As the United States continues to engage in tariff brinkmanship around the world, Trump recently claimed to have conducted more than 200 trade negotiations and said he had recently spoken with China. However, this statement was quickly refuted by the Chinese Embassy in Washington, which stated that there are no consultations or negotiations between China and the United States on tariffs and emphasized that the United States should stop creating confusion.

Political analysts believe that low-level communications may continue, but it is doubtful whether any substantive agreement can be reached. The trade embargo currently in effect has dragged down economic growth in the first half of the year. We do not believe that there will be any clear solution to the US-China trade negotiations in the foreseeable future.

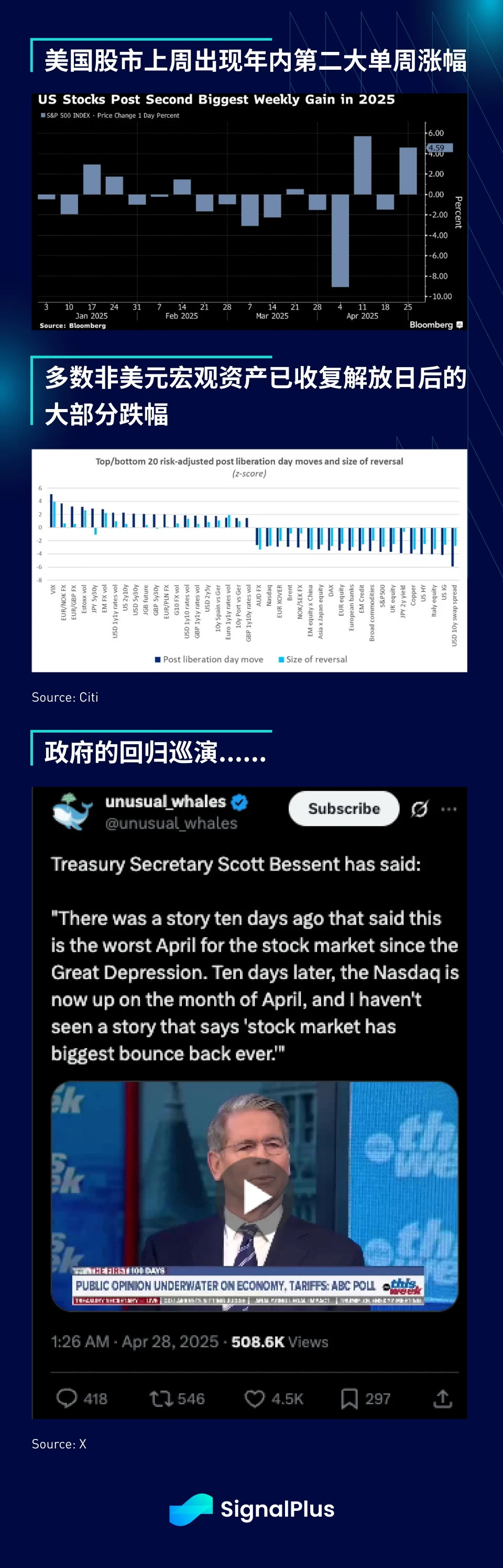

The market stabilized in the absence of further negative news, with U.S. stocks posting their second-largest weekly gain of the year last week and most non-U.S. dollar macro assets recovering most of their losses since Liberation Day.

