Original author | Arthur Hayes

Compiled by | Odaily Planet Daily ( @OdailyChina )

Translator | Dingdang ( @XiaMiPP )

Editors note: Arthur Hayes, co-founder of BitMEX exchange, has just published an article titled Quid Pro Stablecoin, which points out that the US Treasury is promoting the policy of stablecoins issued by large banks to implement debt monetization in disguise to solve the problem of financing huge fiscal deficits. This stablecoin revolution is not actually for financial freedom, but a transfer of financial control tools packaged as innovation. Hayess articles have a strong personal style. In order to ensure that the reading experience is consistent with the original style, Odaily Planet Daily will retain a certain style of the original language when compiling, and only slightly modify some words. The following is the original text:

Stock investors are chanting: “Stablecoin, stablecoin, stablecoin; Circle, Circle, Circle.”

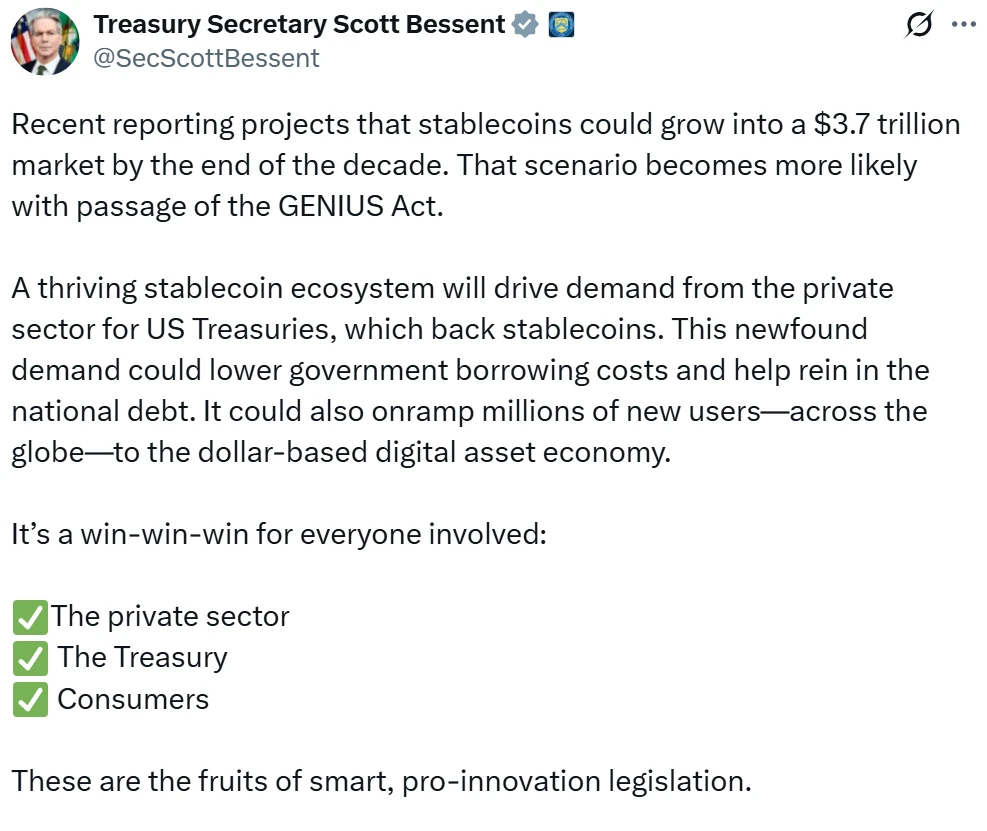

Why are they so bullish? Because U.S. Treasury Secretary Scott Bessent (BBC) believes that a thriving stablecoin ecosystem will drive private sector demand for U.S. Treasuries, which are the backing assets of stablecoins. This new demand could reduce government borrowing costs and help control national debt.

