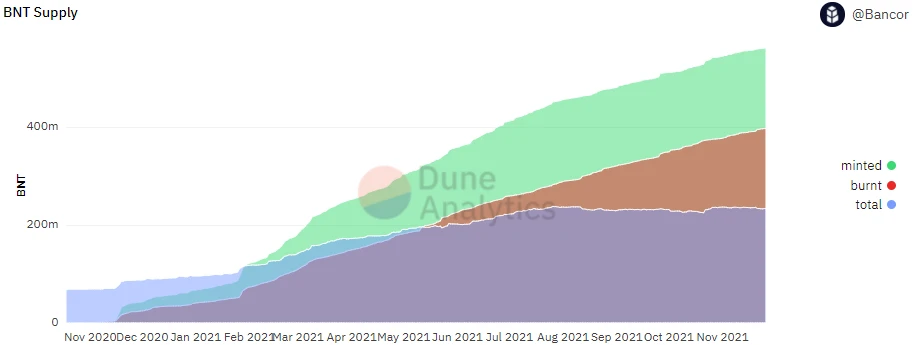

4.1 Supply

The total supply of BNT at the initial ICO was 79,323,978, and it maintained a dynamic supply for two years until the ETHBNT airdrop became a fixed supply, and the total supply became 69,148,642, a decrease of nearly 10 million.Liquidity mining

Liquidity mining

· The team will start liquidity mining in November 2020 for a period of 72 weeks (no more than March 2022).

· Bancor provides BNT rewards to liquidity providers in whitelisted pools every week. Large fund pools receive 100,000-200,000 BNTs per week, and medium-sized pools receive 10,000-20,000 BNTs per week.

· Every two weeks, two new tokens can be added to the liquidity mining program. Once activated, the token fund pool will continue to receive BNT token rewards within 12 weeks;

· Once activated, the token pool will continue to be rewarded with BNT tokens within 12 weeks.

· 70% of the BNT liquidity mining rewards will be allocated to the BNT side of the liquidity pool, and the remaining 30% will be allocated to the basic ERC20 (eg TKN) side.

· Initially set up 6 large capital pools and 2 medium capital pools.

4.2 Requirements

In the v2.1 version, there is an upper limit setting for the whitelist pool of liquidity protection, that is, there is an upper limit for the BNT forged by the protocol in a single pool and in the entire network. If the user needs to deposit other types of tokens, it is necessary to expand the amount of BNT tokens deposited by the user. Users who deposit BNT will receive vBNT, which can be used for governance and to obtain protocol transaction fees.

In Bancor v3, although it is still a simple deposit of BNT for LPs, v3 will actually automatically seek the optimal BNT revenue solution within the protocol to some extent, so it may increase the demand for BNT.

4.3 Analysis

Since there is no data on BNT tokens newly added through liquidity mining so far, the following content is only a rough judgment based on existing data.

BNT inflation mainly comes from 3 parts:

1) Liquidity mining;

2)The agreement forges BNT, which is not circulated in the market.This part of BNT will be destroyed as users add BNT to the pool or withdraw liquidity.

