Overview

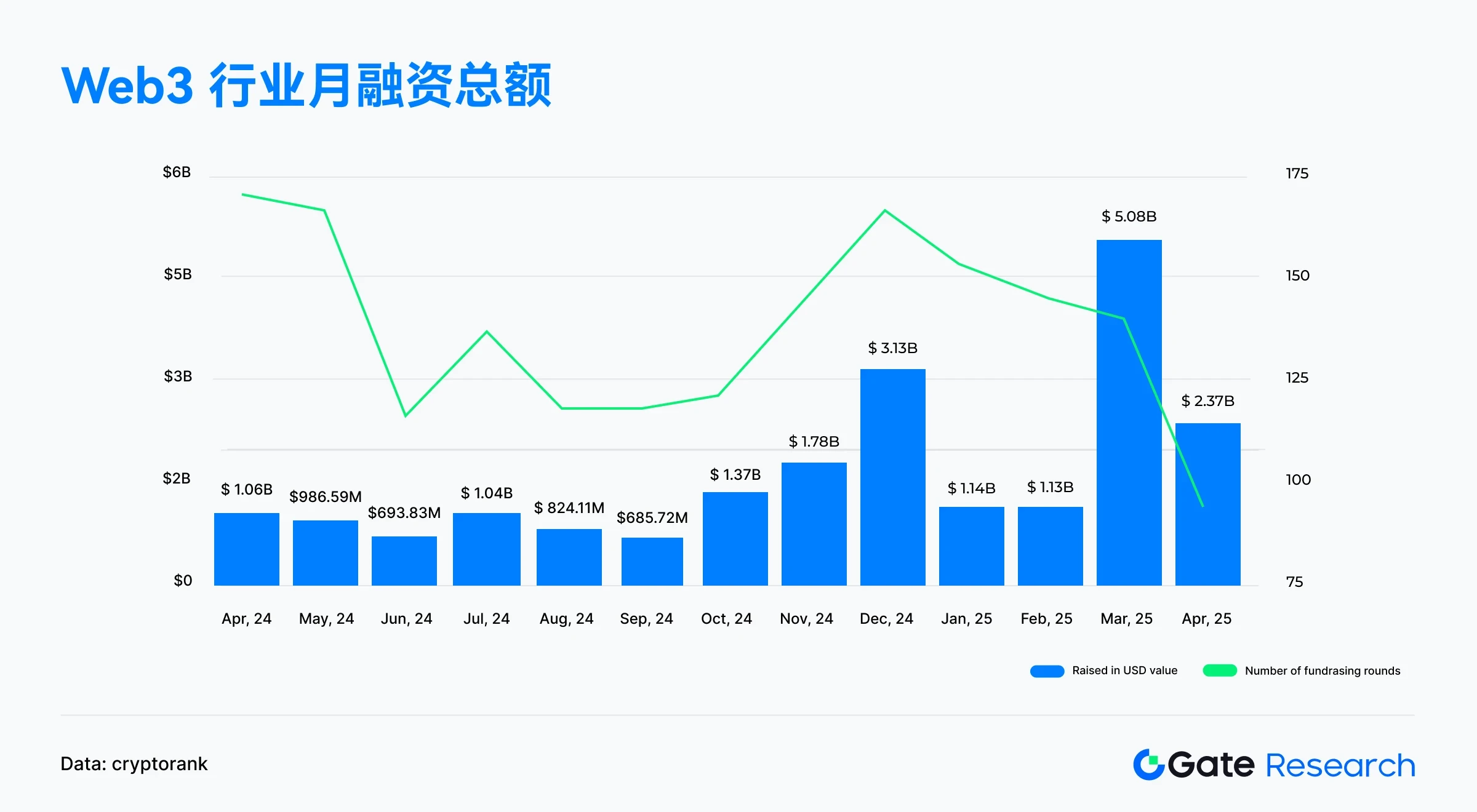

• According to the Cryptorank Dashboard data on May 7, 2025, the Web3 industry completed 94 financings in April 2025, with a total of US$2.37 billion. The scale and number of financings both declined, and the market has obviously cooled down.

• Traditional financing methods are returning, with MA and structured financing dominating large transactions. These include Ripple’s acquisition of Hidden Road for $1.25 billion, reflecting the market’s preference for resource integration capabilities, risk control mechanisms, and mature development paths.