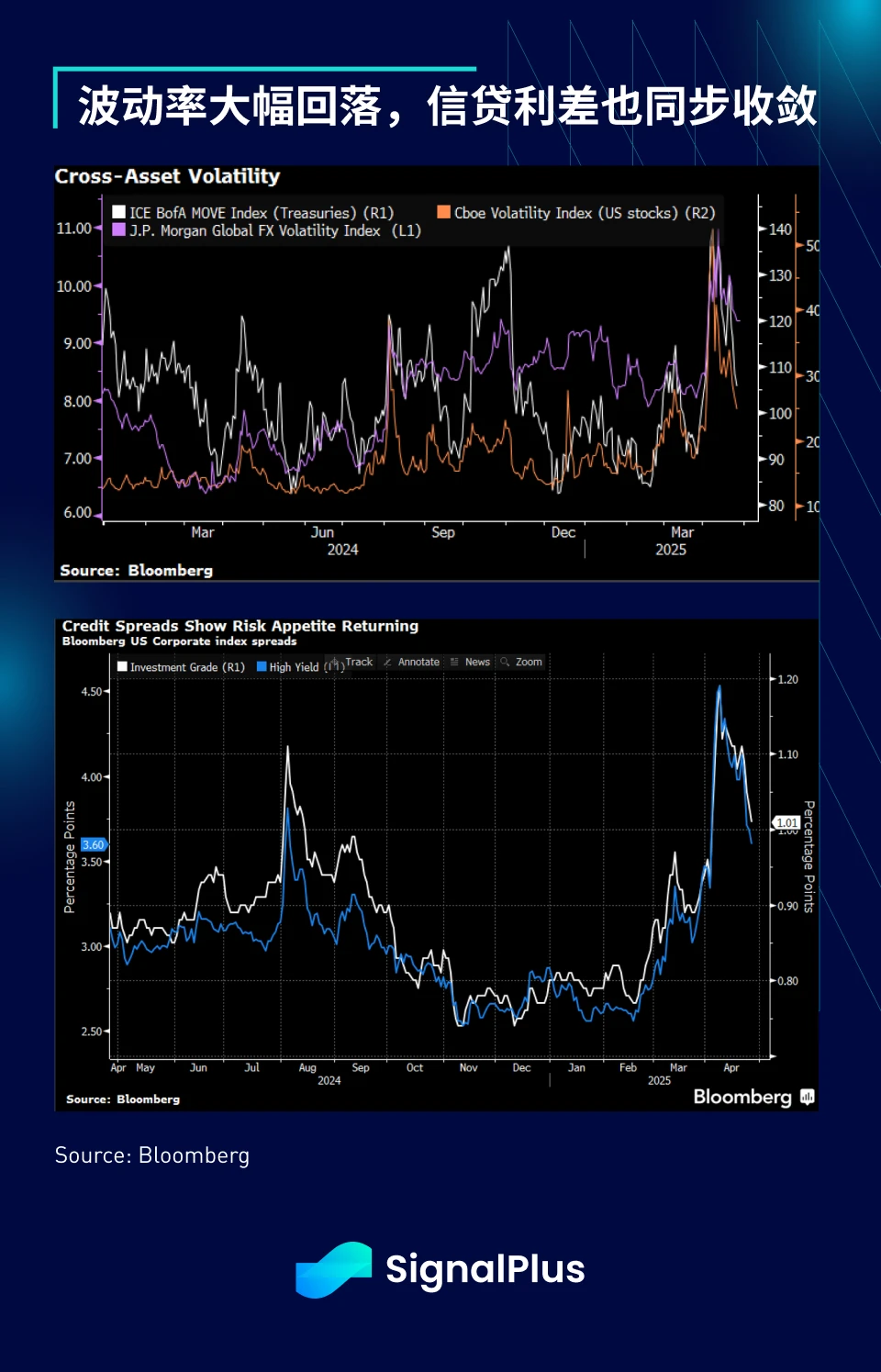

Volatility and credit spreads have similarly recovered, expensive tail hedges are expiring, and the worst-case scenario has not yet occurred (at least for now). We expect risk markets to move further higher to illogical levels before re-entering a more pronounced bearish phase in the second half of this year.

