Original author: Ryan, Tiger Research

This report, written by Tiger Research , analyzes how South Korea’s June 3 presidential election will trigger four major changes in the global cryptocurrency market.

Summary of key points

South Korea as a core Web3 hub: With $5.4 billion in daily trading volume and 9.7 million active users, South Korea is the world’s third-largest cryptocurrency market after the United States and China. It is a key benchmark for global projects to expand into Asia.

Accelerated taxation could lead to a drop in trading volumes: Although the implementation of cryptocurrency taxes is currently postponed to 2027, the new government is likely to push it forward. Drawing on international precedents, trading volumes could drop by more than 20%.

ETF approval is likely, other reforms may face delays: All major candidates support the introduction of a Bitcoin spot ETF, increasing the likelihood of its early approval. In contrast, regulatory reforms around the Korean won stablecoin and the “one exchange, one bank” policy are expected to be longer-term agenda items.

1. Is South Koreas June presidential election just about the local area?

South Korea is set to hold its presidential election on June 3. While this may seem like a local political event, its impact transcends borders due to the country’s influence on the global cryptocurrency market.

Source: Tiger Research

South Korea is widely considered the third most important market for global Web3 projects after the United States and China. This position is not just the result of a marketing strategy. According to the Financial Services Commissions 2024 report, South Koreas daily cryptocurrency trading volume reached 7.3 trillion won, with more than 20 million registered accounts and 9.7 million active users.

This position is further reinforced by investor behavior. South Korean users have consistently shown strong interest in altcoins other than Bitcoin and Ethereum. On-chain activity is also high, making South Korea a valuable indicator of new projects’ acceptance in the global market.

For many global projects, establishing a presence in South Korea has become a strategic entry point into the wider Asian market. This gives the upcoming elections special weight, as key campaign issues now include cryptocurrency taxation, regulation of Korean won stablecoins, and approval of cryptocurrency ETFs.

These developments are not limited to domestic stakeholders. Global investors and project operators must also pay attention to the election results. Both tightening and loosening of regulation are possible, and projects with large Korean user bases may be particularly sensitive to the policy direction set by the next government.

2. What changes will occur after the South Korean presidential election?

Source: Tiger Research

2.1. The end of the cryptocurrency tax deferral policy

Under the Financial Services Commission’s roadmap for corporate participation in the crypto-asset market, corporate entities are being gradually granted access to the cryptocurrency market. This gradual opening up of the market inevitably requires a corresponding overhaul of the tax framework.

Currently, South Korea’s virtual asset taxation has been postponed until 2027. The original plan was to impose a 20% tax on annual earnings exceeding approximately $1,850 from January 2025. However, the implementation was delayed by two years.

A growing point of contention is that both individuals and companies benefit from tax deferrals despite currently generating income from cryptocurrency trading. According to the Financial Services Commission’s roadmap, listed companies and registered professional investment firms will be allowed to invest in virtual assets through corporate accounts starting in the second half of 2025.

Given this shift, it is unlikely that the deferrals for individuals and companies will be extended again. The government may seek legislative amendments to repeal the current deferrals and bring forward the tax.

Political positions of the parties have always been divided on the issue of tax deferral. The Democratic Party initially advocated raising the tax exemption threshold rather than deferring taxation, although it ultimately supported the deferral policy. Depending on the election results, the policy may shift to raising the deduction limit rather than maintaining the deferral policy.

If the tax is implemented, domestic exchanges are likely to see a significant drop in trading volumes - in line with international precedent. In 2022, India imposed a 30% tax on cryptocurrency gains and introduced a 1% withholding tax on all transactions. This led to a 10% to 70% drop in trading volumes on major platforms such as WazirX and CoinDCX. Similarly, Indonesia saw a year-on-year drop in trading volumes of around 60% after the introduction of a high tax in 2023.

While South Korea’s proposed tax rate is less aggressive, these examples suggest that trading volumes on local exchanges could fall by more than 20%, with funds likely to shift to offshore platforms.