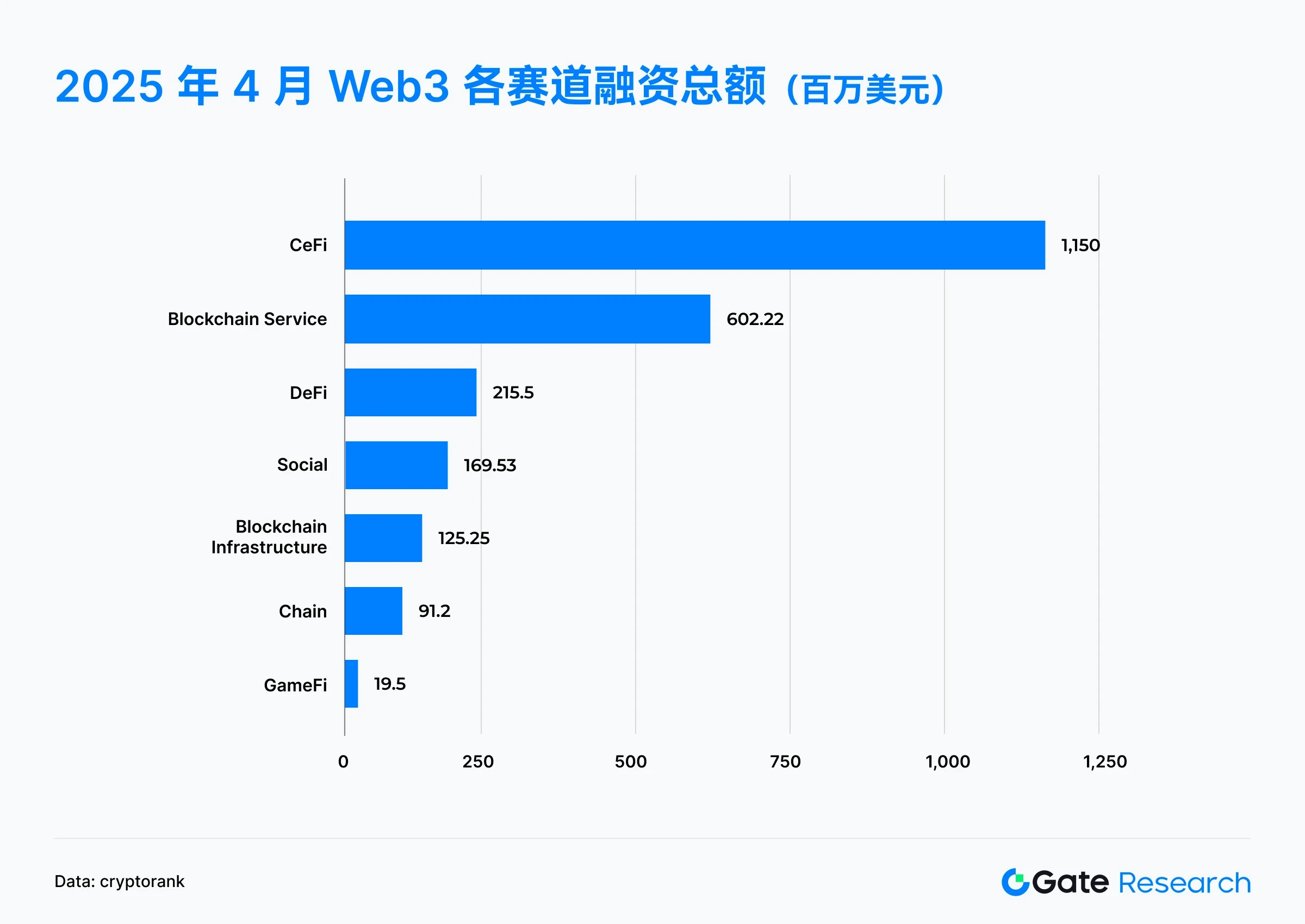

• Financing in April was mainly concentrated in CeFi (US$1.15 billion) and blockchain services (US$602 million), followed by DeFi and Social; this shows that capital is more inclined to bet on Web3 companies with traditional financial integration capabilities and clear compliance paths.

