Original author: 0xLouisT

Original translation: TechFlow

God laughs at those who cherish causes and yet complain about the results of those causes. - Bossuet

In recent months, there has been a lot of discussion about the failure of ETH L2, but it is wrong. Many people blame L2 for ETHs poor performance and believe that the expansion plan is a failure. As the value of ETH falls, holders are looking for scapegoats, but we ignore the real problem - we are partially responsible for some of the root causes.

Cause and effect analysis

Lets look at the consequences that everyone complains about, which are actually quite obvious:

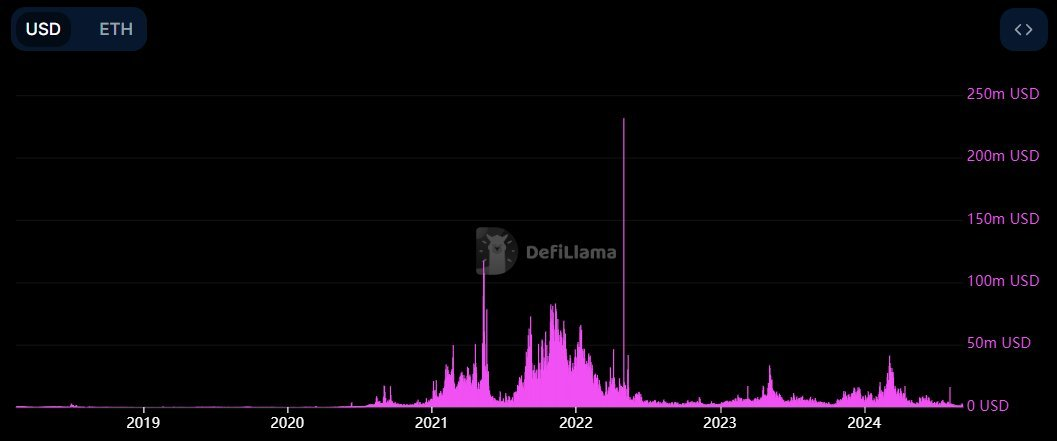

1. ETH revenue plummets: Ethereum is responsible for this due to its scaling roadmap. However, this does not mean failure. Ethereums scaling plan aims to achieve a 100x increase in the number of users by reducing fees and increasing throughput. The plan was to reduce transaction fees on L2 by 100x, which has been achieved. However, even with the sharp drop in fees, the number of users did not grow as expected, but has been decreasing since 2021. Even if the fees are reduced by 100x, if it is accompanied by 100x activity, the revenue will naturally stabilize and ETHs revenue will return to its previous level. Therefore, we need to increase the number of users of ETH by 100x.