2.2. Introduction of Cryptocurrency ETFs

Source: Tiger Research

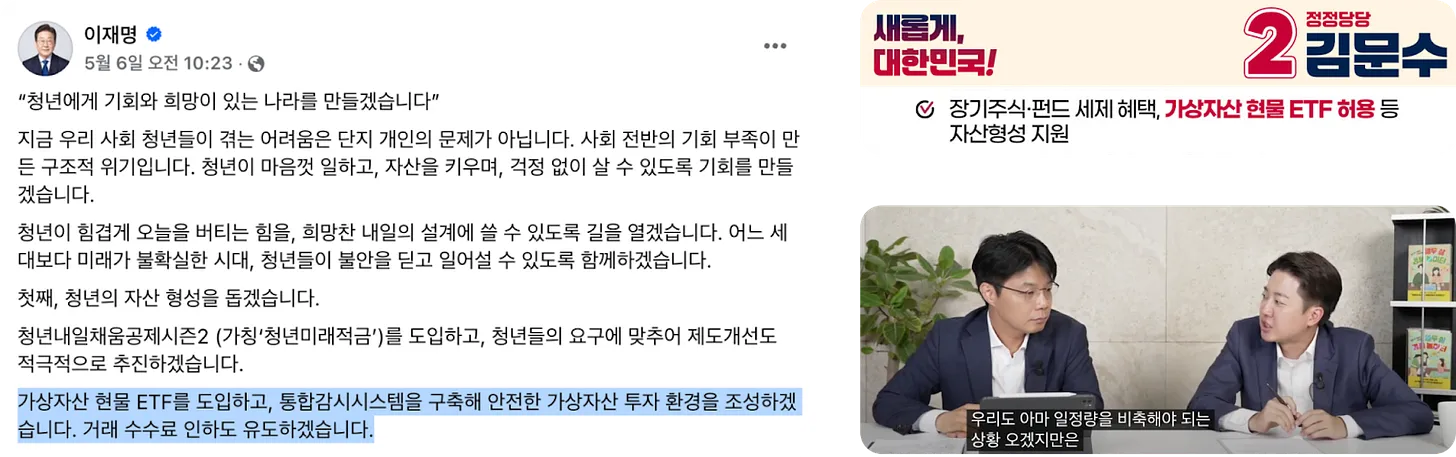

Lee Jae-myung (Democratic Party): On May 6, Lee Jae-myung announced his support for a spot cryptocurrency ETF via Facebook as part of his broader initiative to support youth asset formation. He also proposed lowering investment fees to improve accessibility.

Kim Moo-sung (People Power Party): On April 27, he expressed openness to allowing public institutions to invest in the cryptocurrency market. His ten core policy promises included the introduction of a spot cryptocurrency ETF under the banner of “middle-class wealth expansion.”

Lee Joon-seok (Reform Party): On May 20, Lee Joon-seok proposed through his YouTube channel that the government should hold Bitcoin as a national strategic reserve through tools such as ETFs.

The introduction of a spot cryptocurrency ETF is the only policy proposal that has bipartisan consensus among the leading candidates, making it one of the most likely outcomes to be achieved in the near term. Policy discussions are expected to begin in earnest soon after the election.

If spot ETFs are introduced, they will naturally compete with existing exchanges that facilitate spot trading of Bitcoin. This will promote healthier market dynamics and improve the overall quality of service. For investors, especially those with smaller portfolios, lower fees can reduce barriers to entry and improve accessibility.

In the long run, the launch of spot ETFs could be a catalyst for further financial innovation. It could pave the way for new products that integrate cryptocurrencies with traditional finance, such as derivatives, index funds, and other hybrid investment tools.

2.3. Re-examining the “one exchange, one bank” model

To manage anti-money laundering (AML) risks in the cryptocurrency space, South Korea has maintained an implicit one exchange, one bank principle. Under this model, each licensed cryptocurrency exchange is only allowed to work with one commercial bank to issue real-name verified deposit accounts. For example, Upbit only works with K-Bank, while Bithumb is linked to KB Kookmin Bank.

This framework contrasts with jurisdictions such as the United States, where platforms like Coinbase offer integration with a variety of financial services, including Apple Pay, Google Pay, and various banking institutions.