image description

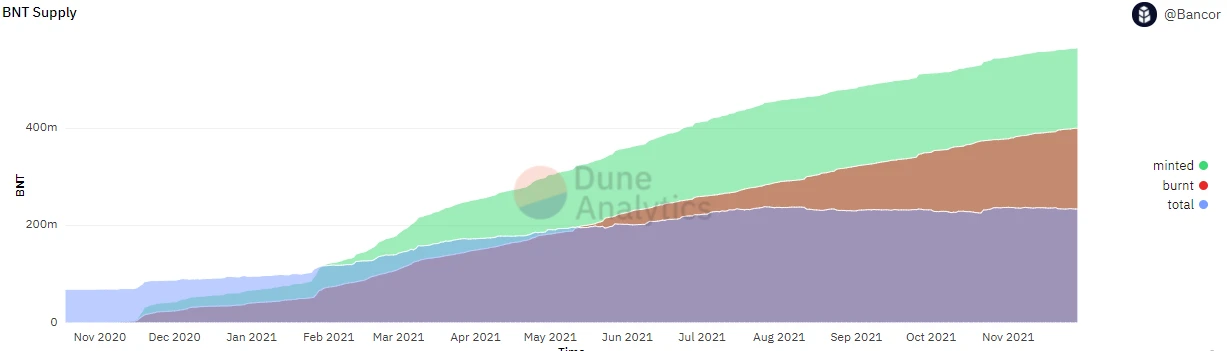

Figure 4-1 BNT Token Supply

Combined with Figure 3-3, the liquidity protected in the Bancor protocol has been basically maintained at about 1 billion US dollars since May 2021, so adding liquidity to the pool will result in a negligible increase in the system forging BNT. In Figure 4-1, the total amount of BNT tokens has increased from about 200 million to 230 million tokens in the six months from May 2021 to the present, an increase of 30 million tokens.

From May to now (24 months), assuming that 6 large pools (WBTC, ETH, LINK, DAI, USDT and other mainstream trading pairs) and 2 medium-sized pools are maintained for liquidity mining, then about 14.88 million ~ 2,936 additional coins will be issued Ten thousand BNT. At the same time, combined with the v2.1 summary released by the team, the protocol fees generated by the transaction can basically cover the impermanent loss compensation.Therefore, it can be concluded that the main reason for the current BNT token inflation is liquidity mining, rather than the protocol forging BNT to compensate for impermanent losses.

After the v3 version, because the total amount of liquidity protection may increase, the number of BNT tokens forged by the protocol will increase, so the total amount of tokens may increase accordingly, but the actual circulation of tokens is mainly affected by liquidity mining. Compensation for mining and impermanence loss forged BNT (if the handling fee cannot cover the impermanence loss).

And in the v2.1 version, the calculation of impermanence loss is settled after the end of the period, and the time period is lengthened, which can calculate the impermanence loss more accurately. In the v3 version, the function of instantaneous loss compensation is added, and it is expected to use the oracle machine to make quotations. This feature may create arbitrage space for the agreement and increase the pressure of the agreements impermanence loss coverage.

secondary title

5. Competition

5.1 Industry Overview

The subdivision track that Bancor belongs to is: DEX.

