Original article by @Web3_Mario

Powell may be caught in the crossfire. Macro data is not enough to cause the market to panic about monetary policy risks.

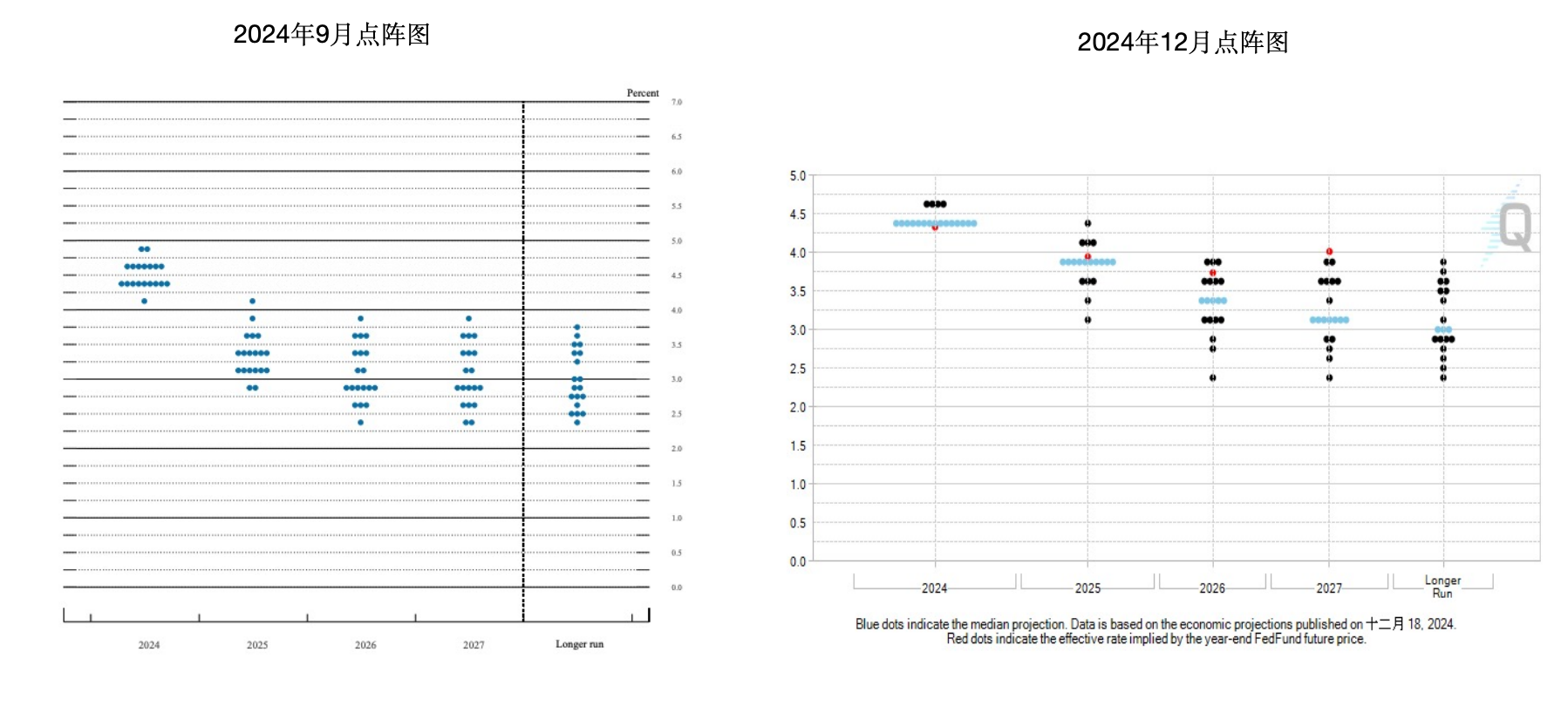

The FOMC interest rate decision in the early hours of last Thursday was in line with market expectations, ending with a 25 BP reduction. The market generally attributed the decline in the risk market to two aspects. First, the dot plot showed that there was no unanimous consensus in this meeting, among which Cleveland Fed Chairman Hammack tended to keep the interest rate unchanged. In addition, the median target interest rate for 25 years was raised to 3.75% ~ 4.00%. Compared with the median target interest rate of 3.25% ~ 3.5% in the last September dot plot, the expectation of interest rate cuts was lowered from 4 times to 2 times. Here is a brief introduction. The so-called dot plot refers to a chart tool used by the Federal Reserve to express the expectations of monetary policy makers on the future interest rate path. It is part of the Summary of Economic Projections (SEP) released at the Federal Open Market Committee (FOMC) meeting, usually released four times a year, mainly used to observe the policy consensus within the Federal Reserve.

