Tokenized real-world assets (RWAs) are digital tokens recorded on a blockchain that represent ownership or legal rights to physical or intangible assets. The scope of tokenization covers a wide range of asset classes, including real estate (residential, commercial properties and real estate investment trusts REITs), commodities (gold, silver, oil and agricultural products), art and collectibles (high-value art, rare stamps and vintage wines), intellectual property (patents, trademarks and copyrights) and financial instruments (bonds, mortgages and insurance policies).

By enabling fractional ownership, tokenization increases the liquidity of assets and democratizes investment opportunities that were once limited to high-net-worth individuals and institutional investors. The blockchain’s immutable ledger ensures transparent ownership records and reduces the risk of fraud; at the same time, tokenized assets traded on decentralized exchanges bring unprecedented market accessibility and efficiency.

According to McKinseys analysis, the total market value of all types of tokenized assets (excluding cryptocurrencies and stablecoins) is expected to reach approximately $2 trillion by 2030, $1 trillion in the pessimistic scenario, and $4 trillion in the optimistic scenario. These estimates do not include stablecoins (including tokenized deposits, wholesale stablecoins, and central bank digital currencies CBDCs) to avoid double counting, as these instruments are often used as cash payment instruments in the settlement of tokenized asset transactions.

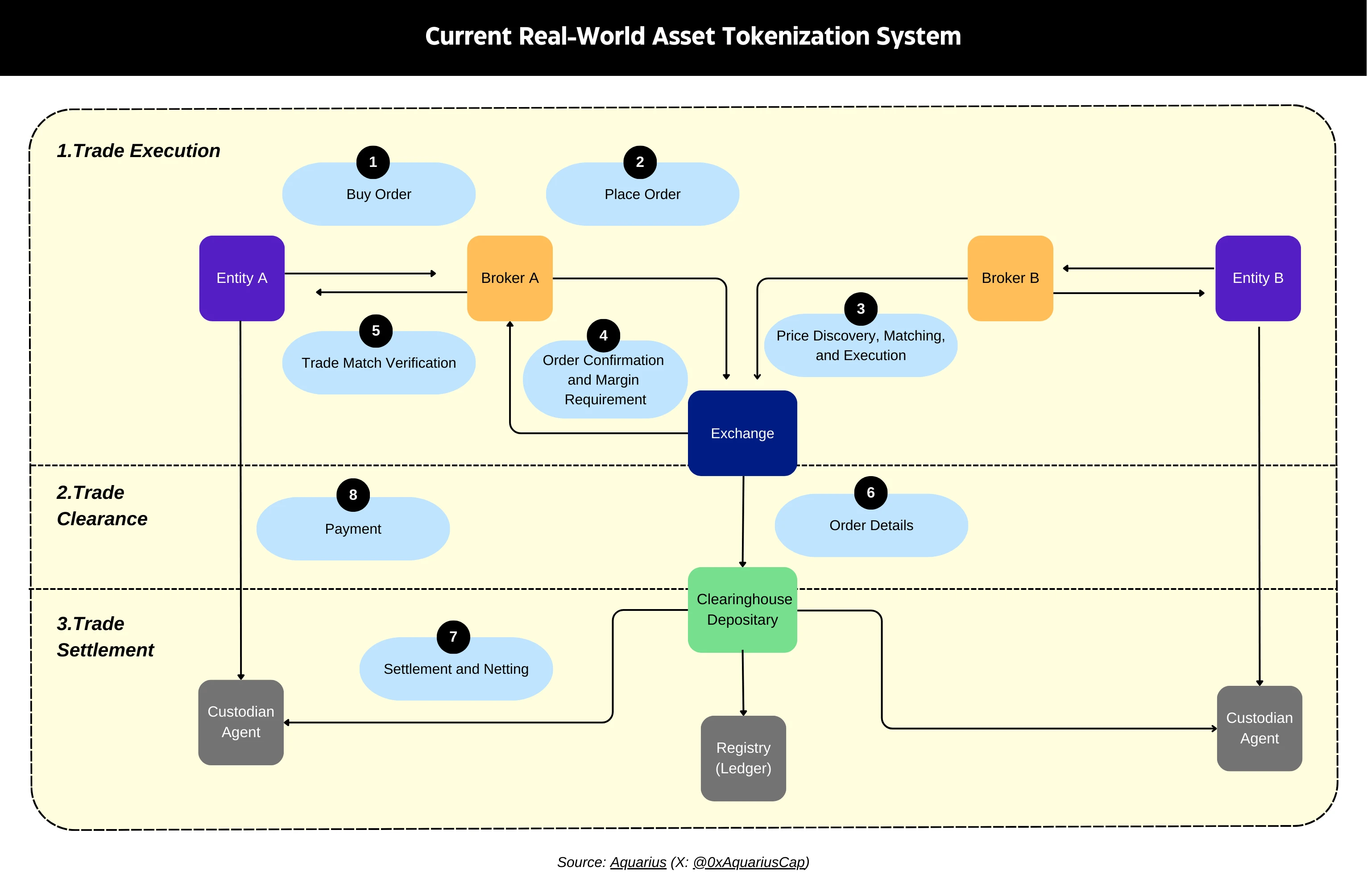

Current system

Tokenization of real-world assets refers to the representation of off-chain asset ownership in the form of digital tokens through blockchain or similar distributed ledgers. This process connects the characteristics, ownership and value of an asset to its digital form. Tokens serve as a digital holding tool that enables its holder to claim ownership of the underlying asset.

Historically, physical holding certificates have been used to prove ownership of assets. While useful, these certificates are vulnerable to theft, loss, forgery, and money laundering. In the 1980s, digital holding instruments began to emerge as a potential solution. However, limited computing power and encryption technology at the time prevented this from happening. Instead, the financial industry turned to centralized electronic registries to record digital assets. While these paperless assets brought certain efficiency gains, their centralized nature required the involvement of multiple intermediaries, which introduced new costs and inefficiencies.

Distributed ledger technology-based systems

The development of distributed ledger technology (DLT) has made it possible to revisit the concept of digitally held securities or tokens.

DLT consists of a series of protocols and frameworks that enable computers to propose and verify transactions in a network while keeping records synchronized. By decentralizing record keeping, this technology shifts responsibility away from a single central authority. Such decentralization reduces administrative burdens and reduces the risk of system failures caused by reliance on central entities, making the system more resilient (see Figure 1).