So this chart appeared:

This chart shows the market capitalization comparison between Circle and Coinbase. Don’t forget that Circle has to give 50% of its net interest income to its “father” Coinbase. So why is Circle’s market capitalization nearly 45% of Coinbase? This makes people wonder…

And this chart that makes me sad (after all, I own Bitcoin, not CRCL):

This chart shows Circle’s stock price relative to the price of Bitcoin, indexed to the time Circle went public (100). Since its IPO, Circle has outperformed Bitcoin by nearly 472%.

Cryptocurrency players should ask themselves: Why is the BBC so bullish on stablecoins? Why did the Genius Act gain bipartisan support? Do American politicians suddenly care about financial freedom? Obviously not. Maybe they recognize financial freedom in the abstract, but empty ideals cannot drive substantive actions. There must be more realistic political motivations here. Looking back to 2019, Facebook tried to integrate the stablecoin Libra into its social empire, but was jointly blocked by politicians and the Federal Reserve, and the project eventually died in the womb. To understand why the BBC began to praise stablecoins, we must return to the core problem he faced.

The Ministry of Finance’s urgent need

BBC (i.e. Treasury Secretary Scott Bessent) is facing the same problem as his predecessor Yellen: their bosses ( the US president and politicians in the House and Senate ) are keen to spend money without restraint but are unwilling to raise taxes. The willfulness of the president and congressional politicians ultimately falls on the head of the Treasury Secretary. They must borrow enough funds for the government at a reasonable cost. However, the market soon sent a signal: no one is willing to buy long-term government bonds of debt-ridden developed economies at high prices and low returns. This is the doomsday bond market carnival scene that BBC and Yellen have faced in recent years:

This chart shows 30-year bond yields in the UK (white), Japan (gold), the US (green), Germany (magenta), and France (red).

But what’s worse is that the “real value” of these bonds is being seriously eroded: Real value = bond price / gold price

TLT US is an ETF that tracks US Treasuries with maturities of more than 20 years . Divide it by the price of gold and benchmark it against an index of 100. The result shows that over the past five years, the real value of long-term Treasuries has fallen by 71%.

If the historical record wasn’t bad enough, finance ministers face the following constraints:

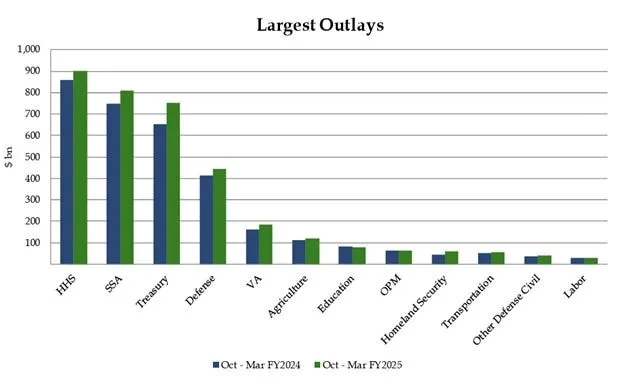

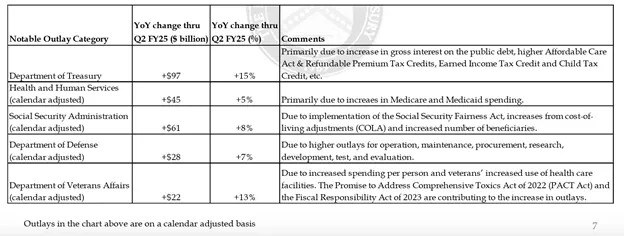

① Financing an annual federal deficit of approximately $2 trillion through 2025, as well as $3.1 trillion in maturing debt.

This table shows the main expenditures of the US federal government and their year-on-year changes. Note that almost all expenditures are growing at a faster rate than nominal GDP.

The first two charts show that the weighted average interest rate on existing Treasury bonds is still lower than any point on the current yield curve.

The financial system issues credit with nominally risk-free government bonds as collateral. Therefore, interest must be paid. Otherwise, once the nominal default occurs, it will destroy the entire dirty fiat financial system.

As maturing debt is refinanced at higher rates, interest expenses will continue to increase because the entire Treasury yield curve is above the weighted average interest rate on current debt.

