On June 17, Infini suddenly announced the complete closure of all Card services.

As a star project in this round of U card craze, Infini has not shut down its services even though it recently encountered an operational crisis in which about 50 million US dollars of funds were stolen. Instead, it has chosen to withdraw from the market voluntarily. The explanation given by Infini co-founder @0x sexybanana is also quite representative:

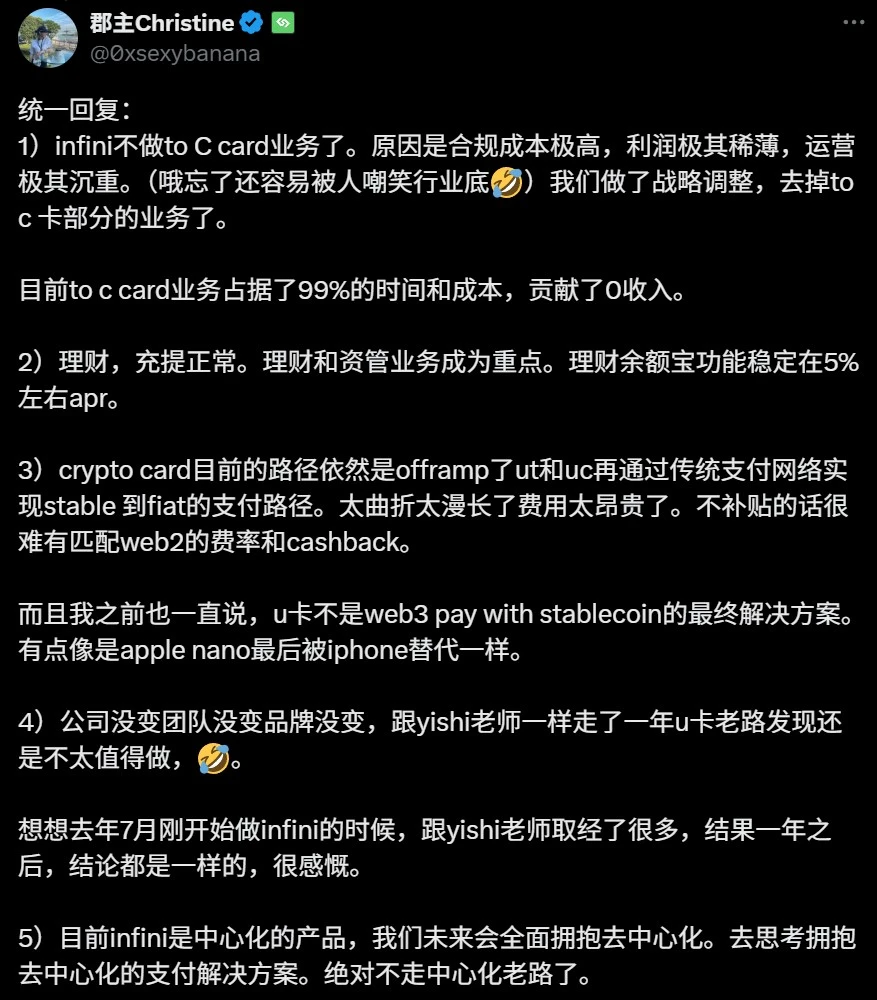

Compliance costs are extremely high, profits are thin, and operations are heavy... We have made strategic adjustments and removed some of the to C card business.

This reflects the real situation of this business - heavy compliance investment, low profit returns, and high risks. After all, since last year, the PayFi narrative has been high-profile, especially in the first half of this year, when U card projects were launched in large numbers, and the business was booming until Infinis sudden exit.

Source: @0x sexybanana

This makes us wonder: Is U Card a good business?

U Card has never been a good business

To discuss the issue of U Card, we must first clarify a basic premise: the current doubts in the market are not about consumption with cryptocurrency, but the feasibility of the operating model behind the U Card that is highly dependent on traditional financial intermediaries.