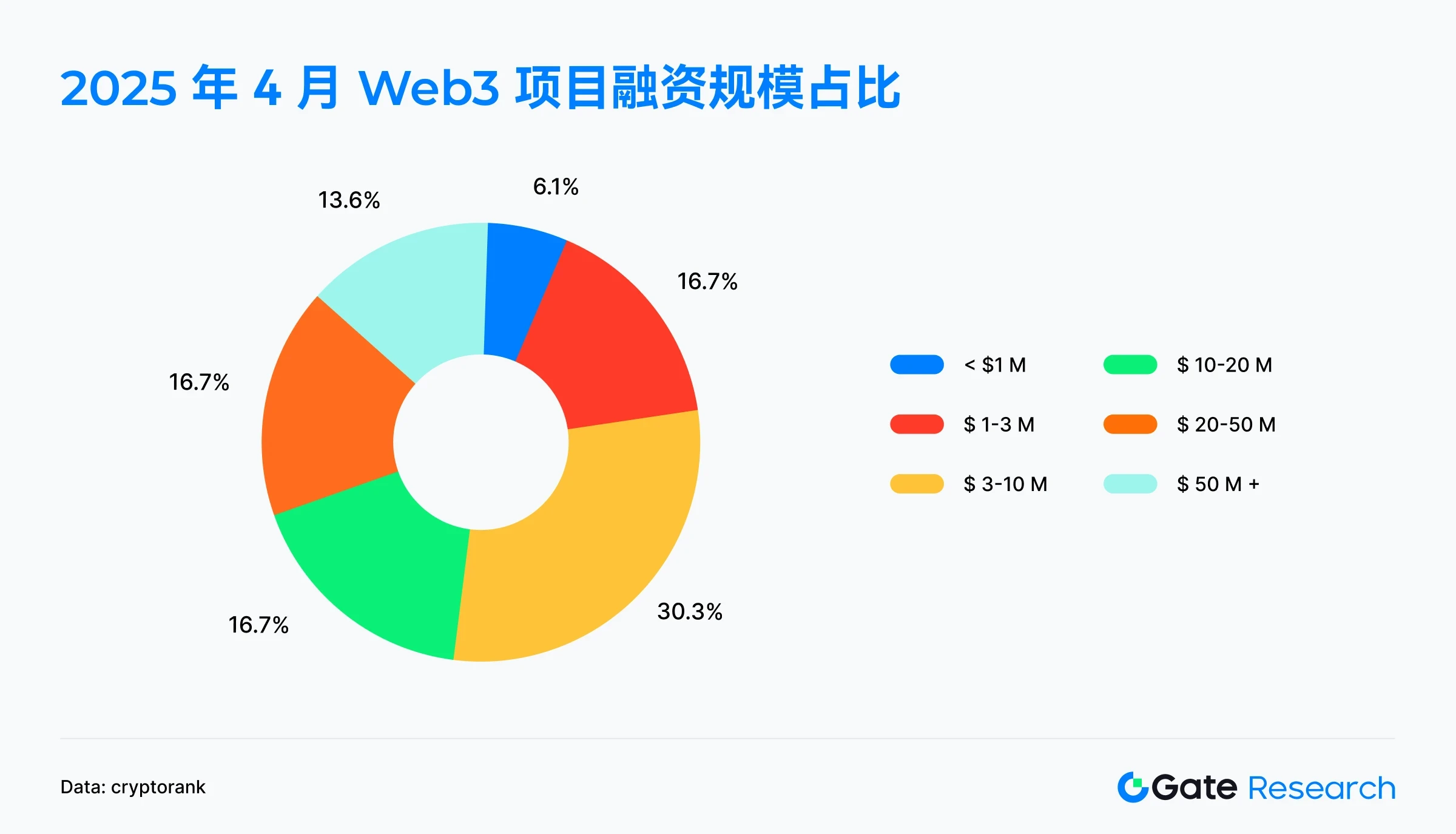

• The Web3 financing ecosystem is shifting from “cast-net support” to “structured betting”, with medium and large projects dominating. Projects with financing amounts exceeding US$10 million account for 47%, reflecting that capital prefers mid-tier projects with commercialization paths and growth verification capabilities.

