MAV IEO has added another group of loss-making friends, and recently there have been many cases of getting trapped in the opening results of Binance's Launchpad/Launchpool. Although there was a recent rally, many people have not yet recouped their investments.

This article will help you understand the basic valuation logic of various projects, to avoid blindly rushing in at the highest point, and also review and compare the historical performance of Launchpool and Launchpad, and give a sharp evaluation of the similarities and differences between these two areas and the speculative strategies.

A. Valuation Logic

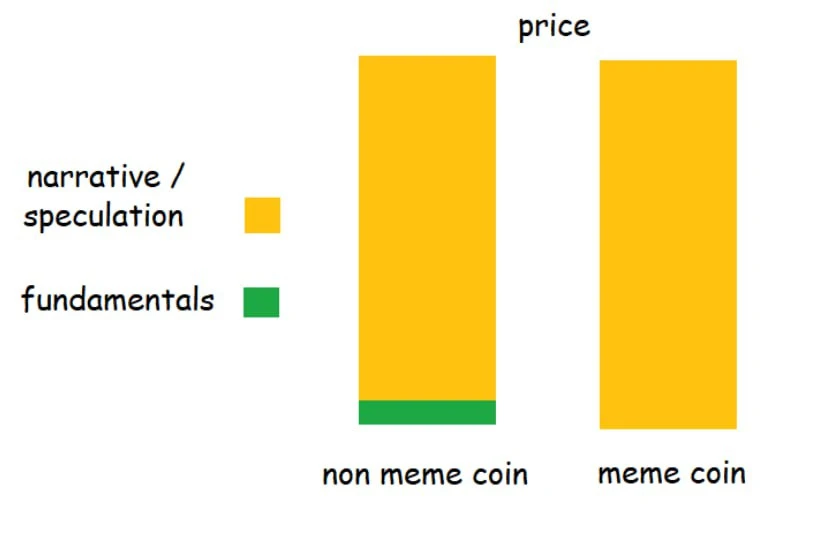

If it is not a "meaningless governance token" or a memecoin, it can theoretically be compared on a relatively large scale by comparing the benefits given to token holders. However, since cryptocurrencies are a game of attention, the so-called fundamentals are too insignificant in the face of narratives, so valuation is generally compared within the same type of projects.

For example, MAV belongs to the DEX track in the DeFi category. The common indicators for DeFi are TVL, which is a commonly used evaluation scale, and the total fee income and protocol income, which are not commonly used for evaluating profit-making ability. Specifically, for the DEX aspect, there is an additional trading volume indicator to evaluate business scale. As for the token itself, there are two indicators: the current market cap (mcap) and the fully diluted valuation (FDV), which correspond to short-term and long-term liquidity.

Refer to the valuation benchmark chart made by @BiteyeCN, which uses TVL or fee income as business evaluation indicators, and provides valuation advice under mcap/FDV. Of course, there are often some tricks behind the data. For example, the issue with evaluating MAV based on one week's fees is that MAV has an airdrop and is listed on Binance, so there is naturally no shortage of traders trying to boost trading volume, which inevitably results in an artificially inflated volume (3/n).

Using more refined logic and common sense to make judgments is also a good method. The price of MAV $0.5+ will lead to its FDV being close to Pancake. No matter how close the relationship between MAV and Binance is, it is still closer to Cake. So it is not very realistic to expect the price to exceed $0.5 with the backing of Binance. Before this, DEX Hashflow, which was also launched through Binance launchpool, currently has an FDV of around 400M, and the corresponding MAV price is below $0.2.

So if someone really wants to speculate based on "believing in Binance's vision", $0.5 is obviously already far beyond the range that the initial launchpool can support. Currently, the market price of around 0.45 is already a relatively high position.

DeFi projects are relatively easy to evaluate because they have practical earning capabilities due to their application focus. On the other hand, important user activity data for public chain projects are mostly artificially generated, and their reference value is low, with only the TVL data being barely reliable. Therefore, compared to data public chains, background seems to be more important. This is also one of the reasons why VCs are flourishing in this field, as seemingly brainlessly giving 10B to projects with good backgrounds.

Refer to the valuation of ARB that we boasted about in the past, based on TVL and ecosystem, a valuation of 2 times OP FDV was given. However, after ARB launched its token, the price difference was tremendous, which led to embarrassment. Instead, after some time, with the continuous decline in OP price, ARB successfully achieved a 2 times OP FDV.

B. FDV is not just a number

FDV = Total token circulation x Token price

When evaluating projects, people often prefer to use market capitalization (mcap) rather than FDV for comparison. However, this is mostly because newly issued projects with high popularity have low circulation, making mcap a cheaper option for comparison. But FDV is much more than just a number.

