Every asset - every stock, bond, and fund - can be tokenized, which will bring about an investment revolution. This is a sentence from Larry Fink, Chairman and CEO of BlackRock. Larry Finks vision that everything can be tokenized not only depicts a technical possibility, but also foreshadows a profound change in the financial field. The time, place and occasion when Larry Fink said this is more important than the sentence itself. This sentence appeared in BlackRocks annual letter to all investors on March 31 this year. However, in BlackRocks annual letter last year, stablecoins, RWA, tokenization, digital assets, these most popular words in the market this year, were not mentioned at all. The only thing related to digital assets was BTCs ETF. This years annual letter from BlackRock is shouting for the democratization of finance brought by tokenization.

Why do so many bigwigs, including Larry Fink, choose to discuss real-world assets (RWA) at this moment? Some people say that it is because the income on the DeFi chain is not good, so everyone is looking for income from the real world. Some people say that it is because RWA is the only hot spot now, and whoever touches it will rise, whether it is currency or stock. Others say that there was also a RWA craze in 2017-2018, and at that time it was called ICO, which was a trend. Some people also say, why analyze so much, if you don’t do RWA, you will almost be out of work!

We may still need to understand the ins and outs of this RWA trend so that we can make the right choice in the next 6-12 months, so that RWA can truly take off in Asia and gain a place in the subsequent global competition.

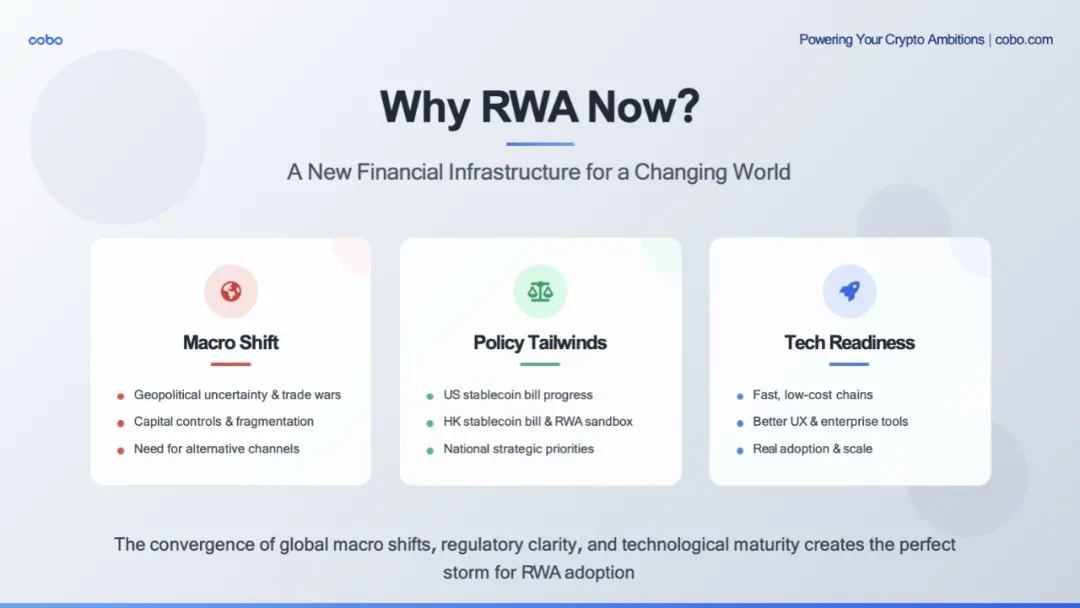

Today, the world is undergoing a major macro-evolution. For the first time in decades, we are living in a world full of geopolitical uncertainty, trade wars and capital controls, as well as a fragmented and even weaponized global financial system. The dollar remains strong, but countries are seeking to hedge their risks, and cross-border capital flows are being more strictly controlled.

Under such circumstances, it is natural for global capital to look for faster, cheaper, and more open channels for flow. At the same time, digital asset-related policies are also catching up. Both parties in the United States are promoting stablecoins and tokenization policy frameworks, and tokenization in Asia is no longer a niche experiment - digital assets have risen to a national strategy. Finally, the technical support level is also gradually maturing. In the past 12 to 18 months, we have seen tremendous progress: transaction fees on Tron, Solana, Base, and various Layer 2 chains are almost zero, the final confirmation time of stablecoin on-chain transactions has reached sub-seconds, and the user experience of digital wallets is rapidly improving - such as abstracting gas fees, one-click approval, and institutional-level banking experience custody services.

So, why does Larry Fink mention RWA now? It’s not because the hype cycle has arrived, but because the world needs it more than ever before - a way and vision to connect traditional finance to future finance in an efficient, compliant and global manner.