To put it bluntly, since the term U card began to be widely accepted, it basically refers to a specific business operation model:

From the early Dupay to the later OneKey Card and Infini, they are essentially forms of overseas prepaid consumption cards. The Web3 project obtains authorization through cooperative financial institutions and card organizations (such as Mastercard and Visa), and then packages them into off-chain consumption solutions that crypto users can use.

Functionally, this model opens up the consumption link by aggregating third-party intermediaries, exchanging stablecoins for legal currencies such as US dollars and recharging them into prepaid cards. This has indeed greatly alleviated the problem of Web3 users spending/passing Crypto directly. It is a convenient solution in the Off-Ramp scenario and can be regarded as a transitional product that realizes the combination of Crypto and existing card payments in a specific historical stage.

But commercially, it is an extremely fragile business, because the lifeblood of the entire U Card operating model lies in the fact that its business model is extremely dependent on the permission and stability of third-party institutions.

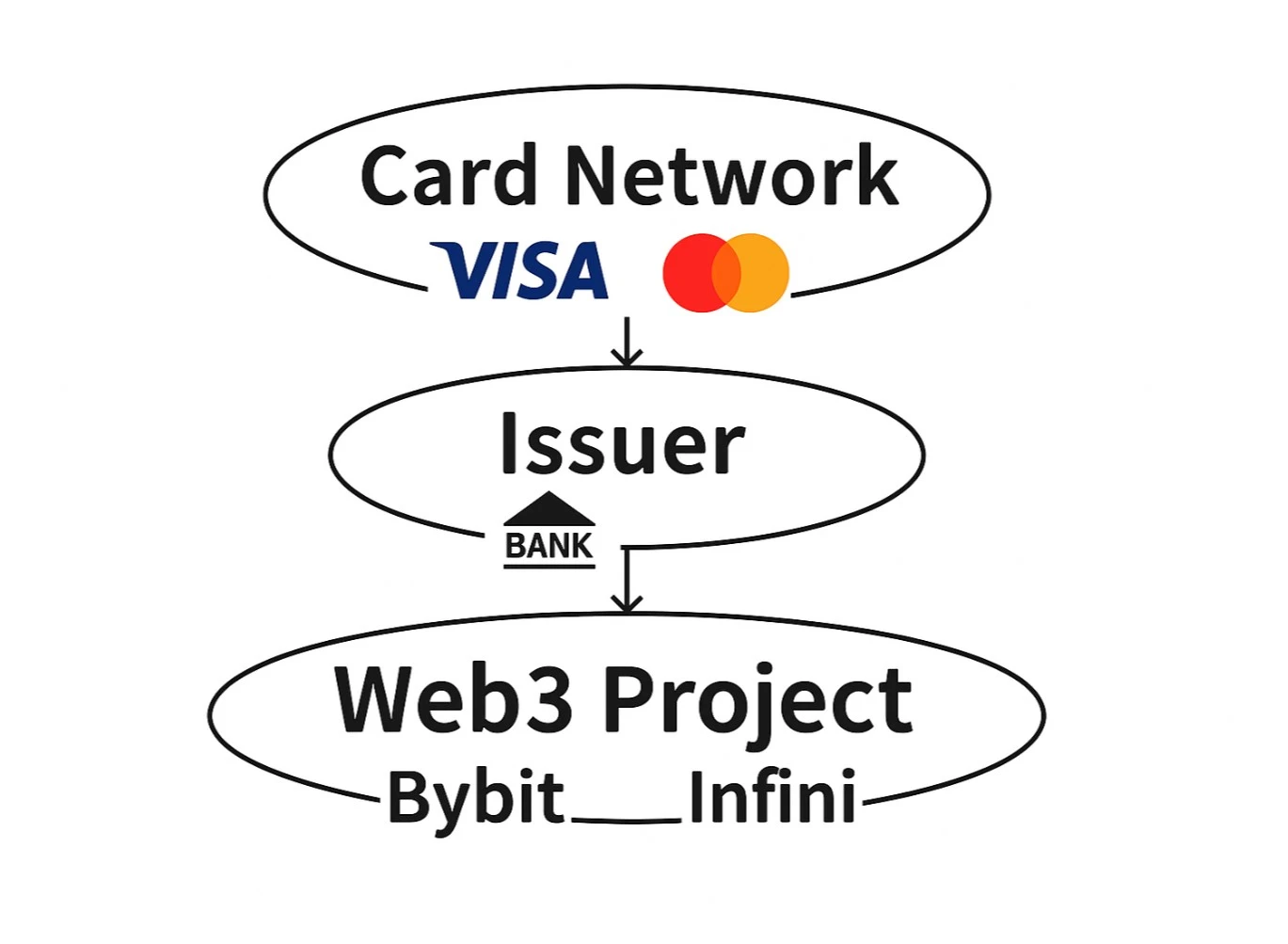