In addition, in the subsequent QA session, some of Powells remarks were interpreted by the market as hawkish guidance, mainly in two aspects: first, he seemed to show a concerned attitude towards the inflation outlook for the next year, and Powell did not give a positive response to the Feds attitude towards establishing Bitcoin reserves. However, after reading the full text, it seems that Powells concerns about inflation risks do not come from changes in certain macro indicators, but more from the uncertainty of Trumps policies. At the same time, he also revealed enough confidence in the outlook for the future economic prospects.

In addition, in the subsequent QA session, some of Powells remarks were interpreted by the market as hawkish guidance, mainly in two aspects: first, he seemed to show a concerned attitude towards the inflation outlook for the next year, and Powell did not give a positive response to the Feds attitude towards establishing Bitcoin reserves. However, after reading the full text, it seems that Powells concerns about inflation risks do not come from changes in certain macro indicators, but more from the uncertainty of Trumps policies. At the same time, he also revealed enough confidence in the outlook for the future economic prospects.

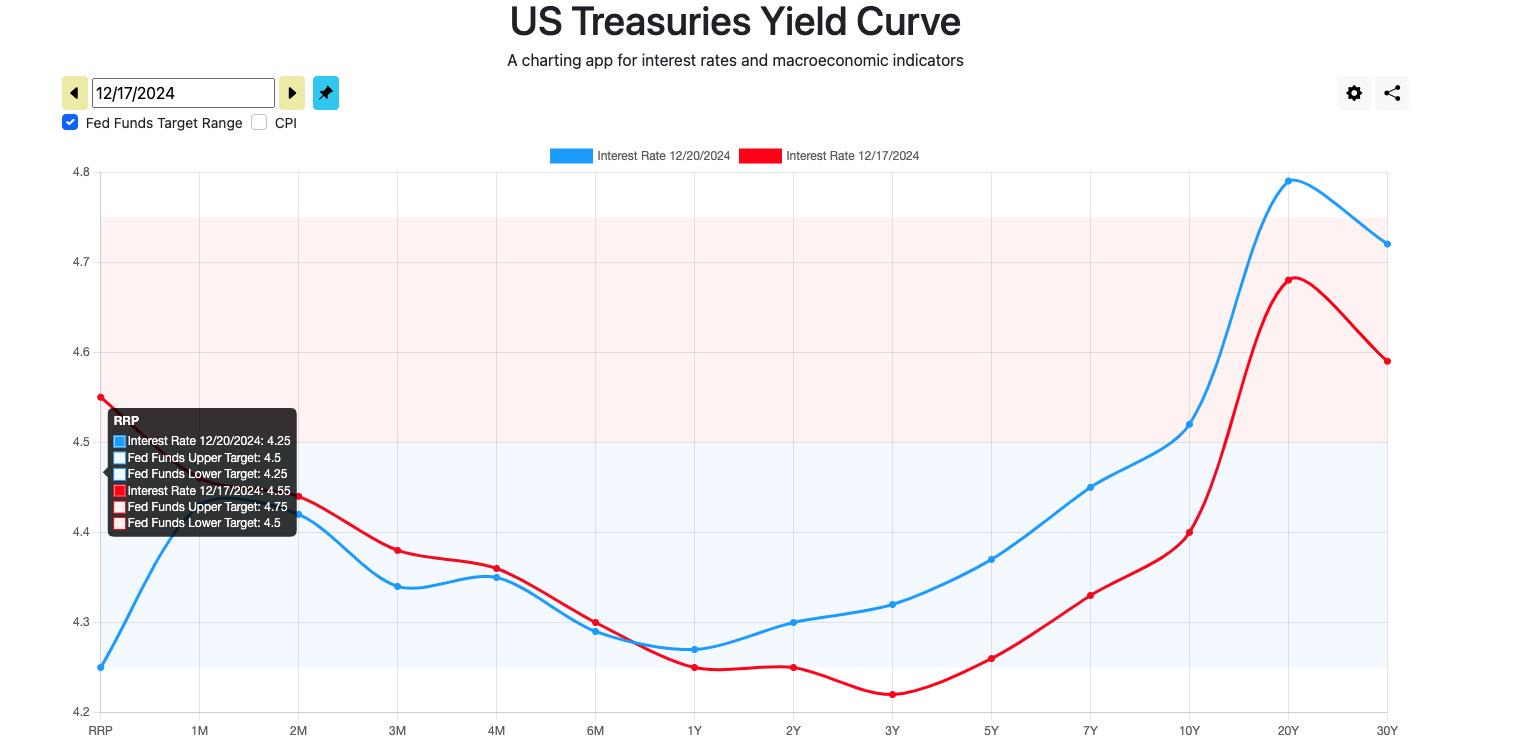

So lets take a look at why we say that. First, lets look at the changes in the U.S. Treasury yield curve before and after the Feds decision and related content were made public. We can see that long-term interest rates have indeed risen, but the impact on the 1-year yield is not very large. This shows that the market does have more concerns about the long-term economic outlook, but at least the risks are not occurring in the short term.

From the price of the 30-day federal funds futures contract expiring in December 2005, we can see that the market has actually reacted to the prospect of two future rate cuts as early as November. Therefore, it seems insufficient to attribute the correction mainly to the risk of the Feds future interest rate decision. I would like to add that the calculation of the implied interest rate is 100 minus the current futures price.

Next, lets look at several sets of macro data, including the PCE index, non-farm and unemployment rates, and GDP growth details. It can be seen that the US PCE index has not risen significantly at least in the past period of time. Both the year-on-year growth rate of PCE and the year-on-year growth rate of core PCE have remained below 2.5. At the same time, the expected inflation rate of the University of Michigan has remained stable, and the unemployment rate has not increased significantly. At the same time, non-farm in November has also increased compared with the previous period, which also shows that the job market has also shown a strong side. Considering Trumps tax cuts and GDP growth has stabilized in the end, and there has been no obvious decline in any item. Therefore, from the perspective of macro data, there is no data to support the judgment of inflation rekindling or economic recession in the next year. This also shows that Powells concerns still come from Trumps uncertain policy effects.