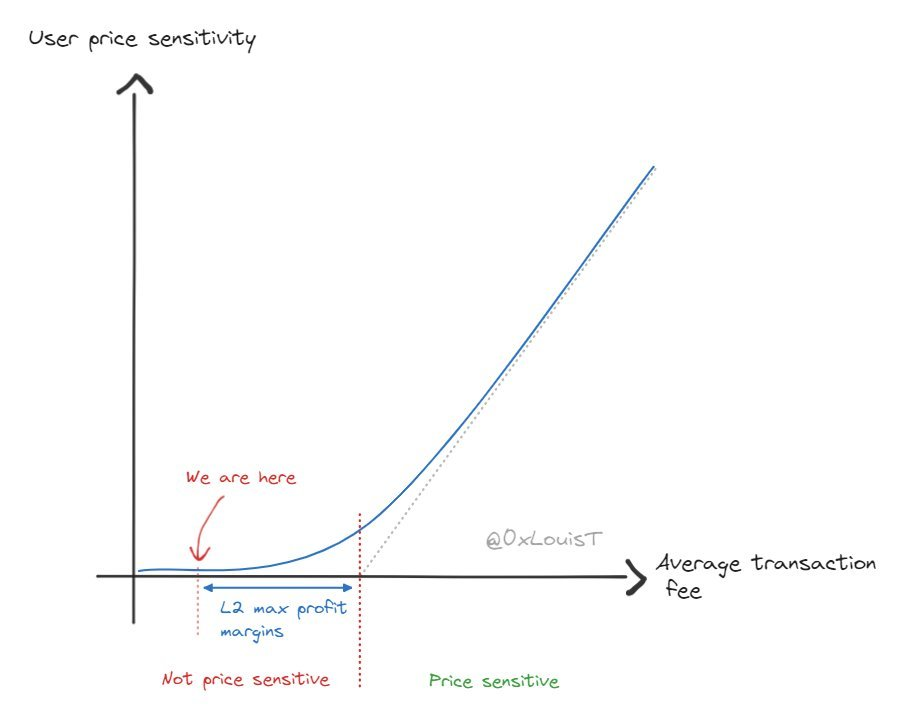

2. Impact of L2 on L1: It is true that L2 can set its own fees, and when the fees are only a few cents or dollars, users tend to be insensitive to prices. This mechanism is flawed because it allows L2 to make higher profits from user fees. -> Ethereum needs to regain pricing power.

3. L2s are not attracting enough users: L2s themselves are not a means to achieve 100x growth in users; they are a tool to facilitate growth, not a core driver. We need to rekindle user interest in Web3. -> We need to increase the number of users of ETH by 100x.

How to solve these problems?

We have identified two key issues that have fueled the L2 debate:

1. We need to increase the number of ETH users by 100 times

Lowering transaction fees alone will not restore demand for ETH block space. The key is: how do we achieve a 100x increase in the number of users? While there is no clear answer, the following factors may be crucial. My opinion is:

We need to attract users through new innovations and application scenarios.

A bull run will significantly increase the demand for ETH block space: prices can influence market trends. Imagine if the price of ETH reached $10,000, we wouldn’t be having these discussions now.

2. Ethereum needs to regain pricing power

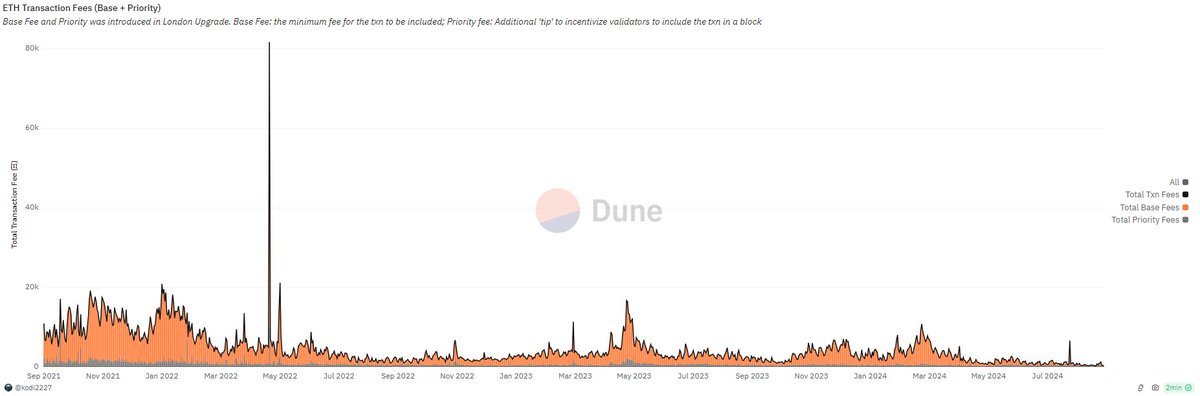

While ETH still has pricing power, the current situation is like a car driving in low gear. If L2 is making a lot of profit from user fees, it means that Ethereum may be priced too low. The root of the problem is that fees are set too low across the entire network. When fees are only a few dollars or cents, users are generally insensitive to price. However, if activity on all L2s increases, fees will gradually rise until they reach a critical point where users begin to pay attention (as shown in the figure below).

