I. Summary

In the first half of 2025, the global macro environment continues to be highly uncertain. The Fed has repeatedly suspended interest rate cuts, reflecting that monetary policy has entered a wait-and-see stage, while the Trump administrations tariff increase and escalating geopolitical conflicts (such as the Iran-Israel conflict, the Middle East energy line crisis, and the destruction of Russian fighter jets) have further torn the global risk preference structure. We will start from five macro dimensions (interest rate policy, US dollar credit, geopolitics, regulatory trends, and global liquidity), combine on-chain data and financial models, and systematically evaluate the opportunities and risks of the crypto market in the second half of the year, and put forward three core strategic recommendations, covering Bitcoin, stablecoin ecology, and DeFi derivatives.

II. Review of the global macro environment (first half of 2025)

In the first half of 2025, the global macroeconomic landscape continued the multiple uncertainties that have characterized it since the end of 2024. Under the interweaving of multiple factors such as weak growth, inflation stickiness, the vague outlook for the Federal Reserves monetary policy, and escalating geopolitical tensions, global risk appetite has shrunk significantly. The dominant logic of macroeconomics and monetary policy has gradually evolved from inflation control to signal game and expectation management. As a frontier field for global liquidity changes, the crypto market also shows typical synchronous fluctuations in this complex environment.

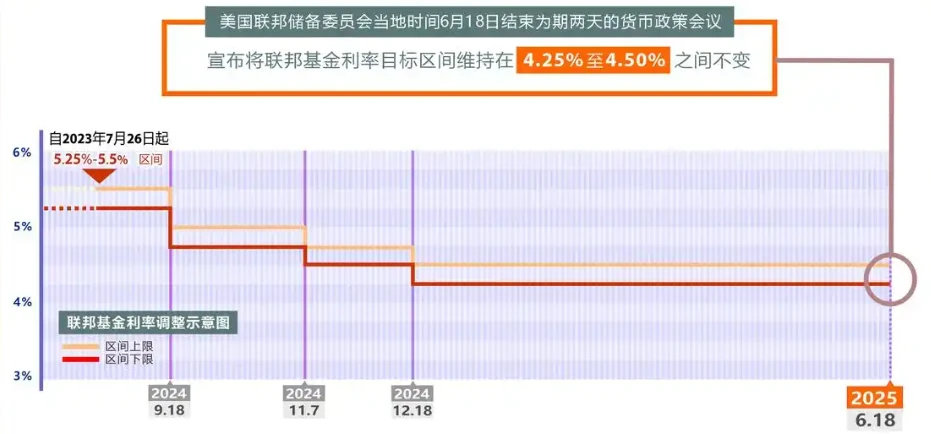

First, from the perspective of the Feds policy path review, at the beginning of 2025, the market had reached a consensus on the expectation of three interest rate cuts within the year, especially against the background of a significant decline in the month-on-month growth rate of PCE in the fourth quarter of 2024. The market generally expected that 2025 would enter the beginning of an easing cycle under the stable growth + moderate inflation. However, this optimistic expectation soon encountered a reality shock at the FOMC meeting in March 2025. Although the Fed did not take any action at that time, the statement after the meeting emphasized that inflation is far from reaching the target and warned that the labor market is still tight. Since then, CPI has rebounded more than expected twice in April and May (3.6% and 3.5% respectively), and the year-on-year growth rate of core PCE has always remained above 3%, reflecting that sticky inflation has not subsided as the market expected. The structural causes of inflation - such as rigid increases in housing rents, sticky wages in the service industry, and periodic shocks to energy prices - have not undergone fundamental changes.

Faced with the pressure of rising inflation again, the Fed once again chose to pause interest rate cuts at its June meeting, and lowered its forecast for the number of interest rate cuts in 2025 from three at the beginning of the year to two through the dot plot, and the federal funds rate was expected to remain above 4.9% at the end of the year. More importantly, Powell hinted at the press conference that the Fed has entered a stage of data dependence + observation and waiting, rather than the easing cycle confirmation period interpreted by the market before. This indicates that monetary policy is shifting from directional guidance to time point management, and the uncertainty of the policy path has significantly increased.

On the other hand, the first half of 2025 also showed a phenomenon of intensified division between fiscal policy and monetary policy. As the Trump administration accelerates the strategic combination of strong dollar + strong border, the US Treasury Department announced in mid-May that it will optimize the debt structure through a variety of financial means, including promoting the legalization of US dollar stablecoins, and trying to use Web3 and financial technology products to spill over US dollar assets and achieve liquidity injection without obvious expansion of the balance sheet. This series of fiscal-led measures to stabilize growth are clearly decoupled from the Federal Reserves monetary policy direction of maintaining high interest rates to suppress inflation, and market expectation management has become increasingly complicated.