Given the US wars in Ukraine and the Middle East, the defense budget will not be reduced.

As the baby boomers enter their peak years of receiving “disease care” from Big Pharma, health care spending will continue to increase into the early 2030s, with the government footing the bill.

② The Ministry of Finance must sell bonds while controlling the 10-year Treasury bond yield to not exceed 5%.

Whenever the 10-year yield approaches 5%, the MOVE index (a measure of bond market volatility) soars, and a financial crisis is imminent.

③ The bond issuance method must stimulate the financial market.

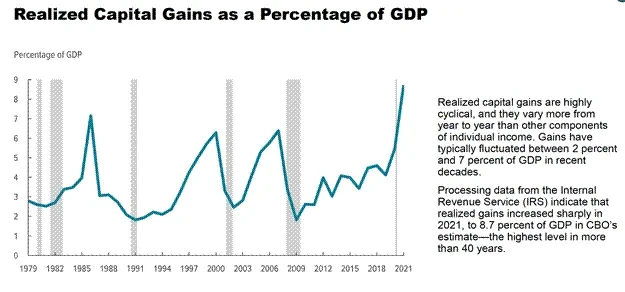

This chart from the Congressional Budget Office shows that capital gains taxes have surged as U.S. stocks have soared since the 2008 financial crisis.

The U.S. government needs to rely on tax revenues from annual stock market gains to make up for its fiscal deficit.

Who does the government serve? The wealthy asset owners, of course. In the past, only white male property owners had the right to vote. Today, even with universal suffrage, power is still dominated by the top 10% of households that control corporate wealth. During the 2008 global financial crisis, the Fed printed money to save the banks and the financial system, but the banks were still allowed to seize peoples homes and businesses. The rich enjoy socialism, the poor face capitalism! No wonder New York mayoral candidate Mamdani is so popular - the poor want a taste of socialism, too.

When the Fed was still implementing quantitative easing (QE), the Treasury Secretarys job was actually easy. The Fed printed money and bought Treasury bonds, which allowed the US government to borrow cheaply and pushed up the stock market. But now that the Fed must at least appear to be fighting inflation, it cannot easily cut interest rates or restart QE. So the Treasury Department has to bear the heavy responsibility alone.

By September 2022, the market began to sell off Treasuries on the margin, driven by the belief that the largest peacetime federal deficit in U.S. history would persist and the Fed’s hawkish stance . In just two months, the 10-year Treasury yield nearly doubled and the stock market fell nearly 20% from its summer high. At this point, Yellen put on her red-soled shoes and took action. In a paper from Hudson Bay Capital , this approach was called Flexible Treasury Issuance (ATI). Yellen began issuing more short-term Treasury bills (T-bills) instead of coupon bonds. Over the next two years, as the Feds reverse repurchase facility (RRP) balance declined, about $2.5 trillion in liquidity was injected into financial markets. If the goal was to achieve the three policy objectives I listed earlier, Yellens ATI policy was perfectly achieved.

But that was then, what about now? It’s the BBC’s turn. How can it accomplish all three tasks in the current environment? With the RRP almost exhausted, where is it going to find the trillions of dollars of idle money that is either sitting on a balance sheet somewhere or willing to buy government bonds at high prices and low yields?

The market environment has been pretty tough in the third quarter of 2022. The chart below shows the Nasdaq 100 Index (green) versus the 10-year Treasury yield (white): As yields surged, stocks also pulled back sharply.

The effect of the ATI policy is that it effectively consumes RRP (red) and drives up financial assets such as the Nasdaq 100 (green) and Bitcoin (magenta). The 10-year Treasury yield (white) has never broken through 5%.

There are still two pools of money in the hands of the large TBTF banks (Too Big to Fail, Systemically Important Banks) that are willing to buy trillions of dollars of Treasury bonds as long as there is enough profit incentive. These two pools of money are: demand/time deposits and reserves held by the Federal Reserve . I focus on these eight TBTF banks in particular because their existence and profitability depend on government guarantees on their liabilities, and regulatory policies are more favorable to them than non-TBTF banks. Therefore, as long as there is a little profit margin, they are willing to follow the governments instructions. If the BBC asks them to buy these bad debts, in return, he needs to give them a risk-free return.