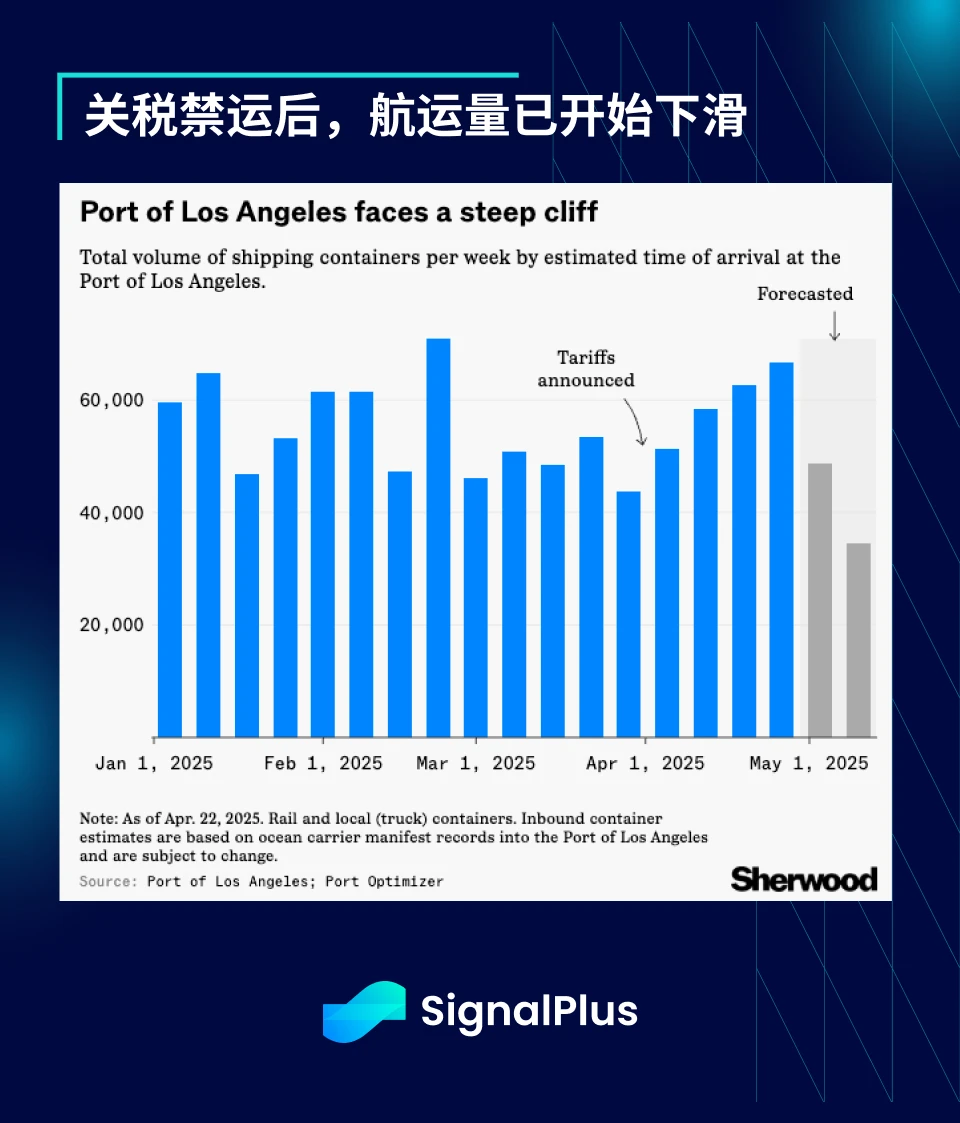

As countries cut reliance on each other’s supply chains, the disruption of trade relations and the damage to economic growth are real. If the US current account deficit begins to reverse in the coming years, global portfolios will also reassess their reliance on the dollar.