The Trump administrations tariff policy has also become one of the dominant variables in the global market turmoil in the first half of the year. Since mid-April, the United States has successively imposed a new round of tariffs ranging from 30% to 50% on Chinas high-tech products, electric vehicles, and clean energy equipment, and threatened to further expand the scope. These measures are not simply trade retaliation, but more of an intention of the government to create inflationary pressure through imported inflation and thus force the Federal Reserve to cut interest rates. Against this background, the contradiction between the credit stability of the US dollar and the interest rate anchor has been brought to the fore. Some market participants began to question whether the Federal Reserve still has independence, which in turn triggered a repricing of long-term U.S. Treasury yields. The 10-year U.S. Treasury yield once surged to 4.78%, and the term spread between the 2-year and 10-year bonds turned negative again in June, and expectations of a recession rose again.

At the same time, the continued escalation of geopolitics has a substantial impact on market sentiment. Ukraine successfully destroyed the Russian strategic bomber TU-160 in early June, triggering a high-intensity verbal confrontation between NATO and Russia; in the Middle East, Saudi Arabias key oil infrastructure suffered a suspected Houthi armed attack at the end of May, resulting in damage to crude oil supply expectations and Brent crude oil prices breaking through $130, a new high since 2022. Unlike the market reaction in 2022, this round of geopolitical events did not lead to a simultaneous rise in Bitcoin and Ethereum. Instead, it prompted a large amount of safe-haven funds to flow into the gold and short-term U.S. Treasury markets, and the spot price of gold once exceeded $3,450. This change in market structure shows that Bitcoin is still more regarded as a liquid transaction product at the current stage rather than a macro safe-haven asset.

From the perspective of global capital flows, there is a clear trend of de-emerging marketization in the first half of 2025. IMF data and JP Morgans cross-border capital tracking show that the net outflow of emerging market bonds in Q2 hit the highest single-quarter since the epidemic in March 2020, while the North American market received a relative net inflow of funds due to the stable attraction brought by ETFization. The crypto market is not completely out of the loop. Although the Bitcoin ETF has accumulated a net inflow of more than US$6 billion this year and has performed strongly, small and medium-sized market value tokens and DeFi derivatives have suffered large-scale capital outflows, showing significant signs of asset stratification and structural rotation.

In summary, the first half of 2025 presents a highly structured uncertain environment: monetary policy expectations are drastically tugged, fiscal policy intends to spill over the credit of the US dollar, frequent geopolitical events constitute new macro variables, capital flows back to developed markets, and the structure of safe-haven funds is restructured, all of which lay a complex foundation for the operating environment of the crypto market in the second half of the year. It is not just a simple question of whether to cut interest rates, but a multiple battlefield around the credit reconstruction of the US dollar anchor, the competition for global liquidity dominance, and the integration of the legitimacy of digital assets. In this battle, crypto assets will look for structural opportunities in institutional gaps and liquidity redistribution. The next stage of the market will no longer belong to all coins, but to investors who understand the macro landscape.

3. Reconstruction of the US dollar system and the systematic evolution of the role of cryptocurrency

Since 2020, the US dollar system has been undergoing the deepest round of structural reconstruction since the collapse of the Bretton Woods system. This reconstruction does not stem from the evolution of payment tools at the technical level, but from the instability of the global monetary order itself and the crisis of institutional trust. Against the backdrop of drastic fluctuations in the macro environment in the first half of 2025, the US dollar hegemony faces both an imbalance in internal policy consistency and multilateral monetary experiments that challenge authority from the outside. Its evolution trajectory profoundly affects the market position, regulatory logic and asset role of cryptocurrencies.

From the perspective of internal structure, the biggest problem facing the US dollar credit system is the shaking of the monetary policy anchoring logic. Over the past decade, as an independent inflation target manager, the Federal Reserve has had a clear and predictable policy logic: tightening when the economy is overheated, easing during downturns, and taking price stability as the primary goal. However, in 2025, this logic is being gradually eroded by the strong fiscal-weak central bank combination represented by the Trump administration. The Biden eras insistence on fiscal easing and monetary independence has gradually been reshaped by Trump into a fiscal priority strategy, the core of which is to use the dollars global dominance to reversely export domestic inflation, indirectly prompting the Federal Reserve to adjust its policy path in line with the fiscal cycle.