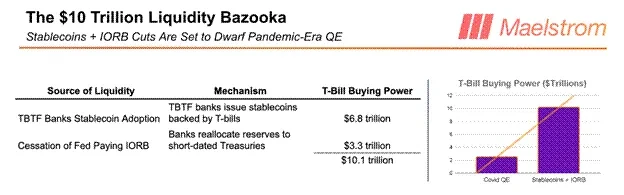

I think the reason why the BBC is so excited about stablecoins is that once stablecoins are issued by TBTF banks, they can release up to $6.8 trillion in short-term Treasury bill purchasing power. These previously idle deposits can be re-leveraged in this illusory fiat financial system, thereby boosting the market. In the next section, I will explain my model in detail to show how the issuance of stablecoins can guide short-term Treasury bill purchases and improve the profitability of TBTF banks.

After talking about the “stablecoin → short-term treasury bill” fund flow, I will also briefly explain that if the Fed stops paying interest on reserves, it will release up to $3.3 trillion in treasury bond purchasing power. This will be another policy that is not technically QE, but has the same positive impact on fixed supply monetary assets such as Bitcoin. Let’s learn about the BBC’s new favorite today - stablecoins.

Stablecoin liquidity mechanism

My forecast is based on several key assumptions:

Assumption 1: Treasury bonds are fully or partially exempted from being included in banks’ supplementary leverage ratio (SLR)

Once exempted, banks do not need to set aside regulatory capital for their government bonds. If fully exempted, banks can purchase government bonds with unlimited leverage.

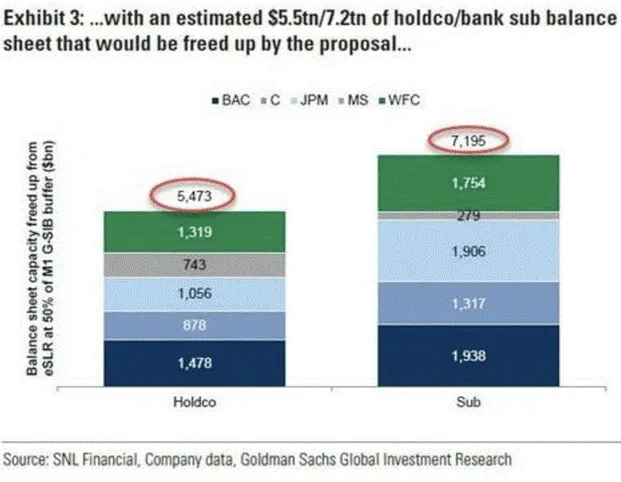

The Federal Reserve has voted to reduce the capital requirements for banks to hold Treasuries. This policy is expected to take effect in the next three to six months. According to the above chart, this new rule can free up $5.5 trillion of balance sheet space for banks to buy Treasuries. Given the forward-looking nature of the market, this will push the Treasury market to start rising before the policy is implemented, thereby pushing down yields (other things being equal).

Assumption 2: Banks are profit-seeking institutions that are good at controlling losses

Between 2020 and 2022, the Fed and the Treasury encouraged banks to buy a lot of Treasury bonds. As a result, they actually bought a lot of high-yield bonds that matured in the long term. However, in April 2023, the Fed implemented the most aggressive interest rate hike cycle since the 1980s, which led to severe bond losses and three bank failures in a week. Even TBTF banks were not immune. For example, Bank of Americas losses on its held-to-maturity bond portfolio exceeded its entire equity capital - if it was marked to market, the bank would face technical bankruptcy. To quell the crisis, the Fed and the Treasury effectively nationalized the entire US banking system through the Bank Term Funding Program (BTFP). Although non-TBTF banks can still fail, they will only be acquired cheaply by large banks such as Jamie Dimon (CEO of JPMorgan Chase). As a result, bank chief investment officers are no longer willing to buy long-term Treasury bonds to prevent the Fed from suddenly raising interest rates again.