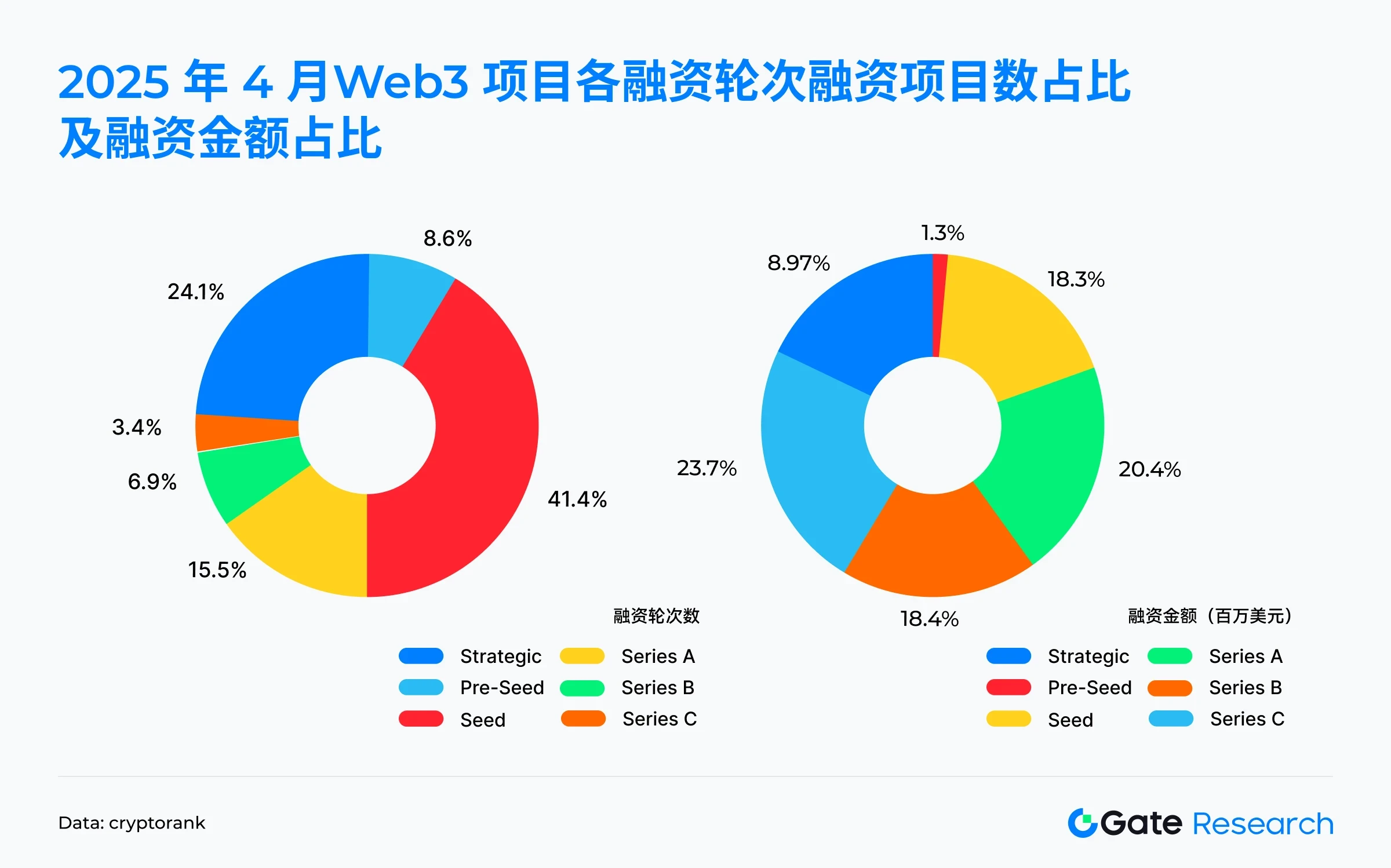

• The financing rounds show a structure of small at both ends and large in the middle, and funds are clearly concentrated on mid- and late-stage projects. Although the number of seed round projects is the largest (accounting for 41.4%), the C round of financing attracted the most funds, accounting for 23.7% of the total financing amount, indicating that capital is focused on mature projects with scalability potential.

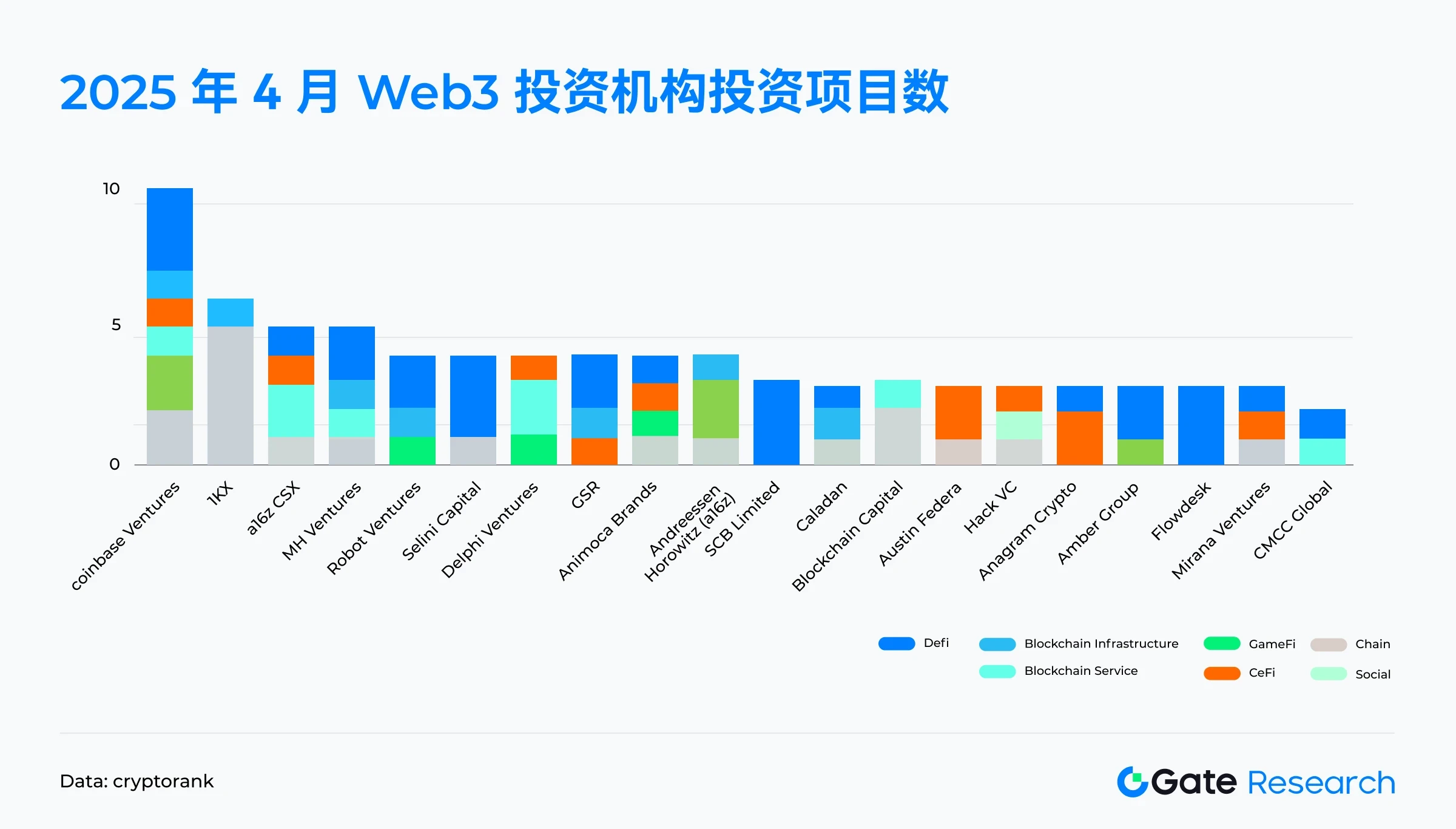

• Coinbase Ventures leads the way with investments in 10 projects, covering DeFi, CeFi and blockchain infrastructure; 1kx, a16z CSX and others follow closely behind.