The most intuitive manifestation of this policy split is that the Ministry of Finance continues to strengthen the shaping of the internationalization path of the US dollar while bypassing traditional monetary policy tools. For example, the Compliance Stablecoin Strategic Framework proposed by the Ministry of Finance in May 2025 clearly supports the global spillover of US dollar assets through on-chain issuance in the Web3 network. Behind this framework is the intention of the US dollar financial state machine to evolve into a technology platform country. Its essence is to shape the distributed currency expansion capacity of the digital dollar through new financial infrastructure, so that the US dollar can continue to provide liquidity to emerging markets while bypassing the central banks expansion of its balance sheet. This path integrates the US dollar stablecoin, on-chain Treasury bonds and the US commodity settlement network into a digital dollar export system, which is intended to strengthen the network effect of US dollar credit in the digital world.

However, this strategy also raises market concerns about the disappearance of the boundary between fiat currencies and crypto assets. As the dominance of US dollar stablecoins (such as USDT and USDC) in crypto transactions continues to increase, their essence has gradually evolved into digital representation of the US dollar rather than crypto native assets. Correspondingly, the relative weight of purely decentralized crypto assets such as Bitcoin and Ethereum in the trading system continues to decline. From the end of 2024 to Q2 2025, CoinMetrics data showed that in the total trading volume on major global trading platforms, the proportion of USDT trading pairs against other assets increased from 61% to 72%, while the proportion of BTC and ETH spot transactions both declined. This change in liquidity structure indicates that the US dollar credit system has partially swallowed the crypto market, and US dollar stablecoins have become a new source of systemic risk in the crypto world.

At the same time, from the perspective of external challenges, the US dollar system is facing continuous temptation from multilateral monetary mechanisms. Countries such as China, Russia, Iran and Brazil are accelerating the construction of local currency settlement, bilateral clearing agreements and commodity-linked digital asset networks, with the aim of weakening the monopoly of the US dollar in global settlement and promoting the steady implementation of the de-dollarization system. Although an effective network to confront the SWIFT system has not yet been formed, its infrastructure replacement strategy has put marginal pressure on the US dollar settlement network. For example, the China-led e-CNY is accelerating cross-border payment interface connections with many countries in Central Asia, the Middle East and Africa, and exploring the use scenarios of central bank digital currencies (CBDCs) in oil, gas and bulk commodity transactions. In this process, crypto assets are sandwiched between the two systems, and the issue of their institutional affiliation has become increasingly vague.

As a special variable in this pattern, the role of Bitcoin is shifting from decentralized payment tool to de-sovereign anti-inflation asset and liquidity channel under institutional gaps. In the first half of 2025, Bitcoin was widely used in some countries and regions to hedge against currency depreciation and capital controls, especially in Argentina, Turkey, Nigeria and other countries with unstable currencies. The grassroots dollarization network composed of BTC and USDT has become an important tool for residents to hedge risks and realize value storage. On-chain data shows that in the first quarter of 2025 alone, the total amount of BTC flowing into Latin America and Africa through peer-to-peer trading platforms such as LocalBitcoins and Paxful increased by more than 40% year-on-year. Such transactions significantly evaded the supervision of the central bank of the country and strengthened the function of Bitcoin as a gray safe-haven asset.

However, it is important to be vigilant that, precisely because Bitcoin and Ethereum have not yet been included in the national credit logic system, their risk resistance in the face of policy stress testing is still insufficient. In the first half of 2025, the US SEC and CFTC continued to increase their supervision of DeFi projects and anonymous trading protocols, especially launching a new round of investigations on cross-chain bridges and MEV relay nodes in the Layer 2 ecosystem, prompting some funds to choose to exit high-risk DeFi protocols. This reflects that in the process of the US dollar system re-dominant market narratives, crypto assets must reposition their roles, no longer a symbol of financial independence, but more likely to become a tool for financial integration or institutional hedging.

Ethereums role is also changing. With its dual evolution to the data verifiable layer and the financial execution layer, its underlying function has gradually evolved from a smart contract platform to an institutional access platform. Whether it is the on-chain issuance of RWA assets or the deployment of government/enterprise-level stablecoins, more and more activities are incorporating Ethereum into their compliance frameworks. Traditional financial institutions such as Visa, JP Morgan, and Paypal have deployed infrastructure on Ethereum-compatible chains such as Base and Polygon, forming an institutional sandwich with the DeFi native ecosystem. This means that Ethereums institutional position as a financial middleware has been reconstructed, and its future direction does not depend on the degree of decentralization but on the degree of institutional compatibility.

