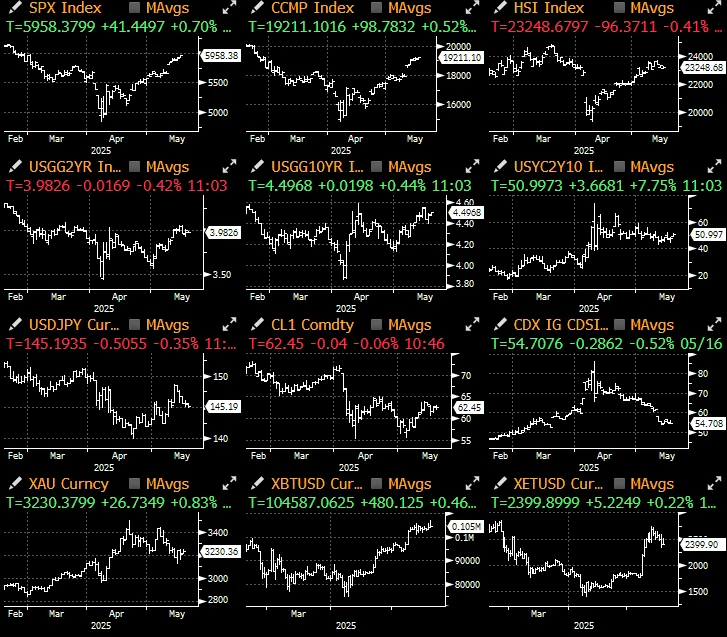

Source: IgniteRatings, X

Moodys downgraded the U.S. governments long-term issuer and senior unsecured debt ratings to Aa 1 from Aaa and changed the outlook to stable from negative.

The one-level downgrade reflects that over the past decade, the proportion of U.S. government debt and interest payments has continued to rise, far higher than other sovereign countries with the same rating.

---Moodys, May 16, 2025

Moodys downgraded the US long-term credit rating, which means that the US sovereign debt has been removed from the AAA ranks by all major rating agencies. This news was released a few hours after the US stock market closed last Friday, and it is said that it also prompted the US House of Representatives Budget Committee to quickly advance the One, Big, Beautiful Bill on Sunday night in an attempt to minimize the potential market impact.

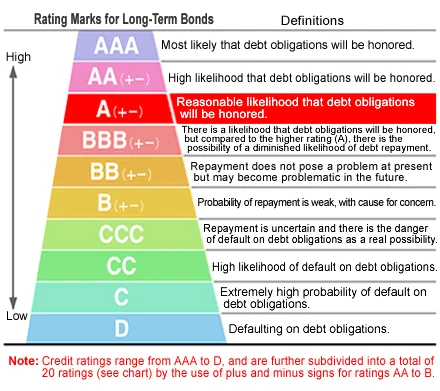

Putting aside the political wrangling and budget bill drama, do credit ratings still matter? Some readers may remember that Silicon Valley Bank (SVB) still held an A credit rating before its collapse, and more experienced readers may not have forgotten the ridiculously high ratings obtained by CDOs, CMOs, subprime mortgages and Chinese real estate bonds.

Regarding this topic, we have organized the relevant key points in the form of FAQ below:

When has the United States ever been downgraded in the past?

July 2011: SP

August 2023: Fitch

Will there be an immediate technical impact?

For institutions that are restricted by ratings and cannot hold non-AAA bonds

Because of the size and non-fungibility of U.S. Treasuries as an asset class, these institutions typically adjust their internal rules (and have done so in the past).

Impact on Centralized Clearing

DTCC and CME treat Treasury bonds as collateral by setting a haircut based on duration and bond type, with less reliance on ratings.

Impact on Money Market Funds

Short-duration allocations weaken the impact of credit ratings. In fact, even after the past downgrades and debt limit disputes, the demand for Treasury bonds has hardly fluctuated.

The long-term reserve asset status of US Treasuries

In fact, President Trump’s tariff policy and global trade restructuring have had a more profound impact on global demand for U.S. debt than any rating agency.

How has the market reacted in the past?