The debate over abolishing the one exchange, one bank principle began to heat up after Woori Bank President Jeong Jin-wan raised the issue during a policy discussion meeting of People Power Party lawmakers. He argued that the current structure poses systemic risks, limits consumer choices, and imposes unnecessary restrictions on corporate clients. Jeong called for a shift to a one exchange, multiple banks model.

As the presidential campaign unfolds, political parties are beginning to take positions. On April 28, the National Power Party included the abolition of the one exchange, one bank rule in its Seven Digital Asset Commitments. The Democratic Party also appears to be reviewing the matter internally. However, caution has since emerged within the Democratic Party, and it is unclear whether the issue will be reflected in formal campaign promises. Financial regulators have similarly maintained a cautious stance, indicating that any changes may require long-term deliberation.

While regulatory prudence is necessary, maintaining the current model based on concerns about market concentration and anti-money laundering risks may need to be reconsidered. The argument that the rule prevents market monopoly is increasingly unconvincing, as Upbit and Bithumb already control about 97% of the domestic market. Allowing multiple banks to cooperate could enhance competition by enabling exchanges to serve a wider user base. This could result in lower fees and more innovative services for both retail and institutional users.

Concerns about anti-money laundering risks also require more nuanced assessment. In fact, the greater risk occurs during outbound transfers to overseas exchanges. Since the implementation of the Travel Rule and improvements in compliance infrastructure, South Korea now operates under stricter international monitoring standards. Against this backdrop, the systemic risks of allowing multiple banking relationships appear to be exaggerated.

2.4. Korean Won Stablecoin

South Korea has historically prioritized the development of central bank digital currencies (CBDCs) over stablecoins. The Bank of Korea is currently conducting a pilot program called Project Han-Gang to test a CBDC-based payment and settlement system. However, as the global trend shifts toward stablecoins, domestic demand for won-based stablecoins is growing.

Source: 21st Presidential Debate: The First Presidential Debate

Lee Jae-myung (Democratic Party):

May 8: Says in an economic YouTube interview that a won-based stablecoin could prevent capital flight by creating a domestic alternative.

May 18: It was emphasized in a televised debate that the Korean won stablecoin will be backed by collateralized reserves to ensure stability.

Lee Joon-seok (Reform Party):

May 18: Questioned the feasibility of Lee Jae-myung’s proposal, citing a lack of clarity on anti-money laundering measures in the issuance of stablecoins.

Kim Moo-sung (National Power Party):

April 28: Included a regulatory framework for stablecoins in its “Seven Digital Asset Commitments.”

The first presidential debate on May 18 brought stablecoins into mainstream political discourse through a duel between Lee Jae-myung and Lee Joon-seok. While the discussion showed directional support, it also highlighted the lack of a detailed policy framework — especially in terms of risk mitigation and compliance.

At this stage, proposals for a won stablecoin remain aspirational rather than operational. Immediate implementation after the election is unlikely. However, given regional trends — particularly in Singapore and Hong Kong, where authorities are actively developing stablecoins pegged to local currencies — South Korea may face increasing pressure to follow suit in order to maintain its competitiveness as a financial center.

Any meaningful progress will require an underlying legal and regulatory framework. Key issues include identifying eligible issuers, ensuring collateral transparency, establishing anti-money laundering protocols, and defining the relationship between stablecoins and CBDC initiatives. Given the complexity of these issues, policy development is expected to take a phased, medium- to long-term approach rather than a quick post-election change.

3. Gradual but inevitable: the changes that are coming

While the policy shifts discussed are significant for the industry, they are unlikely to materialize in the near term. Among the major presidential candidates, only Kim Moon-soo included Web3-related measures in his top ten campaign promises. This suggests that, despite their relevance to the industry, Web3 issues are not currently prioritized in the broader policy agenda.

Regulatory change is therefore expected to proceed incrementally, with discussions likely to run in parallel with more pressing policy matters. However, the trajectory is clear: transformation is inevitable.

As mentioned earlier, the eventual implementation of cryptocurrency taxation is inevitable. In addition, legislative discussions around security token offerings (STOs) are expected to resume. For investors and market participants, these shifts should not be underestimated. Stakeholders must begin preparing for a policy environment that will become increasingly standardized and compliant.

{kind=link}

{kind=link}