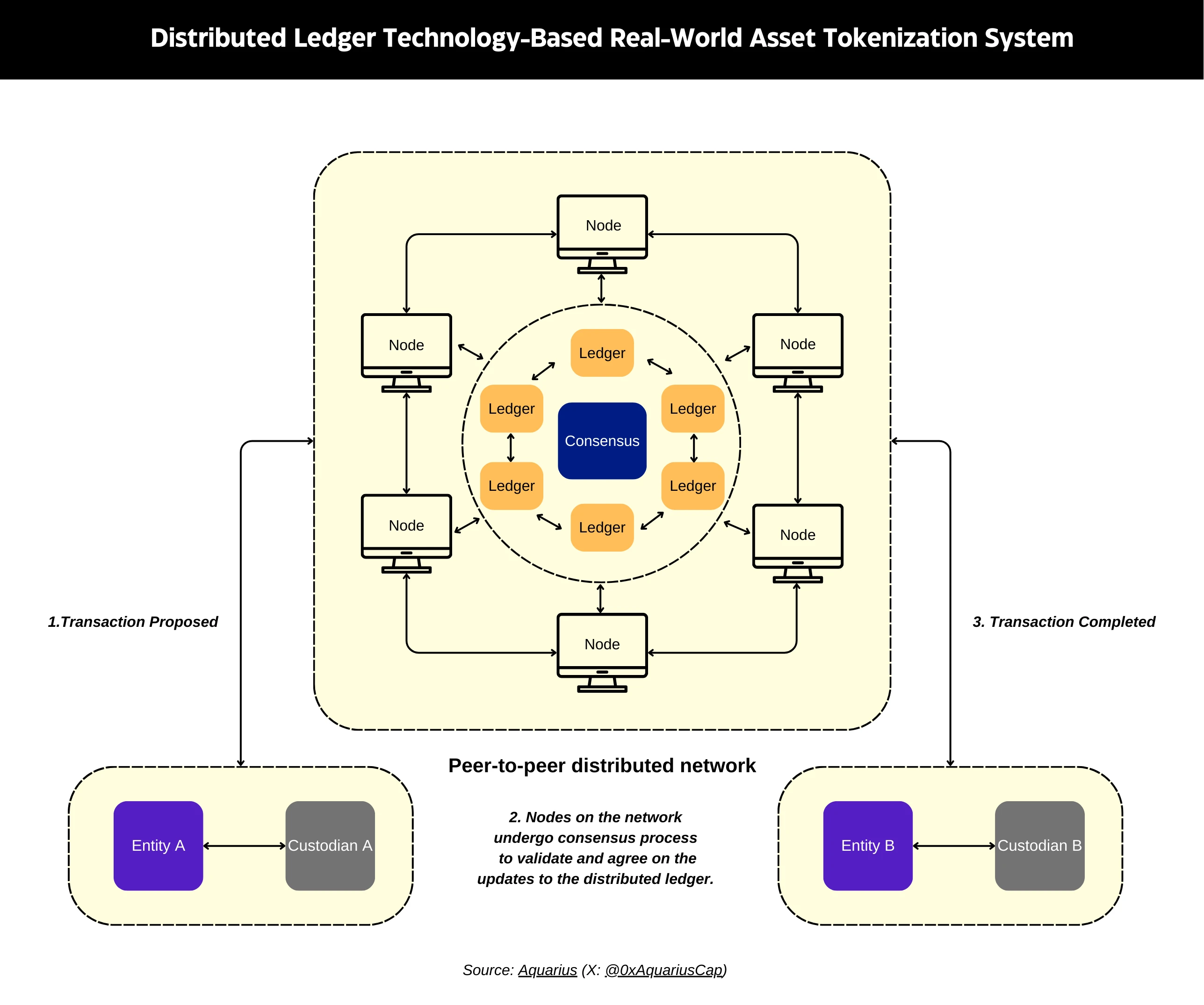

These diagrams compare the transaction flow between traditional systems and DLT-based systems. Figure 1 shows how multiple intermediaries handle trade execution, clearing, and settlement in the current system. Figure 2 shows how a DLT-based system simplifies these processes through a single consensus mechanism.

Decentralized Solutions

Blockchain is a distributed ledger technology that runs on a decentralized network of computers. Tokens can be issued on two types of blockchains: private permissioned chains and public permissionless chains.

Private permissioned chains (such as Ripple) are controlled by a central entity and restrict access to specific users, forming a controlled ecosystem. Public permissionless chains (such as Ethereum) do not require control by a central authority and provide open access to all users. When tokens are issued on public permissionless chains, they can be integrated with decentralized finance (DeFi) protocols (such as decentralized exchanges), thereby increasing their utility and value.

The choice of blockchain—whether a private controlled environment or a public open network—determines the degree of control that a token issuer can maintain. Public permissionless chains give issuers less control than private permissioned chains. The choice of blockchain architecture should align with the issuer’s goals and the intended functionality of the token.

A key advantage of asset tokenization is automation through smart contracts. Smart contracts are programs on the blockchain that execute when two parties meet certain conditions. These contracts automate financial transactions and administrative tasks, reducing the need for manual work and intermediaries. By eliminating counterparty risk, this automation makes operations more efficient and secure, allowing for faster and less expensive transfers.