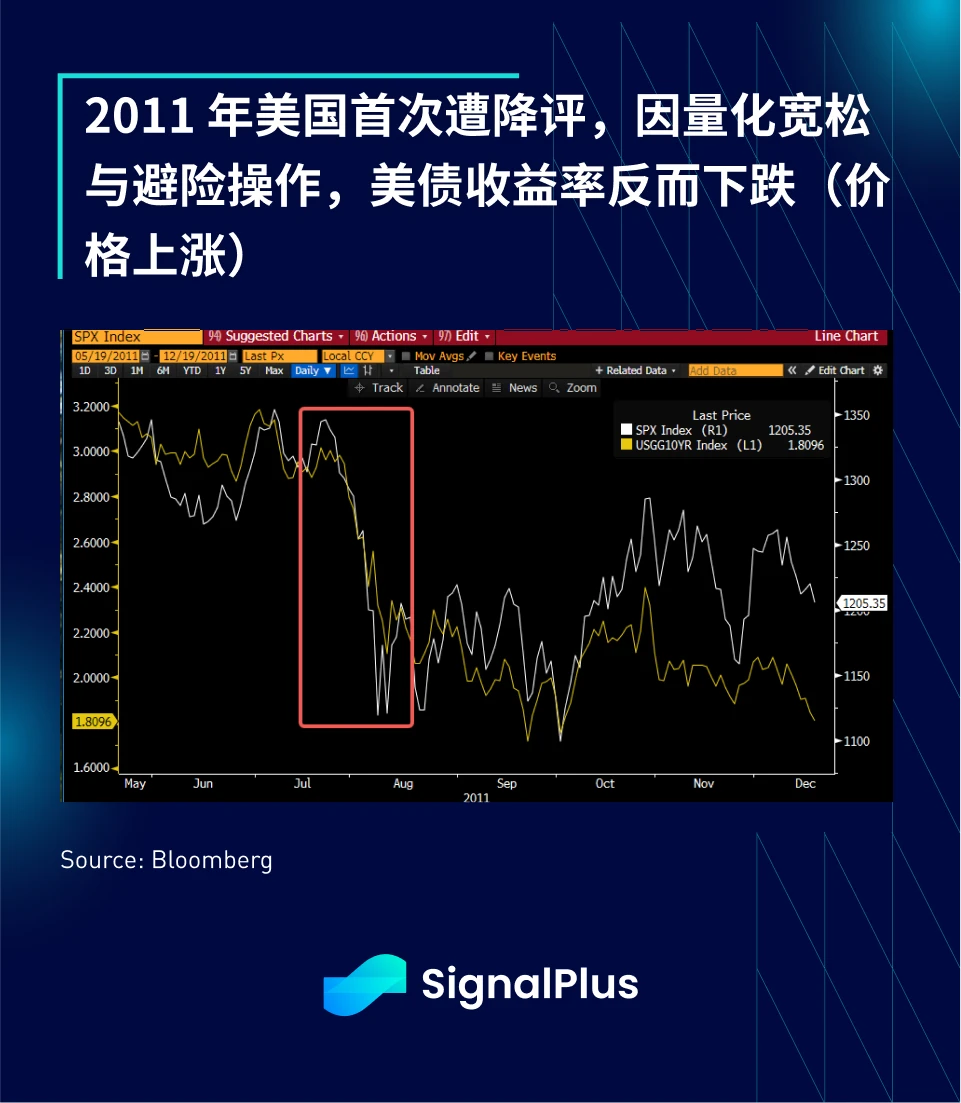

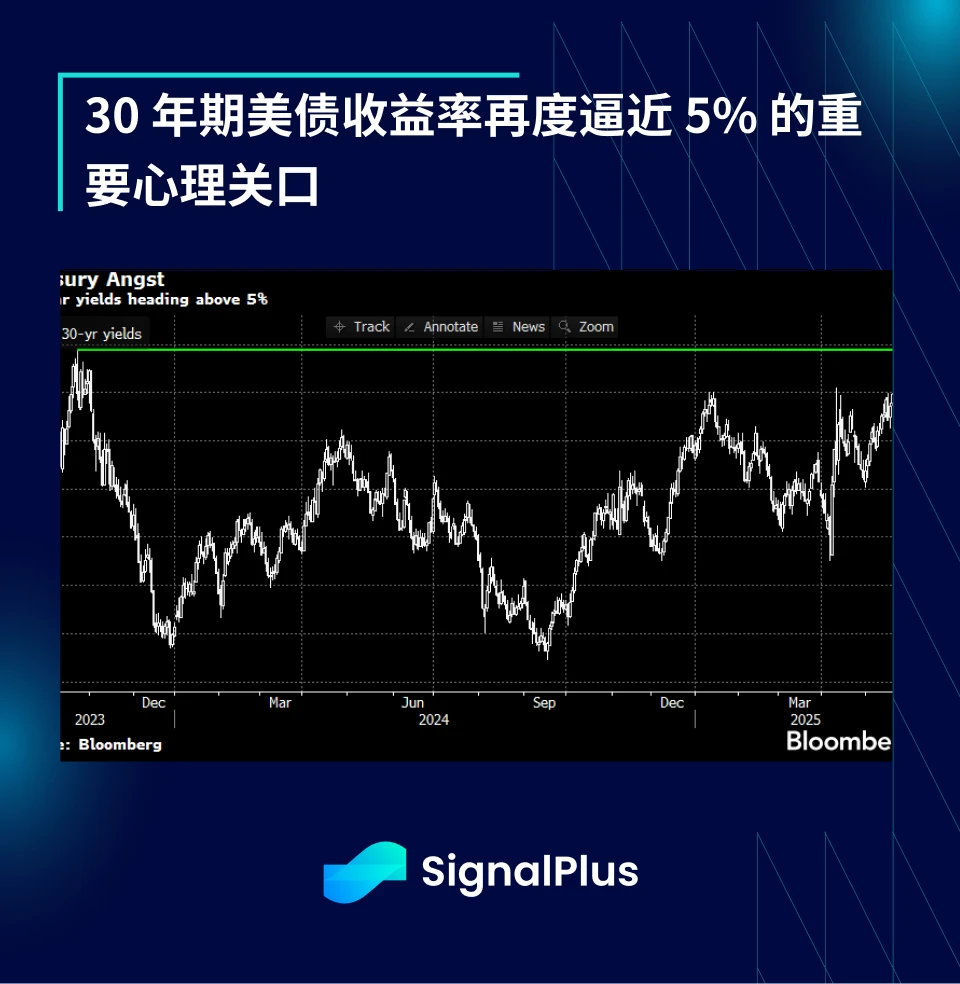

When the ratings were downgraded in 2011, the market was quite shocked because it was the first downgrade and it was during the first generation of the debt ceiling crisis.