The US dollar system is re-dominating the digital asset market through the triple paths of technology spillover, institutional integration and regulatory penetration. Its goal is not to eliminate crypto assets, but to make them an embedded component of the digital dollar world. Bitcoin, Ethereum, stablecoins and RWA assets will be reclassified, revalued, and re-regulated, and will eventually form a Pan-Dollar System 2.0 anchored by the US dollar and characterized by on-chain settlement. In this system, real crypto assets are no longer rebels but arbitrageurs in the gray area of the system. The future investment logic is no longer just decentralization brings value revaluation, but whoever can embed the reconstructed structure of the US dollar will have institutional dividends.

4. On-chain data perspective: new changes in funding structure and user behavior

In the first half of 2025, the on-chain data showed a complex picture of structural precipitation and marginal recovery intertwined. The proportion of long-term holders (LTH) on the Bitcoin chain has once again hit a record high, the stablecoin supply pattern has been significantly repaired, and the DeFi ecosystem has shown strong risk restraint while recovering in activity. What these indicators reflect is the nature of investor sentiment swinging between risk aversion and probing, as well as the process of restructuring the capital structure of the entire market, which is highly sensitive to changes in policy rhythm.

First, the most representative structural signal comes from the continued rise in the proportion of long-term holders on the Bitcoin chain. As of June 2025, more than 70% of Bitcoin has not moved on the chain for more than 12 months, setting a record high. The trend of LTH holdings continuing to increase not only shows that the confidence of long-term investors in the market has not been shaken, but also represents the continuous contraction of the tradable supply, forming potential support for prices. According to Glassnode data, the Bitcoin holding time distribution curve is shifting to the right, and more and more on-chain coins are being locked up for more than 2 years and 3 years. Behind this behavior is no longer just the emotional expression of the coin hoarding party, but also the fact that structural funds - especially traditional funds such as family offices and pension allocation institutions - have begun to dominate the distribution logic of BTC on the chain. Correspondingly, short-term activity has declined significantly. The decline in on-chain transaction frequency and the continuous decline in the Coin Days Destroyed (number of days of coins destroyed) indicator further confirm the trend of market behavior switching from high-frequency gaming to long-term allocation.

This structural precipitation is also deeply consistent with the behavior pattern of institutions. From the analysis of multi-signature wallets and the distribution of on-chain entities, it can be inferred that more than 35% of Bitcoin is currently controlled by highly concentrated, long-term unmoved large addresses. These addresses show clear centralized characteristics, most of which completed their positions in the fourth quarter of 2023 or early 2024, and then remained silent for a long time. Their existence has changed the previous coin-based speculation pattern dominated by retail investors, and laid the foundation for the underlying chip structure of a new round of bull-bear conversion.

At the same time, the stablecoin market has emerged from a clear bottom repair cycle. From the end of 2024 to the beginning of 2025, USDCs market value declined for five consecutive months due to the Feds liquidity contraction and BSA regulatory uncertainty. After entering the second quarter of 2025, USDCs market value returned to the growth channel, reaching US$62 billion as of June, catching up with the growth rate of USDT. This growth is not an isolated incident, but is driven by the broader expansion of the stablecoin ecosystem. New stablecoins such as USDP issued by Paxos and USDe of Ethena have recorded significant growth in the first half of the year, contributing a total of more than US$3 billion in new supply. It is particularly noteworthy that this round of stablecoin expansion is more derived from real economic activity scenarios, rather than the past interest on currency or pure speculation drive.

The increase in on-chain activity also proves that stablecoins are returning from the counterparty assets of the exchange matching system to the essence of payment and circulation tools between on-chain users. Taking the Base chain as an example, in Q2 2025, the monthly active addresses of USDC increased by 41% month-on-month, higher than the growth rate of Ethereum mainnet and Tron in the same period, reflecting that in the L2 ecosystem, the use of stablecoins is more native and high-frequency. The increase in the cross-chain circulation ratio is also significant. The cross-chain behavior of stablecoins on bridge protocols such as Wormhole and LayerZero reached a stage high in May, indicating that funds are looking for more efficient payment and deployment paths, rather than just obtaining trading profits through arbitrage. This trend also reinforces the long-term path of the crypto market evolving towards a combination of multiple chains and real economic scenarios.