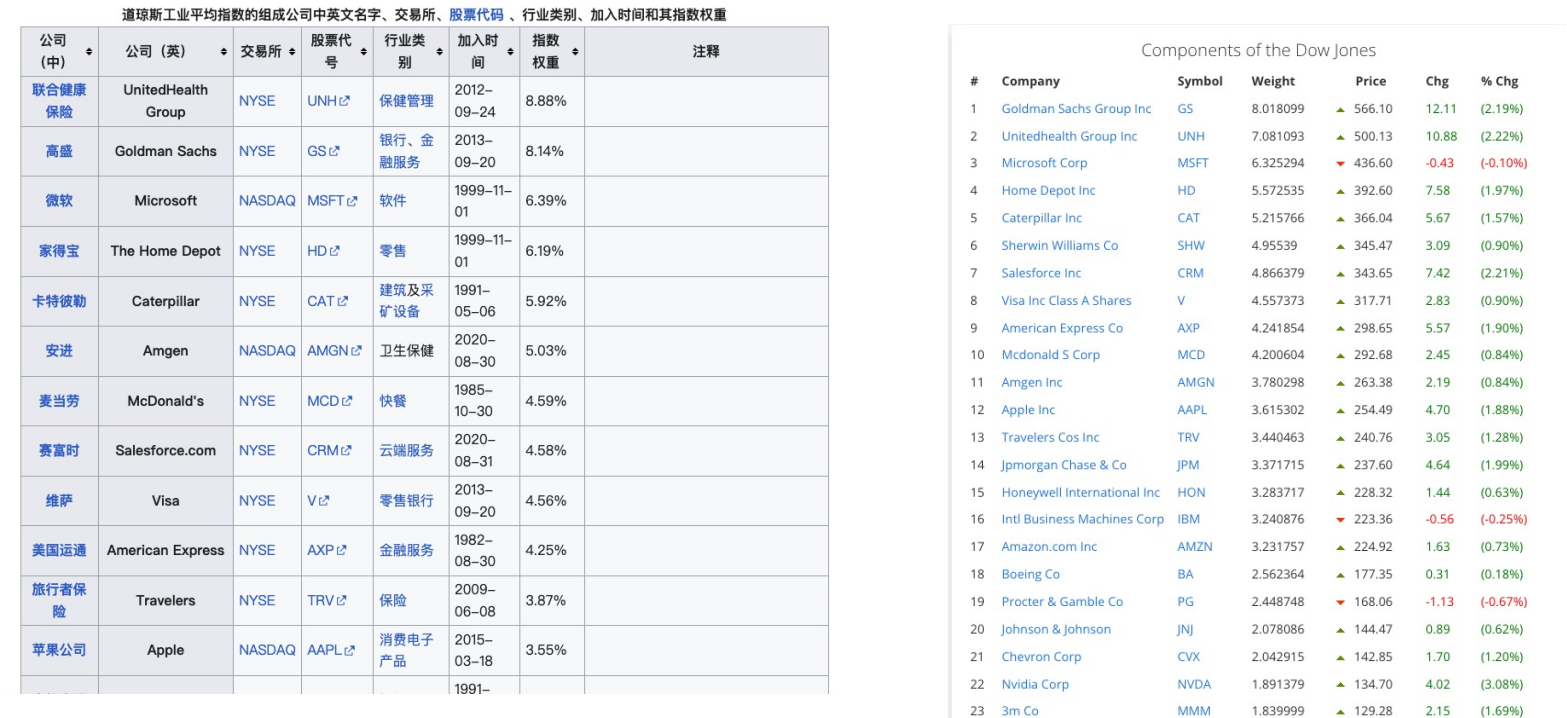

Here is another point to explain. The Dow Jones Index has been falling for a record period. Some people think that this reflects the markets pessimism about the future prospects of US industrial development. However, after a detailed understanding, it seems that the main reason for this impact is not systemic risk, but mainly due to the sharp downgrade of UnitedHealthcare. First of all, the Dow Jones Industrial Average (DJIA) is a price-weighted index, which means that the impact of the price of each component stock on the index depends on the absolute value of its stock price, not its market value. This means that high-priced targets will have higher weights in the Dow Jones Industrial Average. As of November 2, 2024, UnitedHealth Group has the highest weight in the Dow Jones Industrial Average, accounting for 8.88%. In the latest individual stock weights, UNHs weight has dropped to 7.08%. The share price has dropped from 613 on December 4 to the current 500, a drop of 18%. Other high-weight stocks have not seen such a drop. Therefore, the main reason for the decline in the Dow Jones Industrial Average is the single-point risk of the high-weight stock UNH, rather than the systemic risk. So what happened to UNH? The main cause was that UNH CEO Brian Thompson was shot several times by a gunman outside the Hilton Hotel in Manhattan, New York on December 5 and died after being sent to the hospital. The gunmans name is Luigi Mangione, and he has a good social background. The interrogation process showed that his behavior was more due to UNHs exploitation of the American people in terms of medical insurance, which aroused widespread sympathy for him in society and triggered the long-standing contradiction of expensive medical costs in the United States. This is also in line with Trumps medical insurance reform policy direction. Therefore, the resonance of the two caused the stock price to plummet, which will not be elaborated here.

Of course, regarding the episode about Bitcoin reserves, I think Powell’s attitude is not too important. As he said, the decision on whether to promote this proposal lies with the congressmen, not the Fed. At the same time, referring to the establishment and management framework of the US oil and gold reserves, the former is managed by the US Department of Energy, and the latter by the Treasury Department. Of course, the management process involves the collaboration of other departments, such as the SEC, CFTC and other regulators, as well as the policy influence of the FED. However, in this process, these departments play a more collaborative role.