Stocks fell about 20% in July-August, but the 10-year Treasury yield actually fell 120 basis points (i.e. price increase) after the downgrade due to safe-haven hedging and the quantitative easing policy that was ongoing at the time.

In 2023, the downgrade occurred in August, just after the debt ceiling crisis in early summer. At the same time, the US Treasury was recovering market liquidity by rebuilding the Treasury General Account and issuing a large amount of US Treasury bonds. At that time, the SPX index fell by about 10%, and the US Treasury yield continued its upward trend for the year by about 50 basis points. Although this credit rating downgrade may have accelerated the relative trend of the market, overall, it did not bring about a fundamental change to the market structure.

Will this downgrade affect fiscal decisions?

The House Budget Committee did advance its budget bill late Sunday, showing some interest in mitigating potential market shocks.

Will it cut dollar spending and control the deficit? While the downgrade may give more weight to the voices of fiscal hawks, it is unlikely to change the long-term trend of out-of-control spending and concerns about the unsustainable supply of U.S. debt.

This would increase uncertainty about the timing/whether the bill’s final passage would be delayed and could undermine the potential positive effects of the tax cuts due to adverse budgetary implications.

What is the possible market reaction this time?

As for stocks, given past experience and the rapid rise in the market in recent weeks in the absence of broad leadership, the short-term reaction of the stock market is likely to be a knee-jerk decline.

The trend of the bond market is difficult to predict. It depends on factors such as the extent of the decline in stock market risk appetite, the game between fiscal hawks and Trump, whether the Senate can successfully pass the budget before the debt limit expires, and whether this incident will affect Trumps 90-day tariff truce agreement.

Overall, U.S. stocks, U.S. bonds and the U.S. dollar may face negative risks.

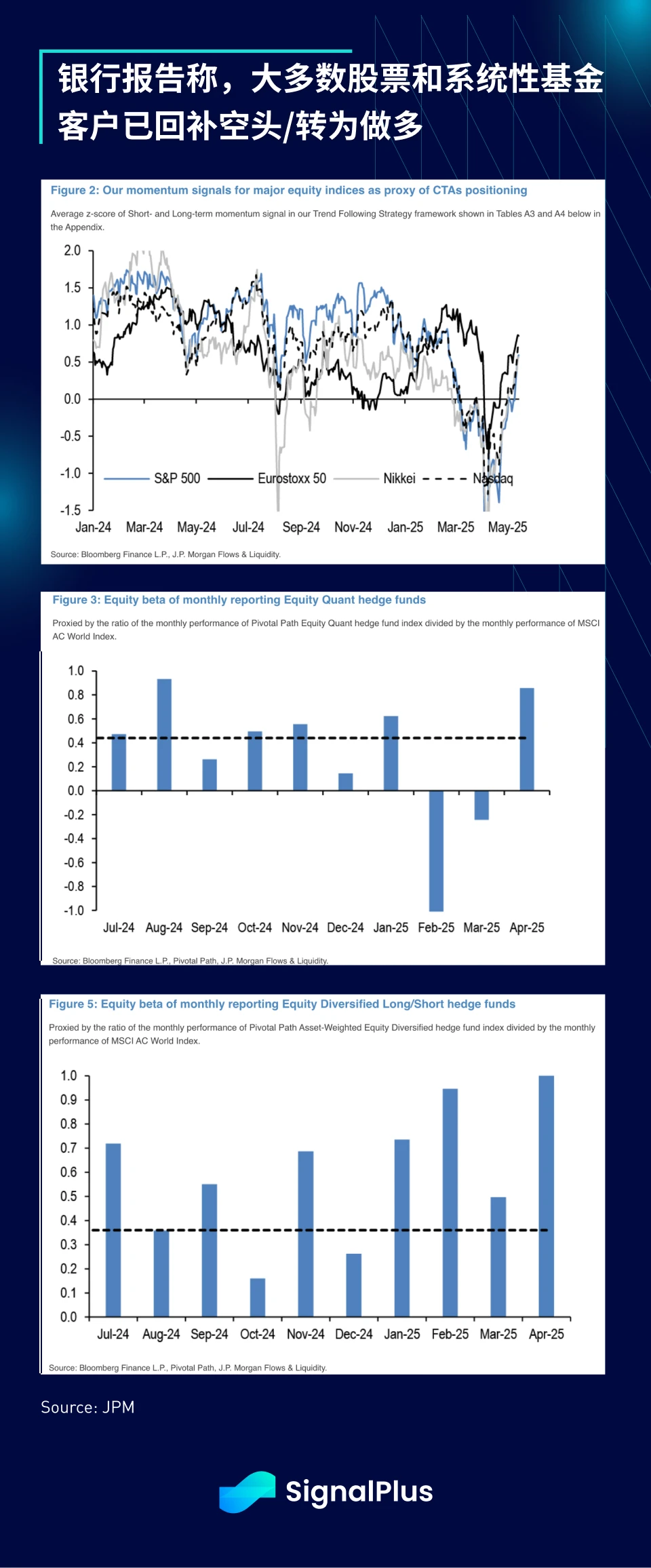

What is the current position of the macro market?

Macro funds, systematic funds and quantitative funds have mostly covered their short/reduce their positions, and have even turned to long positions.