Tokenization Methods

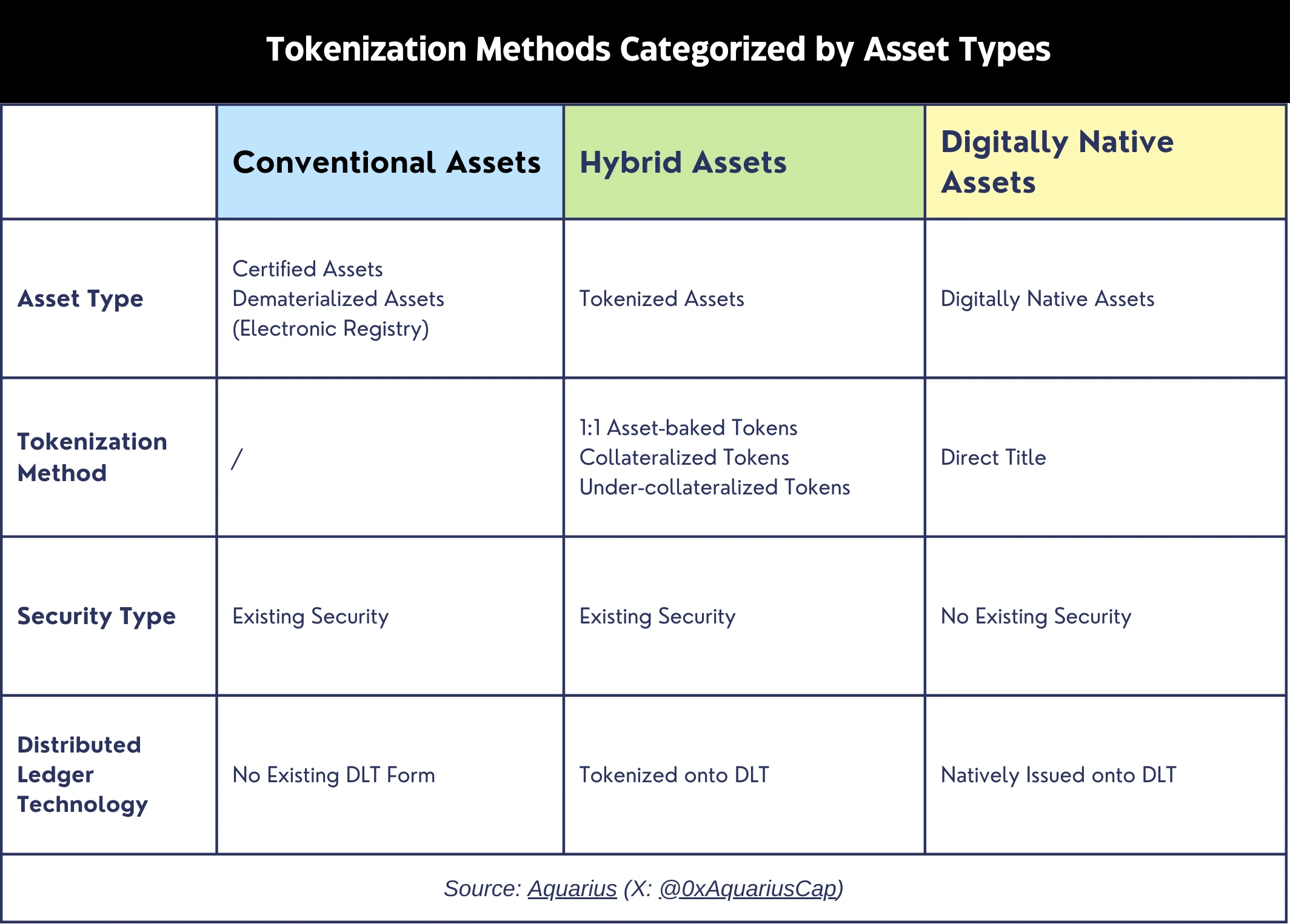

The tokenization of real-world assets has traditionally adopted a simple binary classification: either an asset is tokenized or it is not. However, as we enter the era of digital assets, this overly simplistic perspective is no longer applicable. A more nuanced approach is to analyze assets through two key attributes: their representation and ownership.

The representation includes the economic characteristics of the asset - its function, underlying assets, maturity date and interest rate. In addition, the verification of ownership requires a ledger, which can be off-chain or on-chain. Off-chain assets maintain their rights and representations through physical certificates (such as holding bonds) or paperless forms (such as electronic stock records), which operate under the legal framework. On-chain assets exist in digitally enhanced or digitally native forms and are governed by the blockchain consensus mechanism.

It is important to understand the difference between digitally enhanced assets and digitally native assets. Digitally enhanced (or augmented) assets maintain ownership through an off-chain ledger that serves as their security, while using blockchain tokens as a digital representation. For example, a share of stock ownership may exist on an electronic ledger but be tokenized through a blockchain to enhance its functionality. In contrast, digitally native assets (such as cryptocurrencies) are digital in nature, and their tokens directly represent value and ownership. This means that while the tokens of digitally enhanced assets provide the right to claim ownership from an off-chain ledger, the tokens of digitally native assets directly represent ownership without relying on any off-chain component.

With an understanding of asset types and tokenization, we can further explore the four methods of tokenization. These methods differ in the degree of direct correlation between the token and its underlying asset. Next, we will systematically explore each method, from the most direct token-asset relationship to the least direct relationship.