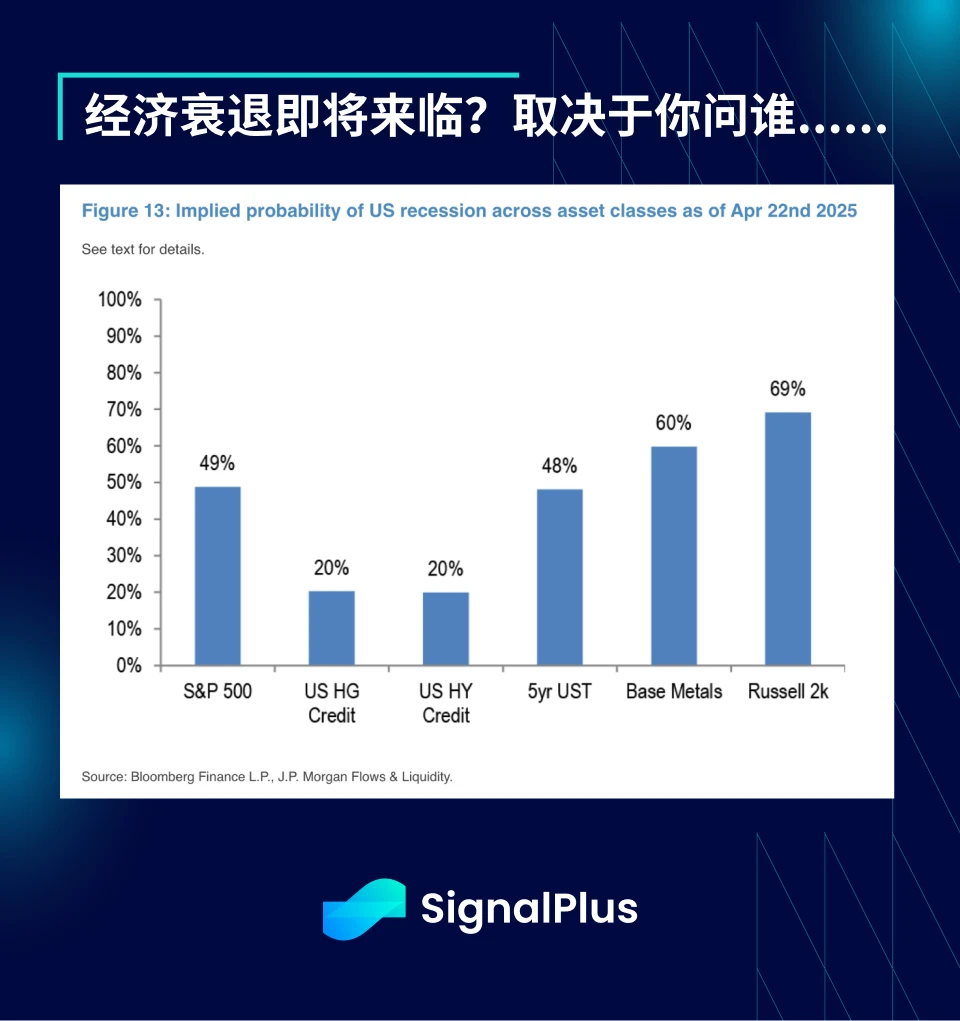

Interestingly, based on historical models, the current credit spread pricing implies a probability of only about 20% for a U.S. recession. On the other hand, the weak performance of small-cap stocks reflects a probability of about 70% for a recession, while U.S. Treasuries and the SPX index basically show a 50-50 trend. Different assets give different answers.

At present, the market is gradually returning to normal. Even U.S. Treasuries have seen the largest four-week inflow of funds in nearly two years. Investors have rushed to buy bonds before the economy is about to slow down and the current inflation pressure continues to cool.

As our long-term readers are well aware, concerns about an imminent collapse in U.S. debt have always been greatly exaggerated. In fact, the size of U.S. debt held by the private sector continued to increase in 2024, offsetting the impact of official (central bank) reductions, and the level of holdings by non-U.S. investors also remained at a relatively high level.

The latest weekly official activity data showed there had not yet been any major sell-off of U.S. Treasuries, and Japans cumulative bond purchases remained stable even as markets worried.