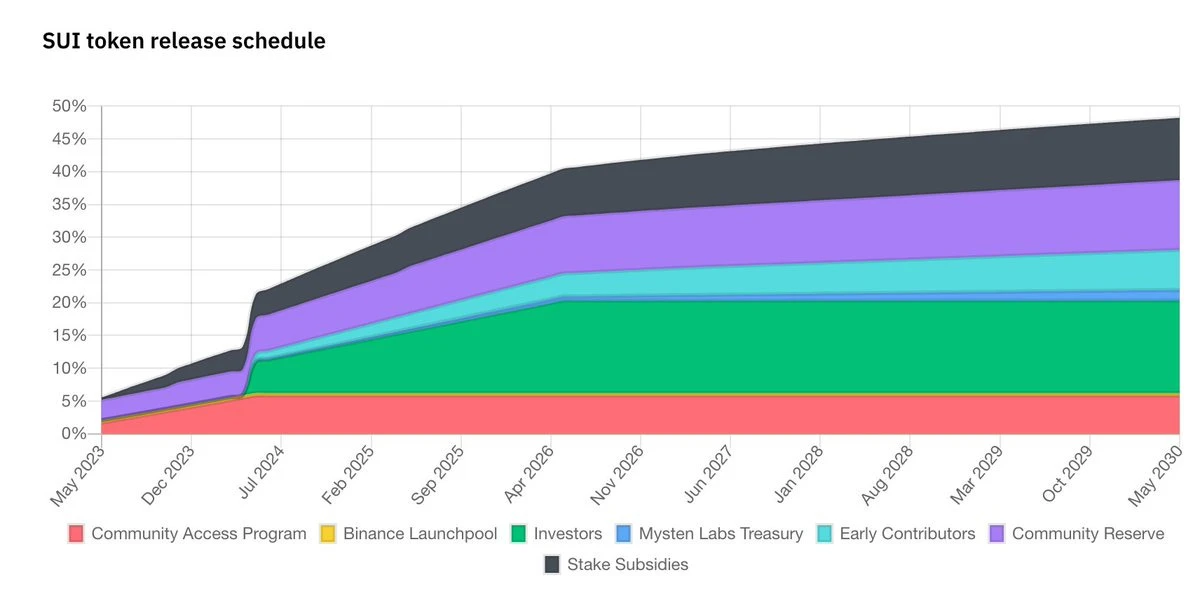

Take the example of SUI, which was part of the joint IEO conducted by OKX/Bybit/Bitget and also gave away 40 M tokens to Binance Launchpool to avoid repeating the mistakes of Blur. The price of SUI has been declining since its launch.

Recently, it was exposed that the project team was secretly unlocking and selling tokens, claiming themselves to have flexible tokenomics. This is the painful process of mcap gradually converging towards FDV, where the increase becomes selling pressure.

However, even if SUI follows the token unlocking plan honestly, its growth is also very fast. Benchmarking and short-term speculation led to SUI having a FDV of 10 B+ and an mcap<1 B at the opening. It can barely support it based on market hype. However, in the long run, it is natural for the price to decrease as the FDV slowly turns into mcap with no improvement in fundamentals.

C. Launchpool & Launchpad Differences and Speculation

Many people refer to MAV as the XX period Launchpad project, but it is actually a Launchpool project. What is the difference between Launchpool and Launchpad projects? Launchpool is free, Launchpad requires BNB holders to pay, which implies Binance's attitude towards them.

Especially for projects launched by Binance, it can be said that the implicit support for Launchpad projects is one level stronger than Launchpool. Previously, as discussed in the tweet, we have already discussed the overall return data of Launchpad.