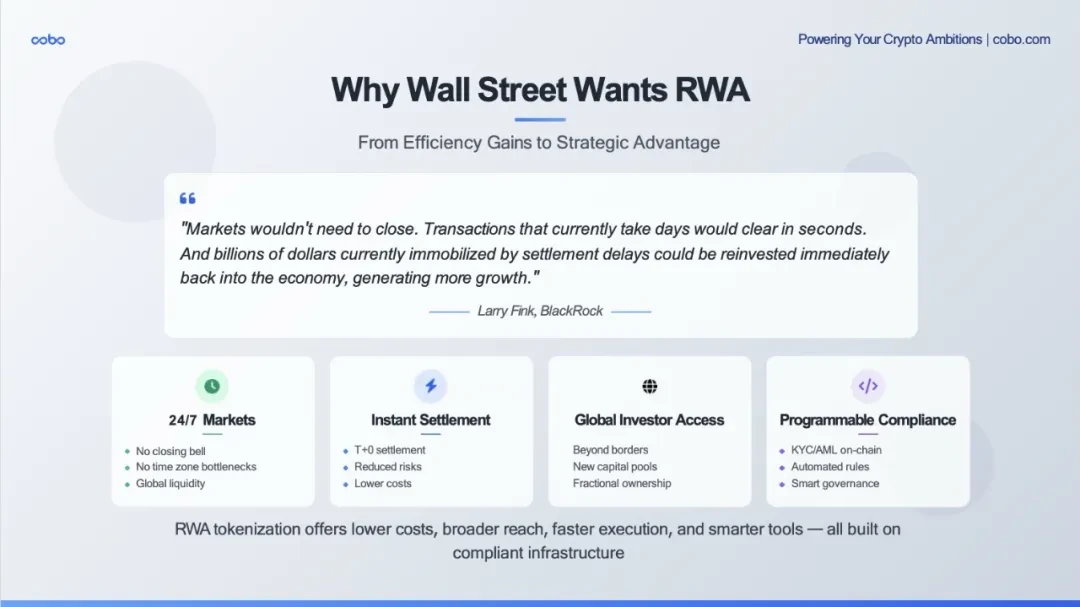

In Larry Finks view, Wall Street needs to reduce costs and increase efficiency. Simply put, real world assets (RWA) can make the market faster, more streamlined, and more global—without touching existing rules. Wall Street is not encrypting for the sake of encryption, but to improve the infrastructure of the existing capital market.

The first is the efficiency issue. The settlement cycle of traditional finance, such as bonds and private credit, is slow, expensive, and has cumbersome operational procedures. In contrast, RWA has achieved the following after being put on the chain:

Instant settlement - T+0, not T+2 or even longer.

24/7 liquidity - no trading hours and no time zone restrictions.

Built-in auditability - the ledger is real-time and publicly transparent.

Large institutions have seen the potential for cost reduction and efficiency improvement and have taken quick action. Large institutions including BlackRock and Franklin Templeton have launched large-scale tokenized treasury bonds on the blockchain, which can be settled on the chain and pay daily returns through smart contracts. These are no longer experiments - they are new financial infrastructures that are in operation.

The second is the issue of reach. Tokenized assets can reach investors that traditional channels cannot reach - especially emerging markets or non-traditional investor groups. For example:

Tokenized treasuries from Ondo, Matrixdock, and Plume are being purchased by DAOs, cryptocurrency vaults, and stablecoin holders in Asia, Latin America, and Africa—groups whose KYC is a strong credit asset that traditional brokers may never be able to touch with these stable returns.

Some real estate tokenization projects in the UAE and the US have enabled fragmented ownership and global distribution subject to compliance thresholds, which was simply not feasible before tokenization.

RWA not only reduces friction, it also expands the market.

Finally, there is programmability. This is where tokenized assets are fundamentally more powerful, as business logic can be embedded in the asset itself:

Comply with the prescribed transfer rules

Built-in revenue payment

Automatic rebalancing

Even embedded governance

Cantor Fitzgerald (whose CEO is the current U.S. Secretary of Commerce, and who has a deep relationship with Tether) recently partnered with Maple Finance to launch a $2 billion Bitcoin-collateralized credit facility—using smart contracts to automate some of the loan structure and risk monitoring. This heralds the beginning of a bigger change: financial products are not only digital, but also smart—they can be traded globally, built-in compliance when designed, and can be instantly integrated into any digital portfolio.

RWA is in full swing, and specific market figures can tell us whether RWA is still a fringe experiment or has become mainstream.

As of June 9, the total value of tokenized real-world assets (RWA) on public blockchains has reached nearly $23.4 billion. This is only the traceable part, and the on-chain asset products include U.S. Treasury bonds, corporate credit, real estate, various funds, and even commodities. $23.4 billion accounts for about 10% of the size of stablecoins and 0.7% of the entire Crypto market, ranking 10th or 11th in market value among all tokens.

Further analysis of the data leads to several observations:

The scale of private credit exceeds that of government bonds

Figures core products, which are the largest in scale, are worth $12 billion (home equity revolving credit, investor mortgages, cash-out refi). From the birth of the loan to the transfer between institutions, the Provenance blockchain (Cosmos) is used to move institutional-level home loans to the chain, and complete the transfer and settlement of ownership/income rights on the chain. Each loan will be minted into a digital eNote and registered in the digital asset registration system to replace the MERS registration and manual custody verification, obtain an on-chain identity, and can be sold, pledged or securitized immediately. 90-95% of Figures existing loans already exist in the form of on-chain eNotes. This process eliminates paper bills, MERS registration fees and manual custody verification, and can reduce friction costs by more than 100 basis points for each loan, shortening the time it takes for funds to arrive from weeks to days.