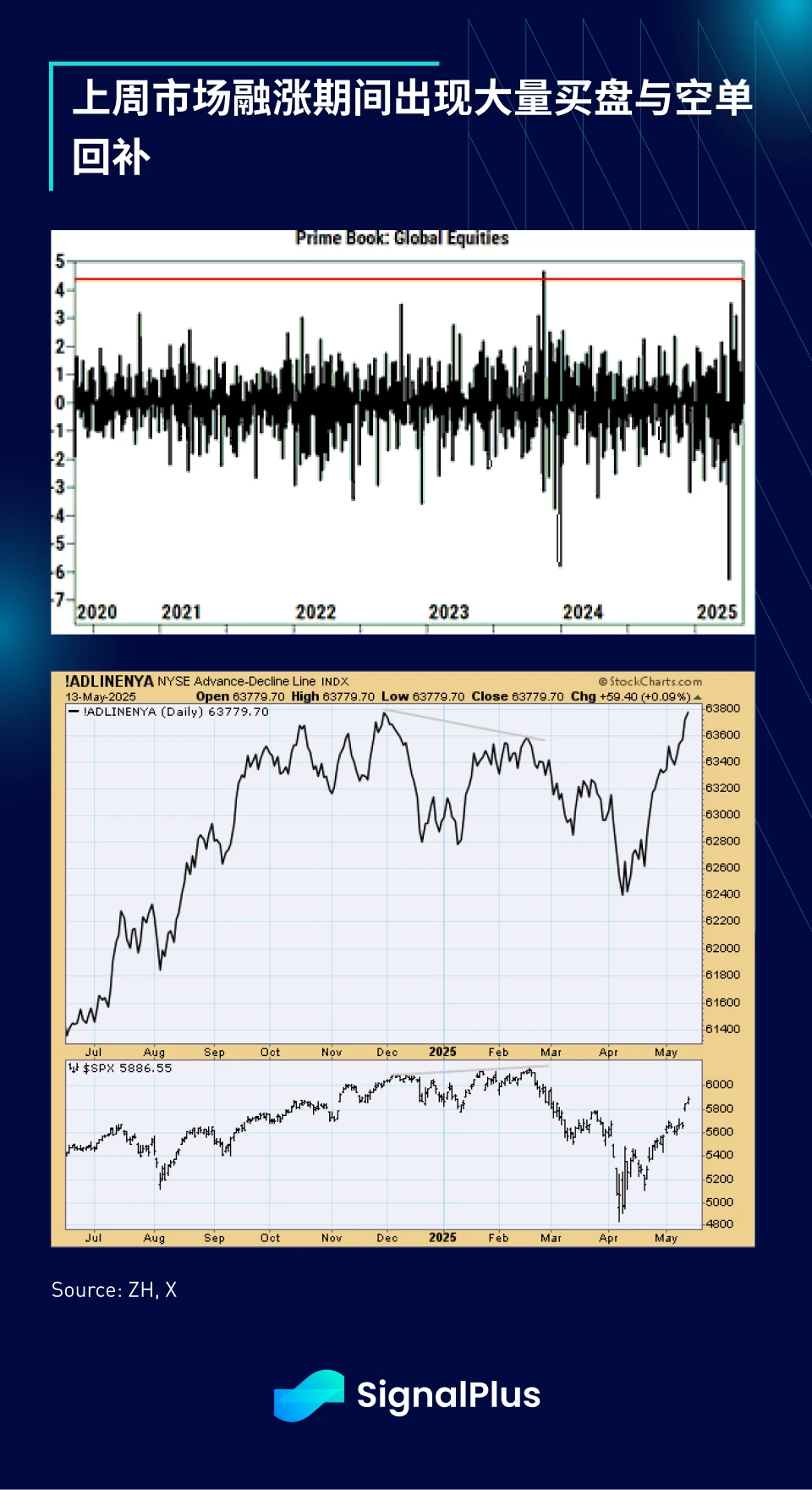

Last week, the market saw a small melt-up as traders rushed to cover their short positions, and the NYSEs Advance-Decline Line indicator hit a recent high.

How did economic data perform last week?

Pretty bad for the bond market.