Taking the common U card issuance logic on the market as an example, they are usually issued by Web3 project parties in cooperation with traditional financial institutions (banks and other card issuers), presenting a three-level architecture of card organization-card issuer-Web3 project:

Card organization layer (such as Visa and Mastercard): control the core card number (BIN) resources and access to the clearing system;

Tier 1 card issuers (such as licensed financial institutions such as DCS and Fiat 24): responsible for compliance, regulatory coordination, fund custody and risk control execution;

Web3 project parties (such as Infini and Bybit): responsible for front-end product packaging, user traffic and promotion operations, but in essence they are just secondary operators who rent licenses;

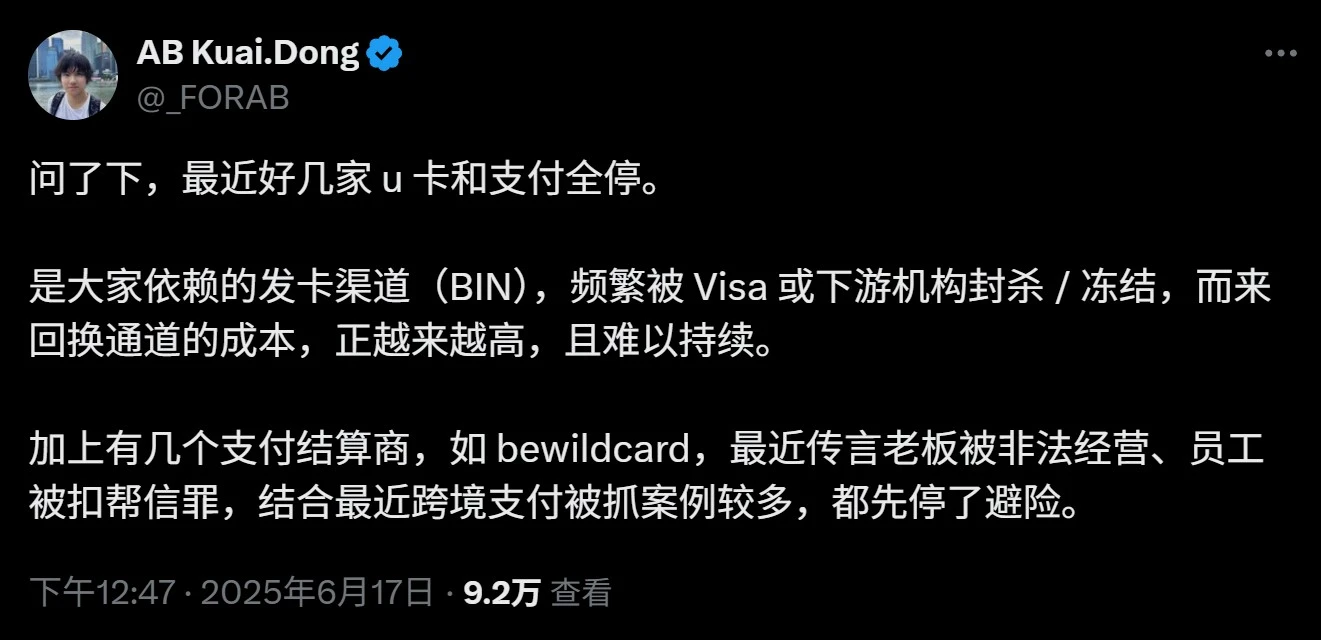

This three-tier architecture seems to have a clear division of labor, but the project party is actually at the end of the ecological chain with the least authority, the greatest responsibility and the highest risk . It lacks bargaining power with card organizations and issuers. Once the source of user funds is questioned, or sensitive behaviors such as money laundering and online fraud funds flow into the card market, even if there is no clear violation, the issuing bank or card organization may cut off the card or close the account based on the risk-prudent principle.