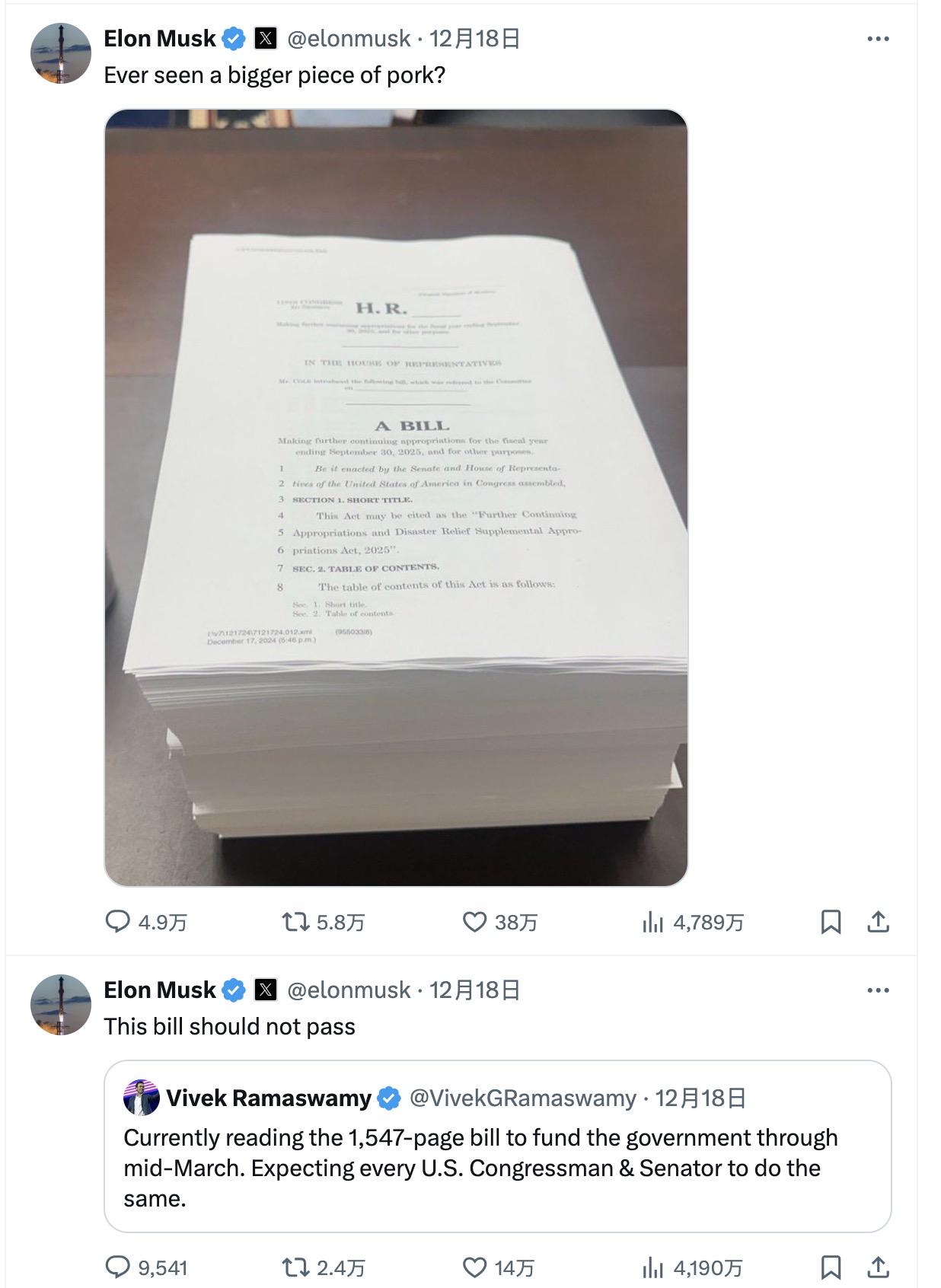

So why did the market react so violently? I believe the main reason is that the uncertainty caused by the strong pressure on Congresss short-term spending bill launched by Trump and Musk last Wednesday, and even threatening to cancel the debt ceiling rules, has triggered risk aversion among funds.

Trump and his powerful accomplices threatened to permanently lift the debt ceiling, casting a shadow on the traditional US dollar credit system, and the market began to hedge

I dont know how many of you have paid attention to the short-term spending game in the U.S. Congress last week. On Tuesday, December 17, House Speaker Mike Johnson reached a short-term agreement with the Democrats on government spending, which would extend government funding until March next year to avoid a government shutdown. At the same time, in order to pass the bill, Johnson also made some concessions to the Democrats and attached several bills that were supported by both parties. However, on December 18, Musk began to madly criticize the proposal in X, believing that the proposal seriously infringed the rights of taxpayers, resulting in the proposal being quickly rejected.

At the same time, the whole process has also won the support of Trump. Trump claimed in True Social that Congress needs to abolish the ridiculous debt ceiling rules before Trump officially takes office on January 20, because he believes that these debt problems are caused by Biden’s Democratic government and should be solved by him. After that, the Republicans quickly amended the new spending bill, not only deleting some compromise expenditures, but also supplementing the proposal to abolish or suspend the debt ceiling. However, the proposal failed to pass the House of Representatives on Thursday (December 19) with 174 votes in favor and 235 votes against. This also triggered the risk of a government shutdown. Of course, the House of Representatives finally passed a new temporary spending bill on December 20, which was only a few hours before the deadline. The proposal to modify the debt ceiling was deleted from the proposal.

Although the new spending bill was passed, avoiding a partial shutdown of government departments, I believe that Trumps attitude towards the abolition of the debt ceiling has obviously caused market concerns. We know that Trump has the greatest power among all US presidents, especially in the House of Representatives, where he has absolute say. The new members of the House of Representatives will be sworn in and officially take office on January 3. At that time, the possibility of passing the abolition of the debt ceiling will be greatly increased. So let us analyze the impact of this.