Financing Overview

According to the data released by Cryptorank on May 7, 2025, the Web3 industry completed 94 financings in April 2025, with a total financing amount of US$2.37 billion. [1] Due to the special treatment of Cryptorank in statistical caliber, this amount is somewhat different from the total amount of individual financing projects (approximately US$3.68 billion); however, in order to maintain consistency with the analysis trend below, this article uses the original statistical caliber provided by its dashboard.

Compared with US$5.08 billion and 140 transactions in March 2025, the total financing amount fell by more than 53% month-on-month, and the number of financing transactions also fell below 100, setting a new low in the past year.

Previously, Web3 financing experienced explosive growth in the first quarter of 2025, especially in March, when the total amount of financing climbed to a historical peak, driven by huge transactions such as Abu Dhabi MGXs $2 billion investment in Binance and Krakens $1.5 billion acquisition of NinjaTrader. However, the market cooled down significantly in April, and the number of financing transactions shrank significantly.

This phenomenon may be driven by the following factors: short-term wait-and-see sentiment after the concentrated release of funds in the first quarter; market correction or stricter regulatory expectations; or perhaps some financing has shifted to more hidden private placements or strategic orientations, resulting in a decrease in publicly disclosed large financing cases. It is worth noting that although the total amount of financing is still high, the number of financings has shown a downward trend since March, indicating that funds are accelerating to concentrate on a few capital-intensive projects, and financing for small and medium-sized projects is becoming more difficult. The Matthew effect within the industry is gradually emerging.

According to the data analysis of the TOP 10 financing projects in April 2025, it can be seen that capital is highly concentrated in a few leading projects, further confirming the trend of the markets Matthew effect continuing to intensify [2].

CeFi still occupies a dominant position: Among the top ten projects, 6 belong to the centralized finance (CeFi) track, with a total financing amount of more than 1.9 billion US dollars, which fully demonstrates that despite the continuous development of the DeFi ecosystem, centralized financial infrastructure is still the most favored area by capital. Among them, SOL Strategies and Securitize have completed large-scale fundraising through traditional financing tools such as post-IPO debt, indicating that the capital market still gives high valuation and liquidity support to Web3 companies with traditional financial integration capabilities.

Traditional financing methods have returned strongly: mergers and acquisitions (MA), post-IPO debt and private placement have become high-frequency financing methods, reflecting that the current market is more inclined to the capital path of controlling acquisition + structured financing to strengthen resource integration and risk control capabilities. It is worth noting that Hidden Road ranked first with a $1.25 billion MA transaction, acquired by Ripple, indicating that traditional blockchain giants are accelerating their strategic layout in the field of CeFi credit networks.

Infrastructure projects are still favored by top capital: The only blockchain infrastructure project in the top ten this month is LayerZero, which received support from a16z and completed a $55 million financing, showing that even in the context of tightening funds, basic interoperability technology still has strong appeal.

In general, the financing landscape in April 2025 presents three major characteristics: CeFi-dominated, MA-driven, and capital centralized. This not only reflects the capital markets increasing emphasis on compliance, profit models, and integration capabilities, but also indicates that the future Web3 investment and financing landscape will further concentrate on a small number of projects with resource advantages and institutional endorsements.

According to the Cryptorank Dashboard data, the financing pattern of the Web3 industry in April 2025 showed a trend of CeFi leading strongly, basic services being stable, defensive technologies being favored, and prudent investment in innovative tracks, and capital allocation preferences gradually shifted from high-risk experimental projects to mature fields with stronger profitability and integration capabilities. The specific performance is as follows:

• CeFi (centralized finance) ranked first with a total financing of US$1.15 billion, accounting for nearly half of the total financing that month, indicating that capital still prioritizes centralized projects with traditional financial attributes and clear compliance paths. Several large transactions (such as Hidden Road and SOL Strategies) have boosted the volume of this track, highlighting the markets high recognition of CeFis infrastructure integration capabilities.

• The Blockchain Service track followed closely with a total financing of US$602 million, showing the markets continued attention to projects that provide infrastructure and tools for the Web3 ecosystem. This may include development platforms, security solutions, data analysis services, etc. These services are crucial to the healthy development of the entire ecosystem.

• DeFi and Social tracks attracted $215 million and $169 million in financing respectively. Although not as large as CeFi, they still maintained a certain level of activity, especially in the strategic MEV platform and social payment innovation direction. Although the overall financing of blockchain infrastructure ($125 million) has decreased compared with the previous period, projects such as LayerZero still rely on technological innovation to gain favor from leading institutions and maintain a high degree of trust.