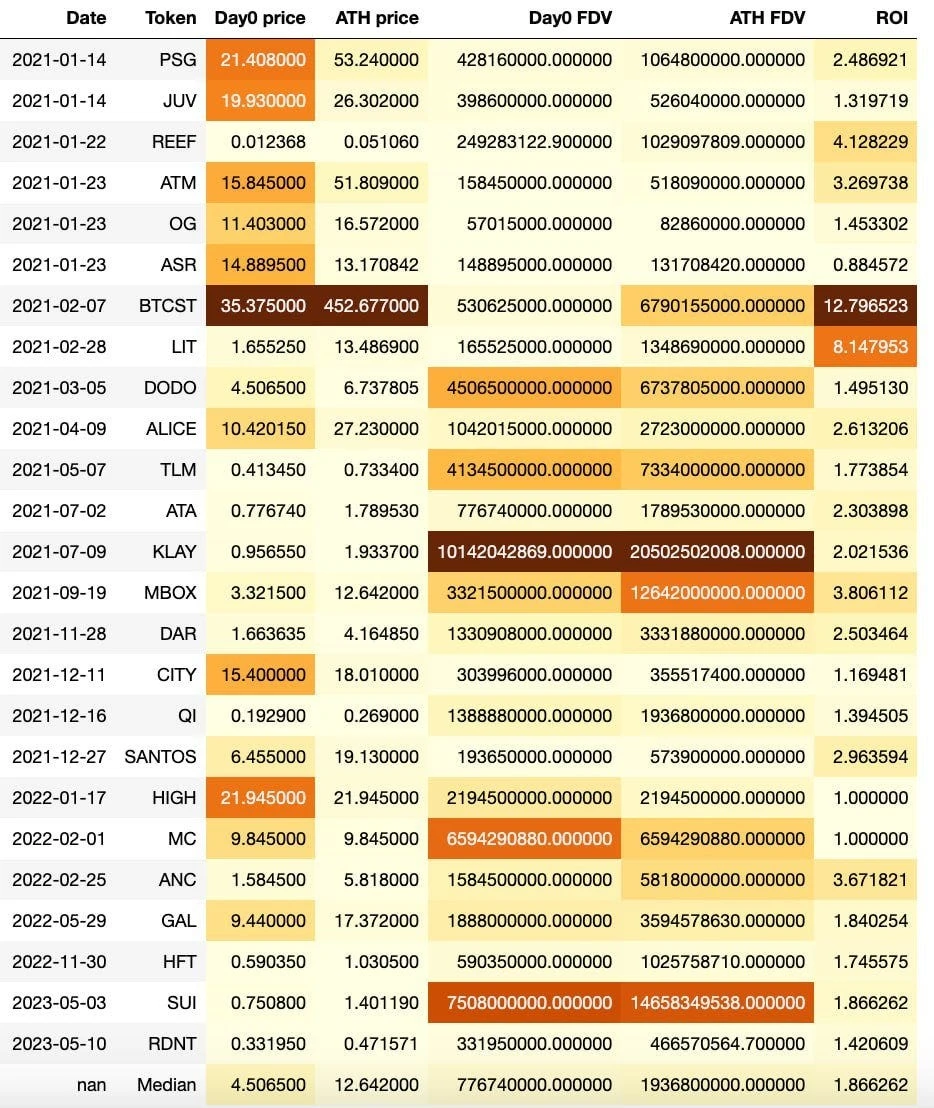

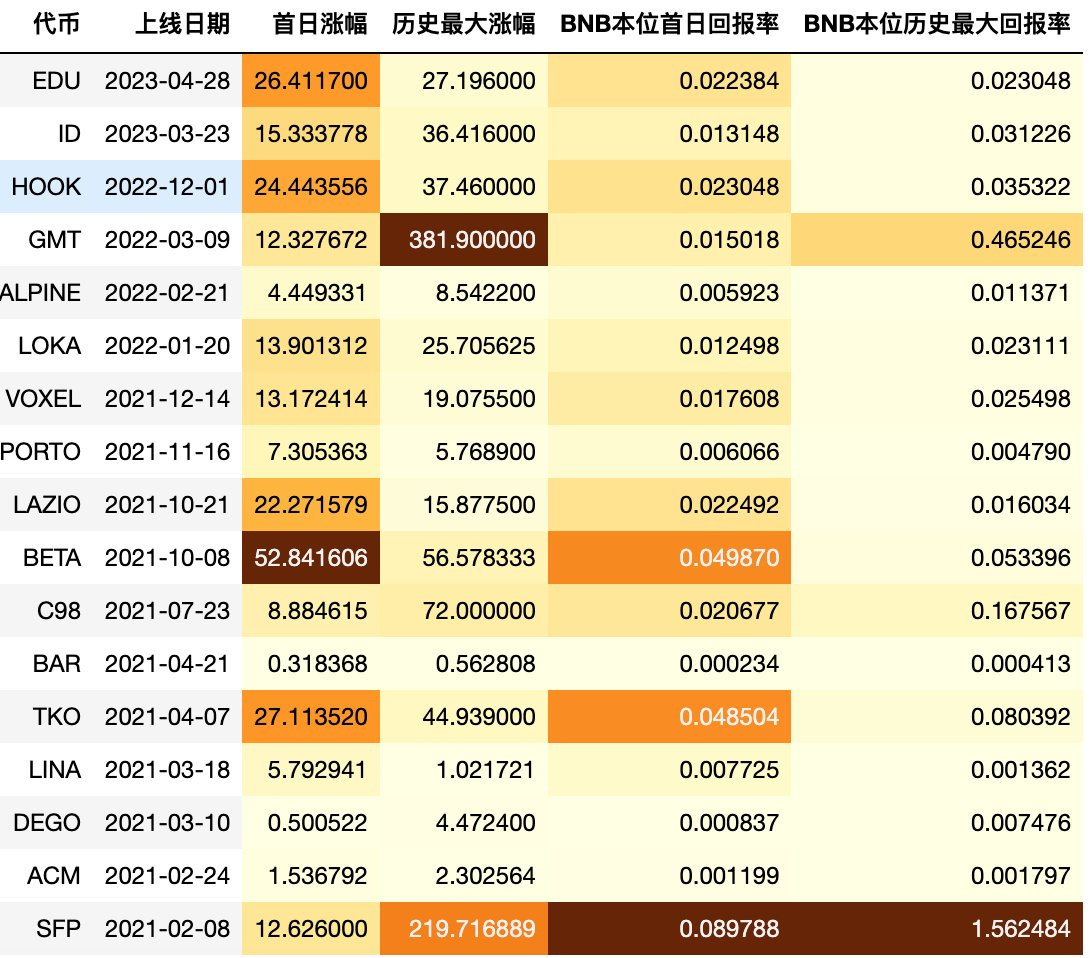

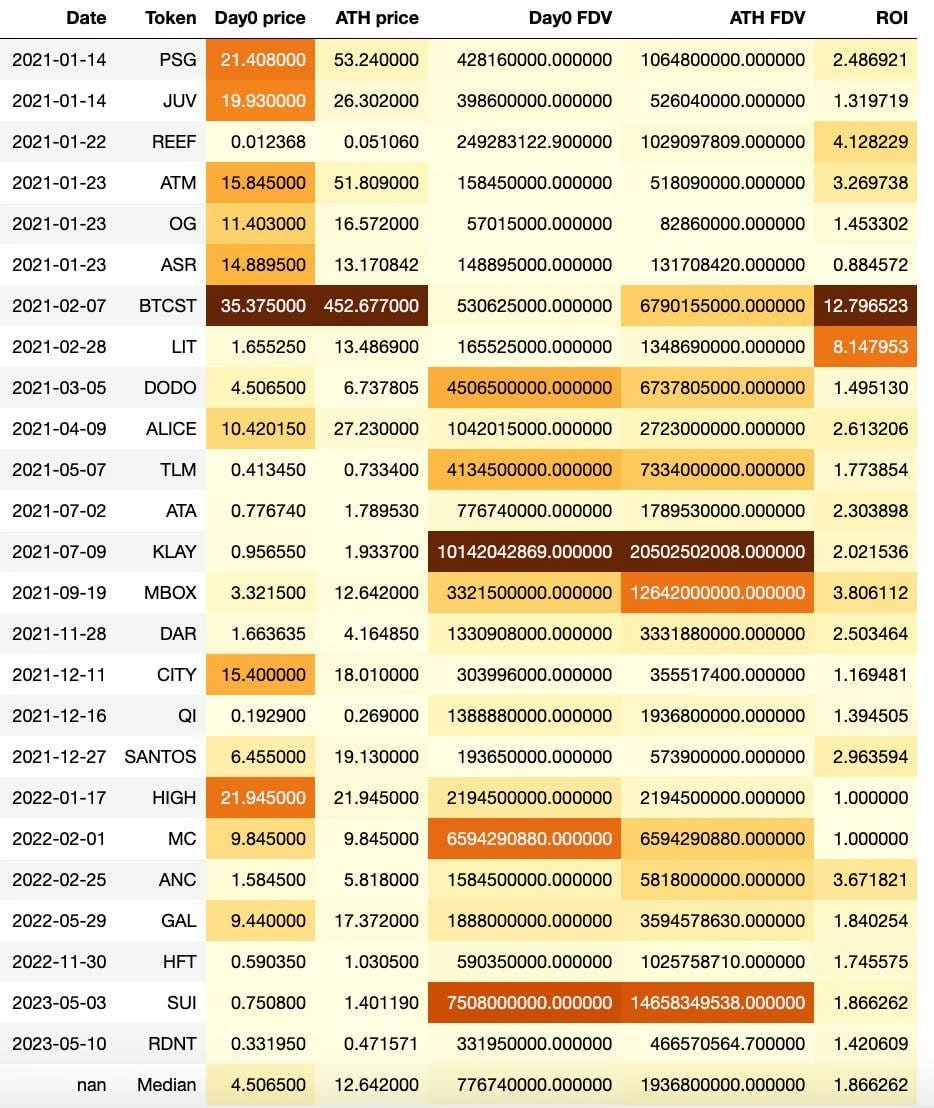

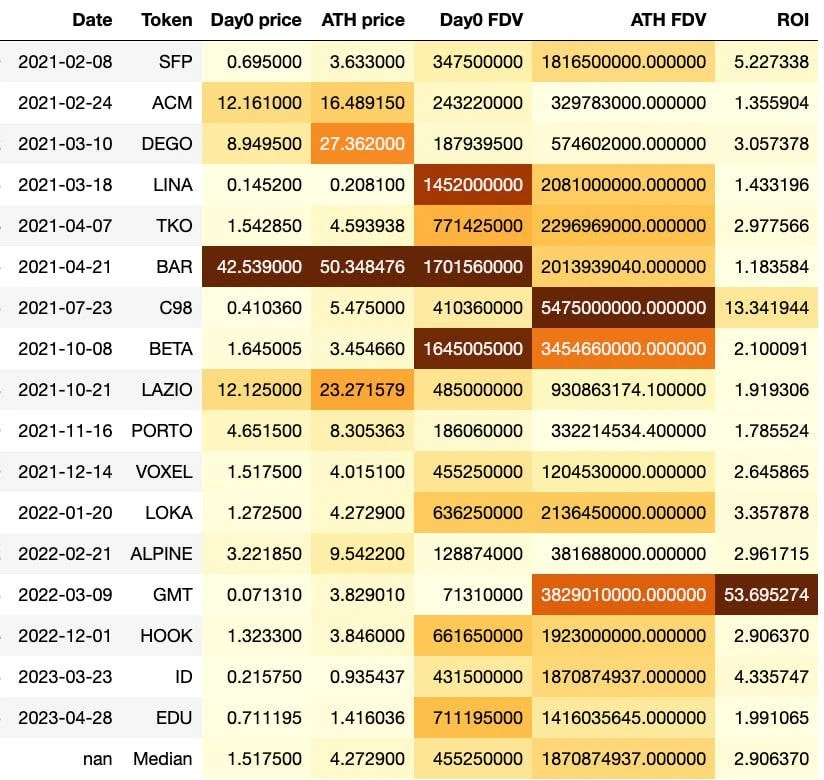

We will analyze from the perspective of opening the user's perspective this time, analyze the opening price (average price on the first day), the highest historical price (closing price), and the corresponding FDV, as well as the return on investment (ROI) of buying at ATH and selling at the opening price. The upper image is Launchpool data, and the lower image is Launchpad data. Focus on the median value in the last row (15/n).

From a historical data perspective, the performance of the previous Lauchpool project is far inferior to the Launchpad project. Assuming buying at the average price on the first day and selling at ATH, the median return on investment for Launchpad is 2.9 times, while for Launchpool it is only 1.9 times.