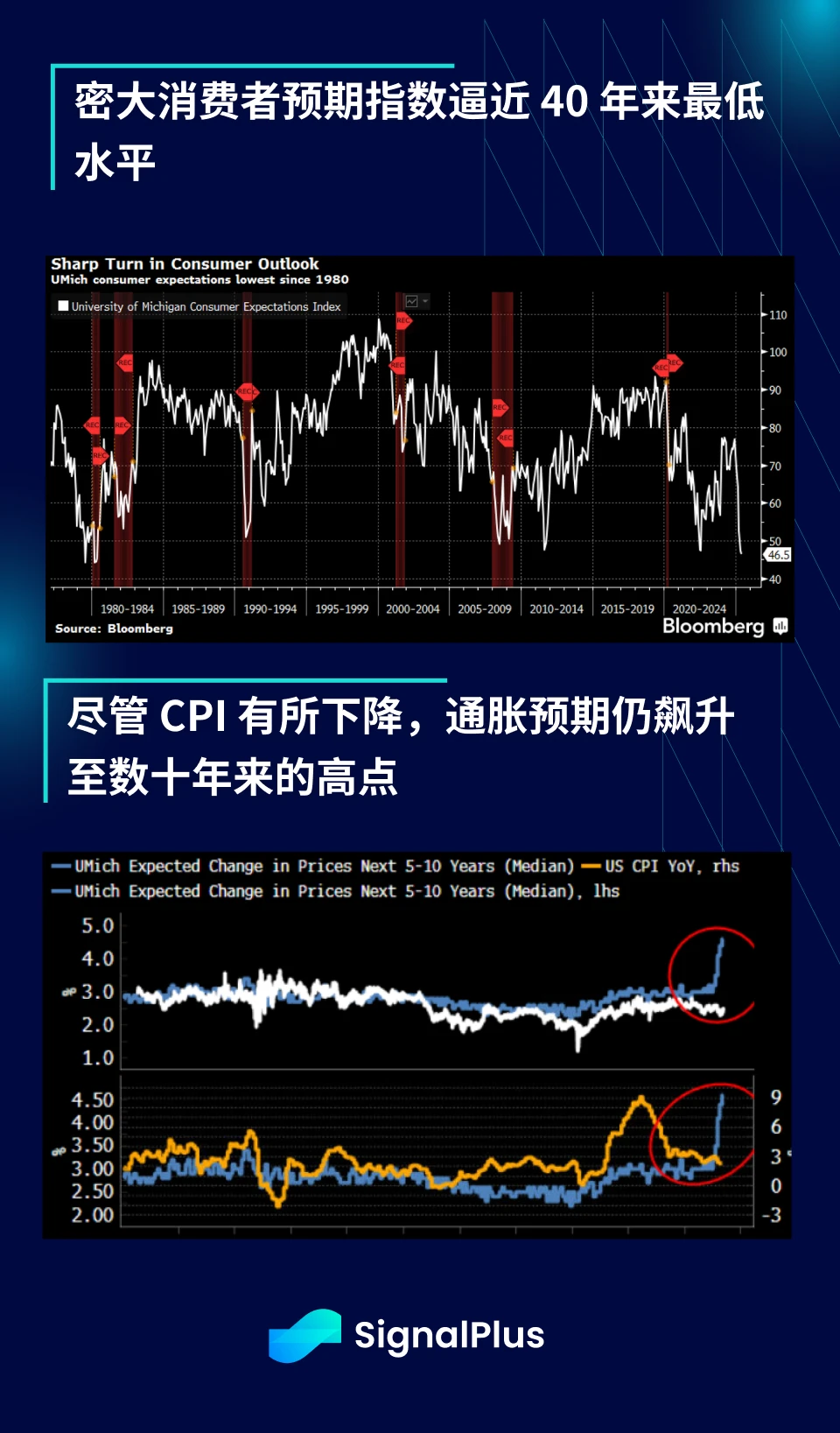

Despite the recent easing of tariff policies, the University of Michigans consumer expectations index still fell sharply.

The overall index fell to its lowest point since June 2022 and is almost approaching its lowest level since the 1980s.

Long-term inflation expectations rose to their highest level since 1991 (4.6%).

One-year inflation expectations are as high as 7.3%, the highest level since 1981.

Should the market worry about foreign selling?

Let’s take a look back at what has happened over the past few months.