However, short-term Treasury bills are different. They have almost no interest rate risk, but their returns are close to the federal funds rate, making them “zero-duration high-yield cash instruments.”

Banks will only be willing to use customer deposits to buy short-term treasury bills if they meet both the high net interest margin (NIM) and extremely low capital occupation conditions.

What is JPMorgan doing?

JPMorgan Chase recently announced that it will issue a stablecoin called JPMD. JPMD will be deployed on Coinbases Ethereum second-layer network Base. Therefore, JPMorgan Chase will have two types of deposits.

The first is what I call conventional deposits. Conventional deposits are still digital, but moving them around the financial system requires banks to communicate with each other using outdated systems and requires a lot of human oversight. Conventional deposits move between 9 a.m. and 4:30 p.m. Monday through Friday. Conventional deposits have low yields; the Federal Deposit Insurance Corporation (FDIC) estimates that the average yield on a conventional demand deposit is just 0.07%, and on a one-year time deposit is 1.62%.

The second type of deposit is a stablecoin, JPMD. JPMD is based on a public blockchain, in this case Base. JPMD is available to customers 24/7, 365 days a year. JPMD is not legally allowed to pay interest, but I imagine JPMorgan Chase will entice customers to convert regular deposits to JPMD by offering generous cashback on purchases. It is not clear whether staking yields are allowed.

Pledge interest: Clients lock JPMD in JPMorgan Chase and receive interest during the lock-up period.

The reason why customers are willing to convert regular deposits to JPMD is precisely because JPMD is more powerful and has cashback incentives. The entire TBTF banking system currently has about $6.8 trillion in demand and time deposits. With the overwhelming advantages of stablecoin experience, these deposits will quickly migrate to JPMD or other TBTF-issued stablecoins.

Why would JPMorgan Chase go to the trouble of encouraging clients to switch to JPMD?

First: reduce costs and increase efficiency.

If all regular deposits were switched to JPMD, JPMorgan could effectively eliminate its compliance and operations departments. Let me explain why Jamie Dimon got excited after learning how stablecoins actually work.

Compliance in the banking industry is essentially a system of rules that says “if X happens, do Y.” These rules can be sorted out by a senior compliance officer and automatically executed by AI. Since JPMD operates on a public blockchain, all addresses can be tracked, and AI can achieve real-time control of the compliance process. It can also generate reports for regulatory audits in seconds, with all data on the chain and full transparency. TBTF banks spend up to $20 billion a year on compliance and IT systems. If all are switched to a stablecoin system, this cost will effectively be reduced to zero .

The second reason is that JPMD allows banks to purchase billions of dollars of short-term Treasury bills risk-free with managed stablecoin assets (AUC).

As long as the regulator allows, TBTF banks will use these deposits to buy government bonds, killing two birds with one stone: making money while helping the Treasury raise funds. After the new SLR rules are relaxed, banks will have about $5.5 trillion in government bond purchase space.

Some readers may say, Cant JPMorgan buy short-term Treasury bills with regular deposits now? My response is: stablecoins are the future. They bring a better customer experience and help banks save $20 billion in costs. The cost savings themselves are enough to drive banks to embrace stablecoins, and the additional net interest margin is just icing on the cake.

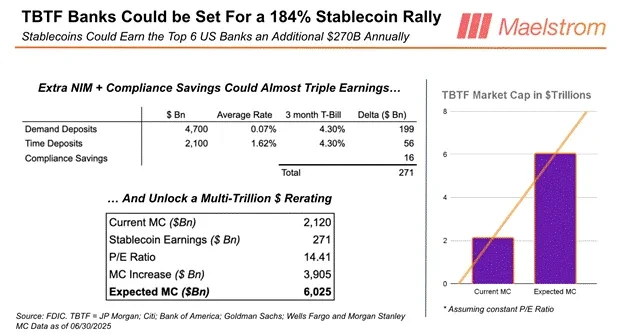

I know many investors are eager to invest their hard-earned money in Circle (CRCL) or other newly issued stablecoin projects. But dont ignore the potential of TBTF banks. If we multiply the average PE ratio of TBTF banks (14.41 times) by the cost savings and net interest margin benefits brought by stablecoins, its valuation can reach $3.91 trillion. The total market value of the eight largest TBTF banks is currently about $2.1 trillion. In other words, stablecoins are expected to increase TBTF bank stock prices by an average of 184%. If you are looking for a counter-consensus, large-scale position trading opportunity, it is: go long a basket of TBTF bank stocks with equal weight allocation.