• Chain projects and GameFi only received US$91.2 million and US$19.5 million respectively, which is at the low end of this month’s financing. This shows that in the current cycle, public chain and chain game innovation have not yet become the focus of capital, and funds are flowing more to sectors with “greater certainty”.

According to the financing scale data of 66 Web3 projects disclosed in April 2025, the financing scale of that month showed the structural characteristics of middle-sized projects dominated + top-tier projects accounted for a large amount + small-amount projects were not popular. The overall distribution shows that the number of medium-sized projects is the largest, while the proportion of large-scale projects has increased significantly, while the proportion of small-amount financing projects is relatively low.

Among them, projects with financing scales between US$3 million and US$10 million accounted for as high as 30.3%, which is the most important financing range. This shows that a large number of projects that have completed technical verification or initial implementation are receiving positive responses from the capital market for their growth potential.

In addition, the number of projects with financing scale exceeding US$10 million accounted for 47% in total, of which projects with financing scale of US$10 million to US$20 million, US$20 million to US$50 million and above US$50 million accounted for 16.7%, 16.7% and 13.6% respectively. This data shows that compared with the previous stage dominated by small and medium-sized financing, the market has paid more attention to projects with mature business paths, clear profit models and medium- and long-term potential, and capital has begun to accelerate the concentration of mid- and low-end and head projects.

Relatively speaking, projects with financing scale below 1 million USD only account for 6.1%, which highlights that financing for small-scale projects is more difficult, investors’ risk appetite tends to be conservative, and they have stricter requirements on project fundamentals.

Overall, the financing data in April 2025 reflects that the Web3 financing ecosystem has shifted from cast-net support to structured bets, and capital resources are accelerating toward projects with clear development paths and strong integration capabilities.

From the data on the number of financing rounds and the proportion of financing amounts, it can be seen that the current market presents the structural characteristics of the number of early-round projects dominates, and funds are concentrated in the middle and late rounds; the capital market is gradually converging on a few middle and late-stage projects with scale potential and technical realization capabilities, and at the same time, the screening of early-stage projects is more stringent, and the investment style tends to be rational and concentrated.

In terms of the proportion of financing rounds, the seed round accounts for the highest proportion, reaching 41.4%, indicating that the Web3 industry is still in an active early entrepreneurial stage with a sufficient number of projects. The second is the strategic round and the A round projects, accounting for 24.1% and 15.5% respectively, while the Pre-Seed round accounts for only 8.6%. The proportion of B round and C round projects is relatively small, accounting for only 6.9% and 3.4%, indicating that the number of projects entering the mid-to-late stage is still limited.

However, from the perspective of the proportion of financing amount, the funds are obviously tilted towards mid- and late-stage projects: although there are fewer projects in the C round, they have the strongest ability to attract funds, with a total financing amount of US$205 million, accounting for 23.7% of the total financing amount; the financing amounts of the A and B rounds are US$177 million and US$159 million respectively, accounting for more than 18%. In contrast, although the number of seed round projects is the largest, it only accounts for 18.3% of the total financing amount, and Pre-Seed accounts for only 1.3%.

This phenomenon of light on projects and heavy on funds concentrated in the middle and late stages reflects that investors currently prefer more stable projects with commercialization capabilities and growth verification, and their risk tolerance for start-up projects is relatively low. The strategic round of financing accounted for 17.8%, which also shows that some mature companies or projects are strengthening their ecological layout or integrating resources through targeted financing.

According to Cryptorank data on May 7, 2025, Coinbase Ventures topped the list with 10 investments, significantly ahead of other institutions, demonstrating its strong participation and resource integration capabilities in the current cycle. Following closely behind are 1kx, a16z CSX and MH Ventures, with investments ranging from 5 to 6, reflecting that while they maintain a high frequency of investment, they also demonstrate their own clear strategic directions.

Judging from the distribution of investment tracks of various institutions, there are certain differences in investment preferences. For example, Coinbase Ventures has a lot of layouts in the fields of DeFi, Blockchain Infrastructure and CeFi; 1kx is more inclined to DeFi and Blockchain Infrastructure; and a16z CSX is active in the direction of DeFi and Blockchain Service.

Financing projects highlighted in April

ZAR

Introduction: ZAR is a digital dollar wallet that aims to empower local merchants around the world to become exchange points for cash and digital dollars. Through the ZAR application, users can easily exchange cash for digital currency and use virtual and physical debit cards to trade globally. The product was founded by Brandon Timinsky and Sebastian Scholl in 2024 and is committed to empowering corner stores around the world to participate in cash and stablecoin exchange transactions, promoting the popularization and application of stablecoins in the real economy. [3]

On April 30, ZAR announced that it had completed a $7 million financing round, led by Dragonfly Capital and VanEck Ventures. [4]

Investment institutions/angel investors: Dragonfly Capital, a16z CSX, VanEck Ventures, Coinbase Ventures, Solana Ventures and Balaji Srinivasan Angel Investors, etc.

Highlights:

1. The platform has not yet been officially launched, but it has attracted about 100,000 users to queue up for registration. More than 7,000 merchants from 20 countries including Pakistan, Indonesia, and Nigeria have expressed their willingness to cooperate. It is expected to be officially launched in the summer of 2025.