5.1.1 Status of DEX

image description

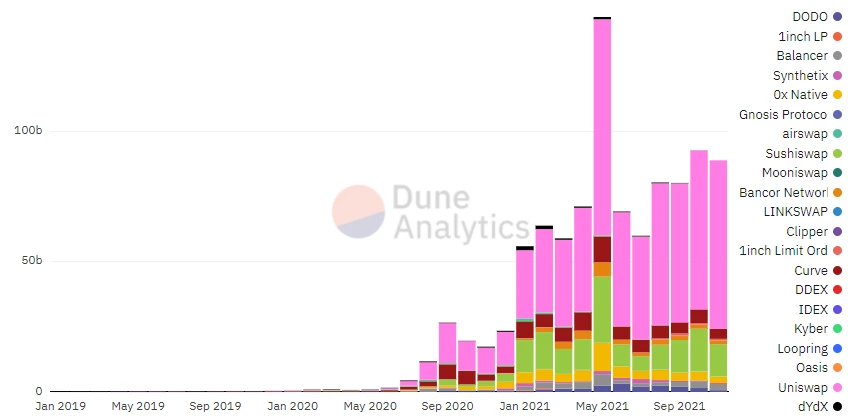

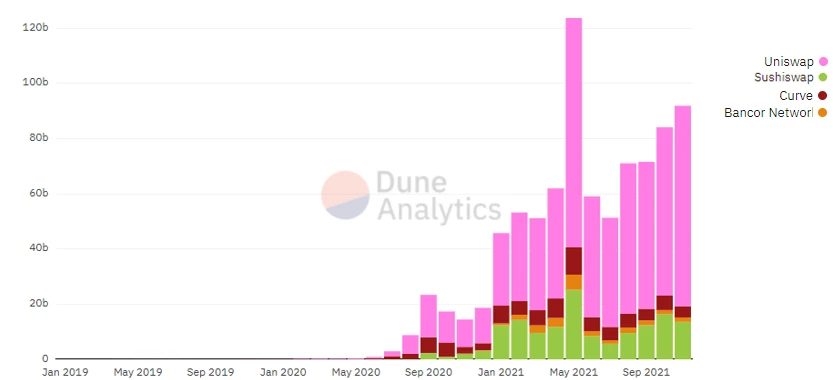

Figure 5-1 DEX monthly trading volume (2019.01-2021.10)

image description

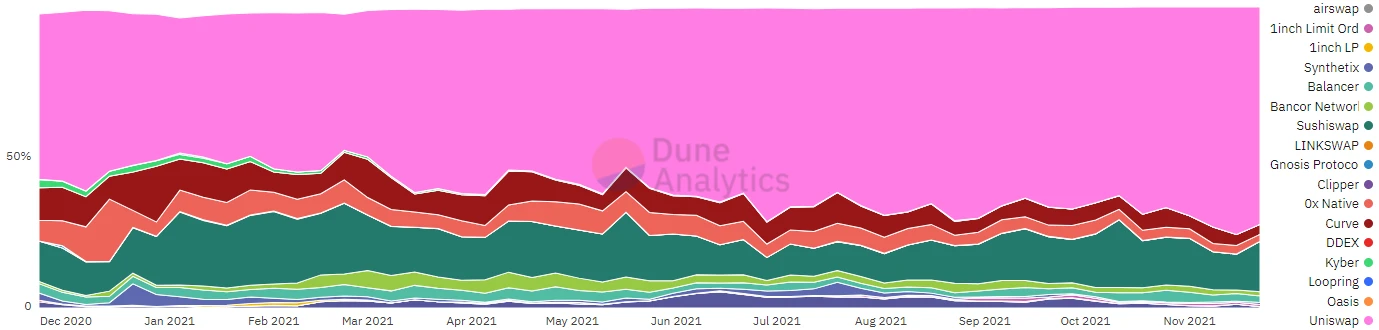

Figure 5-2 DEX market share (2020.12-2021.11)