What about competition?

Don’t worry, the Genius Act ensures that non-bank-issued stablecoins cannot compete on a large scale. The act explicitly prohibits technology companies (such as Meta) from independently issuing stablecoins, and must cooperate with banks or fintech companies. In theory, any institution can apply for a banking license or acquire an existing bank, but all new shareholders must be approved by regulators. Guess how long this approval will take?

Another provision in the bill also hands the stablecoin market to banks: it prohibits paying interest to stablecoin holders. Since interest cannot be used to attract users, fintech companies cannot absorb deposit flows from banks at all. Even companies like Circle that have successfully launched stablecoins will never be able to access the $6.8 trillion in regular deposits held by TBTF banks.

In addition, fintech companies like Circle or small banks do not have government credit guarantees for their debts, while TBTF banks do. If my mother really wants to use stablecoins one day, she will definitely choose the ones issued by TBTF banks. Baby boomers like her will never trust fintech companies or small banks because they do not have government backing.

Summary: Why TBTF Bank’s adoption of stablecoins will completely change the rules of the game?

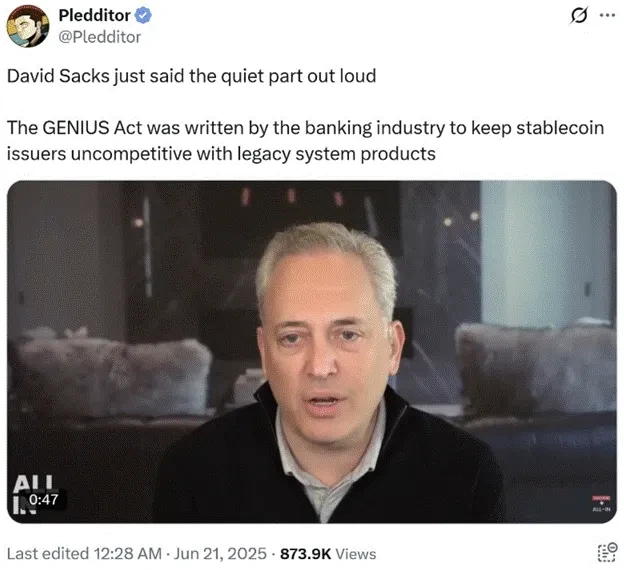

David Sacks, former US President Trump’s appointed “Director of Cryptocurrency Affairs”, feels the same way. I bet that many crypto political donors are upset to see that they are finally excluded from the golden pie of the US stablecoin market. Maybe they should change their strategy and really promote “financial freedom” instead of just picking up scraps from the dinner table of TBTF bank CEO.

In short, TBTF Bank’s stablecoin strategy will: destroy fintech companies’ opportunities in deposit competition; cut high and inefficient compliance costs; increase net interest margin (NIM) without paying interest; and drive bank stock prices up significantly.

In exchange, as long as the BBC grants the stablecoin tool, TBTF Bank will use its stablecoin asset custody balance to purchase up to US$6.8 trillion in short-term government bonds.

Next, I discuss how the BBC is releasing $3.3 trillion of idle reserves from the Federal Reserves balance sheet.