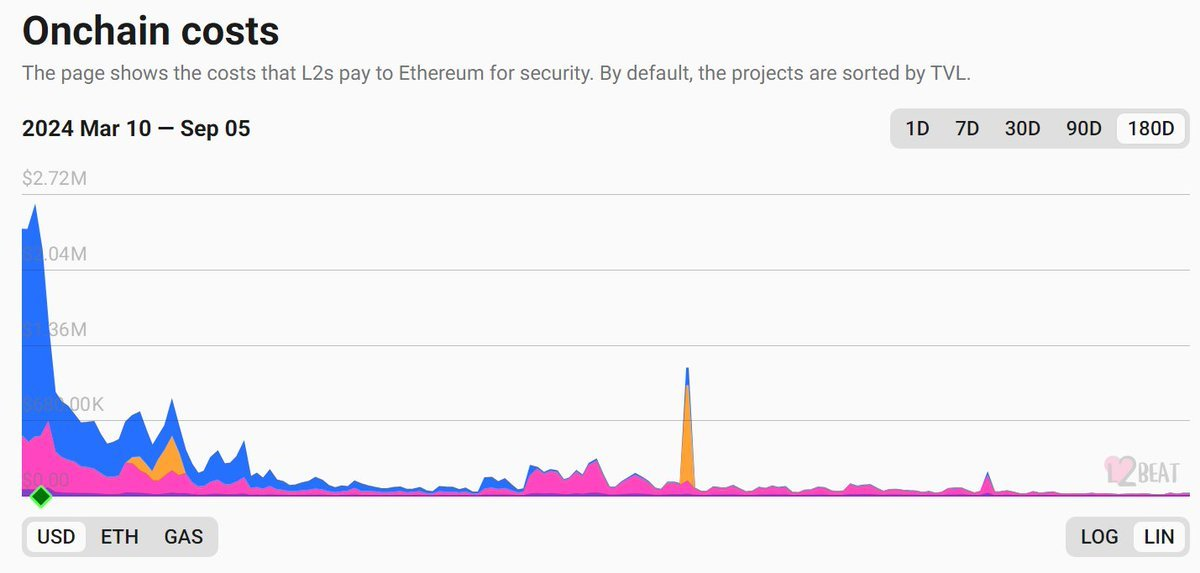

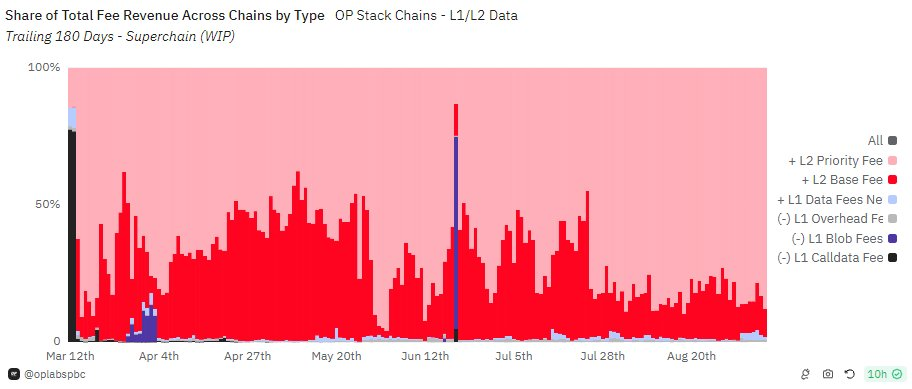

Currently, the base fee on L2 is too low relative to the priority fee (as shown in the figure below). Ideally, the ratio of base fee to priority fee should increase to reach a level similar to that on Ethereum L1 over the past few years (see figure below).

At that point, L2 will need to engage in intense price competition, reducing margins to remain competitive on fees. This is when ETH will begin to regain pricing power (as shown in the chart below).

Ultimately, it can be seen that Ethereums expansion plan did not anticipate operating at such a low number of users. In order to regain pricing power over L2, ETH needs to increase the number of users to 100 times the current level. The network was not designed for such low usage.

Two non-contradictory viewpoints

Finally, let’s explore the two main visions often mentioned by Ethereum holders:

1. ETH as sound money: Since the implementation of EIP-1559, ETH has entered a deflationary state, which is consistent with its vision of being a sound currency. However, due to the lower transaction fees caused by the emergence of L2, this vision seems less convincing and lacks consensus.

2. ETH as a scalable computing network: Scalability planning shifts ETHs vision toward becoming a cheap and scalable computing network, prioritizing scalability over its deflationary and sound money properties.

At first glance, these two visions seem completely incompatible, but they are not. Both rely on demand: if activity surges to 100x its current level, the increased fees will push ETH back into deflation. Ethereum can achieve both sound money and scalability as a computational network. The key is the increase in activity.

In short: Ethereum’s L2 roadmap has been successful in terms of scaling, but this is only half the battle. It is incorrect to blame L2, technology, or even Vitalik for ETH’s revenue and price performance issues. The real challenge lies in attracting 100x the current users; without these users, ETH will risk losing influence.