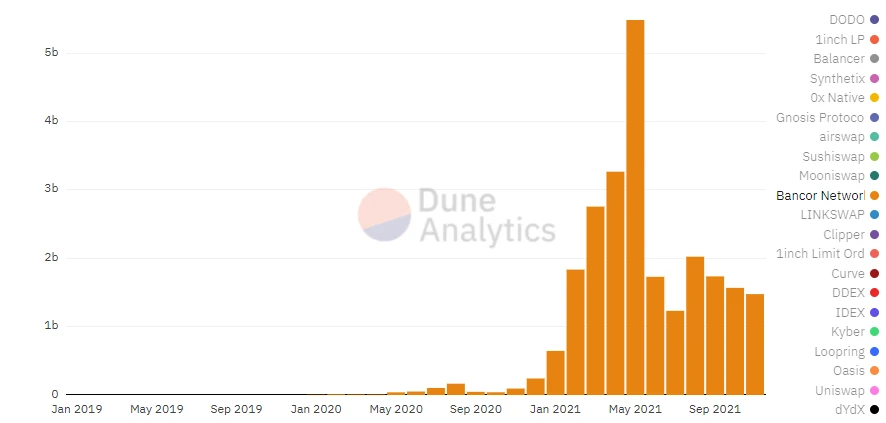

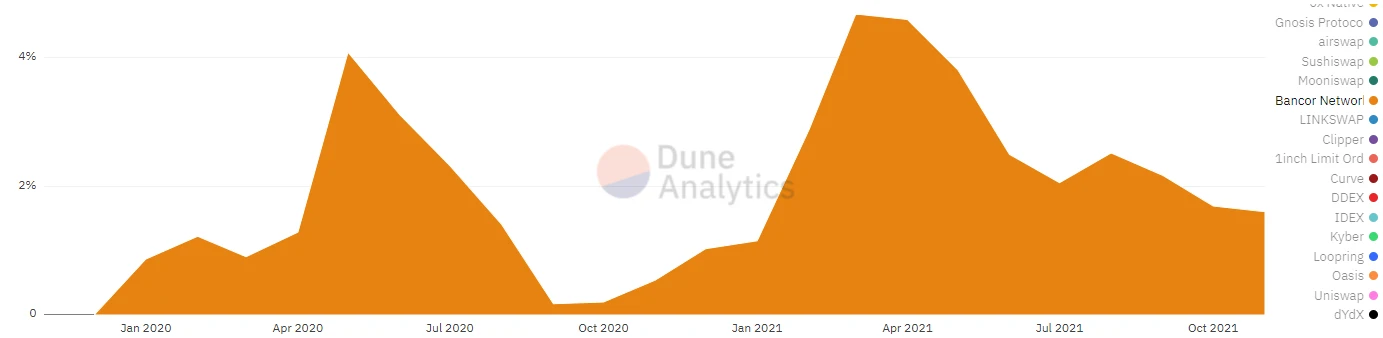

It can be seen from the figure that most of the transactions are concentrated in Uniswap (pink), Sushiswap (green), and Curve (big red). The remaining DEXs with a large market share include 0x Native (rose red), Balancer (blue) and Bancor (cyan). The proportion of Bancors transaction volume began to increase in March 2021 and reached its peak in May 2021. After June, Bancors transaction volume and market share decreased accordingly.

We have enlarged the transaction volume data of the past year to the weekly dimension level, and we can see the obvious and stable echelon stratification:

First echelon:Uniswap. Most of the time, it maintains more than half of the transaction volume share, and even reaches 75% share at most.

second echelon:SushiSwap, Curve, and 0x. The market share of Sushiswap is between 10% and 20%. Although the market share once exceeded 20%, the space was squeezed by Uniswap. Curve belongs to the anchor asset exchange agreement, maintaining a share of 6%~10%. 0x is the leader of the order book protocol, and most of the order book DEX bottom layer currently uses 0x.

Third echelon:Bancor, Balancer, DoDo. The occupancy rate has remained between 1% and 5% for a long time.