Interest on Reserve Balances (IORB)

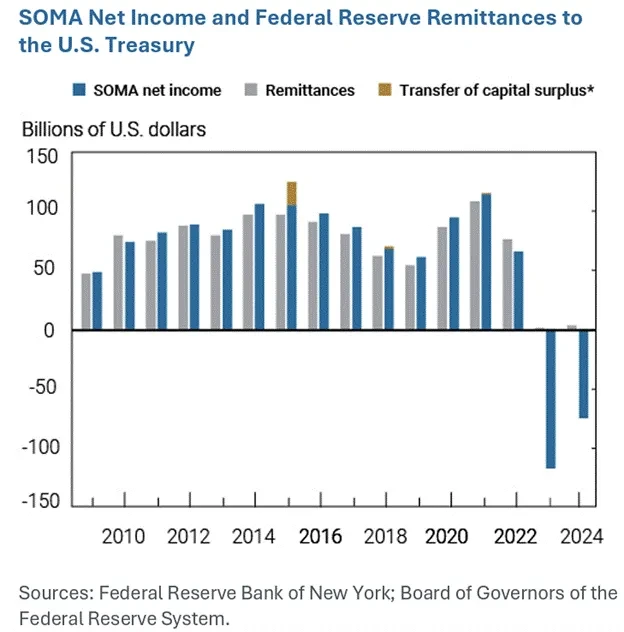

After the 2008 Global Financial Crisis (GFC), the Fed decided to make sure that banks would never go bankrupt due to insufficient reserves. It created reserves by buying Treasury bonds and MBS (mortgage-backed securities), which is what we call quantitative easing (QE). These reserves sit in the banks accounts at the Fed and can theoretically be converted into real money, but the banks dont do this because the money the Fed prints is enough to pay the banks interest.

This interest (IORB) was meant to prevent a surge in inflation, but once interest rates rise, IORB rises, and the Feds book losses on bonds also increase. As a result, the Fed is in a state of negative cash flow and technical insolvency. However, this is entirely a policy choice and can change at any time.

Recently, US Senator Ted Cruz proposed that the Federal Reserve should stop paying interest on reserves to banks. Once this is done, banks will have to convert these reserves into Treasury bonds to make up for this interest loss. I think they are more likely to buy short-term Treasury bonds because these assets have high returns, low volatility, high liquidity, and are similar to cash.

Senator Cruz has been pushing his colleagues to end the IORB mechanism as he believes the reform will significantly help reduce the fiscal deficit. - Reuters

To put it bluntly, why does the Fed print money to pay interest, but not let the banks support the financial operations of this empire? There is no reason. Whether it is the Democrats or the Republicans, everyone likes fiscal deficits. If they stop paying IORB and release the purchasing power of this $3.3 trillion, they can borrow more and spend more freely.

And the Fed is unwilling to pay for Trump’s “America First” agenda? Then the Republicans, once they take control of Congress, could push for legislation to strip the Fed of its power to pay the IORB. The next time bond yields soar, Congress will be ready to release this massive liquidity to finance their new spending spree.

Adjustment of holding strategy during the cautious period

While I remain optimistic about the future, I think there may be a small liquidity vacuum after the passage of Trumps Big Beautiful Bill.

The current draft of the bill already includes a clause to raise the debt ceiling. Although there is still a lot of content waiting for political games, it is certain that Trump will not sign any version that does not raise the debt ceiling. He needs additional debt space to advance his governance goals. The problem is that when the Treasury resumes net borrowing operations, the US dollar liquidity will be compressed in the short term.

Since January 1, the Treasury has been maintaining government spending by draining its checking account, the Treasury General Account (TGA). As of June 25, the account balance was $364 billion. According to the Treasurys latest quarterly refinancing announcement, if the debt ceiling is raised at this time, the TGA account will be replenished to $850 billion in the short term. This means that US dollar liquidity will shrink by $486 billion . The only variable that can buffer this negative impact is the change in the balance of reverse repurchase agreements (RRP). The current RRP balance is $461 billion.

I dont think this is a decisive signal to short Bitcoin, but a market phase that needs to be treated with caution. I think Bitcoin will fluctuate or slightly correct from now until the Jackson Hole conference in August. If TGA replenishment really causes liquidity tightness, Bitcoin may retreat to the $90,000-$95,000 range in the short term. But if the market reacts flatly, Bitcoin is expected to consolidate and fluctuate in the $100,000 range, waiting to break through the historical high ($112,000).