2. Launch the stablecoin ZAR anchored to the South African rand, focusing on regions with unstable currencies and weak banking infrastructure such as sub-Saharan Africa, reducing exchange rate fluctuations and payment costs, and improving financial access efficiency. The ZAR wallet supports USDC and USDT, providing a stable payment channel based on the US dollar peg, enhancing user trust and asset stability.

3. Users can make payments globally through ZARs virtual or physical debit cards, supporting Apple Pay and Google Pay, avoiding the extra fees incurred by traditional international transactions. At the same time, users can also realize two-way exchange of cash and stablecoins at cooperative merchants, simplifying the process of obtaining and using digital assets, and promoting the deep integration of local economy and digital finance.

Pencil Finance

Introduction: Pencil Finance is a decentralized lending protocol dedicated to bringing real-world student loan financing to the chain. It connects investors with verified student loan originators, turning student debt into a transparent, investable asset class. [5]

On April 30, Pencil Finance announced the completion of a $10 million liquidity pool financing. The funds have been deployed in Pencil Finances liquidity pool on the Open Campus EDU Chain to support its first batch of on-chain education loans and education company debt financing business. [6]

Investors: Animoca Brands, Open Campus, etc.

Highlights:

1. Put education loans on the blockchain to create a new track for EduFi. Pencil Finance cooperates with traditional education loan companies to introduce education loans in Southeast Asia and the United States to the blockchain, expanding new asset categories that investors on the chain can configure. Through on-chain deployment and transparent management, it improves capital efficiency and lowers the financing threshold.

2. Risk-weighted structure design to match different risk preferences. Pencil Finance launched a student loan risk-weighted protocol, allowing whitelisted users to provide liquidity for the loan pool and freely choose to invest in priority (low risk and low return) or secondary levels (high risk and high return). At the same time, the platform undertakes loan deployment and repayment management to ensure transparent processes and traceability of revenue chains.

CAP

Introduction: CAP is a stablecoin engine that aims to break the closed-loop dependence of the intrinsic incentive model and provide users with a truly sustainable income path.

It supports the issuance of convertible stablecoins anchored to assets such as USD, BTC and ETH, and through the integration of arbitrage, MEV and RWA income, it popularizes complex strategies that have traditionally only belonged to a few high-level players. [7]

On April 7, Cap announced that it had completed a $11 million financing round, with investors including Franklin Templeton and Triton Capital. The funds will be mainly used to develop its stablecoin engine, which is scheduled to be officially launched later this year. [8]

Investment institutions: Franklin Templeton, Triton Capital, GSR, etc.

Highlights:

1. CAP is a new stablecoin protocol built on MegaETH, dedicated to creating a sustainable stablecoin system driven by real income without relying on inflation incentives. CAP does not rely on traditional DeFi incentives such as token issuance, but is supported by external income such as market making, MEV, arbitrage and RWA (such as corporate bonds), avoiding the flywheel risk of incentive exhaustion → liquidity exhaustion and has stronger scalability and anti-cyclical capabilities.

2. Users can get a foolproof income experience through CAP without complex financial knowledge or connections. Its stablecoin cUSD is backed by USDC/USDT at a 1:1 ratio, which means it is fully collateralized and always redeemable. Unlike other income stablecoins that rely on DeFi liquidity incentives, CAP transfers risks to re-stakeholders (people who pledge ETH through EigenLayer to protect the protocol).

3. CAP builds decentralized infrastructure, integrates RWA income paths such as on-chain arbitrage, MEV and traditional bonds, and forms a synergistic drive. In addition to cUSD, CAP will also launch stablecoins anchored to BTC and ETH to meet the income needs of users with different risk preferences and expand the entry of multiple assets.

Camp Network

Introduction: Camp Network is an innovative Layer-1 blockchain focused on independent intellectual property (IP), designed to provide a verifiable operating environment for the next generation of AI agents with user identities. It aggregates Web2 data and connects traditional platforms with blockchains, enabling users to monetize their digital footprints while maintaining control, thereby solving the problem of AI training data ownership and creator revenue. [9]

On April 29, Camp Network announced the completion of a $25 million Series A financing round, led by 1kx and Blockchain Capital, with participation from OKX, Lattice, Paper Ventures and other institutions, with a maximum valuation of $400 million. [10]

Investment institutions/angel investors: 1kx, Blockchain Capital, OKX, Lattice, Paper Ventures, etc.

Highlights:

1. The core design of Camp Network emphasizes two major capabilities: one is the ability to integrate off-chain data, which can connect to the Web2 platform through API, and upload users social, behavioral and other data to the chain after verification to ensure authenticity and availability; the other is developer-friendliness, which helps developers quickly build DApps based on user data by providing standardized toolkits, such as fan tokens, social derivatives protocols, etc., thereby lowering the threshold for building Web3 applications.