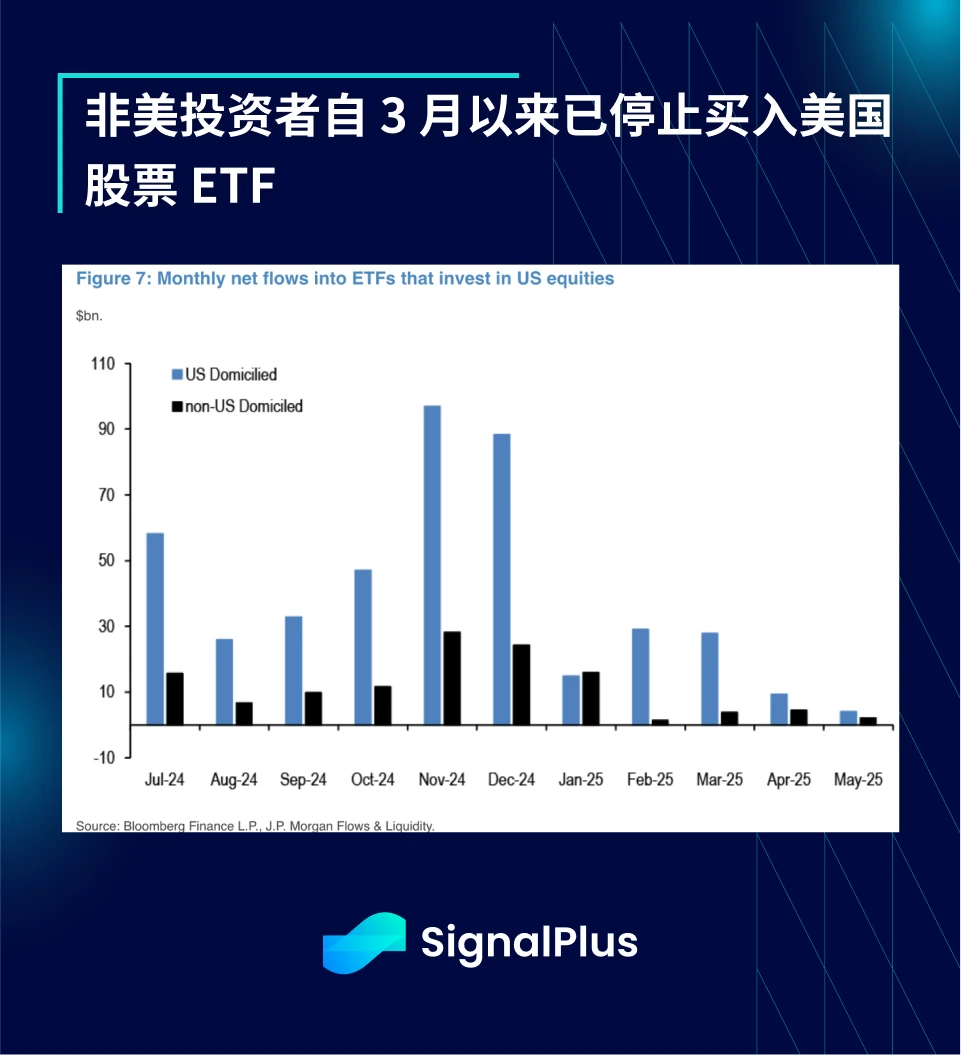

Non-U.S. investors have stopped adding to U.S. stock funds since March and have become net sellers of bond funds, a trend that may continue in the short term.

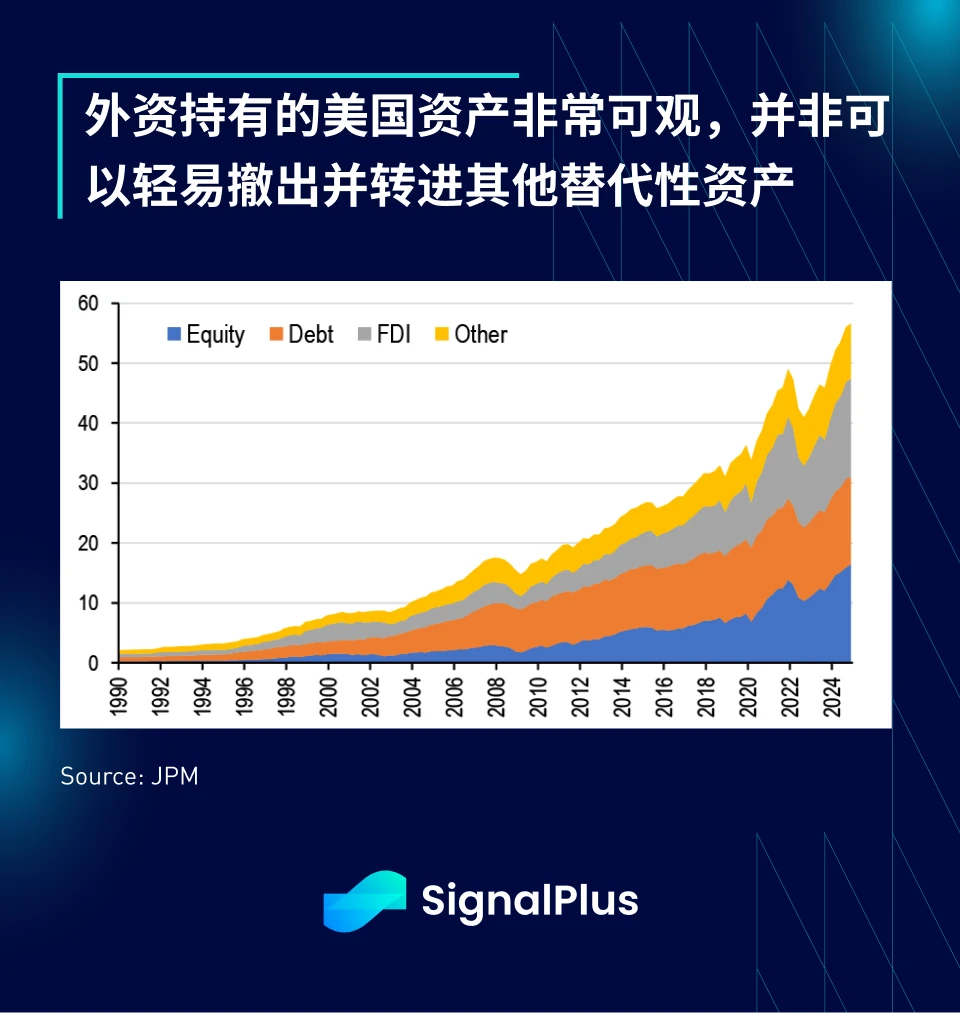

But in terms of actual impact, bank data shows that the total amount of US dollar assets held by foreign investors in 2024 is about 57 trillion US dollars, which has increased significantly compared with 2.2 trillion US dollars in 1990. Among them, about 17 trillion are stock assets and 15 trillion are bonds.

In other words, foreign investors hold approximately 20% of the total supply of U.S. stocks and 30% of the total supply of U.S. bonds.

This is not a small amount and cannot be sold off or reduced in large quantities at will without affecting the entire capital market structure.

Furthermore, assets are dispersed among different foreign holders, and any rash action by any party will involve the game reactions of other participants.

As far as the stock market is concerned, the key is still the earnings performance of companies, and so far it has been good. According to JPM data, the overall earnings of the SPX index exceeded expectations by about 8% in the first quarter. 70% of companies have released financial reports, of which 54% of companies have better-than-expected revenues, 70% of companies have exceeded earnings expectations, and Mag-7s EPS growth is as high as 28%, far ahead of the index.