Direct title : In this approach, the digital token itself acts as the official record of ownership, eliminating the need for a custodian. This approach is only applicable to digitally native assets (see Figure 2). The system uses a single ledger (which may be a distributed ledger) to record token ownership. For example, instead of issuing tokens backed by a share registry, the registry can be tokenized directly, making the token the actual record of ownership. This streamlined approach eliminates the need for a custodian or duplicate registries. While this approach can use a distributed ledger, the registry itself does not necessarily need to be distributed. However, the current legal framework for most asset classes for this tokenization approach remains limited and the regulatory structure is immature.

1:1 asset-backed tokens : In this approach, the custodian holds the asset and issues a token that represents a direct interest in that underlying asset. Each token can be redeemed for the actual asset or its cash equivalent. For example, a financial institution could issue a bond token based on bonds held in a trust account, or a commercial bank could issue a stablecoin token that is backed one-to-one by commercial bank currency in a dedicated account.

Collateralized tokens : This approach involves issuing asset tokens collateralized by an asset other than the asset or underlying interest that is intended to represent them. Typically, tokens are overcollateralized to account for fluctuations in the value of the collateralized asset relative to the value of the underlying asset of the token. For example, the stablecoin Tether is backed not only by cash but also by a range of other assets such as fixed income securities. Similarly, it is possible to create a government bond token backed by commercial bank bonds, or a stock token backed by an overcollateralized portfolio of underlying stocks.

Under-collateralized tokens : Tokens issued in this approach are designed to track the value of an asset but are not fully collateralized. Similar to fractional reserve banking, maintaining the value of the token requires active management of the fractional reserve portfolio and open market operations. This is a riskier form of asset tokenization and has a history of failures. For example, the collapsed Terra/Luna stablecoins were not backed by independent assets and relied on algorithmic stabilization through a supply control algorithm. Other less risky partially collateralized tokens have also been issued.

Why Tokenization?

The tokenization of real-world assets primarily achieves efficiency gains through distributed ledger technology (DLT). The technology enhances transparency, automates processes, reduces operational costs, and eliminates intermediaries and counterparty risks. These benefits enable faster settlement and cost savings through a streamlined and flexible market infrastructure compared to the traditional financial system.

Atomic settlement : The combination of distributed ledger technology and tokenized assets has introduced the concept of atomic settlement. Currently, settlement is mainly carried out through central counterparties, and the commonly used securities settlement method is rolling cycles. In this method, although the transaction is executed on a specific day, the actual settlement (the transfer of ownership according to the predetermined agreement) is usually completed with a delay of one to three days. This involves two stages or transfers: the delivery stage, which transfers the ownership of the securities from the seller to the buyer; and the payment stage, which transfers the cash from the buyer to the seller. Atomic settlement is achieved through smart contracts, whose programmable code executes both stages of the transaction at the same time, or not at all if the predetermined conditions are not met. This method eliminates counterparty risk and significantly improves the speed and efficiency of transactions. In addition, the settlement of transactions through smart contracts also eliminates the need for margin, because there is no risk of delivery failure and subsequent transaction reconciliation. This further releases funds tied up by margin, thereby indirectly improving the liquidity of financial markets.

Increased liquidity : Tokenization significantly enhances the transferability of assets, making previously non-tradable assets tradable. For example, traditional real estate transactions face significant barriers — high transaction costs, complex legal processes, and inherent illiquidity. These barriers, combined with the unique attributes of each property (e.g., location, condition, legal status), make it impractical to trade individual properties on public exchanges like stocks or bonds. Tokenization addresses these challenges through smart contracts, which optimize the transaction process by eliminating intermediaries, simplifying ownership transfers, and automating compliance checks, thereby significantly reducing transaction costs. The same benefits apply to other traditionally illiquid assets such as art, collectibles, infrastructure projects, and private equity shares. In addition, tokenization enables new distributed markets through automated market makers (AMMs). These systems automatically match buyers and sellers through pools of assets managed by smart contracts, providing continuous liquidity. Unlike the fixed trading hours of traditional markets, these blockchain-based systems operate 24/7. Greater accessibility is further enhanced by fractional ownership, lower investment barriers, and simplified trading processes.

Reduction in intermediation : Decentralized data structures enable smart contracts integrated on blockchains to replace traditional intermediaries to verify data. Smart contracts can also replace central securities depositories (CSDs) and automate processes such as asset ownership transfers, dividend payments, and interest distributions.