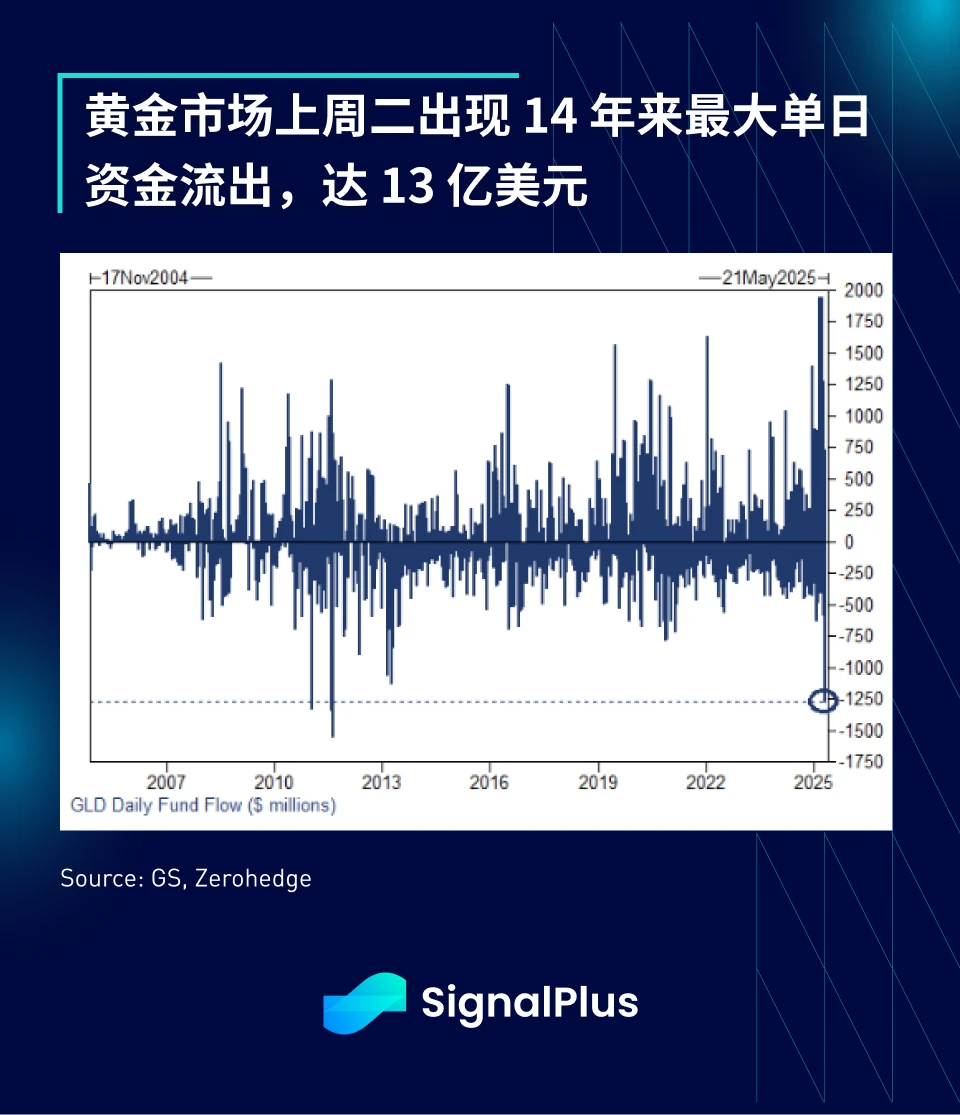

On the other hand, as market risk sentiment rebounded, the gold market saw its largest single-day outflow in more than 14 years last Tuesday, with traders reporting net sales of more than $1.3 billion that day.

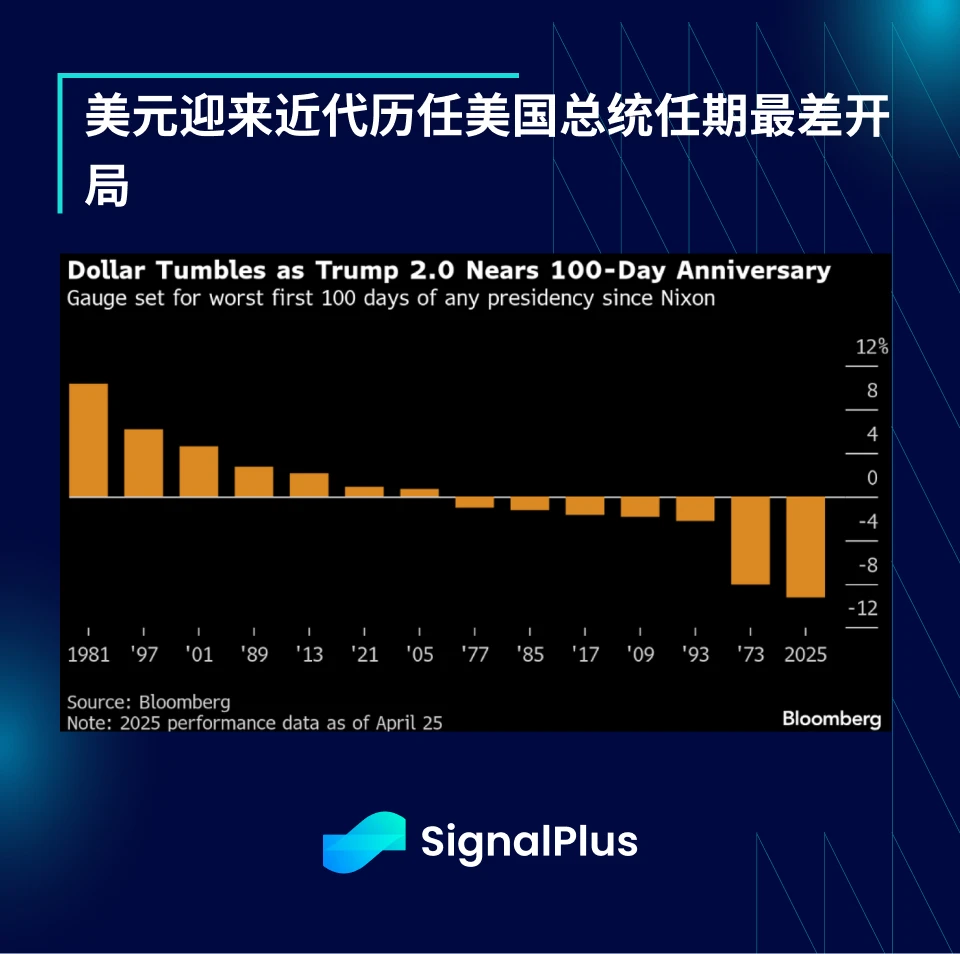

Similarly, the U.S. dollar index performed weakly in the first 100 days of this U.S. president’s presidency, marking its worst start in history, falling more than 10% against major currencies, even worse than when the Bretton Woods system collapsed in 1973.