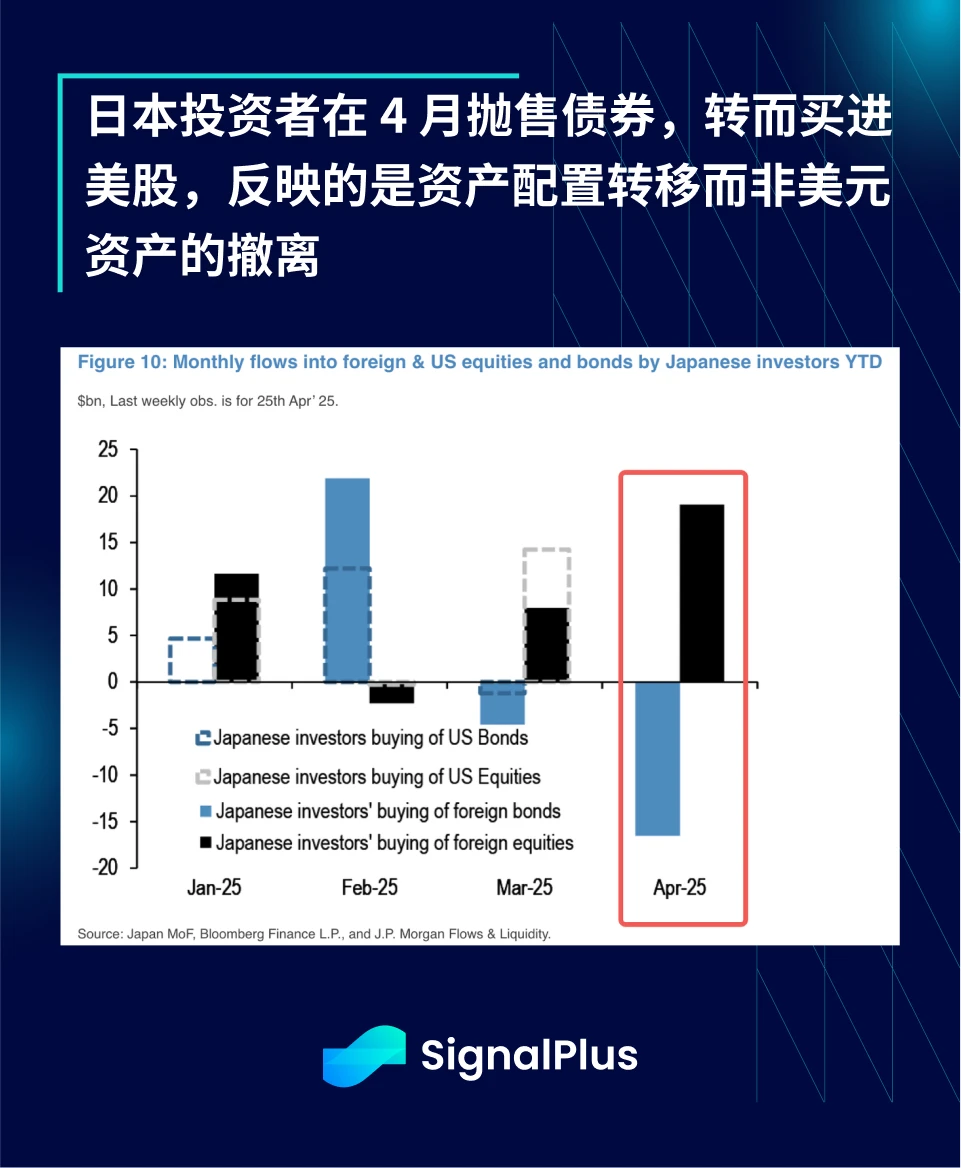

In terms of holding structure (not including vague offshore structures such as Cayman), the United Kingdom, Canada and Japan are currently the worlds top three holders of U.S. assets, and they are also close allies of the United States. China ranks only fourth, accounting for about 4%, which is significantly lower than the 8-9% of the previous group.

Based on the trends over the past month, Japanese investors have indeed reduced their holdings of U.S. Treasuries, but at the same time have significantly increased their holdings of U.S. stocks, so this is more like an asset allocation adjustment rather than a true de-dollarization.

In short, a large-scale capital outflow or de-dollarization should be unlikely in the short term.

How are cryptocurrencies performing?