Fourth echelon:image description

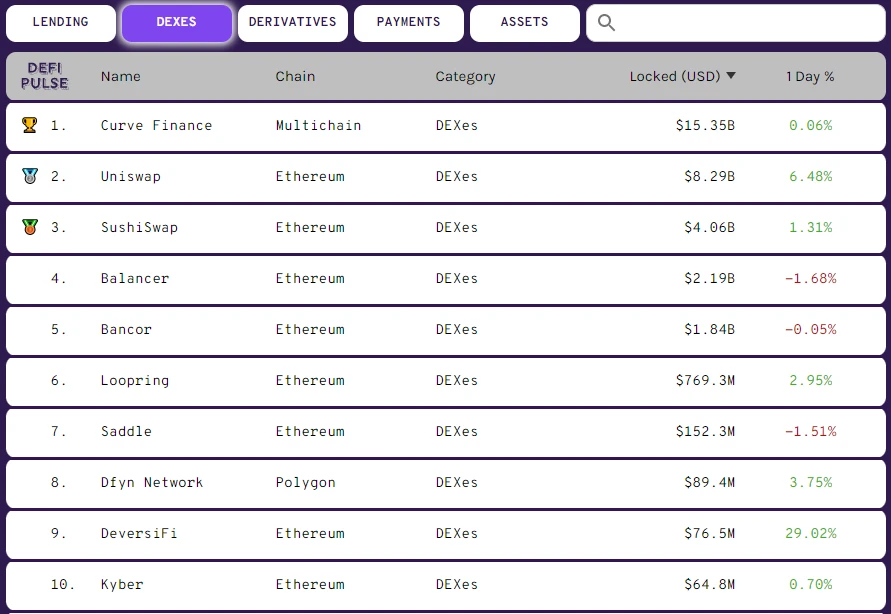

Figure 5-3 Top 10 DEX Liquidity

In AMM DEX, high liquidity usually means better trading price. Therefore, LP (liquidity provider) is an important participant of AMM DEX. In addition to factors such as security, the biggest attraction of DEX to liquidity providers comes from income, which usually includes transaction fee sharing and mining subsidies. As can be seen from Figure 5-3, Curve, Uniswap, and Sushiswap are in the first echelon, with TVL above $4 billion. (Curve counts the aggregated data of multiple chains, while Uniswap and SushiSwap only count the data on the Ethereum chain, so there is a big gap.) The second echelon is Bancor and Balancer, with a liquidity of about 2 billion US dollars.

5.1.2 Track Division

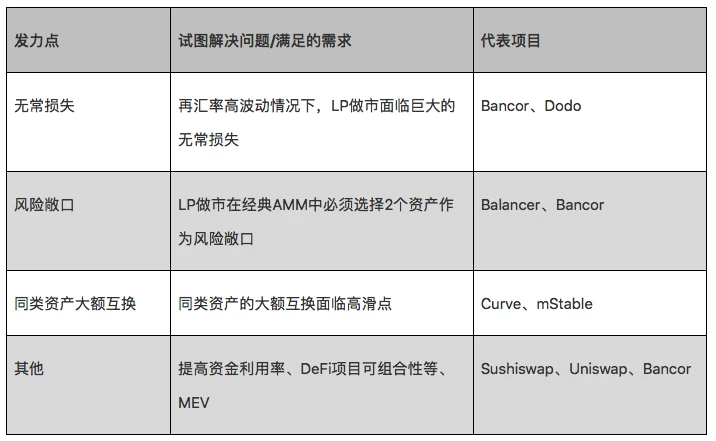

It can be seen from the data in 5.1.1 that,Uniswap stands firmly as the leader of DEX, and the rest of DEX compete for the remaining market share.The competition of DEX mainly comes from the competition on the supply side and the demand side. The DEX track is large, and there are many types of participants (traders, arbitrageurs, LPs (divided into individuals and market makers), project parties, and other DeFi projects), each with their own demands, soDEX has room for product differentiation strategies.

We mainly divide DEX into AMM paradigm and two subdivided tracks outside the AMM paradigm.

①AMM paradigm

image description

Table 5-1 AMM power point

Note: The above classification is divided according to the focus of the project business logic, and it is not perfect in form.

② Outside the AMM paradigm

From a very long-term perspective, the order book is the more ultimate model in form. Both parties to the order book can freely express their willingness to trade (price, quantity), but AMM can only choose one of the two. In mainstream finance, the order book is the most widely used paradigm. At present, blockchain and Defi are still in their early stages. Insufficient basic performance has led to high costs of orders. Insufficient liquidity has led to inefficient order book matching. AMM has emerged along with the trend and occupied most of the market. However, with the development of the second-tier and even the first-tier technology, the liquidity will become more and more abundant, which will most likely lead to a paradigm shift of the entire DEX.

5.2 Competition Analysis

The main task of Bancor is to compete with top DEXs for market share, so the following content focuses on Bancor’s development status and v3 improvements, and compares it with top DEXs (Uniswap, Sushiswap, Curve).

It should be noted that it is currently difficult to find a single indicator that can measure the pattern of the entire market, and trading volume and TVL are both important indicators. The calculation of impermanence loss is complex and cumbersome, so the following data does not consider the impermanence loss of the protocol.