2. Camp Network emphasizes fully decentralized data storage and identity authentication mechanisms, effectively avoiding data monopoly and privacy risks of traditional platforms. At the same time, its integrated LayerZero provides strong cross-chain compatibility, allowing developers to easily deploy multi-chain interoperable applications. In addition, the platform has strong social data aggregation capabilities, which can collect user portraits from Web2 platforms, provide smarter personalized services for Web3 applications, and improve user retention and interaction quality.

3. Camp Network has reached cooperation with leading platforms such as Figma, CoinList, and WalletConnect, and established an ecological fund to support developers and creators. Recently, it has also joined hands with Movement Labs to jointly promote the application of social data in Web3 and accelerate the expansion of the ecosystem.

Blackbird Labs

Introduction: Blackbird is a Web3 loyalty and payment company that connects restaurants and customers, providing a fully customizable loyalty program platform and consumer app. The Blackbird app serves as a digital wallet for users to manage memberships, view $FLY balances, track activities, and interact with restaurants. [11]

On April 8, Blackbird Labs announced the completion of a $50 million Series B funding round led by Spark Capital; the funds will be used for equity and token warrants for an unreleased cryptocurrency. [12]

Investment institutions: Spark Capital, Coinbase, a16z crypto, Union Square Ventures, Amex Ventures, etc.

Highlights:

1. Blackbirds core goal is to eliminate unnecessary intermediaries in the restaurant industry, such as payment processors, through its blockchain platform Flynet, which extract an average of 3% to 5% of restaurant revenue without providing corresponding value. Flynet aims to establish a direct connection between restaurants and customers, significantly reduce costs and optimize the dining experience. For example, compared with traditional credit card fees of more than 3.75%, Flynet only uses a fixed rate of 2%, and immediately returns 1.5% to restaurants for customer acquisition and retention, thereby significantly reducing costs.

2. Flynet has built a universal tokenized points system across restaurants, supporting personalized rewards programs based on on-chain behaviors. Restaurants can design exclusive experiences for users, including hidden menus and celebrity chef interactions, to encourage high-frequency consumption and brand loyalty. When users participate in restaurant consumption, they will receive the platform token FLY as a reward, which can be used to deduct meal expenses at any restaurant in the Flynet network. Currently, the network covers more than 600 high-quality restaurants in New York City, San Francisco, and Charleston, South Carolina, forming a tradable Web3 catering loyalty ecosystem.

3. Blackbird also announced the launch of Blackbird Club, a tiered loyalty program designed to reward loyal users with surprises and exclusive experiences, replacing the traditional points redemption model. Members will enjoy exclusive benefits such as reservation guarantees, priority pre-sales for exclusive events, hidden menu tastings, and special sessions for friends and family.

summary

In April 2025, the Web3 industry completed 94 financings with a total amount of US$2.37 billion. Both the scale and number of financings declined, and the market cooled down significantly. However, the direction and preference of capital have changed significantly, showing a trend of concentrating on more mature, more integrated and compliant fields such as CeFi and blockchain services. Traditional financing methods such as mergers and acquisitions and structured financing have regained their dominance, and large amounts of funds have flowed more to mid- and late-stage and head projects, reflecting investors emphasis on project commercialization capabilities and steady growth. Although early innovation is still happening, capital is more stringent in screening start-up projects, and risk appetite tends to be conservative. Head institutions represented by Coinbase Ventures are still active and actively deploying in key tracks. It is worth noting that star projects such as ZAR, Pencil Finance, CAP, Camp Network, Blackbird, etc. have demonstrated innovative potential in the sub-sectors of stablecoins, education finance, stablecoin income aggregation, IP infrastructure, and encrypted catering applications, and have received support from traditional financial institutions and well-known Web3 funds, indicating that the Web3 ecosystem is still constantly exploring new growth points and application scenarios.

References:

1. Cryptorank, https://cryptorank.io/funding-analytics

2.Cryptorank, https://cryptorank.io/funding-rounds

3. ZAR, https://www.zar.app/

4.X, https://x.com/zardotapp/status/1917569020318097627

5.Pencil Finance, http://pencilfinance.io/

6.Animoca Brands, https://www.animocabrands.com/pencil-finance-announces-usd10m-for-student-loan-financing-backed-by-animoca-brands-open-campus

7.CAP, https://caplabs.io/

8.Coindesk, https://www.coindesk.com/tech/2025/04/06/cap-raises-usd11m-to-fuel-stablecoin-engine-as-industry-heats-up

9.Camp Network, https://www.campnetwork.xyz/

10.Fortune, https://fortune.com/crypto/2025/04/29/camp-network-30-million-ai-blockchain-1kx-blockchain-capital/

11. Blackbird Labs, https://www.blackbird.xyz/

12. Fortune, https://fortune.com/crypto/2025/04/08/blackbird-funding-ben-leventhal-restaurants/

Gate Research Institute is a comprehensive blockchain and cryptocurrency research platform that provides readers with in-depth content, including technical analysis, hot spot insights, market reviews, industry research, trend forecasts, and macroeconomic policy analysis.

Disclaimer

Investing in the cryptocurrency market involves high risks. Users are advised to conduct independent research and fully understand the nature of the assets and products purchased before making any investment decisions. Gate.io is not responsible for any losses or damages resulting from such investment decisions.