The more realistic problem is that the U card business itself naturally faces a high-risk scenario of being abused by online fraud gangs, and the project party does not have endogenous cash flow businesses such as handling fees as a buffer like exchanges. Instead, it has to directly bear the potential losses and regulatory obligations of C-end users.

In this type of model, once an accident occurs at the regulatory level, the card organizations and upstream banks will usually pass on all AML (anti-money laundering) fines to the project party. In minor cases, the deposit will be deducted, and in serious cases, the cooperation will be directly terminated. The intermediary service providers and payment channel providers are only responsible for collecting service fees and tolls, and never bear any substantial risks. This also explains why a large number of U card projects cannot survive more than a year or two.

Therefore, the statement of Infini’s founder that “99% of time and cost investment brings 0 income” is not an exaggeration. In this chain, the bulk of the money is indeed eaten up by the card issuers, and the project parties are just struggling with small profits. Real profits need to be based on huge transaction flows + asset accumulation + high-frequency consumption scenarios, but at the same time, compliance and operation and maintenance costs will also increase exponentially as the business expands.

Moreover, this judgment itself implies a premise - that is, the project party is always at the end of the supply chain, and is limited by its position as a secondary operator and cannot intervene in the upstream. This also shows that the difficulty of Infini and other U cards to continue is not the fate of the industry, but a problem of path selection:

Projects that really want to break through the profit bottleneck need to move upward, enter the account system, and enter the compliance layer, rather than relying solely on the second-hand or even third-hand or fourth-hand capabilities provided by BIN Sponsors such as Interlace.