Trading volume

Trading volume

image description

Figure 5-4 Comparison of transaction volume

image description

user

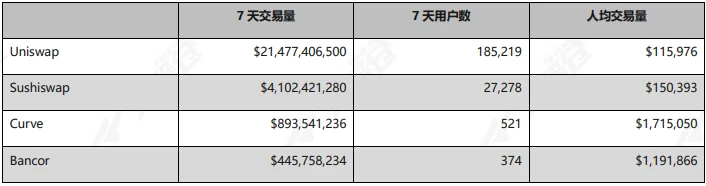

Table 5-2 Comparison of transaction data in the past 7 days

Combining Figure 5-4 and Table 5-2, it can be seen that Bancors trading volume and number of traders are much lower than Uniswap and Sushiswap, but the per capita trading volume is much higher than Uniswap and Sushiswap, just like Curve

Causes may include:

1) Uniswap and Sushiswap have a head effect, so they have become the first choice for project decentralized exchanges to list coins. Long-tail tokens have low liquidity and high slippage, and thus low trading volumes, driving down the average trading volume. At the same time, when the popularity of long-tail tokens is high, they can bring a huge transaction volume to the protocol, so they have a positive effect on the growth of the transaction volume of the protocol.

2) Curve is a benchmark asset transaction, and the mainstream assets have good liquidity, but the contract is complex, so the gas fee is expensive, and it is not suitable for small capital transactions.

income

income

The following data does not take into account the impermanent loss of the liquidity provider, and the actual income of the user should be the total income minus the impermanent loss.

image description

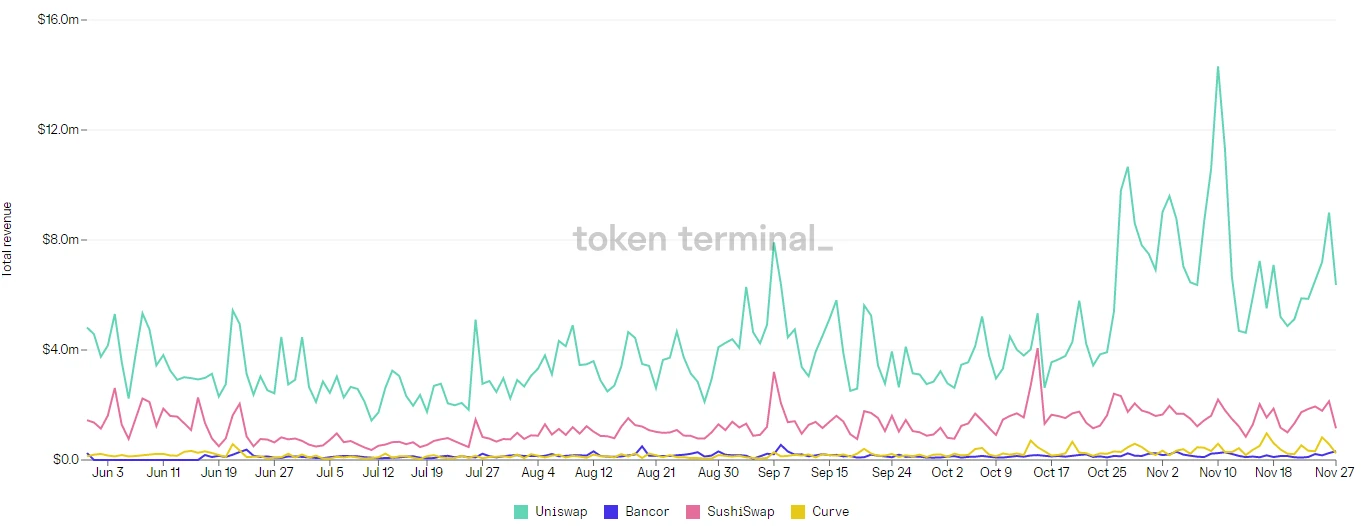

Figure 5-5 Comparison of agreement revenue (2021.06-2021.11)

According to Figure 5-5, the income of Uniswap far exceeds that of other DEXs, with an average daily income of more than 4 million US dollars, while the average daily income of Bancor and Curve protocols is around 100,000 US dollars.