The U.S. debt ceiling refers to the maximum legal amount that the U.S. federal government can borrow. It was first established in 1917. This amount is set by Congress to limit the growth of government debt. The purpose of the debt ceiling is to prevent the government from over-borrowing, but it is not actually an effective means of controlling debt levels, but rather an upper limit on what the government can legally borrow. In addition to establishing fiscal discipline, the debt ceiling is also a very important weapon in the game between the two parties. Often, the opposition party will gain more bargaining chips by attacking the ruling partys spending bills and the risk of a government shutdown caused by it.

Of course, the U.S. debt ceiling has been suspended many times, usually through legislation, where Congress passes a bill to suspend the application of the debt ceiling. Suspending the debt ceiling means that the government can continue to borrow without being restricted by the set ceiling until the deadline specified in the bill or the debt reaches a new level. The more typical cases are as follows:

2011-2013: In 2011, the United States faced a serious debt ceiling crisis. At that time, Congress and President Obama had intense negotiations on how to raise the debt ceiling, and finally reached an agreement to temporarily raise the debt ceiling and take some budget cuts. In addition, in order to avoid government default, in October 2013, the U.S. Congress passed a bill to suspend the debt ceiling and allow the government to borrow until February 2014. At that time, the U.S. debt level was close to the limit, and suspending the debt ceiling avoided the risk of government default.

2017-2019: In 2017, the U.S. Congress once again passed a bill that suspended the debt ceiling, allowing the government to continue borrowing until March 2019. The bill also included other fiscal matters and was tied to an agreement on the budget and government spending. This suspension allowed the U.S. government to avoid a possible default.

2019-2021: In August 2019, the U.S. Congress passed the Two-Year Budget Agreement, which not only increased the ceiling on government spending, but also suspended the debt ceiling, allowing the government to borrow more money until July 31, 2021. This suspension allows the government to continue borrowing without being constrained by the debt ceiling, thereby ensuring the normal operation of the government and avoiding government shutdowns and debt defaults.

2021: In December 2021, in order to avoid a US government default, Congress passed a temporary debt ceiling adjustment bill, raising the debt ceiling to $28.9 trillion and allowing the government to borrow until 2023. This adjustment was made at the last minute before the expiration in October 2021, avoiding the risk of debt default.

It can be seen that each suspension of the debt ceiling is to deal with certain special events, such as the financial crisis in 2008 and the epidemic in 2021. But why does the re-mention of abolishing the debt ceiling at this time have such an impact? The core lies in the current debt scale of the United States. The ratio of US public debt to GDP has reached a historical high, exceeding 120%. If the debt ceiling is abolished at this time, it means that the United States will not be bound by any fiscal discipline for a long time in the future. The impact on the US dollar credit system is actually unpredictable.

So why does Trump need to do this? The reason is very simple. In order to survive the short-term debt crisis risk, we already know that in Trumps focus of governance, tax cuts and reducing public debt are the two most important goals. However, although the tax cut policy can increase economic vitality, it is bound to cause a reduction in government revenue in the short term. Of course, the resulting fiscal gap may be made up by increasing tariffs, but considering that manufacturing countries can respond by lowering exchange rates, this is why the US dollar index has remained strong recently during the interest rate cut cycle. The core is that countries are preparing for a possible trade war. At the same time, the decline in the earnings of local companies caused by the reduction in fiscal spending has also cast a shadow on the potential for economic growth. Therefore, in order to survive the painful period of implementing this policy, Trump certainly hopes to solve this problem once and for all. Therefore, it is very appropriate to abolish the shackles of the debt ceiling and continue to borrow in the short term to survive the fiscal crisis.

Finally, lets look at why it has an impact on cryptocurrencies. I think the core lies in the blow to the narrative of Bitcoin reserves. We know that in the recent core narrative of cryptocurrencies, the United States solution to the debt crisis by establishing Bitcoin reserves is an important part of it, but if Trump directly abolishes the debt ceiling rule, it is equivalent to indirectly hitting the value of this narrative. In the previous analysis, we have already reduced to the current stage of cryptocurrencies looking for new value support, and it is easy to understand that the profit-taking and risk aversion caused by this is also easy to understand. Therefore, I think that in the next period of time, the priority of observing the Trump teams policies is obviously higher than other factors, and it needs to be continuously paid attention to.