Today (June 17, local time) American history has ushered in an important development - the U.S. Senate passed the GENIUS Act . The bill will establish a clear federal regulatory framework for dollar-backed cryptocurrencies (i.e. stablecoins). Next, the bill will be submitted to the House of Representatives and President Trump for approval. If it is successfully passed, it will officially take effect.

Key Provisions of the GENIUS Act

The core content of the bill is to establish a federal framework for the issuance of dollar-backed stablecoins. Its main provisions include:

1:1 asset backing: Each stablecoin must be fully backed by high-quality, liquid reserve assets, such as US dollar cash, insured bank deposits, short-term US Treasury bonds or other safe assets. Issuers must hold at least one US dollar in compliant reserves for each stablecoin. For issuers with a circulation of more than US$50 billion, monthly reserve disclosure and audits are required.

Tiered supervision of large and small issuers: The GENIUS Act adopts a tiered supervision strategy based on the size of the issuer. Large issuers that issue more than $10 billion in stablecoins will be subject to federal supervision; small issuers can choose to be supervised by state regulators.

Ban on algorithmic stablecoins: The bill explicitly bans so-called “algorithmic stablecoins” — tokens that rely on programs or internal crypto assets to maintain their value rather than physical collateral.

No income shall be provided: Payment stablecoins shall not pay interest, dividends or any form of income to holders. If income is provided, it may blur the line between stablecoins and savings financial products, thus raising concerns about regulation and financial stability.

Not securities or commodities: The bill amends the existing securities law to clarify that compliant payment stablecoins do not fall into the category of securities or commodities. This provision resolves the uncertainty in the regulatory community about the classification of stablecoins. Stablecoin issuers will be subject to supervision by the Office of the Comptroller of the Currency (OCC), the Federal Reserve, the FDIC, the NCUA, and state regulators.

Bankruptcy protection: In the event of bankruptcy, the claims of stablecoin holders take precedence over other creditors.

Why is this important?

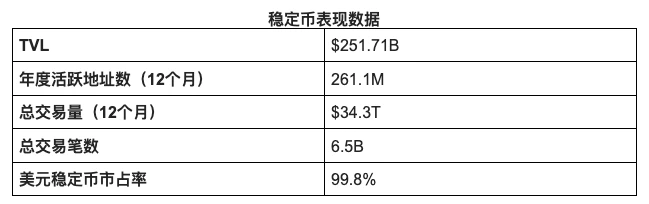

Stablecoins are no longer simply crypto-native assets, but increasingly critical infrastructure in global financial activities. The total market value of stablecoins has exceeded $250 billion, mainly dominated by Tether and Circle. Circle recently listed on the New York Stock Exchange with a market value of $37 billion. Its stock price has risen by more than 400% since its listing, showing the markets high expectations for the mainstreaming of stablecoins and highlighting the positive role of clear regulation on issuers such as Circle.

Stablecoins are deeply embedded in the global payment ecosystem, with annual transaction volume exceeding $30 trillion and the number of active addresses reaching 261 million.

Data sources: rwa.xyz, DeFi Llama, Visa On-Chain Analytics

A recent Coinbase survey showed that 81% of small and medium-sized businesses (SMBs) that are aware of cryptocurrencies are interested in using stablecoins. The number of Fortune 500 companies that plan to adopt or explore stablecoins has more than tripled by 2024.