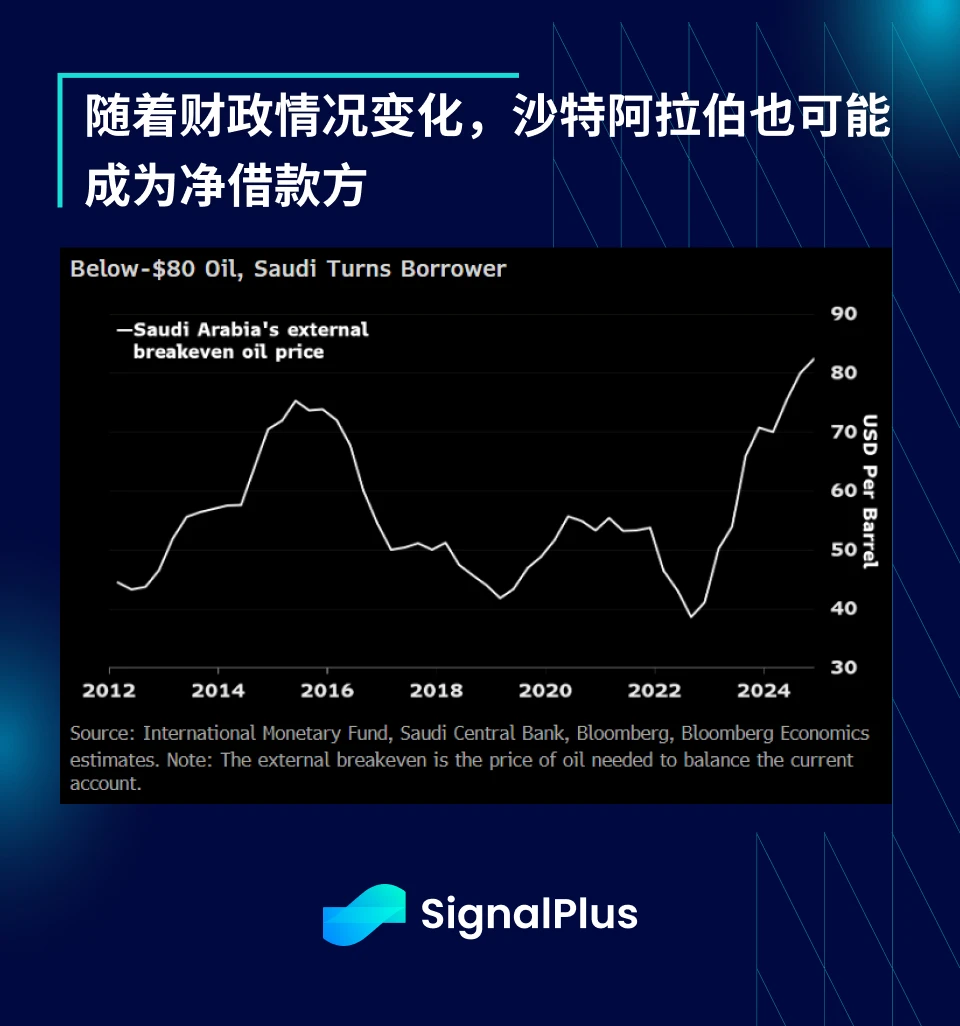

To make matters worse, even if the oil price reaches $80 per barrel, Saudi Arabias fiscal situation may deteriorate from a lender to a borrower, eliminating one of the worlds largest sources of excess capital and raising market concerns about how the United States huge debt will continue to be funded in the future.

Bitcoin has been the main beneficiary of a weak dollar, outperforming both the Nasdaq and gold in April and having one of its best weeks since Trump’s election.

The narrative of BTC as an alternative safe-haven asset continues to grow, as evidenced by the steady increase in its dominance since 2023, which reflects a radical shift in the investment narrative rather than a phenomenon driven solely by market FOMO sentiment.

As market risk sentiment improved, ETF inflows also recovered, recording net inflows for 6 consecutive trading days, recovering from the downturn in the first quarter, and prices also broke through the downward trend line near 88k.