Compared with the structural rebalancing of Bitcoin and stablecoins, the on-chain data of the DeFi ecosystem shows a delicate situation of active repair but risk neutrality. In the first half of 2025, decentralized derivatives and perpetual contract agreements showed far more activity than other sub-sectors, especially platforms such as Abstract, Aevo, and Hyperliquid, with rapid growth in the number of user transactions and the frequency of contract interactions. Aevos daily trading volume exceeded US$1.5 billion in May, and the number of daily active users of Abstract increased by more than 60% year-on-year, reflecting that users still prefer speculative derivatives with low threshold and high leverage. However, behind this enthusiasm lies the reality of low capital utilization. While the TVL of most platforms is growing, their average leverage multiples are not proportional to the growth of the number of open contracts, indicating that although market participants frequently test, there is no systematic leverage accumulation as a whole. This contradictory phenomenon reveals the core signal: although the market is hot, the risk preference of funds has not been truly released, and they are more in a strategic wait-and-see state of waiting for policies to become clear.

Combining the three characteristics of long-term precipitation on the Bitcoin chain, stablecoin supply repair and DeFi fund risk restraint, it can be found that the on-chain data in the first half of 2025 revealed that the crypto market is in a complex intersection of chip reconstruction-expectation compression-heat marginal repair. The capital structure is shifting from the pan-hot money dominance in 2023-2024 to a composite structure with structural precipitation as the bottom and short-term transactions as the surface, and user behavior is repeatedly pulling between short-term speculation and long-term allocation. Under this structure, although it is difficult for the crypto market to form a sustained unilateral rise in the short term, once the macro policy path is clear, such as the Federal Reserve entering a clear interest rate cut cycle, stablecoin legislation breakthroughs, or ETF incremental funds in place, this structure will quickly release its inherent bullish momentum. Therefore, although the on-chain data is quiet on the surface, it actually contains undercurrents, becoming one of the key variables for judging the market elasticity and turning point timing in the second half of the year.

5. Analysis and strategic recommendations on the crypto market trend in the second half of the year

Looking ahead to the second half of 2025, the crypto market will enter a critical turning point of macro and structural resonance. Its core variable is no longer just a single price fluctuation or local theme speculation, but a dynamic game between multi-dimensional macro paths, institutional certainty, and on-chain structural reconstruction. Judging from the currently known policies and on-chain signals, the evolution of the crypto market is approaching a repricing window: the revision of existing policy expectations, the repricing of the actual interest rate environment, and the reshaping of investors risk pricing models will jointly constitute the main line logic of market fluctuations and trends in the next 6 to 9 months.

From a macro policy perspective, the Feds interest rate path and marginal changes in US dollar liquidity will continue to be the global decisive force. The current tone of late interest rate cuts and slow pace has been widely accepted by the market, but with the marginal loosening of the US labor market, the decline in corporate investment willingness, and indicators such as CPI and PCE showing potential signs of deflation, the probability of the Fed entering the symbolic interest rate cut or even preventive interest rate cut channel is increasing. Once the Fed makes its first interest rate cut in the middle of the year to the beginning of the third quarter, even a small attempt of 25 bps may quickly trigger the sentiment amplification effect in the crypto market. Historical experience shows that in the early stages of each round of liquidity release, the elasticity of crypto assets is often higher than that of traditional risky assets because they are essentially pure liquidity trading targets. Therefore, once the interest rate cut start signal is confirmed, the market may see a script similar to the first rise in logical assets, then spread of theme rotation after Q3 2020.

However, risks cannot be ignored. The uncertainty brought by the global political cycle will continue to overshadow the logic of asset pricing. The US presidential election, the redistribution of power in the European Parliament, the trend of financial decoupling between Russia and the West, and the new round of trade games between China and the United States may cause periodic disturbances to investors risk preferences and capital flows. In particular, if Trump wins the election, his extreme policy tendencies such as technology control, weaponization of the US dollar, and strategic reserves of Bitcoin may be good for Crypto in the short term, but the geopolitical shocks and financial decoupling risks behind it may also trigger the risk re-rating of the global capital system. Therefore, the entire second half of the crypto market will be dominated by the scissors gap of moderate macroeconomic easing and high geopolitical uncertainty, presenting a fluctuating upward pattern of pulse rise-policy suppression-structural rotation.