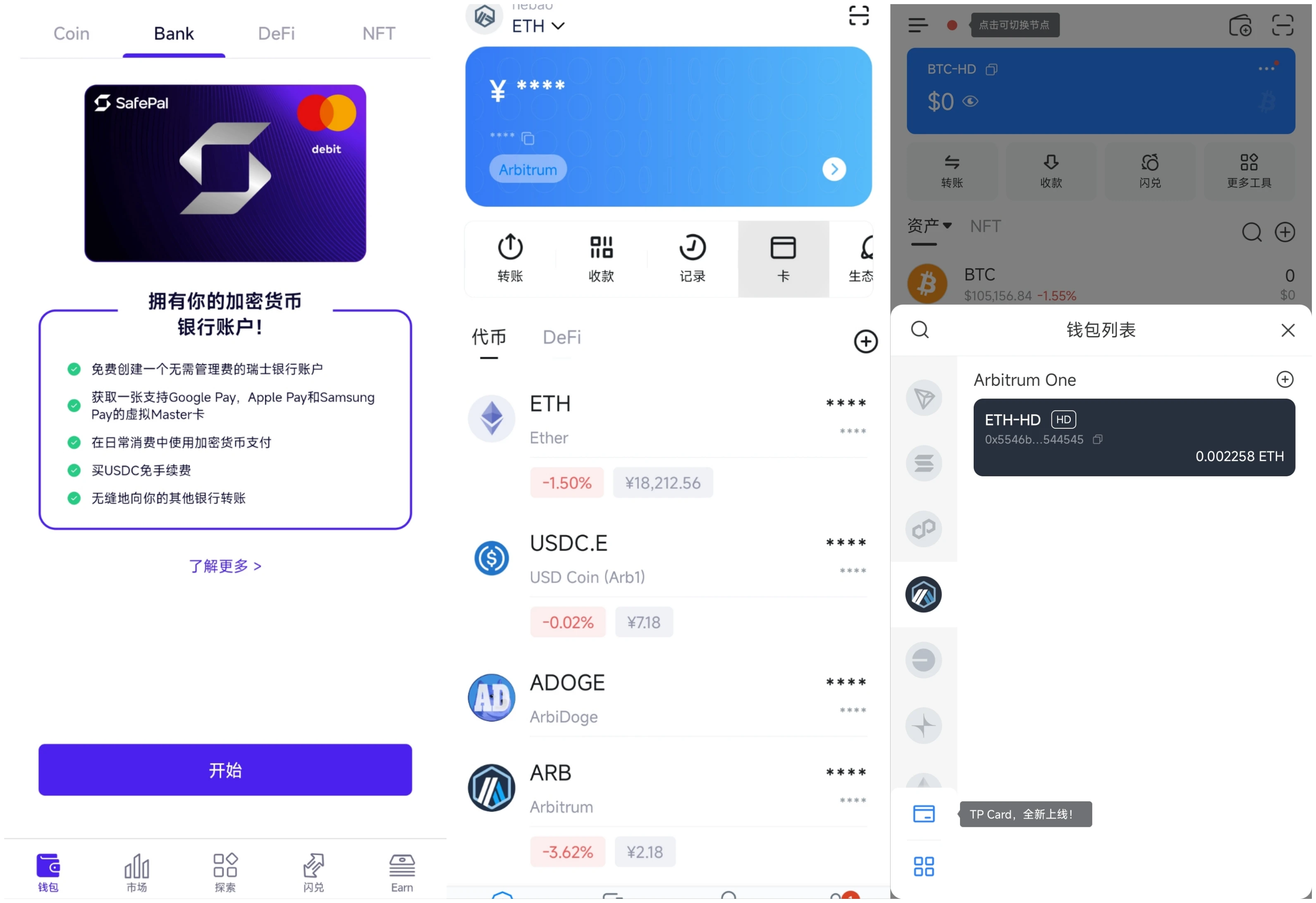

In fact, the projects that are still providing similar services on the market are no longer pure U card products that do on-chain diversion + off-chain splicing. Take SafePal, imToken, and TokenPocket as examples. These three companies are all based on the Swiss bank Fiat 24. They can be said to have the same origin, but the integration paths and entry strategies are different:

SafePal takes into account both personal bank account + co-branded MasterCard services, and puts the Bank service on the first-level page of the first-level entrance;

As a Fiat 24 partner, imToken mainly provides MasterCard services. Compared with SafePal, it hides the bank account service, but also places the card in the first-level entrance;

TokenPocket is more obscure, with the service entrance buried in the secondary entrance. It is also mainly based on MasterCard services, and the Android system needs to download the Google Play version to enable it;

From left to right: SafePal Bank page, imToken Card entrance, TP Card entrance

Especially for companies like SafePal that have directly entered the card issuance and account levels through strategic investment in Fiat 24, they are no longer the middlemen at the end of the chain, which fundamentally reduces the friction and costs in the middle links. They can then pass this advantage back to users and provide preferential policies such as no account opening fees and 0 handling fees for deposits and withdrawals.

However, for wallets/exchanges, U-card services are not their main business, but are just a plus point for Web3 custody/non-custodial business - they can attract traffic and customers, as well as increase users long-term loyalty and subsequent AUM. From this perspective, not making money or even losing money in the short term is acceptable.

Therefore, as a bonus point to improve user loyalty and asset service stickiness, the main players are almost all wallets and exchanges. The former is represented by SafePal, imToken, TokenPocket, and Bitget Wallet, while the latter includes leading exchanges such as Bybit and Bitget.

As mentioned before in A Chaotic Era of Crypto Payment Cards, a Business that is Hard to Sustain? , Web3 wallets naturally have the ability to manage crypto assets and are ideal carriers of PayFi services. They can also build a longer-term payout structure from the perspectives of traffic diversion, AUM, user binding, etc. The same is true for exchanges.