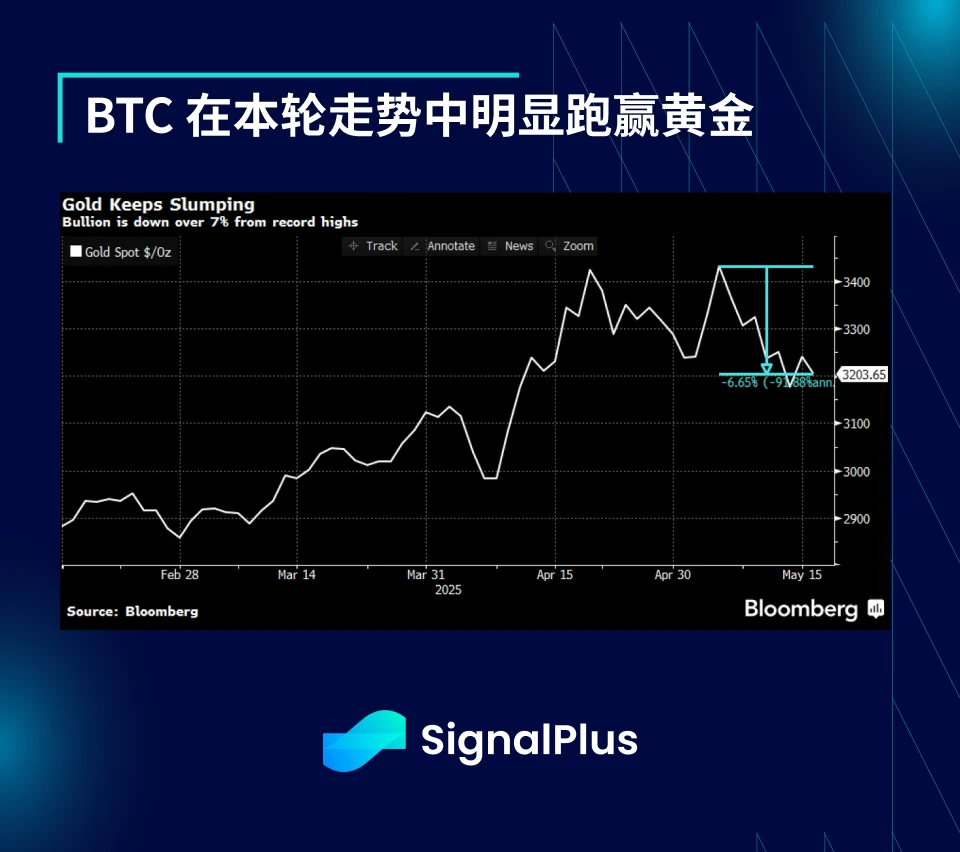

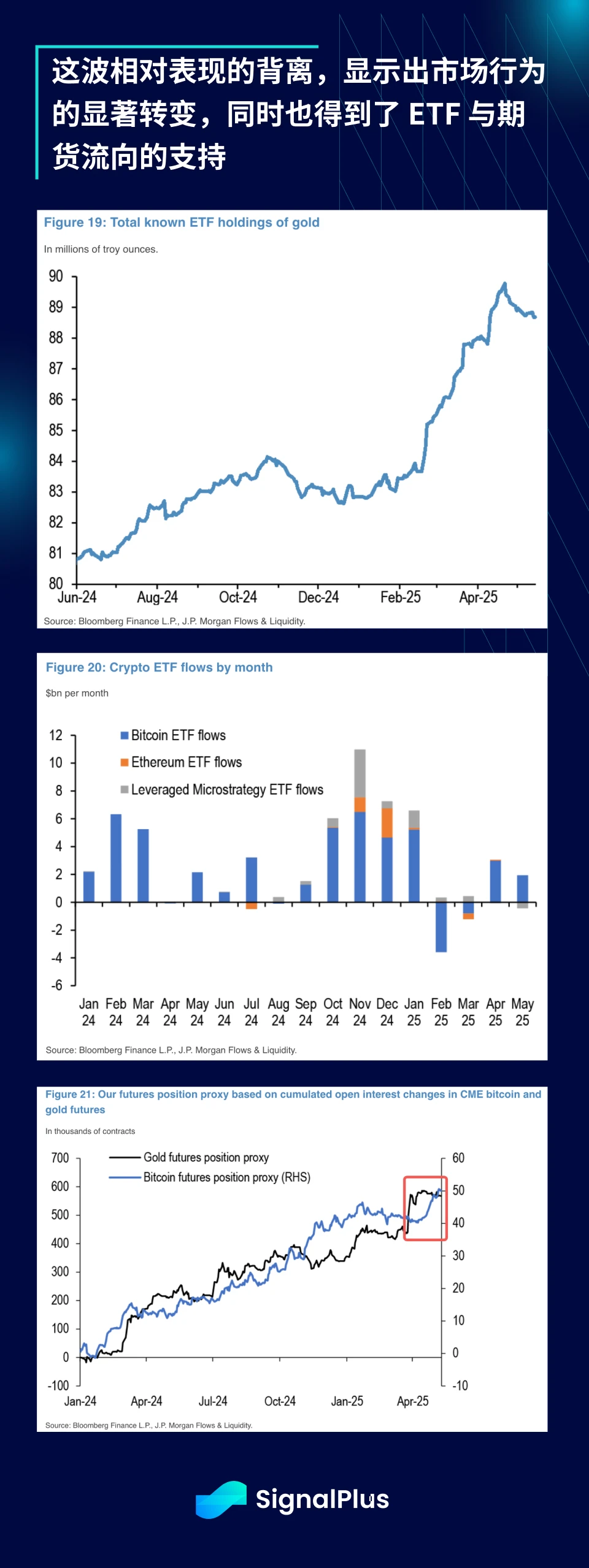

Interestingly, while gold prices are down about 7% from their highs, cryptocurrency prices have remained stable throughout the move.

Unlike the trend of gold prices and BTC rising synchronously in previous months, BTC has continued to rise recently despite the weakening gold prices, which is also reflected in the ETF fund flows.

Gold ETFs saw outflows, while BTC ETF flows rose slightly, and CMEs gold and BTC futures positions also showed a similar situation.

Overall, as the macro market stabilizes, the dollar depreciation trade is reflected in most asset classes. We expect the correlation breaks and relative value opportunities between such micro assets to continue to appear until the next round of major geopolitical developments actually take place.

I wish you all a smooth transaction!

You can use the SignalPlus trading vane function for free at t.signalplus.com/news , which integrates market information through AI and makes market sentiment clear at a glance. If you want to receive our updates in real time, please follow our Twitter account @SignalPlusCN, or join our WeChat group (add the assistant WeChat, please delete the space between English and numbers: SignalPlus 123), Telegram group and Discord community to communicate and interact with more friends.

SignalPlus Official Website: https://www.signalplus.com