From the perspective of market structure, the current round of the crypto market is entering the mid-to-late stage of ETF funds dominate, on-chain structure stabilizes, and theme rotation slows down. Bitcoin spot ETF has become the dominant incremental force in the market, and its net inflow rhythm almost directly determines the BTC price trend. Although the ETF inflow data slowed down in May and June, the long-term structure has not reversed, but instead shows that mainstream institutional funds are waiting for a better allocation point. At the same time, the on-chain structure has gradually stabilized. The de-liquidation of chip distribution under the dominance of LTH, the active repair of stablecoins as on-chain payment and deployment tools, and the continued expansion of the DeFi ecosystem under a low leverage state all indicate that the crypto market is forming a more resilient internal operating system. Once the macro environment cooperates, the elastic release of the structure will be much higher than the previous speculation-dominated cycle.

But it is worth noting that the rotation of themes is slowing down significantly. From the end of 2024 to the beginning of 2025, hot topics such as AI+Crypto, RWA, and Meme 2.0 took turns to dominate market attention and capital focus, but after entering the middle and late 2025, the efficiency of capital inflows into theme projects has declined significantly, and the cycle of narrative conversion into price has become longer and the space has become narrower. Investors patience with theme speculation is weakening, and idle narratives are no longer sustainable. This means that the structural opportunities in the market in the second half of the year will focus more on the path of narrative verification supported by reality: such as the growth of real users of AI protocols, continuous optimization of BTC on-chain data, and the circulation data of stablecoins such as USDC exceeding expectations, etc., can truly drive the mid-term market.

From the perspective of tactical operation suggestions, the asset allocation level should pay more attention to the coordination of structure and rhythm. Bitcoin is still the most certain mainline asset, and the logic of long-term holding has not changed. It is suitable to continue to capture its valuation revaluation opportunities as digital gold in the interest rate cut cycle through the dual-track layout of ETF and cold wallet. Ethereum has game flexibility, but it is necessary to be vigilant about the loss of Alpha caused by the weakening of the innovation momentum of on-chain applications. It is recommended to focus on the sub-sectors of liquidity + new narrative in its ecosystem, such as RWA derivative agreements and L2 chain stablecoin growth. High-speed public chains such as Solana and TON have certain valuation repair space, but the participating positions and rhythm should be strictly controlled to cope with the possible volatility risks of liquidity ebb.

In addition, it is recommended to use a certain proportion of positions to strategically capture the secondary rotation potential of Meme assets. Although the strength of Meme narratives has dropped significantly, the short-term sentiment trading opportunities based on the resonance of X platform traffic and liquidity have not been completely extinguished. For users who are familiar with on-chain fund flow monitoring, they can combine data such as SocialFi, cross-chain bridge traffic changes, and whale address changes to conduct light combat operations at the intraday or weekly level. On this basis, strengthen the risk management mechanism to ensure that the Meme configuration does not exceed 10% of the total market value of the portfolio.

Finally, from the perspective of institutional and strategic research, the second half of 2025 is more suitable for building a defensive bull market framework rather than aggressive bull market expectations. Although the market has upward momentum, its external variables are too complex, and any external policy, war shock or regulatory reversal may constitute a reverse squeeze on the market direction. Therefore, it is recommended to focus on the following three indicators as leading signals for the phased shift of the crypto market: First, the changes in the Feds policy path and dot plot, whether to release expectations of continuous interest rate cuts; second, whether ETF fund flows are re-enlarged, especially whether the average daily net inflow returns to more than US$500 million; third, the changes in the on-chain circulation and activity of stablecoins (especially USDC and USDe), whether they can maintain the monthly growth trend and break through the 2024 high. Once the three resonate, it will constitute a confirmation signal for the market to transition to the trend repricing stage, and the upward slope of the subsequent market is expected to increase significantly.

In the second half of 2025, the crypto market will enter a mid-term repair cycle of structural precipitation turning to policy-driven. Although the market trend is not absolutely unilateral, under the combined forces of macro warming, on-chain optimization and capital rotation repair, the crypto market has the strategic foundation to achieve a slow bull breakthrough in range fluctuations. The key lies in whether investors can understand the rhythm of macro changes, anchor the trend of on-chain data, and thus build a long-term strategic layout with a high winning rate in fluctuations and tug-of-war.

VI. Conclusion

In 2025, the crypto market will enter a new cycle dominated by institutional games and guided by liquidity reconstruction. We recommend that investors take finding structural opportunities in defense as the core strategy line and grasp the new Alpha path brought about by the reconstruction of US monetary tools and the recovery of the Sino-US capital arbitrage chain. Patience will be the most powerful strategy this year, and understanding the system is the real skill to cross the cycle.