Securitize partners with Drift Protocol to bring Apollo’s $1 billion diversified credit fund on-chain.

To date, Maple Finance has issued over $2.5 billion in tokenized loans.

Centrifuge is powering real-world credit pools for DeFi protocols like Aave and Maker.

Tokenized Treasury Bonds Become a Trend

BlackRocks BUIDL Fund: with a total management scale of US$2.9 billion, it is currently in the lead.

Ondo’s scale is US$1.3 billion, and Franklin Templeton’s BENJI fund tokenization scale is approximately US$775 million.

Matrixdock and Superstate pushed the category to over $7 billion.

These are not crypto-native experiments, but rather mainstream financial institutions using blockchain as infrastructure to settle and distribute government bonds.

Commodity futures tokens are an earlier attempt than treasury bond tokenization and have certain first-mover advantages.

Fund-based RWAs, including real estate funds, are catching up strongly.

In the UAE, MAG Group (one of Dubai’s largest developers), MultiBank (the largest financial derivatives trader), and Mavryk (a blockchain technology company) announced a $3 billion partnership to put luxury properties on the blockchain.

Platforms such as RealT and Parcl in the US are letting retail investors buy fractional shares of income-generating properties – with the proceeds distributed directly to their wallets.

These asset tokens are yield-generating, tradable, legally enforceable assets that are particularly attractive in today’s market environment — they generate income, have low volatility, and are now within the reach of stablecoin holders, DAOs, and fintech treasurers.

Based on the above analysis, we believe that tokenized RWA is no longer just a concept - it is already a market: real assets, real issuers, real returns, and these numbers are growing at a compound rate.

Let’s take a look at some specific and real RWA project cases, especially RWA practices in Hong Kong and Asia: Five representative RWA projects, covering different stages and models from traditional banks to technology companies, from gold to new energy, and from pilot to formal operation.

1. HSBC Gold Token

This is a typical case of traditional banks entering the RWA field

Key Insight: HSBC chose a private blockchain to focus on retail customers and avoid the complex secondary market

Strategic Implications: Banks are more concerned with compliance and risk control than maximizing liquidity

Explanation: Traditional financial institutions may first choose a closed ecosystem when testing the waters

2. Longsun Group × Ant Digital Technology (new energy charging piles)

This represents China’s RWA exploration in the field of “new infrastructure”

The financing scale of RMB 100 million proves the recognition of institutions for the tokenization of physical assets

Key point: Still in the sandbox stage, indicating that supervision is proceeding cautiously

Investor composition: Domestic and foreign institutions + family offices, showing the interest of cross-border capital

3. GCL Energy Photovoltaic Power Station RWA

Larger scale: more than RMB 200 million, showing the attractiveness of green energy assets

ESG concept: Green power assets are in line with global ESG investment trends

Circulation design: Still in the design stage, indicating that the tokenization of complex assets requires more technical and legal innovations

4. UBS × OSL Tokenized Warrants

International bank pilot: UBS’s participation as a Swiss banking giant is of great significance

B2B model: Directed issuance to OSL, focusing on process verification rather than scale

Technical verification: The focus is on proving the technical feasibility of tokenized warrants

5. China Asset Management Hong Kong Digital Currency Fund

The most transparent case: On the Ethereum public chain, data is fully traceable

Retail-oriented: 800 address holders, truly targeting ordinary investors

Compliance balance: KYC requirements and on-chain transparency

From the above five projects, we can simply extract a few keywords: private chain, institutional and targeted retail, pilot non-scale. These projects cover different backgrounds in Hong Kong, mainland China and the world, showing a flourishing attitude. Specifically, Hong Kong is relatively open and supports innovation; mainland projects are cautiously promoted and sandbox pilots are carried out; internationally: major banks are actively testing the waters. The real challenge for the current projects is the liquidity challenge: most projects face insufficient liquidity in the secondary market, which is also the current bottleneck of RWA.

Compared with some projects in Hong Kong which are still in the experimental stage, let us look at the five leading RWA projects currently operating on a large scale in the global market. They represent the best practices in the current market.

1. BUIDL - BlackRocks flagship product

Leading in size: $2.9 billion, the largest among all tokenized treasury products

Institutional-oriented: only 75 holding addresses, but monthly trading volume is as high as $620 million

Key Insight: The average address holds nearly $40 million, demonstrating huge demand from institutional investors

Strategic significance: BlackRock chooses quality over quantity and focuses on serving large institutions

2. BENJI - Franklin Templetons retail experiment

Most interesting data: 577 addresses, but 30-day trading volume is only $20

Retail-oriented: This is a product that is truly for ordinary investors

Liquidity challenge: There is almost no secondary trading, which means that holders are more likely to buy and hold. It is also possible that the holders are not ordinary strangers, but the most familiar ordinary people.