Ultimately, in such a financial application scenario with strong supervision, strict compliance and low profits, if you only try to promote it by organizing forums, subsidies and other forms, it will be a very difficult nut to crack for Web3 startup teams that do not have a main traffic base and lack financial underlying knowledge. This is also the fundamental reason why Infini finally chose to abandon the consumer U card and focus on financial management and B-side services.

From Crypto to TradFi, it’s a good business

Are U cards themselves useless?

That is not the case.

As mentioned above, U Card has indeed completed its phased mission at the historical node of its birth: helping global crypto users to quickly realize the consumption of on-chain assets, bypassing the cumbersome legal currency withdrawal process, and allowing Crypto assets to enter the real world through the form of prepaid cards.

As an off-ramp shortcut for early Crypto users to connect on-chain assets with daily consumption, even though the U card is highly dependent on traditional financial infrastructure such as Visa and Master, it is not a good business that is easy to make a profit, but the user needs it meets are real.

If we make an analogy, it is more like the telephone food ordering service before the popularity of Meituan and Ele.me. It is indeed an improvement in user experience, but it is still a product of stitching together under the old system. It does not have sufficient scale and structural stability, and is ultimately destined to be replaced by a better solution.

Interestingly, just before Infini announced its closure, in the early morning of June 18th, Beijing time, the U.S. Senate passed the GENIUS Act, which is hailed as a milestone in crypto payment legislation, with 68 votes in favor and 30 votes against. The bill is likely to be reviewed by the House of Representatives and officially signed into law during Trumps term.

Source: Politico

This means that stablecoins and stablecoin payments are entering a more compliant and institutionalized reshaping cycle. The grassroots era is coming to an end, and a new round of PayFi opportunity window is opening.

Therefore, the real question is, what kind of financial entry and exit do crypto users really need?

The answer may not be a U card, but a compliant, stable and scalable financial account system - it can not only spend U, but also complete the on-chain-off-chain two-way circulation and realize a true closed loop of asset flow.

In other words, U cards are destined to be replaced by licensed banks with regulatory qualifications and risk control capabilities. Traditional financial institutions will more proactively embed Web3 payment paths and usage scenarios, and on the basis of ensuring compliance, complete the full-link connection of user wallets, merchant collections, and asset deposits and withdrawals through bank accounts, payment channels and clearing systems.

This is also the path currently taken by mainstream wallets such as SafePal, imToken, and TokenPocket. They no longer use cards as their core selling point, but instead cooperate with licensed bank Fiat 24 to open up the financial entrance and exit from Crypto to TradFi around account compliance and deposits and withdrawals. Card services are just supporting tools.

As a Principal Member of MasterCard, Fiat 24 can bypass intermediary service providers and directly connect with the central bank (ECB) and card organizations, so it can achieve lower card issuance costs and transaction fees. The Swiss FINMA financial intermediary license it holds also allows users to open a regulated bank account with the same name and achieve compliant conversions between stablecoins and fiat currencies. This is an upstream advantage that is clearly different from players such as Infini.