Moreover, Launchpool has two projects that reached their peak at the opening and have been stuck since then, while Launchpad has not experienced this situation yet (of course, the data of the average opening price is convenient for horizontal comparison but cannot reflect the whole picture, and it is highly probable that the EDU is still stuck since the opening day).

As for the reasons, we can observe that in terms of FDV ATH, Launchpad and Launchpool are actually close, both around 1.9 billion, but the median FDV on the first day of Launchpool is much higher at 780 million compared to 460 million for Launchpad.

This is mainly due to the liquidity issue of Launchpool. Launchpad generally provides around 5% of the shares, while Launchpool, as a free coin distribution, generally provides less, usually below 2%. Although the opening price of Launchpool is artificially high, since most BNB holders sell at the opening, the higher the opening price, the more advantageous it is for BNB holders. Therefore, Binance naturally has no strong motivation to differentiate this point.

For investors, the long-term game value of Launchpool is obviously lower than that of Launchpad, so it is necessary to do a good valuation analysis and be more conservative in preparation. Mindlessly rushing in and holding for the long term can easily lead to being stuck.

If you're lazy to estimate the value, refer to the median first-day FDV of 460M on Launchpad. Once the FDV of Launchpool's application projects exceeds this value, the probability of high returns in the future is not very high.

Summary

Using similar project valuations as a benchmark is the most common valuation method. Launchpool's project performance is not as good as Launchpad's. Due to liquidity issues, coin prices often start off artificially high, so caution is needed. There are a few cases where Launchpool's opening price has remained high since its launch, while Launchpad has basically never experienced a complete loss.