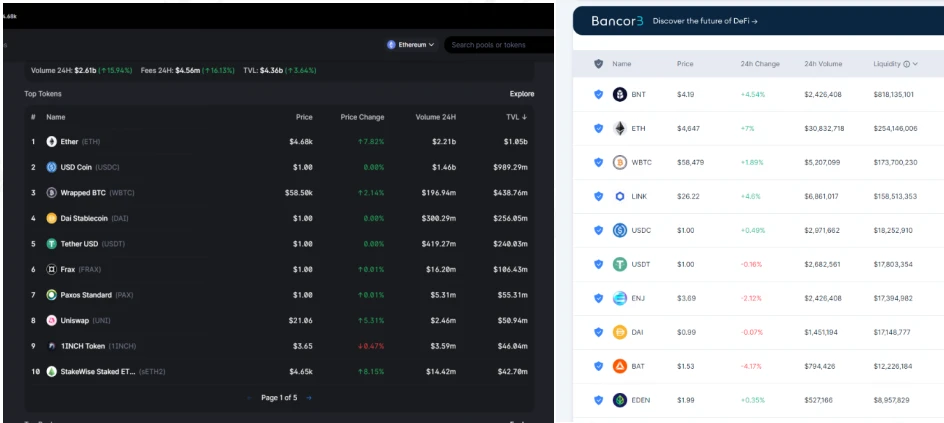

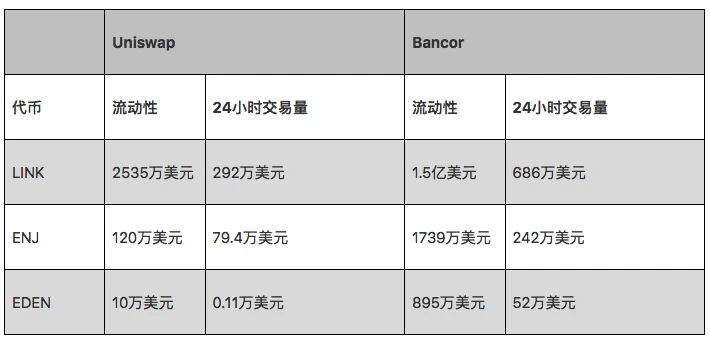

5.2.2 Liquidity

image description

image description

It can be seen from Table 5-2 that some of Bancor’s liquidity pools are competitive, and the reason for the small BNT trading volume is also that it has a small number of “healthy” pools and fewer types of tokens that can be traded normally . Because of the existence of liquidity protection, the biggest problem is that it limits the single currency addition of small currencies. Therefore, when the liquidity limit is lifted, Bancors small currencies have the opportunity to expand their liquidity and compete for a certain market share.

5.2.3 Impermanence Loss Scheme

At present, the DEX solutions for impermanent loss on the market are mainly Bancor and DoDo. Based on the practice of the past year, Bancors plan subsidizes liquidity providers who suffer impermanent losses through transaction fees, and forges BNT when necessary, so it can achieve 100% impermanent loss coverage. However, because the Dodo plan introduces the quotation of the oracle machine, and there is a difference between the quotation of the oracle machine and the real-time price in the market, it will suffer greater impermanent losses except for stable currency transactions. Dodos current largest source of transaction volume is stable coins.

That is to say, Bancor is currently the only DEX in the market that has successfully solved the impermanent loss problem, and its economic model is sustainable.

Summary: Judging from the current data, Bancors operation is better than that of the v1 version, but it still lags behind the top DEX, and it is difficult to compete for more market share from the top.

secondary title

6. Risk

paradigm shiftmarket competition

market competition

At present, the head effect in the DEX field is obvious. Uniswap, Sushiswap, and Curve have occupied most of the market share for a long time, forming their own ecology. Whether it is for the project party or for the users, it has formed a head effect.