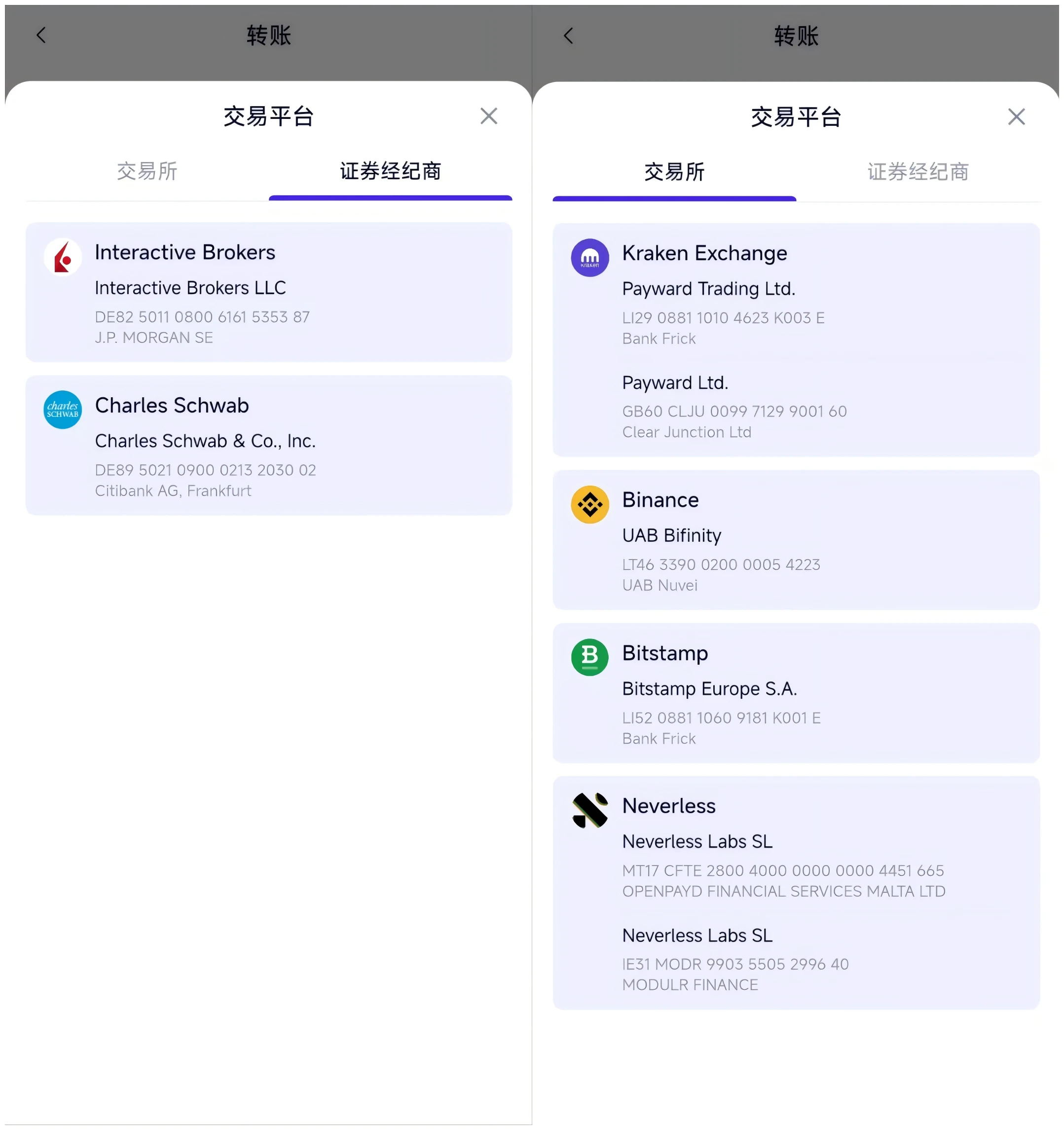

SafePal Bank service supports brokerage firms and CEX deposit and withdrawal services

Taking SafePals Bank service as an example, it made a strategic investment in Fiat 24 as early as 2023. From the perspective of business structure, it does not need to rent a license as a middleman. The essential difference between it and pure card businesses such as Infini lies in that by directly controlling the account system and card issuance resources, it has broken through the limitations of secondary operators and can achieve a better balance between cost and risk control.

For example, the preferential rates provided by SafePal to the community, such as “free deposits and withdrawals, and no account and card opening fees”, are structural cost advantages that are difficult to achieve for most projects that are still in the “outsourced card issuance” stage.