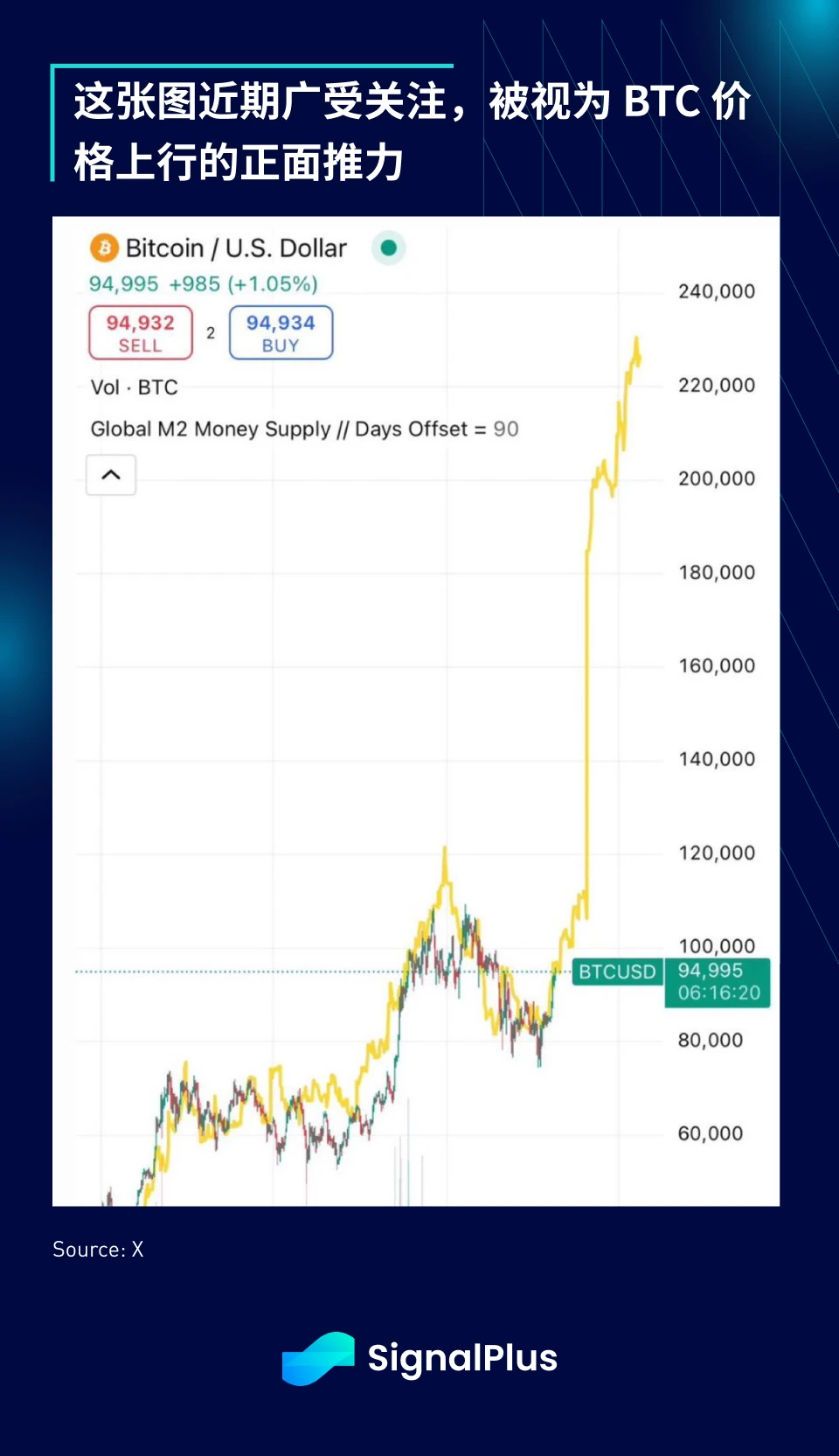

There is a popular argument in the market recently that BTC is about to rise due to the delayed reaction of the increase in M2 money supply. Although we do not fully agree with this view, as there are more complex details behind the data, we are still optimistic about the medium-term trend of BTC, and we expect that monetary and fiscal policies will be relaxed in response to the economic slowdown caused by tariffs.

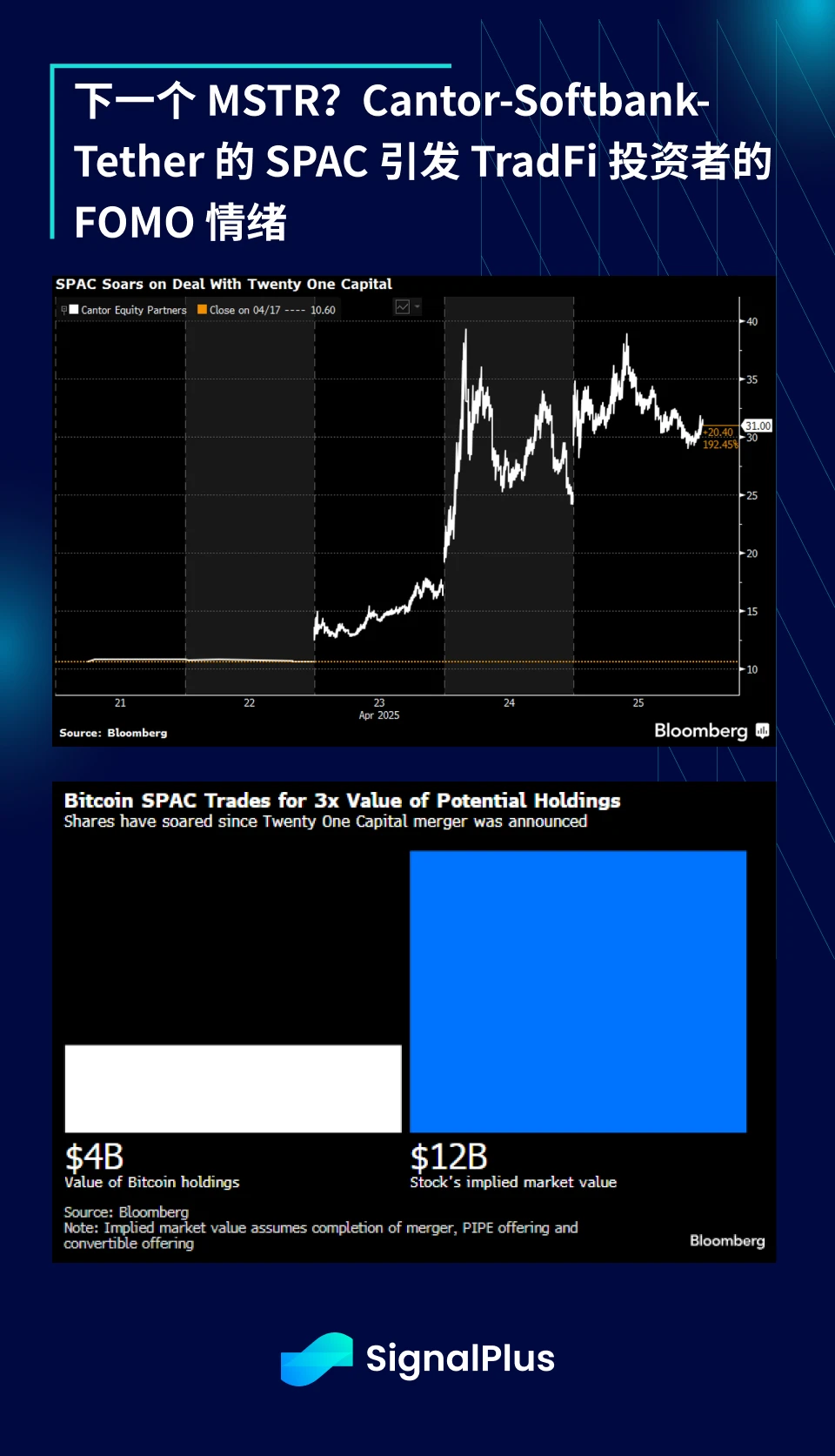

At the same time, we also expect FOMO behavior to return, but it will not necessarily appear in the DeFi native field. The recent Bitcoin SPAC jointly launched by Cantor, SoftBank and Tether has attracted the attention of a large number of TradFi investors.

It is important to note that FOMO sentiment is more likely to flow back from the TradFi market to the cryptocurrency market rather than vice versa. As products linked to cryptocurrencies become increasingly popular on traditional trading platforms, future market booms may be driven by mainstream investor behavior.

Looking ahead to this week, the US and Europe will release their latest GDP data, other inflation indicators will be released in Europe, and the US non-farm payrolls report is scheduled for release on Friday. The Bank of Japan is expected to keep interest rates unchanged at 0.5% at its meeting on Thursday, while the Federal Reserve has entered a silent period before its May 7 meeting.

On the stock market front, more than half of the Mag-7 members (Microsoft, Meta, Amazon, Apple) will report earnings this week, and corporate EPS forecasts have been revised down significantly.

It is expected that the market will turn its focus to economic data and corporate earnings reports this week, ignoring the noise related to trade. I wish you all good trading!

You can use the SignalPlus trading vane function for free at t.signalplus.com/news , which integrates market information through AI and makes market sentiment clear at a glance. If you want to receive our updates in real time, please follow our Twitter account @SignalPlusCN, or join our WeChat group (add the assistant WeChat, please delete the space between English and numbers: SignalPlus 123), Telegram group and Discord community to communicate and interact with more friends.

SignalPlus Official Website: https://www.signalplus.com