I guess that by then, Powell will announce the end of quantitative tightening (QT) at the meeting, or release some seemingly unremarkable but highly influential new bank regulatory policies. By early September, when the debt limit is raised and the TGA is filled, the Republican Party will also fully enter the stage of spending money to buy votes to ensure that the 2026 midterm elections will not be crushed by figures like left-wing candidate Mamdani. By then, the green K-line will pierce the short-selling defense line, and the capital market will once again usher in a surging torrent of funds.

Maelstrom (our portfolio) will be overweight in collateralized USDe (Ethena USD) from now until the end of August. We have liquidated all altcoin positions. Depending on price action, we may also moderately reduce our exposure to Bitcoin. Some of the altcoins bought around April 9 have brought 2x to 4x returns in three months. But in the absence of a clear liquidity catalyst, the altcoin sector is likely to be bloodbathed. After this wave of pullback, we can confidently pan for gold in the garbage dump and perhaps get a 5x or 10x return before the next low tide of fiat currency liquidity creation in late 2025 or early 2026.

Tick the Boxes

TBTF Bank issues stablecoins that could unlock up to $6.8 trillion in purchasing power for short-term Treasury bonds.

The Federal Reserves cessation of interest payments on reserves (IORB) will further free up the purchasing power of $3.3 trillion in short-term Treasury bonds.

A total of $10.1 trillion is expected to flow into the short-term Treasury market through the BBC policy mix. If my prediction comes true, this wave of $10.1 trillion in liquidity injection will have the same level of stimulus effect on risky assets as the $2.5 trillion that Yellen injected that year.

This is another liquidity arrow in the hands of Treasury Secretary Scott, which can be pulled out of his policy quiver when necessary and hit the market directly. And when necessary may be after Trumps Big Beautiful Bill is passed and the debt ceiling is raised. At that time, market concerns will re-emerge: How can this massive amount of Treasury bonds be sold without blowing up the entire market?

Are you still waiting for Powell to announce unlimited quantitative easing (QE Infinity) and a sharp rate cut before you sell bonds and buy cryptocurrencies? Wake up - at least until the United States clearly enters a hot war with Russia, China, Iran, or a systemically important financial institution explodes, that scene will not appear, and even a recession will not be called.

Many financial advisors are still telling clients to buy bonds, citing the upcoming downward yield curve. I agree that central banks around the world will eventually cut rates and print money to avoid a collapse in government bond markets. And even if the central banks don’t, the Treasury will. This is the core point I’m making in this article: I believe Bessent will be able to unlock up to $10.1 trillion in Treasury buying power by supporting stablecoin regulation, granting an SLR (supplementary leverage ratio) exemption, and stopping interest on reserves (IORB). But here’s the thing: what’s the point of holding bonds for a long time to make 5% or 10%? You’ll miss out on Bitcoin skyrocketing 10x to $1 million, or the Nasdaq 100 surging 5x to 100,000 (expected to happen in 2028).

The real stablecoin opportunity is not to bet on old fintech companies like Circle, but to see clearly that the US government has handed a trillion-dollar liquidity nuclear warhead disguised as innovation to those TBTF banks.

This is not DeFi, this is not financial freedom. This is debt monetization dressed up as Ethereum.

And if you are still waiting for Powell to whisper unlimited QE to you before starting to increase your holdings of risky assets, then I can only say: congratulations, you are the liquidity exit when others retreat.

Instead, go long Bitcoin, go long JPMorgan, and forget about Circle .

The Trojan horse of stablecoins has crept into the castle. When it opens, it is filled not with libertarian dreams but with a liquidity bomb of Treasury bonds bought with trillions of dollars to prop up the stock market, finance the fiscal deficit, and keep the baby boomers safe.

Don’t sit on the sidelines waiting for Powell’s blessing. The BBC is “warmed up” and now he’s going to spread his liquidity juice all over the world.