In addition, the bank account system based on Fiat 24 not only supports daily card payments, but also opens up key scenarios for closed-loop funds on and off the chain:

Deposit/Withdrawal with brokerage firms: Users can convert crypto assets into Euros and transfer them to mainstream brokerage accounts such as IBKR, Charles Schwab, and Tiger Brokers through SEPA remittances to achieve cross-market allocation of on-chain assets;

CEX channel deposit and withdrawal: supports transfers to exchanges that support euro deposits, such as Kraken and Bitstamp, or reverse withdrawals to personal bank accounts, avoiding gray OTC risks, completing the deposit and withdrawal paths of cryptocurrencies and fiat currencies, and ensuring a clear and compliant capital chain;

Off-chain fund repatriation: Through cross-border payment service providers such as Wise, users can even indirectly transfer Euro remittances back to domestic bank accounts or Alipay and WeChat, realizing a closed-loop flow of assets from the chain to the local system;

This entire path goes far beyond the traditional U card usage of swipe and its done and truly possesses account attributes, compliance capabilities and service scalability.

From U-card to account, and then to the future stable currency payment

From a business logic perspective, the card + account model obviously has greater structural resilience and growth potential, in which compliant banks dominate accounts and supervision, while Web3 wallets focus on on-chain asset access and user interaction. The two form a collaborative architecture with clear responsibilities and mutual complementation, which is far more sustainable than the pure card business promoted by the project party alone.

The author has always believed that Crypto and TradFi have never been on opposite sides, but are accelerating the evolution process of integration and leveraging each other. After all, TradFi excels in compliance supervision, account structure and risk control system, while Crypto has natural advantages in asset openness, programmability and trustless execution.

Therefore, before the payment system undergoes a complete transformation in the future, the most robust, realistic, and sustainable path is for licensed financial institutions to lead compliance accounts and clearing and settlement systems, while Web3 projects focus on on-chain entry and asset operations, forming the optimal combination of compliance and flexibility.

This model is an ongoing solution. Although it may not be highly profitable, it is highly structurally resilient and is the most feasible PayFi solution at the current stage. It is also the path taken by SafePal, imToken, etc.: cooperating with Fiat 24 to provide real and usable IBAN accounts, Mastercard payment cards, SEPA channels, and compliant deposit and withdrawal capabilities of brokerages and CEXs, thus realizing a closed loop of assets on and off the chain.

If the timeline is extended further, the ultimate form of PayFi may be an on-chain payment network that completely leaves Visa/Master behind:

Merchants accept stablecoin payments and no longer convert fiat currencies;

Users send transactions directly from their wallets, with funds self-custodied and cleared on-chain;

The backend is supported by compliant stablecoins and clearing and settlement networks, without the need for Visa/Mastercard or SWIFT channels;

In fact, this trend is already happening. From Circles launch of Programmable Wallets and CCTP (cross-chain USDC clearing) to global payment giant Stripes acquisition of stablecoin API service provider Bridge for US$1.1 billion at the end of last year, they are all trying to connect on-chain accounts, stablecoin assets and merchant payment terminals, bypassing the issuing banks and card organizations in the traditional payment chain.

This also shows that traditional payment network giants are no longer warning against encryption, but are actively integrating on-chain capabilities and moving closer to the Web3 account structure and stablecoin clearing network. This system is expected to truly bypass the high cost and low efficiency bottlenecks of the traditional payment system, and may even surpass existing cross-border payment solutions such as Airwallex and Wise in terms of cost and experience, becoming the next generation of global payment infrastructure.

But that is for the future.

It can be foreseen that the U card belongs to the historical completion tense, the current compliant bank account model of SafePal/Fiat 24, etc. is the present ongoing tense, and the on-chain stablecoin clearing and settlement network is the real future occurrence tense.

Ultimately, whoever can penetrate the evolutionary path of these three-layer structures will be qualified to occupy a place in the next round of payment paradigm change.

Last words

Therefore, the exit of Infini is just the natural end of U card, a transitional product that is destined to be replaced.

We can perhaps view it as a tentative connection between the Web3 world and the real world when the compliance channel is not yet clear. To a certain extent, it has fulfilled the historical mission of making Crypto spendable.

However, as the regulatory red lines become clearer and the status of stablecoins continues to rise, users demands are shifting from being able to swipe to being able to circulate, manage finances, and close the loop. This requires truly building underlying capabilities, especially the two-way synergy of Crypto and TradFi.

The next PayFi game is no longer on the cards.