Market Insight: Retail investors may care more about returns than liquidity

3. OUSG - Ondo Finance’s Institutional Products

Balanced Strategy: $690 million in value, 70 addresses, $14 million in trading volume

Institutional efficiency: Although not as large as BUIDL, the transaction activity is relatively high

Clear positioning: Focus on US qualified investors and avoid the complexity of retail regulation

4. USTB - Compliance-driven products

Medium: $640 million, 67 addresses

High trading activity: $63 million in 30-day trading volume shows good liquidity

Dual compliance: For US accredited qualified investors, with the strictest compliance requirements

5. USDY - A breakthrough in globalization

Biggest Find: 15,487 Addresses! This is a truly “popular” product

Global strategy: Serving non-US investors exclusively, avoiding the complexity of US regulation

Popular investment: Each address holds only about $40,000 on average, truly achieving inclusive finance

Through the analysis of international projects, we can draw several core insights and trends: Investor type determines product design. Institutional products are generally held by only a few large investors, with high unit prices and low frequency of transactions; retail products are mostly held by retail investors, with small unit prices and mainly held; and global products focus on avoiding regulatory complexity through regional differentiation.

Based on the current RWA projects in Hong Kong and the international market, we can draw several observations:

There is no one model that fits all markets: institutional and retail markets require completely different product designs;

Regulation is the biggest watershed: product performance for U.S. and non-U.S. investors differs greatly, and U.S. professional investors have a clear advantage in terms of liquidity;

Liquidity remains a challenge: even for the most successful products, secondary markets are not very active;

The key to scale: either go deep (large-scale institutional investment) or go broad (popular retail investment).

The above data and analysis reveal an important reality to us: successful RWA products need to find their own liquidity and unique product-market fit.

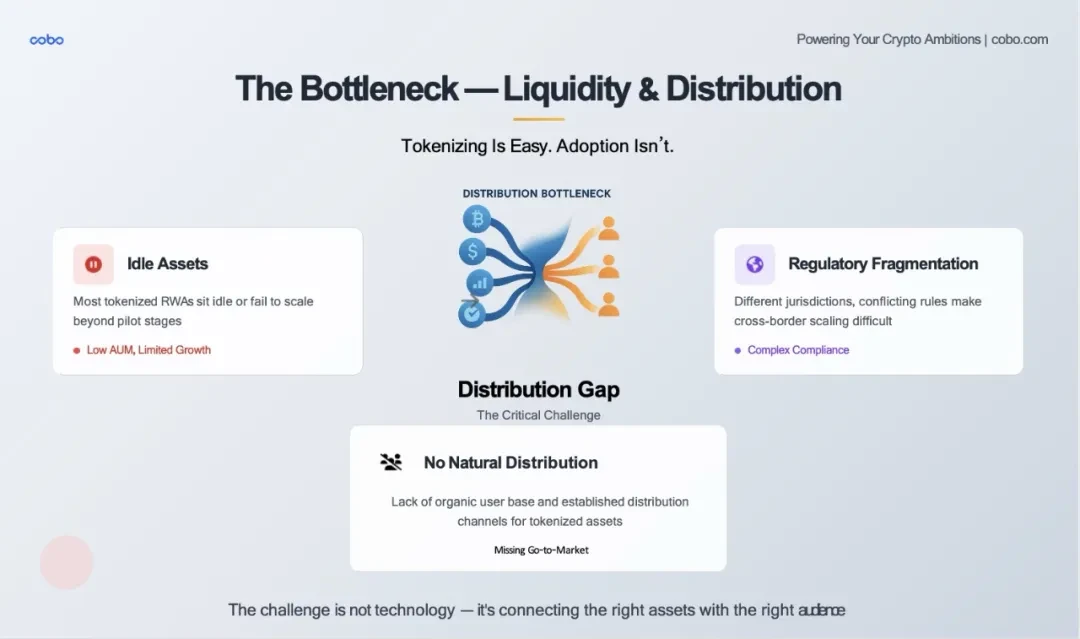

RWA tokenization is easy, but distribution is hard. Anyone can mint a token representing a piece of real estate or a U.S. Treasury bond. Getting these tokens to the right buyers at scale, compliantly, and consistently is the real challenge.

In addition to the top RWA projects we have seen before, there are actually dozens of tokenized treasury products on the chain, many of which offer considerable returns, but most of them have less than a few million dollars in assets under management (AUM). Why? Because they are not integrated into the DeFi protocol, not listed on regulated exchanges, and institutional buyers cannot easily obtain them without a customized docking process.

The value of a tokenized asset directly depends on how easy it is to exit. Currently, except for a few pools such as Maple or Centrifuge, the liquidity of the RWA secondary market is very weak. One of the reasons is that RWA does not have a bond market like NASDAQ or even a decent one. This also leads to opaque pricing, which limits institutional participation.

Finally, fragmented regulation of RWAs remains a major obstacle. Each jurisdiction has different views on whether tokens are securities, how they are managed, and who can hold them. This is slowing down the cross-border scale of RWAs, especially in Asia.

Therefore, we see that the quality of RWA assets is improving and the infrastructure is becoming increasingly powerful, but the last mile has not yet been opened: how to match tokenized assets with appropriate funds, establish liquidity, and make RWA truly play a role.

This is the challenge facing the RAW industry today, but also its biggest opportunity.

To solve this liquidity problem, the real breakthrough is not just better infrastructure, but the fit between product and market. This is not as simple as putting old traditional assets on the new blockchain track. The core question is: Who really needs this asset? If this asset becomes more accessible, what new markets can it serve? If US stocks are traded 24 x 7, and if more and more brokerages can buy and sell digital assets, will there still be demand for tokenized ETFs and US stock trading?

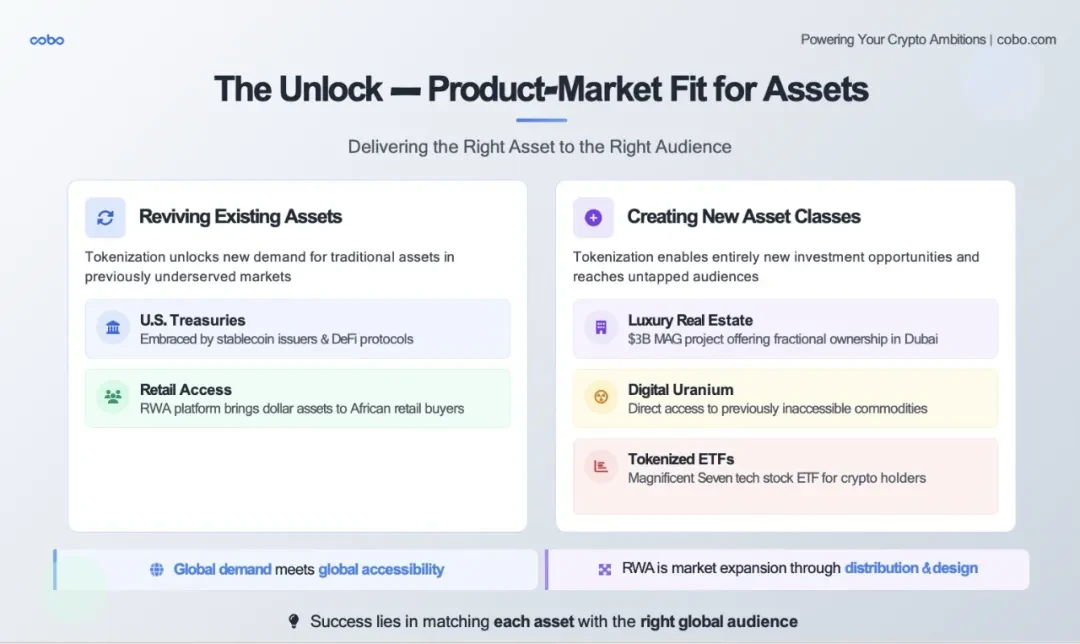

Tokenization can do two very powerful things: it can find new demand for existing assets that have stagnated in traditional markets, and it can create entirely new investable assets and deliver them in new ways to investors who have never been able to participate before.

Re-stimulating demand : RWA is now the hottest hot chicken U.S. Treasuries are actually such a case. In traditional financial markets, the U.S. Treasury market is becoming crowded and less attractive. However, in the crypto world and emerging markets, they have gained new opportunities: on-chain stablecoin issuers are using tokenized treasuries to obtain on-chain returns. Blockchain platforms designed specifically for RWA have sold U.S. Treasuries directly to retail investors in Africa, allowing these retail investors to obtain dollar-denominated, income-carrying assets that local banks have never provided. In this case, tokenization does more than digitize assets - it also matches assets to a global, underserved audience that craves security and returns.

Innovating new investable assets : When tokenization creates new assets, this is an even more exciting opportunity.

Case 1: Take luxury real estate in Dubai as an example. The growth of Dubai real estate in the past few years has impressed many overseas investors. But how many investors can really enter this market? First of all, do investors have to fly to Dubai? Secondly, you need a reliable real estate agent. But sorry, they don’t show up during the day. Traditionally, this market is closed - opaque, high threshold, and difficult for foreigners to enter. Now, through tokenization, projects like the $3 billion MAG are opening up fragmented ownership of high-end properties to global buyers - and are equipped with compliance, income and liquidity paths. Under this model, is it possible for the grand occasion of Shanghai people sweeping houses in Japan after the epidemic to be repeated in this project in Dubai? Here we see that the tokenization of new assets is not just financial inclusion - it is market expansion.

Case 2: Commodities like uranium. Most retail investors have never been exposed to uranium - it is too complex, too restrictive, and too niche. However, through the new tokenized tool Digital Uranium, investors can now directly invest in this critical resource that powers the global nuclear energy transition. A brand new asset - delivered to a brand new audience - becomes investable through tokenization.

Case 3: Stocks are also being restructured. When the crypto market is down, tokenized NASDAQ Magnificent Seven ETFs — like the Magnificent Seven — provide traders who are looking for real-world returns without having to exit cryptocurrencies. In other words, tokenization allows assets to follow funds, not the other way around.

Case 4: Private lending. Tightening spreads in traditional financial markets have put lenders on the sidelines. Platforms like Maple and Goldfinch are using tokenization to fund small and medium-sized enterprise (SME) loans in underserved areas, while allowing global DeFi users to earn returns from real-world cash flows.

So, the bigger picture of RWA should be this: tokenization is not just about packaging old financial instruments, it is about redefining what can be an asset - and putting it in the hands of those who value it most. This is what product-market fit looks like in the on-chain era: global demand meets global accessibility, new assets meet new liquidity, and match them well to find product-market fit.

These new audiences - including institutional investors, treasury departments of fintech companies, and crypto-native investors - actually straddle two fields. Some are in traditional finance, while others are native to DeFi. The only way for RWA to truly achieve large-scale development is to build a bridge between the two. It can be understood this way: traditional finance (TradFi) brings assets - including credibility, compliance, and scale; decentralized finance (DeFi) brings distribution - 24/7 access, smart contract automation, and global liquidity. The opportunity lies in how to connect the two securely, compliantly, and programmably.

This is not just talk, but is happening: Ondo Finance brings BlackRocks tokenized treasury bonds to the chain and connects them to the DeFi vault; Centrifuge converts off-chain credit into on-chain assets for use by protocols such as MakerDAO and Aave; Maple and Goldfinch enable institutional lenders to access global yield-seeking funds through DeFi channels. These examples all show what sparks can be created when traditional financial assets meet DeFi liquidity.

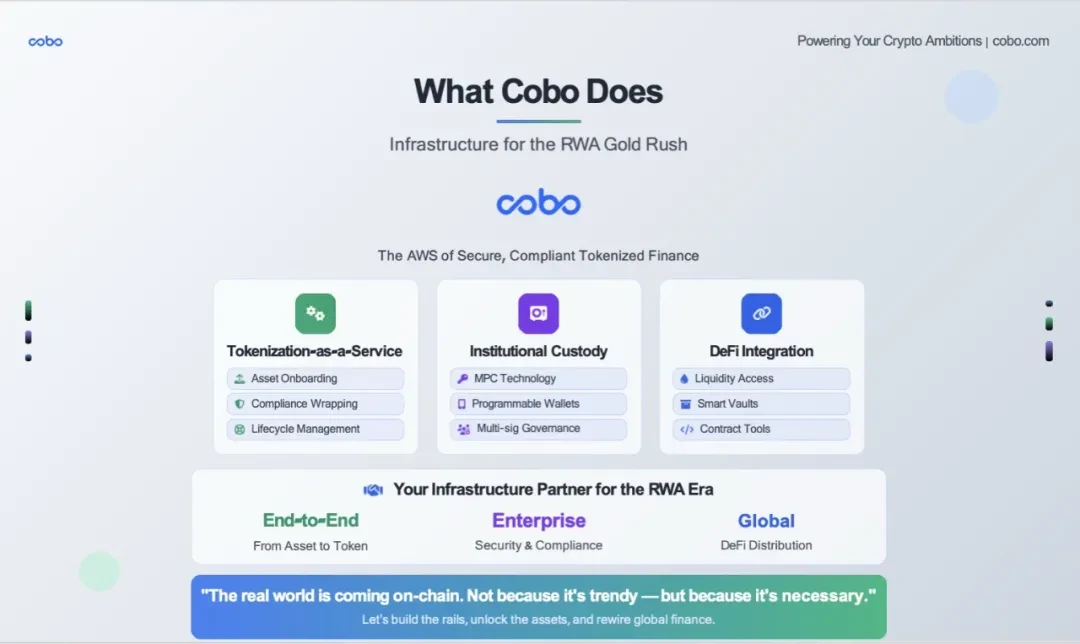

After understanding the trend opportunities and confirming the direction, what we need is to obtain the right tools to participate in this RWA boom. This is where Cobo comes in: Cobo provides end-to-end infrastructure for tokenized assets. Whether it is an asset issuer, fund or securities company, Cobo can help you bring real-world assets to the chain safely and compliantly.

Specifically, we do this:

Tokenization as a Service

We help you connect various assets such as government bonds, credit, real estate, etc. to the platform and package them through smart contracts.

You can choose the chain, compliance framework, and access permissions.

We take care of the technology, legal structure and full life cycle management.

Institutional-grade custody

Cobo is a qualified custodian under regulated institutions.

Our MPC (Multi-Party Computation) wallet technology stack gives you security, automation, and full control — no seed phrases and no single point of failure.

We support whitelisted transfers, time-locked vaults, multi-sig governance — all the security features you need to ensure your tokenized assets are secure.

DeFi Integration

We dont just package your assets, we provide you with the tools to distribute and interact with them.

Whether you want to connect to Aave, provide staking services, or build a liquidity pool - we can distribute and interact with the infrastructure needed by institutional wallets such as Web3 wallets and MPC wallets that can interact directly with the blockchain.

Think of Cobo as a middleware layer between traditional assets and on-chain liquidity. From asset access to custody, from compliance management to role-based authorization to interaction with the blockchain in a risk-controlled environment, Cobo is your infrastructure partner to help you build and expand your business in this new market.

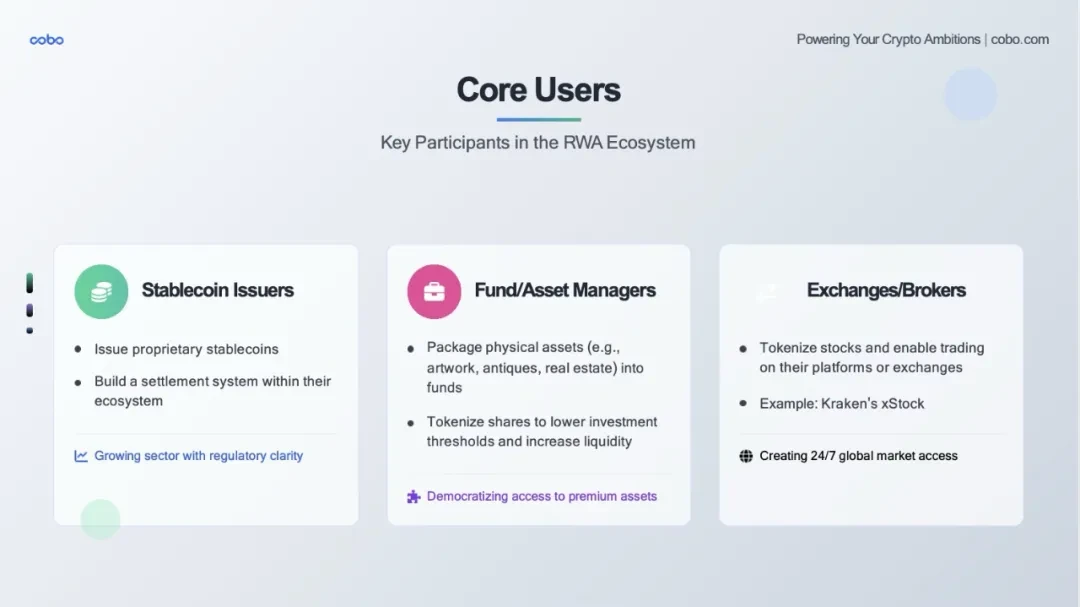

Our RWA Engine can serve all stablecoin issuers, asset managers, exchanges and exchange-like institutions.

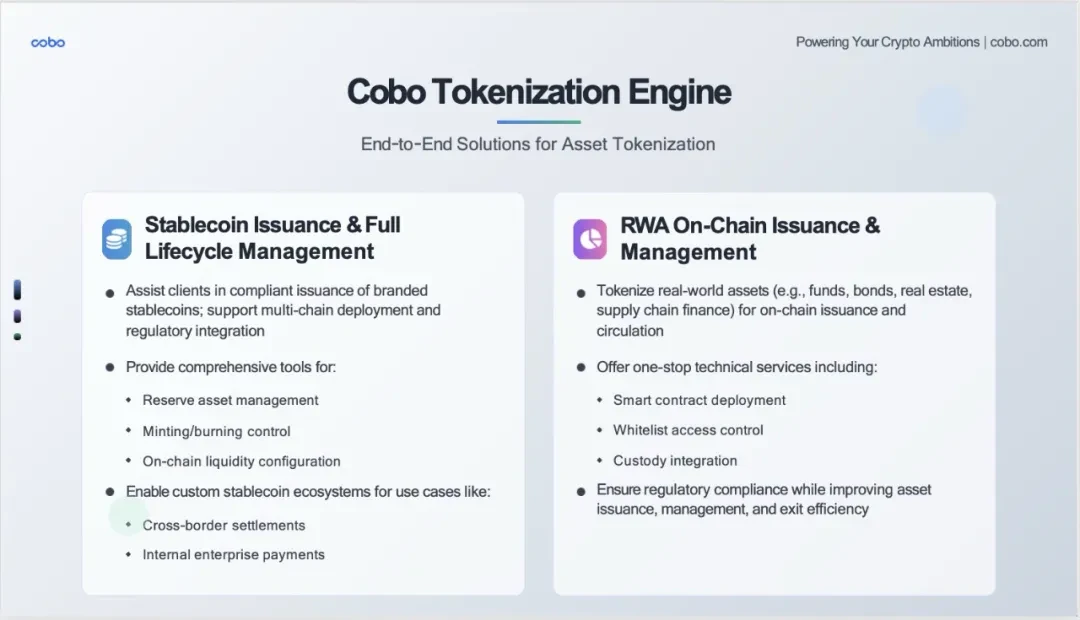

Cobo Tokenization Engine is our core technology engine built for the RWA era. Rather than simply providing a single tool, we have built two complete end-to-end solutions covering the two most important tracks in the tokenization space.

Left: Stablecoin issuance and full life cycle management

In our interactions with clients, we found that many institutions want to issue their own branded stablecoins, but face three major challenges:

High technical threshold: smart contract development, multi-chain deployment

Compliance is complex: Regulatory requirements in different jurisdictions

Operational difficulties: reserve management, liquidity allocation

Cobo’s Solution

We provide not only technical tools, but also a complete ecosystem:

Compliance issuance: Help customers issue branded stablecoins in compliance with local regulatory requirements

Multi-chain deployment: One system supports multiple mainstream blockchains such as Ethereum, BSC, Polygon, etc.