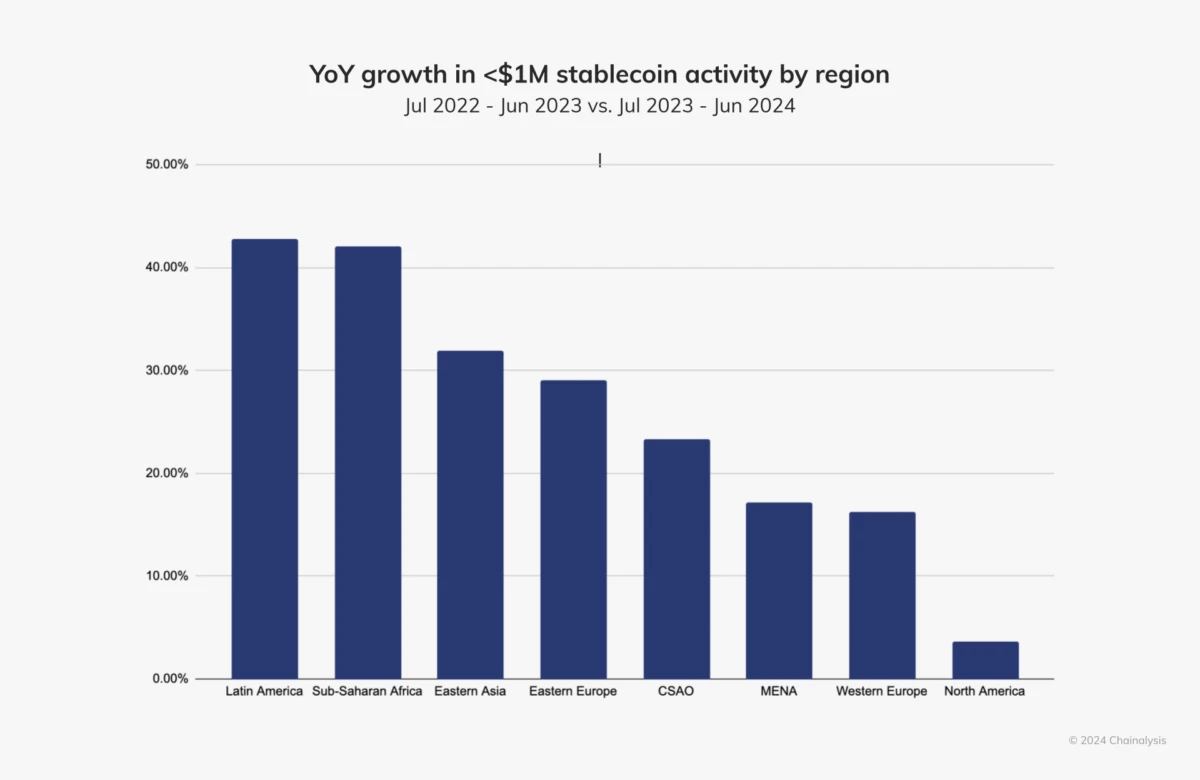

In emerging markets, stablecoin adoption is also accelerating. In regions with high currency volatility, stablecoins provide an alternative. According to Chainalysis 2024 Stablecoin Report, Latin America and Sub-Saharan Africa lead the world in retail and professional stablecoin transfers, with annual growth rates exceeding 40%; East Asia and Eastern Europe follow closely behind, with growth rates of 32% and 29%, respectively.

Source: Chainalysis

The EU (through MiCA), Singapore (Payment Services Act) and Hong Kong (Stablecoin Act) have all made clear progress in regulating stablecoins, while the United States has been constrained by political differences and has been slow to come up with clear policies.

But the passage of the GENIUS Act in the Senate may break the deadlock.

Impact on investors, startups and the industry ecosystem

Regulated stablecoins: US stablecoin issuers such as Circle and Paxos will benefit from regulatory legitimacy, opening the door for institutional funds to flow into the on-chain payment field in compliance. The bill requires that stablecoins must be backed by cash or US bonds, which will also consolidate the position of these mainstream compliant issuers, while unregulated stablecoin issuers that provide illegal currency support or promise returns may exit the US market. However, the requirement of no return may also force Circle to change its marketing strategy. Currently, Circle will share revenue with Coinbase as an important distribution channel for USDC.

Offshore stablecoins: The era of regulatory arbitrage for offshore stablecoins is coming to an end. The GENIUS Act imposes heavy penalties on unregulated offshore issuers. As the largest stablecoin by market value, Tether (USDT) may face major challenges in the future if it is not registered with the U.S. Office of the Comptroller of the Currency, similar to the situation it encountered in Europe. However, USDTs moat is still solid and it is difficult to be replaced in the short term. Moreover, Tether may re-enter the U.S. market by issuing new compliant U.S. dollar stablecoins .

Fintech companies: This bill also marks that US crypto legislation is gradually moving away from the stage of relying solely on law enforcement and toward structured policy making. Stablecoins are moving towards becoming legal financial carriers, which will not only promote adoption by retail users, but also drive more capital inflows. Take Stripe as an example. It has accelerated its layout in the stablecoin field through mergers and acquisitions: it acquired payment infrastructure platform Bridge for US$1.1 billion in February, and recently acquired wallet service provider Privy. Although technology giants like Meta are not prohibited from issuing stablecoins, they will face strict compliance requirements and special attention . This uncertainty may actually benefit the development space of start-ups.

Whats next?

House Deliberation and Potential Amendments: While Senate passage is critical, it is only one step in its legislative process. The focus now shifts to the U.S. House of Representatives. Currently, the momentum for stablecoins is strong, but we should pay attention to possible amendments proposed by the House of Representatives. Any changes could affect the future stablecoin landscape.

Regulatory details and implementation: Although the GENIUS Act establishes a general framework for the issuance of stablecoins, specific rules such as capital adequacy, liquidity, and risk management still need to be further formulated by regulators. We need to observe how regulators such as the Federal Reserve, the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC), and the Financial Crimes Enforcement Network (FinCEN) translate this framework into specific rules. What actions the states will take under this regulation is also another thing worth paying attention to.

References: