Original author: TVBee (X: @bloc kTVBee )

DePin is a relatively abstract project, not as intuitive as public chains, Defi, and MEME. However, DePin may be an application with a broader scenario...

DePin track and data that cannot be ignored

DePin is unique in two aspects:

The first is DePin’s business areas and service objects.

DePin is developing in the fields of cloud computing, cloud rendering, file storage, network hotspots and even meteorology, and its services are not limited to the Web3 field.

For example, Aethir, as a decentralized cloud computing platform in the fields of AI training and reasoning, and game computing, has provided a large number of cloud computing services for Web2 enterprises. GEODNET, a geographic and meteorological data information platform based on GNSS satellite reference stations, is committed to providing services for agriculture, engineering, transportation, geology, etc.

Second, DePin data is difficult to obtain. Although the working principles of public chains are not exactly the same, there are many similarities. Defi products and MEME data are even more homogeneous, and these data are relatively easy to obtain. However, the gap between DePin projects is large, and their main work may not be performed on the blockchain, so the data of this track is often overlooked.

Defillama is a very powerful data platform, but it mainly focuses on DeFi projects. @tokenterminal is a comprehensive data platform that focuses on a wider range of projects and data.

Recently, @AethirCloud has established in-depth cooperation with Token Terminal.

How deep is the cooperation? The two parties have established a tag registry for the #Aethir smart contract on the chain. This is a data tool dedicated to Token Terminal, which is used to identify various behaviors and data of Aethir applications on the chain. On this basis, Aethirs on-chain data can be standardized and calculated.

On this basis, Aethir is included in the infrastructure category and has a certain degree of comparability with other similar projects. On this basis, several major DePin projects are compared below.

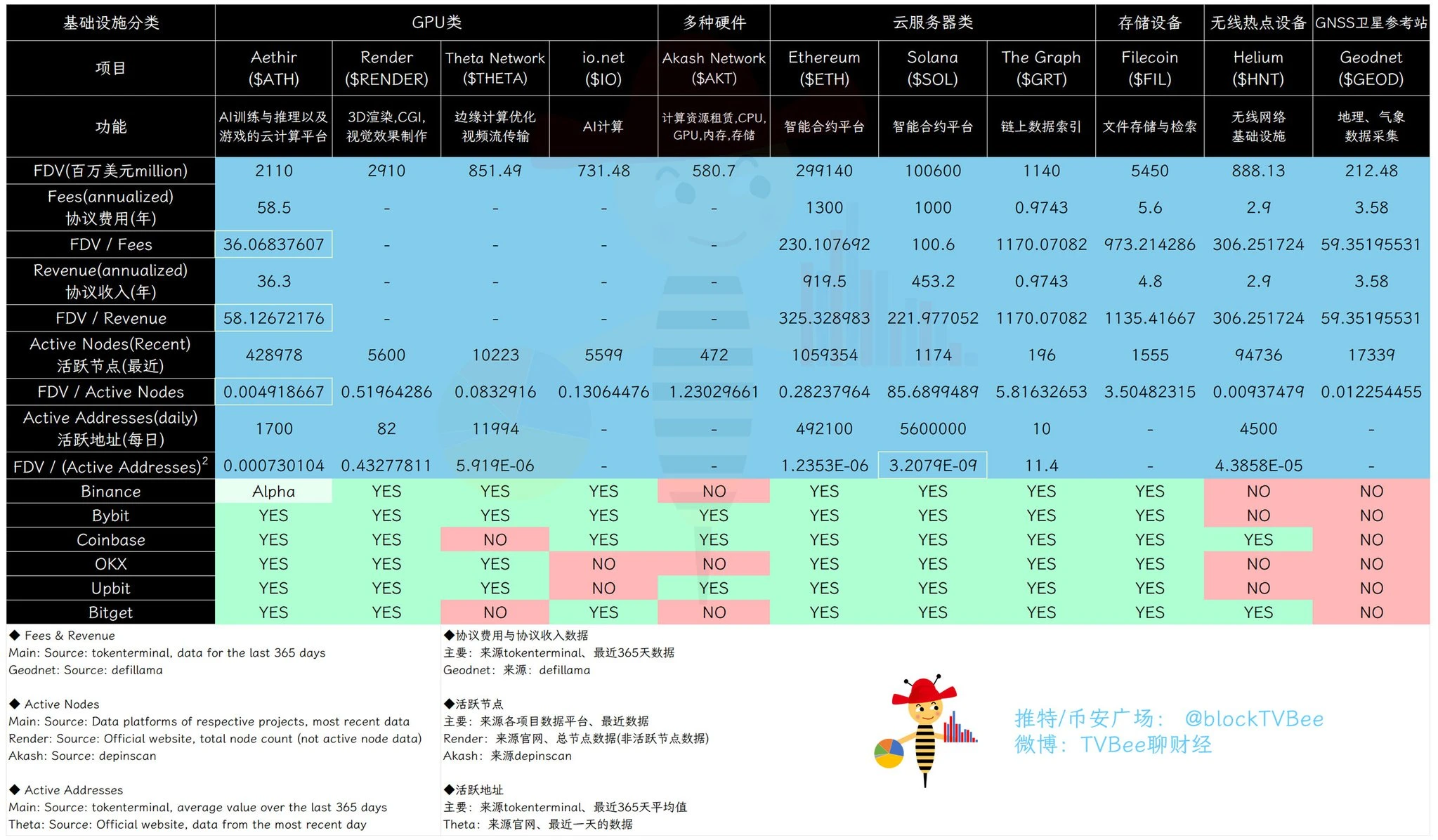

DePin Data Comparison

Demand side

The two indicators of protocol fees and protocol revenue are used to measure the demand for the DePin project.

Agreement Fees

The protocol fee is calculated as the sum of fees paid by all users over a period of time, which can reflect the ability of the DePin project to create economic value.

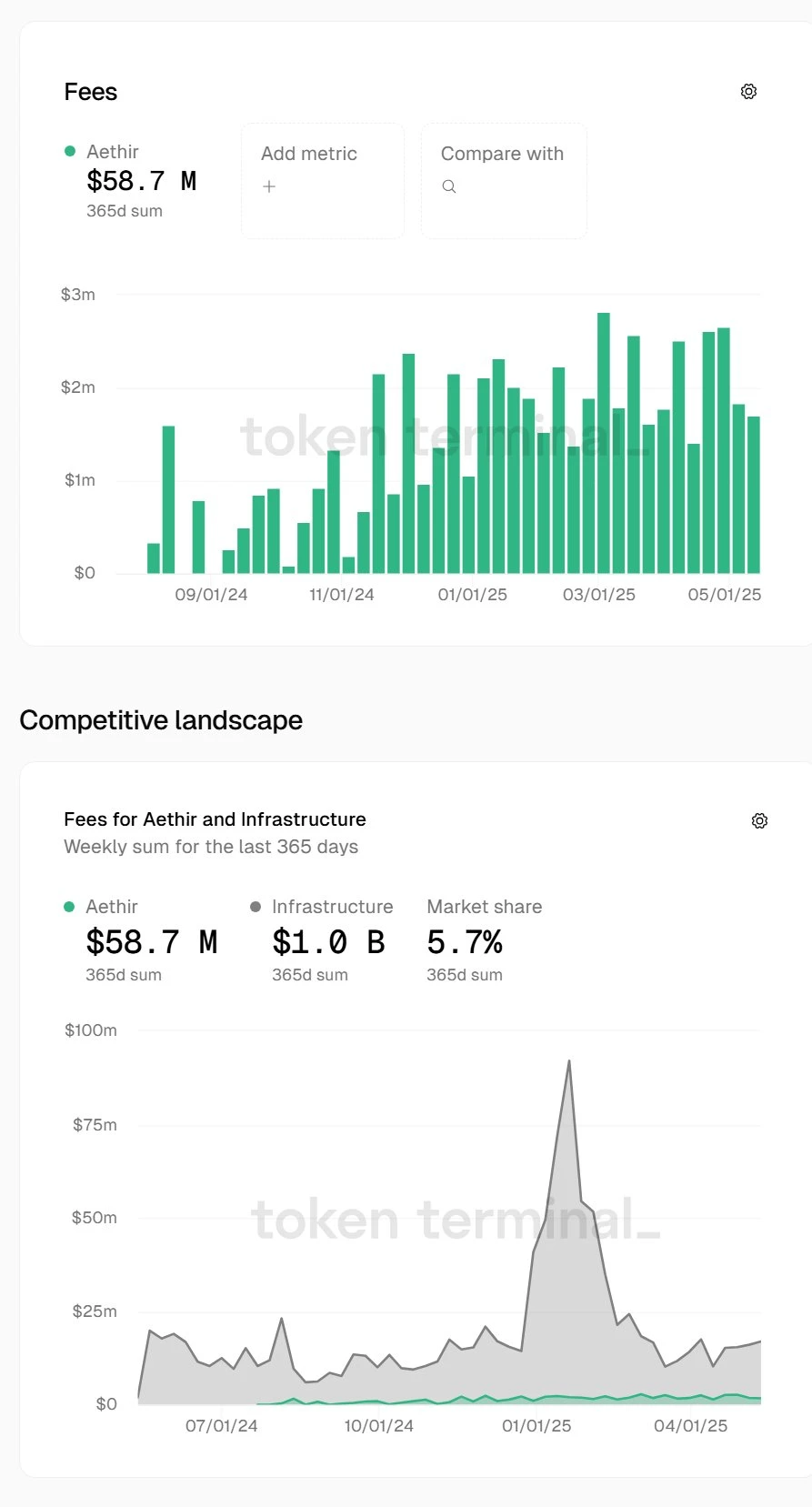

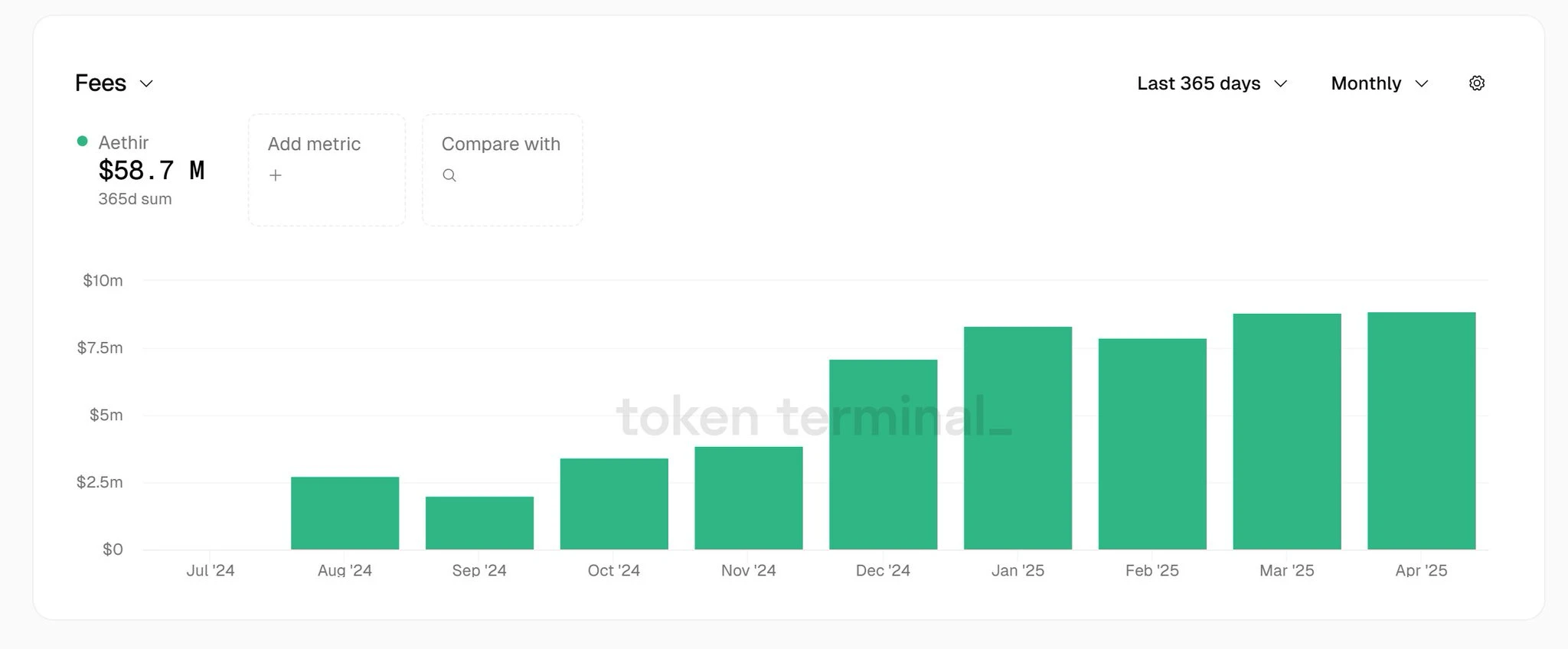

For example, in the past year, Aethir has generated a total of $58.7 million in protocol fees, accounting for 5.7% of the market share in the infrastructure market as counted by Token Terminal.

Aethirs protocol fees have a major feature, which is that they are generally on the rise and have no correlation with the bull and bear markets of Web3. March and April were the months when the cryptocurrency market fell significantly, but Aethirs protocol fees did not fall at all in March and April.

This is because Aethir is an enterprise-level cloud computing platform, and its service objects and revenue sources are mainly game companies, AI companies, etc. in the Web2 field.

Agreement income

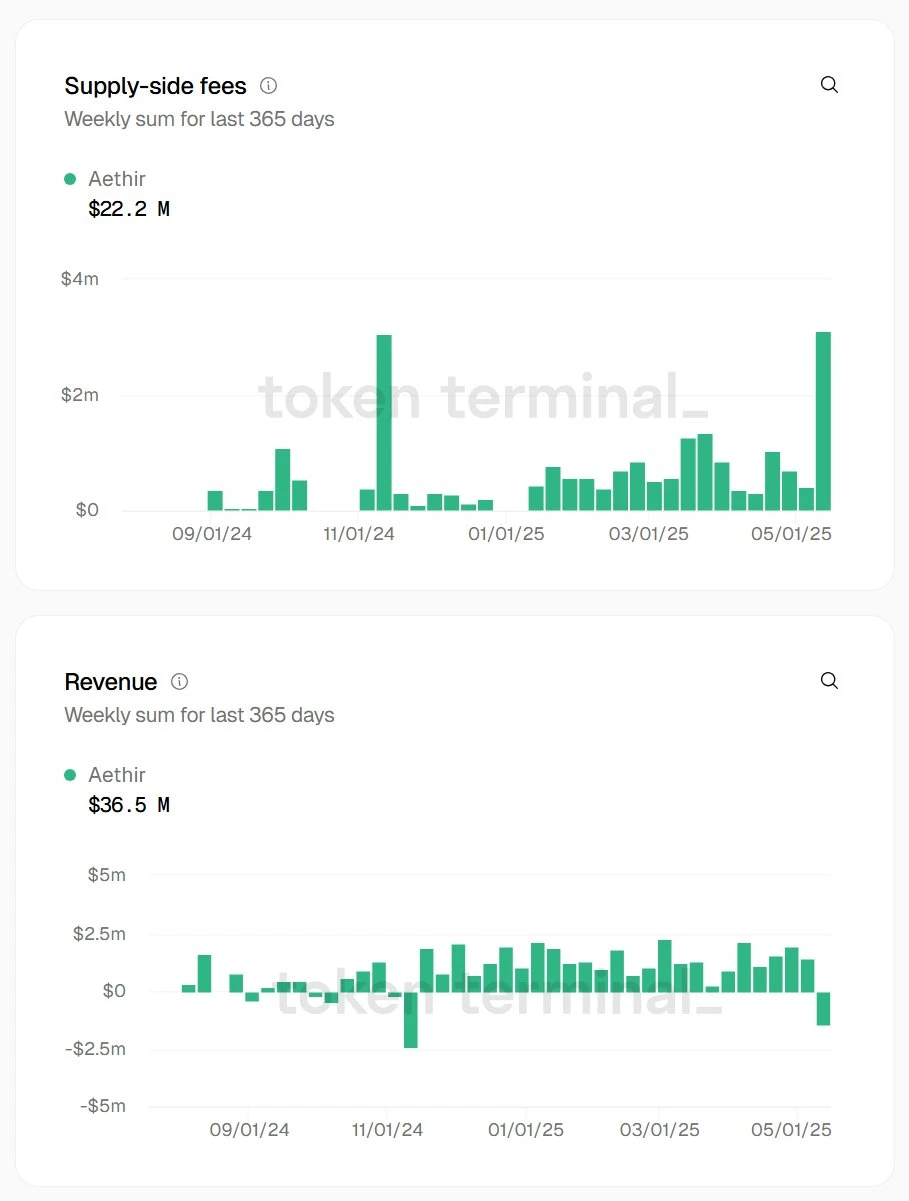

Protocol income is the retained portion after deducting dividends from protocol fees. It can reflect the net capital inflow of the DePin project and the income distribution system.

For example, in the past year, Aethir has distributed a total of $22.2 million in dividends, and retained agreement income is $36.5 million (5870-2220 = 3650).

The protocol fee and protocol income data in the table are mainly from Token Terminal, and Geodnet’s data is from Defillama.

Data comparison

In comparison, the protocol fees generated by public chains are the highest. Yes, as a decentralized accounting system or database, public chains are essentially a kind of DePin. However, as the main carrier of the Web3 ecosystem, public chains will not be labeled as DePin.

Apart from public chains, Aethir is the DePin project with the highest protocol fees and protocol revenue. The protocol fee of Filecoin, which was once very popular, is less than one-tenth of Aethir.

Value comparison

Use FDV to divide the agreement fees and agreement revenue respectively. This ratio is similar to the calculation logic of the price-to-earnings ratio and can be used to evaluate and compare the value of projects.

After comparison, it is found that Aethir has the lowest FDV/Fees and FDV/Revenue ratios, which means that Aethir may be the most underestimated relative to these items in the table.

Interestingly, it’s not because Aethir is not listed on Binance spot trading. Another project, $GEOD, is listed on even fewer exchanges, but both ratios for this project are also higher than Aethir.

Supply side

Active Nodes

DePin nodes refer to the physical infrastructure that actually provides services in the decentralized physical infrastructure network, including GPUs, CPUs, cloud servers, storage devices, wireless hotspots, etc.

The more active nodes there are, the stronger the service capabilities of the DePin network and the higher the total service cost.

Among them, the active node data mainly comes from the official websites of various projects, and the data of Akash comes from the depinscan platform developed by IOTX (DePin data platform, which can view the social data of each DePin, token market data and even the global distribution map of nodes and other information).

Data comparison

Because node costs vary greatly across different types of infrastructure, it is important to compare data on active nodes within a category.

In the GPU category, Aethir obviously has the largest number of nodes. In this category, Render ranks the highest in market value, but no data on active nodes can be found on its official website. Only the total number of nodes since the project was launched is found, which is 5,600, but this number is only 1.3% of Aethirs active nodes.

Among cloud service types, Ethereum has the highest number of nodes.

Value comparison

We still use FDV divided by the number of active nodes as the value/cost multiplier to measure the value of the DePin project.

Although different types of nodes have different costs, the cost of GPUs is likely to be higher than that of hardware such as cloud servers and storage devices. Therefore, Aethir has the lowest value/cost multiplier, which again shows that Aethir may be underestimated.

After Aethir, Helium’s multiplier is also very low, and it may also be underestimated from the supply-side dimension.

Ecological synthesis

Number of active addresses

According to the Metcalfe equation, the value of a network is proportional to the square of the number of active users. Therefore, the number of active addresses on the chain is used as an indicator for comprehensive comparison of the ecosystem.

The number of active addresses in the table mainly comes from Token Terminal, which calculates the average daily number of active addresses in the past year. The Theta data comes from its official website, which should be the data for the past day.

Data comparison

There is no doubt that Solana has the most active addresses, followed by Ethereum. Of course, DePin networks with different purposes are not comparable.

Among the GPU computing DePin projects, Theta has the highest active address, but its data comes from the official website and is not an annual average, so it may not be comparable with the data of other similar projects. Under the premise of comparability, Aethir is the GPU computing DePin with the highest active address.

Value comparison

Without considering data comparability, Theta may be an underestimated GPU computing DePin.

Under comparable conditions, Aethir is an underestimated GPU computing DePin.

Last words

Aethir is the first GPU computing DePin project to accept Token Terminas deep acquisition data. And according to the ratio of FDV to demand, supply, and the square of the number of active addresses, $ATH may be undervalued.

Unlike other projects, the revenue of DePin projects such as Aethir, which mainly serve areas other than Web3, is not related to the fluctuation of the cryptocurrency market. Aethirs revenue shows a stable growth trend.

On the other hand, DePin projects represented by Aethir earn revenue from non-Web3 fields, which is extremely rare. This means that the main revenue model of such projects is not in the secondary market, and may even attract money from outside the cryptocurrency circle...