Comprehensive Tool Kit:

Reserve asset management: real-time monitoring, automated reporting

Minting/Destruction Control: Precise Supply Management

On-chain liquidity configuration: deep integration with mainstream DEX and CEX

Application scenario display

Cross-border settlement: Companies can issue their own stablecoins for international trade settlement

Internal payments: Large groups can use it for internal transfers and employee salaries

Right: RWA on-chain issuance and management

The data we just saw - BUIDLs $29 billion, China Asset Managements $120 million - all prove the huge potential of the RWA market. However, to truly scale up, industrial-grade infrastructure is needed. What we provide to RWA issuers is a real move-in ready solution:

Smart contract deployment: audited, modular contract templates

Whitelist access control: precise permission management to meet different regulatory requirements

Custody Integration: Seamless integration with our custodian, MPC wallet and Hong Kong Trust Company

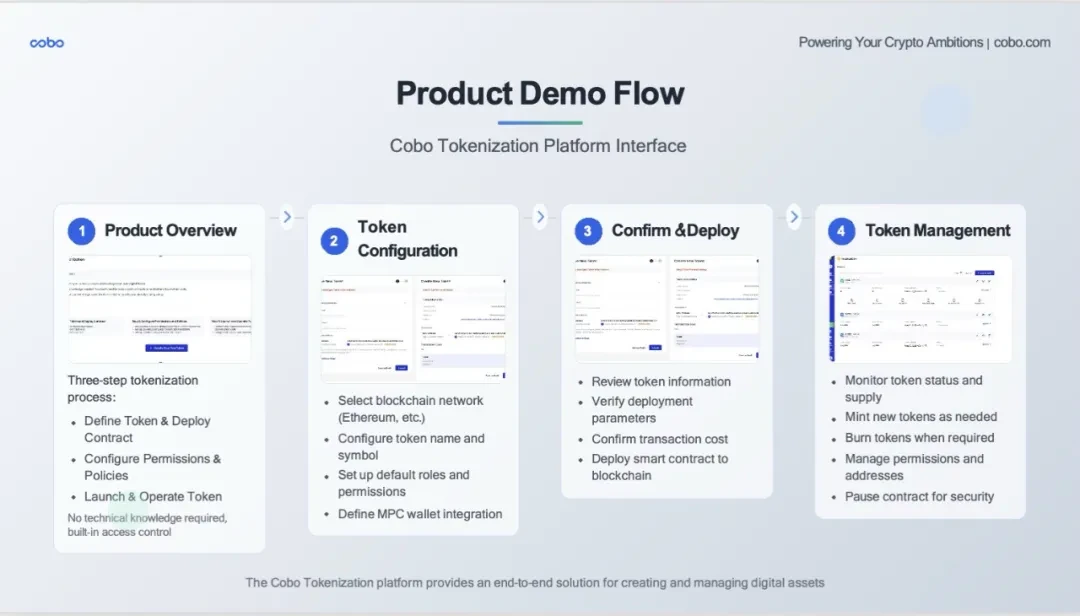

Shown here is the actual user interface and operation flow of our tokenization platform.

Step 1: Product Review (Product Overview)

This is the first screen the user sees.

The three-step process is clearly demonstrated: define tokens deploy contracts, configure permissions policies, launch operate tokens

No technical threshold commitment: The interface clearly states no technical knowledge required

One-click start: lowering the user threshold

Step 2: Token Configuration

Here is the actual configuration interface:

Blockchain selection: Users can choose different blockchains such as Ethereum mainnet

Basic information of tokens: name, symbol and other necessary information

Security settings: MPC wallet integration to ensure asset security

Customized settings: meet the personalized needs of different customers

Step 3: Confirm Deploy

This is the key confirmation link:

Information verification: all parameters are clear at a glance

Cost transparency: Clearly display the deployment fee ($0.99)

MPC wallet display: Demonstrating our core security technology

Final confirmation: Give users a final chance to check

Step 4: Token Management

This is the management interface after deployment:

Multi-token management: support for managing multiple token projects at the same time

Status monitoring: Success, Processing, Failed and other status are clearly displayed

Rich in functions: complete functions such as casting, destruction, permission management, contract suspension, etc.

Data details: total supply, personal holdings, contract address and other key information

We have discussed a lot today - from market trends to technical architecture, from specific cases to product demonstrations. But I would like to summarize todays core points in one sentence:

First sentence: The inevitability of reality - the irreversibility of tokenization;

Second sentence: The nature of motivation - RWA is not because blockchain is cool or tokenization is trendy. It is because the limitations of the traditional financial system - geographical boundaries, time constraints, high costs, complex processes - these problems must be solved;

The third sentence: A call to action. Asset parties need to bring high-quality real-world assets; technology parties need to provide reliable infrastructure (this is our role); investors: provide liquidity and trust; regulators: provide a compliance framework.

This window won’t stay open forever. Early adopters will reap the biggest rewards—not just financial gains, but the opportunity to shape the future financial system.