Enabling automation : One of the main advantages of asset tokenization is automation through smart contracts. Smart contracts are programming codes deployed on the blockchain that automatically execute when predetermined conditions are met. Smart contracts have the ability to simplify many manual tasks, especially in industries such as insurance. For example, they can automate policy issuance and claim payments. If a flight is delayed or cancelled, a smart contract can automatically trigger a travel insurance payout without the need for manual processing. The effectiveness of such automation depends heavily on the integration and real-time monitoring of relevant data. Third-party services called “oracles” provide external data to smart contracts, acting as a bridge between the blockchain and the outside world, as smart contracts cannot directly access external data. Automation is most feasible in asset classes where data is quantifiable, standardized, and reliably accessible through oracles. Stocks, bonds, and derivatives are the best examples, as their market data is easily accessible and can be easily integrated into smart contracts. However, automation is more challenging in industries where data is subjective or difficult to quantify. For example, real estate involves complex transactions that require manual verification of legal documents, subjective property valuations, and compliance with diverse regulatory frameworks—making it more difficult to fully automate through smart contracts.

Facilitating Compliance : Compliance is a key aspect of tokenized assets. As regulatory frameworks such as know-your-customer (KYC), anti-money laundering (AML), and counter-terrorist financing evolve, a safer environment for digital finance and transactions is created. The underlying technology of tokenized assets makes compliance with these requirements more efficient and uniform by standardizing and automating processes. KYC and AML regulations can be encoded directly into the blockchain or into individual asset transfer rules, allowing for more efficient interactions. For example, when a customer establishes a relationship with a new financial institution, their identity information can be automatically transferred with their consent. Research on the impact of tokenization on banking infrastructure has shown positive results. By analyzing more than 50 operational cost indicators, the study showed that improved audit capabilities and transaction transparency can reduce the total cost of compliance by 30% to 50%.

Automated Market Makers (AMMs) : Smart contracts are revolutionizing traditional market making through automated market makers (AMMs). While traditional market makers provide liquidity by acting as buyers and sellers of securities, AMMs take a different approach. They use smart contracts to automatically match buyers and sellers through pools of assets provided by liquidity providers. These smart contracts embedded in the blockchain algorithmically determine asset prices and manage asset pools. The automated nature of AMMs significantly reduces costs and improves performance. Studies have shown that AMMs have significantly lower transaction costs compared to traditional systems, especially in assets with high trading volume and low to medium volatility.

Risks and costs of RWA tokenization

Despite the many advantages that tokenized assets bring, their adoption still faces significant challenges. The main risks come from underlying technology and regulatory considerations. Technical concerns include network security vulnerabilities, system scalability limitations, settlement processes, network stability, and efficiency issues. On the regulatory side, key issues involve anti-money laundering compliance, governance frameworks, identity verification, and data protection and privacy. Researchers suggest that solving digital asset regulatory issues should not be limited to incorporating new technologies into existing frameworks. Instead, we should explore how blockchain technology and smart contracts can be used to enhance regulatory compliance.

In addition to technical and regulatory challenges, investor behavior and market dynamics present additional complexities. Achieving widespread adoption will require significant education and awareness efforts. Market risks include the potential for overvaluation of assets through speculative trading and increased price volatility due to the digital nature of these assets. In addition, the high energy consumption of blockchain consensus mechanisms raises environmental concerns. These multifaceted challenges must be addressed to fully realize the benefits of tokenization in the financial sector.

The transition to a tokenized financial system involves significant costs. The most significant expenses come from the infrastructure changes required to support blockchain and tokenization technologies. Organizations need to invest in secure, scalable blockchain platforms, acquire specialized software for managing tokenized assets, and train employees to adapt to these new systems. Integration costs are also not negligible - these new systems need to be connected to existing financial infrastructure while maintaining security and operational integrity. Educational activities to increase understanding and overcome skepticism also constitute significant direct and opportunity costs for governments. Finally, the high electricity consumption of blockchain consensus mechanisms poses both financial and environmental challenges.

Disclaimer

This article is for general information purposes only and does not constitute investment advice, a recommendation or a solicitation to buy or sell any security. This article should not be relied upon in making any investment decision and should not be relied upon for accounting, legal, tax or investment advice. You are advised to consult your own advisors regarding any legal, business, tax or other relevant matters relating to any investment decision. Certain information contained in this article may have been obtained from third-party sources, including portfolio companies of funds managed by Aquarius. The opinions expressed in this article are those of the author alone and do not necessarily reflect the views of Aquarius or its affiliates. These opinions are subject to change without notice and may not be updated.